|

市場調査レポート

商品コード

1624594

ラテンアメリカの医薬品包装:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Latin America Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ラテンアメリカの医薬品包装:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

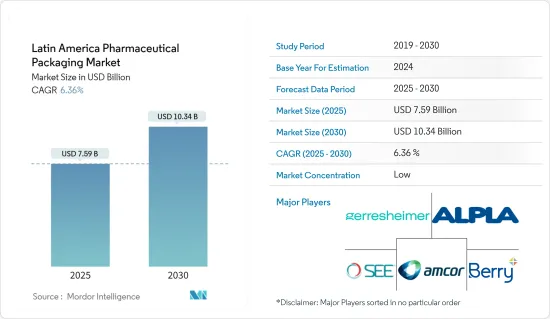

ラテンアメリカの医薬品包装市場規模は2025年に75億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.36%で、2030年には103億4,000万米ドルに達すると予測されます。

主なハイライト

- 医薬品包装は、ライフサイクルを通じて医薬品の提示、保護、識別、封じ込めに極めて重要です。製品が消費されるまでの間、規制基準へのコンプライアンスを確保しつつ、保管、輸送、陳列を容易にします。適切な包装は、気候、生物学的、物理的、化学的条件を含む様々な環境要因から医薬品を保護します。最適であるためには、医薬品包装は費用対効果が高く、製品の保存期間を通じて十分な安定性を提供しなければならないです。包装材料と製品タイプの選択は、医薬品特有の性質に基づき、選択された包装が適切な保護と明確な識別を提供し、封入された医薬品の完全性を維持することを保証します。

- ラテンアメリカの医薬品包装業界は、同地域の経済成長と都市化によって需要が増加しています。継続的な医療を必要とする高齢者人口が増加していることも、この動向に拍車をかけています。医薬品製造部門が勢いを増すにつれ、同地域の包装ベンダーは市場の大きな潜在力を活用できるようになります。海外からの投資、現地生産の増加、新製品開発は、この地域の包装業界の成長に貢献しています。その結果、ラテンアメリカはまもなく医薬品包装の主要市場であり続けると予想されます。

- ラテンアメリカの医薬品産業は、同地域最大かつ最も資本集約的なセクターのひとつです。研究開発(R&D)は、革新的な医薬品の開発において重要な役割を果たしており、過去20年間、ラテンアメリカの平均寿命の延伸に貢献してきました。この研究開発への注力は、治療法や治療法の大幅な進歩につながり、この地域特有のさまざまな健康課題に対処しています。

- 従来、ラテンアメリカの医薬品市場を独占してきたのは、西欧と米国の大手多国籍企業でした。これらの老舗企業は、広範な資源、世界な研究ネットワーク、高度な製造能力を活用し、この地域で強い存在感を維持してきました。しかし近年、業界への新規参入によって情勢が変わり始めています。

- これらの新規参入企業には、中国、インド、韓国の多国籍企業が含まれ、異なる医薬品開発・製造アプローチをもたらしています。さらに、ラテンアメリカの発展途上国からも、ジェネリック医薬品やニッチな治療領域に特化した地元企業が台頭しています。このように市場参入企業が多様化することで、競合が増加し、イノベーションが促進され、ラテンアメリカの人々の医薬品へのアクセスが改善される可能性があります。ラテンアメリカの医薬品情勢の変化は、既存企業や新興企業にとってチャンスであると同時に課題でもあります。市場が開拓を続ける中、規制環境、知的財産権、ヘルスケア政策などの要因が、この地域における業界の将来を大きく左右することになるでしょう。

- ラテンアメリカ製薬工業協会(ALIFAR)は、政府や政府間機関とは独立して活動する非営利の国際組織です。ラテンアメリカ全域の国営製薬会社を代表しています。ALIFARの会員は、ラテンアメリカ12カ国から400社を超え、この地域の医薬品市場の90%以上を占めています。ALIFARは、会員企業の利益を擁護し、ラテンアメリカの製薬産業の開発を促進する上で重要な役割を果たしています。ALIFARは、会員間の協力関係を促進し、ベストプラクティスを共有し、この地域の製薬業界が直面する共通の課題に取り組んでいます。

- ラテンアメリカにおける医薬品需要の増加は、人口増加、平均寿命の伸び、慢性疾患の増加によってもたらされています。こうした需要と製薬業界の技術進歩は、ボトル、アンプル、その他の容器などのパッケージング・ソリューションに対するニーズの高まりに直結しています。その結果、ラテンアメリカの医薬品包装市場は大きな成長を遂げました。包装材料や包装ソリューションのメーカーは、医薬品の安定性、安全性、規制基準への準拠など、業界の進化する要件を満たすために適応する必要がありました。

- 医薬品包装原材料に関連する環境問題への懸念は市場を制限する可能性があるが、同時にこの地域の製薬業界における包装技術革新の機会にもなります。持続可能性への注目が高まるにつれ、従来の包装材料に対する監視の目が厳しくなり、メーカーは環境に優しい代替品を模索するようになっています。このシフトはコストと規制遵守の課題をもたらすが、環境に配慮した新しい包装ソリューション開発の道も開く。

- 企業は、生分解性材料の開発、プラスチック使用量の削減、医薬品包装のリサイクル性向上のための研究開発に投資しています。このような取り組みは、環境への懸念に対応し、消費者の嗜好の変化や規制要件に沿ったものです。その結果、業界では環境への影響を最小限に抑えながら製品の完全性を維持する革新的な包装設計が急増しており、先進的な企業にとっては新たな市場セグメントと競争上の優位性を生み出す可能性があります。

ラテンアメリカ医薬品包装市場の動向

プラスチックボトルが大きな市場シェアを占める

- プラスチックはその汎用性、耐久性、柔軟性、持続可能性により、医薬品包装に広く使用されています。医薬品包装には、ポリ塩化ビニル、ポリエチレン、ポリプロピレン、ポリスチレンなど、さまざまな素材のプラスチックボトルが使用されています。この業界では、透明で耐久性があり、軽量なプラスチックを保管や流通に利用しています。これらのプラスチック素材は、割れにくい、様々な形やサイズに成形しやすい、様々な医薬品に適合する、などの利点があります。

- さらに、プラスチック包装は湿気、光、汚染物質から医薬品を保護し、製品の完全性を確保し、保存期間を延ばすのに役立ちます。医薬品包装にプラスチックを使用することは、一般的にガラスや金属のような代替材料よりも軽量で経済的であるため、製造や輸送における費用対効果にも貢献します。

- プラスチックボトルは、シロップ、カプセル、錠剤、眼科用剤など、様々な液体・固形医薬品の包装に広く利用されています。製薬業界がプラスチック包装を好むのは、その強度、軽量性、柔軟性によるもので、多様な形状やサイズに対応できます。医薬品用プラスチックボトル市場は、技術の進歩や経口固形・液体医薬品用プラスチック容器の採用増加により拡大しています。

- 医薬品用途のプラスチックは、毒性がなく、発がん性がなく、生体適合性があり、生体環境に無害でなければならないです。これらの厳しい要件は、医薬品の安全性と有効性を保証するものです。医薬品の開発プロセスでは、PET包装材が医薬品に溶出・抽出されないかどうかの厳しい試験が行われます。この試験は、包装と医薬品の内容物との間の汚染や相互作用を防ぐために非常に重要です。PETボトルは効果的なオイルバリアを提供し、輸送中に化学物質がこぼれないようにします。このバリア特性は、液体医薬品の完全性を維持し、外部からの汚染を防ぐために重要です。さらに、PET包装は耐久性と破損に対する抵抗力を備えており、様々な取り扱いや輸送条件にさらされる可能性のある医薬品容器にとって不可欠な品質です。

- 医薬用プラスチックボトルの需要は増加しており、ラテンアメリカのプラスチックボトル市場評価に影響を与えています。2023年、ラテンアメリカとカリブ海諸国からの医薬品輸出額の合計は約93億米ドルに達し、分析期間中、この地域の医薬品輸出額で最高レベルを記録しました。2022年には、メキシコが医薬品輸出額でラテンアメリカ諸国をリードしています。さらに、固形容器の成長は、栄養素を含む医薬品の採用増加により助長される可能性があると予測されています。人体の栄養バランスを維持するための栄養強化に対する社会人の意識の高まりは、栄養補助食品の消費を促進し、同地域のプラスチックボトル需要を促進すると予想されます。

- 目の疾患を持つ人は一般的にスポイトボトルを使用します。これらの特殊な容器は、眼科の薬や溶液を正確に投与することを可能にします。Gerresheimerのような企業は、固形、液体、眼科用製品など様々な用途の医薬品プラスチック包装を提供しています。同社の製品群には、液体製剤や点眼液用のPETボトルが含まれます。これらのボトルは、眼科用医薬品の保存と調剤、適切な投与量の確保、製品の完全性の維持に関する特定の要件を満たすように設計されています。眼科用途でのスポイトボトルの使用は、この地域で眼に関連する疾患の有病率が上昇し続けていることから、ますます重要になってきています。

著しい成長が期待されるメキシコ

- メキシコはラテンアメリカの医薬品市場シェアに大きく貢献しています。同地域の医薬品産業の成熟市場であるメキシコでは、特に医薬品包装において数多くの製品イノベーションが起きています。この技術革新の原動力となっているのは、メキシコ全土に存在する大規模なベンダーです。メキシコの医薬品市場は、強固なヘルスケアシステムとジェネリック医薬品およびブランド医薬品に対する需要の増加に支えられ、着実に成長しています。

- 同国の戦略的立地とNAFTA(現USMCA)などの貿易協定により、地域の医薬品事情における重要なプレーヤーとしての地位はさらに高まっています。最近の動向として、メキシコでは医薬品の研究開発活動が活発化しており、国内外の企業が現地施設に投資しています。これにより、高品質で費用対効果の高い医薬品の生産が増加し、ラテンアメリカ医薬品市場におけるメキシコの地位はさらに強固なものとなっています。

- メキシコの製薬産業における包装部門は、特にダイナミックです。この分野の技術革新は、医薬品の安全性の向上、保存期間の延長、患者のコンプライアンス強化に重点を置いています。こうした先進パッケージングには、インテリジェントなパッケージング・ソリューション、環境に優しい素材、さまざまな患者グループのニーズに応えるデザインなどが含まれます。規制の複雑さや他の新興市場との競合といった課題にもかかわらず、メキシコの製薬業界は進化と適応を続けています。技術革新へのコミットメントと確立された製造能力により、メキシコはラテンアメリカ医薬品市場における継続的な成長と影響力において有利な立場にあります。

- メキシコのヘルスケア産業は主に価格主導型であり、国産品は政府販売において価格優位性を持っています。企業は、品質を確保するためにすべての衛生登録基準を遵守しなければならないです。外資系企業は、コスト削減策を検討し、マーケティングや販促資料で新技術の利点を強調すべきです。2023年、メキシコの医薬品売上高は約108億3,000万米ドルに達し、2022年の101億2,000万米ドルから増加します。この地域の医薬品生産の拡大、市販薬の利用可能性の増加、地元企業による多額の投資が、ブラジルの医薬品セクターの大幅な成長に寄与しています。これらの動向は、輸出の増加とともに、全国的な医薬品包装需要の増加につながると予想されます。

- ヘルスケア費用の増加や、病院や製薬メーカーなどのエンドユーザーの間での嗜好の高まりは、予測期間中にメキシコでの製品使用を促進すると予想されます。バイアルは、他のガラス容器と同様にリサイクルが容易で、環境に優しいと考えられています。同国の医療・ヘルスケア分野では、エンドユーザーが従来の容器からバイアルに移行したことにより、これらの製品に対する有利な需要が発生しています。

ラテンアメリカの医薬品包装業界の概要

ラテンアメリカの医薬品包装市場は、既存企業が技術革新と買収に注力しているため、断片化しています。Amcor Group GmbH、Berry Global Inc.、Schott AG.などの企業は、新製品を革新し、環境に対応し、政府のコンプライアンスを確保するために、研究開発に多くの資源と資金を投入しています。

- 2024年5月- ドイツを拠点とする医薬品・ヘルスケア包装専門企業のゲレスハイマーは、メキシコのケレタロにある施設を拡張する予定です。この拡張は、RTF(Ready-to-Fill)注射器の生産能力を増強し、北米市場の高級注射器需要に対応することを目的としています。これらのプレフィラブルガラスシリンジは、肥満管理用グルカゴン様ペプチド-1製剤を含む注射用バイオ医薬品用に設計されています。この拡張は2023年11月の起工式で始まり、ゲレスハイマーはこのプロジェクトに約1億ユーロ(1億600万米ドル)の投資を行う。

- 2023年11月- アムコーは、ポリエチレンの流れでリサイクル可能なオールフィルム医療用包装を作るため、モノPEラミネートを導入しました。この技術革新により、患者の安全性を確保しつつ、パッケージの二酸化炭素排出量を削減できると報告されています。このフィルムは、ドレープ、保護材、カテーテル、注射・チューブシステムなどを収納する3D熱成形パッケージのリサイクル対応蓋を可能にすると期待されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場力学

- 市場促進要因

- 国内医薬品生産の増加

- 地域の医薬品・包装分野への直接投資の増加

- 市場抑制要因

- 医薬品包装原材料に関する環境問題

- 原材料価格の変動

第6章 市場セグメンテーション

- 包装材料別

- プラスチック

- ガラス

- 金属

- 紙

- 製品タイプ別

- ブリスターパック

- プラスチックボトル

- プレフィラブルシリンジ

- バイアルとアンプル

- 閉鎖容器

- 容器

- その他の製品タイプ

- 国別

- ブラジル

- メキシコ

- コロンビア

- アルゼンチン

第7章 競合情勢

- 企業プロファイル

- Amcor Group GmbH

- Sealed Air Corporation

- Berry Global Inc.

- Schott AG

- Gerresheimer AG

- Aptar Group Inc.

- ALPLA Werke Alwin Lehner GmbH & Co KG

- Pretium Packaging

- Silgan Holdings Inc.

- Greiner Packaging International GmbH

第8章 投資分析

第9章 市場の将来

The Latin America Pharmaceutical Packaging Market size is estimated at USD 7.59 billion in 2025, and is expected to reach USD 10.34 billion by 2030, at a CAGR of 6.36% during the forecast period (2025-2030).

Key Highlights

- Pharmaceutical packaging is crucial in drug product presentation, protection, identification, and containment throughout their lifecycle. It facilitates storage, transport, and display while ensuring compliance with regulatory standards until the product is consumed. Adequate packaging shields the drug from various environmental factors, including climatic, biological, physical, and chemical conditions. To be optimal, pharmaceutical packaging must be cost-effective and provide adequate stability throughout the product's shelf life. The selection of packaging materials and types is based on the specific nature of the drug, ensuring that the chosen packaging offers appropriate protection and clear identification and maintains the integrity of the enclosed pharmaceutical product.

- The pharmaceutical packaging industry in Latin America is experiencing increased demand driven by the region's expanding economies and urbanising population. The growing elderly demographic requiring continuous medical care further fuels this trend. As the pharmaceutical manufacturing sector gains momentum, packaging vendors in the region can capitalise on the market's significant potential. Foreign investments, rising local production, and new product development contribute to the growth of the regional packaging industry. Consequently, Latin America is expected to remain a key market for pharmaceutical packaging shortly.

- The pharmaceutical industry in Latin America stands as one of the region's largest and most capital-intensive sectors. Research and development (R&D) plays a crucial role in developing innovative drugs, contributing to increased life expectancy in Latin America over the past two decades, albeit at a high cost. This focus on R&D has led to significant advancements in medical treatments and therapies, addressing various health challenges specific to the region.

- Traditionally, large multinational companies from Western Europe and the United States have dominated the pharmaceutical market in Latin America. These established firms have leveraged their extensive resources, global research networks, and advanced manufacturing capabilities to maintain a strong regional presence. However, in recent years, the landscape has begun to shift with the entry of new players into the industry.

- These new entrants include multinational companies from China, India, and South Korea, bringing different drug development and manufacturing approaches. Additionally, local firms from several developing countries within Latin America have emerged, often focusing on generic drugs or niche therapeutic areas. This diversification of market participants has led to increased competition, potentially driving innovation and improving access to medicines for Latin American populations.The evolving pharmaceutical landscape in Latin America presents opportunities and challenges for established and emerging companies. As the market continues to develop, factors such as regulatory environments, intellectual property rights, and healthcare policies will significantly shape the industry's future in the region.

- ALIFAR, the Latin American Association of Pharmaceutical Industries, is a non-profit international organisation operating independently from governmental and intergovernmental bodies. It represents nationally owned pharmaceutical companies across Latin America. ALIFAR's membership encompasses over 400 companies from 12 Latin American countries, accounting for over 90% of the region's pharmaceutical market. The organization plays a crucial role in advocating for the interests of its member companies and promoting the development of the pharmaceutical industry in Latin America. ALIFAR works to foster collaboration among its members, share best practices, and address common challenges faced by the industry in the region.

- The growing demand for pharmaceutical drugs and medicines in Latin America has been driven by population growth, increasing life expectancy, and a rising prevalence of chronic diseases. This demand and technological advancements in the pharmaceutical industry have directly led to an increased need for packaging solutions such as bottles, ampules, and other containers. The pharmaceutical packaging market in Latin America has consequently experienced significant growth. Manufacturers of packaging materials and solutions have had to adapt to meet the industry's evolving requirements, including considerations for drug stability, safety, and compliance with regulatory standards.

- Environmental concerns related to pharmaceutical packaging raw materials may limit the market but also provide opportunities for innovation in packaging within the pharmaceutical industry in the region. The increasing focus on sustainability has heightened scrutiny of traditional packaging materials, prompting manufacturers to explore eco-friendly alternatives. This shift presents cost and regulatory compliance challenges but also opens avenues for developing novel, environmentally responsible packaging solutions.

- Companies are investing in research and development to create biodegradable materials, reduce plastic usage, and improve the recyclability of pharmaceutical packaging. These efforts address environmental concerns and align with changing consumer preferences and regulatory requirements. As a result, the industry is witnessing a surge in innovative packaging designs that maintain product integrity while minimising environmental impact, potentially creating new market segments and competitive advantages for forward-thinking companies.

Latin America Pharmaceutical Packaging Market Trends

Plastic Bottles to Hold Significant Market Share

- Plastic is widely used in pharmaceutical packaging due to its versatility, durability, flexibility, and sustainability. Pharmaceutical packaging employs plastic bottles made from various materials, including polyvinyl chloride, polyethene, polypropylene, and polystyrene. The industry utilises transparent, durable, lightweight plastic for storage and distribution. These plastic materials offer several advantages, such as resistance to breakage, ease of moulding into various shapes and sizes, and compatibility with a wide range of pharmaceutical products.

- Additionally, plastic packaging helps protect medications from moisture, light, and contaminants, ensuring product integrity and extending shelf life. The use of plastic in pharmaceutical packaging also contributes to cost-effectiveness in manufacturing and transportation, as it is generally lighter and more economical than alternative materials like glass or metal.

- Plastic bottles are extensively utilised for packaging various liquid and solid medicines, including syrups, capsules, tablets, and ophthalmic preparations. The pharmaceutical industry favours plastic packaging due to its strength, lightweight nature, and flexibility, allowing for diverse forms and sizes. The market for pharmaceutical plastic bottles has expanded, driven by technological advancements and the increased adoption of plastic containers for oral solid and liquid medications.

- Plastics in pharmaceutical applications must be non-toxic, non-carcinogenic, biocompatible, and harmless to the biological environment. These stringent requirements ensure the safety and efficacy of pharmaceutical products. The drug development process includes rigorous testing of PET packaging for leaching and extractability in conjunction with the drug. This testing is crucial to prevent contamination or interaction between the packaging and the pharmaceutical contents. PET bottles provide an effective oil barrier, helping to resist chemical spills during transport. This barrier property is significant for maintaining the integrity of liquid medications and preventing contamination from external sources. Additionally, PET packaging offers durability and resistance to breakage, essential qualities for pharmaceutical containers that may be subject to various handling and transportation conditions.

- The demand for pharmaceutical plastic bottles has increased, impacting the market valuation of plastic bottles in Latin America. In 2023, the combined value of pharmaceutical exports from Latin America and the Caribbean reached approximately USD 9.3 billion, marking the region's highest level of pharmaceutical exports during the analyzed period. In 2022, Mexico led Latin American countries in pharmaceutical export value.Further, it is anticipated that the growth of solid containers may be aided due to the increased adoption of medicines containing nutrients. The increasing awareness of nutritional enrichment among working professionals for maintaining balanced nutrition in the human body is anticipated to promote the consumption of dietary supplements and drive demand for plastic bottles in the region.

- Individuals with eye conditions commonly use dropper bottles. These specialised containers allow for the precise administration of eye medications and solutions. Companies like Gerresheimer provide pharmaceutical plastic packaging for various applications, including solid, liquid, and ophthalmic products. Their product range includes PET bottles for liquid dosage forms and ophthalmic solutions. These bottles are engineered to meet specific requirements for preserving and dispensing eye medications, ensuring proper dosage and maintaining product integrity. The use of dropper bottles in ophthalmic applications has become increasingly important as the prevalence of eye-related disorders continues to rise in the region.

Mwxico is Expected to Witness Significant Growth

- Mexico is a significant contributor to the pharmaceutical market share in Latin America. As a mature market in the region's pharmaceutical industry, Mexico has experienced numerous product innovations, particularly in pharmaceutical packaging. This innovation is driven by the presence of significant vendors throughout the country. The Mexican pharmaceutical market has grown steadily, supported by a robust healthcare system and increasing demand for generic and branded medications.

- The country's strategic location and trade agreements, such as NAFTA (now USMCA), have further enhanced its position as a critical player in the regional pharmaceutical landscape. In recent years, Mexico has seen a rise in pharmaceutical research and development activities, with domestic and international companies investing in local facilities. This has increased the production of high-quality, cost-effective medications, further solidifying Mexico's position in the Latin American pharmaceutical market.

- The packaging sector within Mexico's pharmaceutical industry has been particularly dynamic. Innovations in this area have focused on improving drug safety, extending shelf life, and enhancing patient compliance. These advancements include intelligent packaging solutions, eco-friendly materials, and designs catering to different patient groups' needs. Despite challenges such as regulatory complexities and competition from other emerging markets, Mexico's pharmaceutical industry continues to evolve and adapt. The country's commitment to innovation and established manufacturing capabilities position it well for continued growth and influence in the Latin American pharmaceutical market.

- The Mexican healthcare industry is primarily price-driven, with domestically produced goods having a pricing advantage in government sales. Businesses must comply with all sanitary registration standards to ensure quality. Foreign companies should consider cost-cutting measures and highlight the benefits of new technology in their marketing and promotional materials. In 2023, Mexico's pharmaceutical product sales reached approximately USD 10.83 billion, an increase from USD 10.12 billion in 2022. The region's expanding pharmaceutical production, increased availability of over-the-counter medicines, and significant investments by local businesses contribute to the substantial growth of the Brazilian pharmaceutical sector. These trends are expected to lead to an increase in pharmaceutical packaging demand nationwide, along with growing exports.

- The increasing cost of healthcare and the growing preference among end-users such as hospitals and pharmaceutical manufacturers are expected to drive product usage in Mexico during the forecast period. Vials, like other glass containers, are easily recyclable and considered environmentally friendly. The medical and healthcare sectors in the country are experiencing a lucrative demand for these products due to end-users' shift from conventional containers to vials.

Latin America Pharmaceutical Packaging Industry Overview

The pharmaceutical packaging market in Latin America is fragmented, as established companies focus on innovation and acquisition. Companies like Amcor Group GmbH, Berry Global Inc., Schott AG. invest a lot of their resources and money in Research and development to innovate new products, meet with the environment, and ensure government compliance.

- May 2024 - Gerresheimer, a Germany-based company specialising in pharmaceutical and healthcare packaging, is set to expand its facility in Queretaro, Mexico. This expansion aims to boost production capacities for ready-to-fill (RTF) syringes, addressing the North American market's demand for premium syringes. These prefillable glass syringes are designed for injectable biopharmaceuticals, including glucagon-like peptide-1 drugs for obesity management. The expansion started with a ground-breaking ceremony in November 2023, and Gerresheimer is channelling an investment of around EUR 100 million (USD 106 million) into the project.

- November 2023 - Amcor has introduced a mono-PE laminate to create all-film medical packaging recyclable in the polyethylene stream. This innovation reportedly reduces the package's carbon footprint while ensuring patient safety. The film is expected to enable recycle-ready lidding for 3D thermoformed packages, which house items like drapes, protective materials, catheters, and injection and tubing systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Domestic Pharmaceuticals Production

- 5.1.2 Growing FDI In regional pharmaceutical and packaging sector

- 5.2 Market Restraints

- 5.2.1 Environmental Concerns related to Pharmaceutical Packaging Raw Materials

- 5.2.2 Fluctuations In Raw Material Prices

6 MARKET SEGMENTATION

- 6.1 By Packaging Material

- 6.1.1 Plastic

- 6.1.2 Glass

- 6.1.3 Metal

- 6.1.4 Paper

- 6.2 By Product Type

- 6.2.1 Blister Packs

- 6.2.2 Plastic Bottles

- 6.2.3 Prefillable Syringes

- 6.2.4 Vials and Ampuls

- 6.2.5 Closures

- 6.2.6 Containers

- 6.2.7 Other Product Types

- 6.3 By Country

- 6.3.1 Brazil

- 6.3.2 Mexico

- 6.3.3 Columbia

- 6.3.4 Argentina

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Sealed Air Corporation

- 7.1.3 Berry Global Inc.

- 7.1.4 Schott AG

- 7.1.5 Gerresheimer AG

- 7.1.6 Aptar Group Inc.

- 7.1.7 ALPLA Werke Alwin Lehner GmbH & Co KG

- 7.1.8 Pretium Packaging

- 7.1.9 Silgan Holdings Inc.

- 7.1.10 Greiner Packaging International GmbH