|

|

市場調査レポート

商品コード

1624582

中国のプラスチック包装:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)China Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のプラスチック包装:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

中国のプラスチック包装市場規模は、出荷量ベースで2025年の1,514万トンから2030年には1,865万トンに拡大し、予測期間(2025~2030年)のCAGRは4.26%と予測されます。

中国では、消費者意識の高まりと製造業の急成長がプラスチック包装市場の拡大を牽引しています。この成長は、急増する食品産業と盛んな包装部門によってさらに促進されます。

主なハイライト

- 中国は、プラスチックの主要生産国としても消費国としても、世界の舞台で圧倒的な存在感を示しています。中国がプラスチックの生産と輸出に力を入れるようになったのは、PET(ポリエチレンテレフタレート)、HDPE(高密度ポリエチレン)、その他のポリマーベースのボトルや容器への依存度が高まったことが主な原因です。これらの素材は、飲食品、医薬品、パーソナルケアなどの分野で極めて重要です。

- 中国を筆頭とするアジアのボトル入り飲料水に対する需要の高まりが、プラスチック市場を牽引しています。国連機関である国連大学水・環境・健康研究所のデータは、この動向を浮き彫りにしており、アジア太平洋諸国がボトル入り飲料水の消費量の大半を占めていることを明らかにしています。米国に次いで世界第2位のボトル入り飲料水市場である中国は、PETプラスチックの需要をさらに増大させています。

- 環境に優しい製品に対する需要の急増に対応して、中国のメーカーは持続可能なパッケージングに向けて顕著な方向転換を図っています。例えば、2024年5月、中国に進出しているオーストリアのAlpla Werke Alwin Lehner GmbH &Co KGは、リサイクル可能なPETワインボトルを発表しました。この革新的なボトルは、従来のガラス製に比べ炭素消費量を38%削減するだけでなく、同社の環境面での信頼性も高めています。

- しかし、市場は代替パッケージング・ソリューションへのシフトの高まりという課題に直面しています。世界の廃棄物や海洋ゴミの重大な原因となっているプラスチック汚染との中国の戦いは、環境問題を浮き彫りにしています。世界トップのプラスチック生産国・消費国である中国は、特に紙パッケージのような代替品への消費者のシフトが顕著であるため、市場の成長が危機に瀕しています。

中国のプラスチック包装市場の動向

食品産業が市場を独占する見込み

- 国家統計局(NBS)の報告によると、2023年の中国の国内総生産(GDP)は17兆5,200億米ドル(126兆600億元)に達し、前年比5.2%増を記録しました。米国農務省(USDA)は、世界最大の食料輸入国である中国の食料輸入総額が2023年には1,400億米ドルを超えると強調しました。

- 中国における消費者の嗜好の変化、特に包装食品の増加傾向は、プラスチック包装の需要増加を促しています。米国農務省は、中国の食品市場における重要な動向は急成長するeコマース部門であると指摘しています。予測によると、中国の食品eコマース市場は2024年に1,480億米ドルに達し、硬質プラスチック包装ソリューションの需要をさらに促進します。

- さらに、中国の外食産業は2023年に、特に調理済み食品分野で力強い復活を遂げました。オン・ザ・ゴー食品消費の増加は、硬質および軟質プラスチック包装ソリューションの使用に拍車をかけています。この動向は、中国における持ち帰り食品産業の活況によってさらに増幅され、プラスチック包装に対する需要の高まりにつながっています。

- 中国の食品輸入には、乳製品、加工食品、食肉(特に牛肉に重点が置かれている)など、消費者向けのさまざまな製品が含まれます。米国農務省のデータによると、2023年の中国のこれら消費者向け製品の輸入総額は1,064億米ドルに上ります。中国への主要輸出国であるニュージーランド、タイ、ブラジル、米国はそれぞれ10~12%のシェアを占めており、中国のプラスチック包装需要を牽引する上で極めて重要な役割を果たしています。

ボトルと瓶が最も高い市場シェアを占める。

- ポリエチレンテレフタレート(PET)、ポリプロピレン(PP)、ポリエチレン(PE)は、包装ソリューション用のプラスチックボトルと瓶の生産に使われる主要材料です。これらの素材は軽量で割れにくく、マテリアルハンドリングが容易です。中国では、飲食品業界のボトルや瓶の需要が急増し、硬質プラスチック包装のニーズが急速に高まっています。具体的には、ペットボトル入り飲料水、ジュース、ソフトドリンク、医薬品、家庭用洗剤、パーソナルケア用品の包装にPETボトルの使用が増加していることが、プラスチック包装市場の拡大要因となっています。

- 中国で急成長している医薬品分野では、包装にPETボトルや容器を使用するケースが増えており、この分野の成長をさらに後押ししています。メディアプラットフォームであるPolicy Circleのデータによると、2023年から24年にかけて、中国はインドの医薬品輸入の43.45%を占め、プラスチック包装ソリューションの需要が高まっていることが明らかになっています。

- リサイクル可能で再利用可能な包装に対する消費者の嗜好の高まりを受けて、Amcor Groupのような中国メーカーは、飲料ボトルを含む持続可能な硬質包装ソリューションの発売を優先しています。2024年4月、スイスに本社を置き中国にも拠点を持つAmcor Groupは、炭酸清涼飲料用に特別に設計された、100%消費者再利用(PCR)材料のみで作られた1リットルペットボトルを発表しました。

- プラスチック製品製造の主要拠点として、中国は重要な生産マイルストーンを見てきました。ChemmAnalystの報告によると、2023年12月、中国のプラスチック製品生産量は約698万トンに達し、前年比2.8%増となった。特に、中国はプラスチック製品、特にボトルを米国やオーストラリア、マレーシア、日本を含むアジア諸国に輸出しています。

中国のプラスチック包装産業の概要

中国のプラスチック包装市場は断片的な様相を呈しています。Amcor Group、Berry Global Inc.、ALPLA Werke Alwin Lehner GmbH &Co KG、Silgan Holdings Inc.、Shangdong Haishengyu Plastic Industryなどの主要企業は、市場でより大きなシェアを獲得しようと、積極的に製品ポートフォリオを強化しています。これらの企業は、中国市場での優位性を主張するために、M&A、パートナーシップ、事業拡大、新製品の発売、提携などの有機的戦略と無機的戦略を組み合わせて採用しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- 飲食品分野におけるプラスチック包装需要の急増

- 環境に優しい包装オプションの採用増加

- 市場の課題

- プラスチック包装に対する環境問題の高まり

第6章 業界の規制と政策と基準

第7章 市場内訳

- 包装タイプ別

- 軟質プラスチック包装

- 製品タイプ別

- パウチ

- 袋

- フィルム&ラップ

- その他の製品タイプ

- エンドユーザー産業別

- 食品

- 飲料

- ヘルスケア

- 化粧品・パーソナルケア

- 家庭用ケア

- その他のエンドユーザー産業(産業、eコマース、その他)

- 硬質プラスチック包装

- 製品タイプ別

- ボトルとジャー

- トレイと容器

- キャップ・クロージャー

- その他の製品タイプ

- エンドユーザー産業別

- 食品

- 飲料

- ヘルスケア

- 化粧品・パーソナルケア

- 家庭用ケア

- その他のエンドユーザー産業(産業、自動車、その他)

- 軟質プラスチック包装

第8章 競合情勢

- 企業プロファイル

- Shangdong Haishengyu Plastic Industry Co. Ltd

- ALPLA Werke Alwin Lehner GmbH & Co KG

- Amcor Group

- Berry Global Inc.

- Silgan Holdings Inc.

- Taizhou Huangyan Baitong Plastic Co. Ltd

- Shenyang Powerful Packing, Co., Ltd.

- Jieshou Tianhong New Material Co. Ltd

- Qingdao Haoyu Packing Co. Ltd

- Ningbo Kinpack Commodity Co. Ltd

第9章 リサイクルと持続可能性の展望

第10章 市場の将来

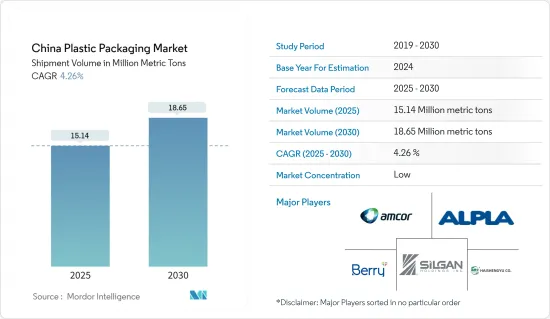

The China Plastic Packaging Market size in terms of shipment volume is expected to grow from 15.14 million metric tons in 2025 to 18.65 million metric tons by 2030, at a CAGR of 4.26% during the forecast period (2025-2030).

In China, heightened consumerism and a burgeoning manufacturing sector are driving the expansion of the plastic packaging market. This growth is further fueled by a surging food industry and a thriving packaging sector.

Key Highlights

- China is a dominant player on the global stage, both as a leading producer and consumer of plastic. The nation's intensified focus on plastic production and export is largely due to its heightened reliance on PET (Polyethylene Terephthalate), HDPE (High-Density Polyethylene), and other polymer-based bottles and containers. These materials are pivotal for sectors like food and beverage, pharmaceuticals, and personal care.

- Asia's rising appetite for bottled water, with China leading the charge, is propelling the plastic market. Data from the United Nations University Institute for Water, Environment and Health, a UN agency, underscores this trend, revealing that Asia-Pacific nations dominate bottled water consumption. China, as the world's second-largest bottled water market, only behind the United States, further amplifies the demand for PET plastics.

- Responding to the surging demand for eco-friendly products, Chinese manufacturers are making a notable pivot towards sustainable packaging. For instance, in May 2024, Alpla Werke Alwin Lehner GmbH & Co KG, an Austrian firm operating in China, unveiled a recyclable PET wine bottle. This innovative bottle not only slashes carbon consumption by 38% compared to traditional glass but also enhances the company's environmental credentials.

- However, the market faces challenges from a growing shift towards alternative packaging solutions. China's battle with plastic pollution, a significant contributor to global waste and marine debris, highlights the environmental stakes. As the world's top producer and consumer of plastic, China's market growth is at risk, especially with a noticeable consumer shift towards alternatives like paper packaging.

China Plastic Packaging Market Trends

Food Industry is Expected to Dominate the Market

- In 2023, China's gross domestic product (GDP) reached USD 17.52 trillion (126.06 trillion yuan), marking a year-on-year increase of 5.2%, as reported by the National Bureau of Statistics (NBS). The United States Department of Agriculture (USDA) highlighted that China, the world's largest food-importing nation, saw its total food import value exceed USD 140 billion in 2023.

- Shifting consumer preferences in China, especially the rising trend of packaged foods, are driving an increased demand for plastic packaging. The USDA notes that a significant trend in China's food market is the burgeoning e-commerce sector. Forecasts suggest that China's food e-commerce market will hit USD 148 billion in 2024, further fueling the demand for rigid plastic packaging solutions.

- Moreover, China's food service industry made a strong comeback in 2023, particularly in the prepared food segment. The uptick in on-the-go food consumption has spurred using rigid and flexible plastic packaging solutions. This trend is further amplified by the booming takeaway food industry in China, leading to a heightened demand for plastic packaging.

- China's food imports encompass a range of consumer-oriented products, including dairy, processed foods, and meat, with a notable emphasis on beef. USDA data reveals that in 2023, China's imports of these consumer-oriented products totaled USD 106.4 billion. Key exporters to China, New Zealand, Thailand, Brazil, and the United States each holding a 10-12% share, play a pivotal role in driving the nation's demand for plastic packaging.

Bottles and Jars Segment to Register Highest Market Share

- Polyethylene terephthalate (PET), polypropylene (PP), and polyethylene (PE) are the primary materials used in the production of plastic bottles and jars for packaging solutions. These materials are lightweight and unbreakable, enhancing their ease of handling. In China, the food and beverage industry's surging demand for bottles and jars is rapidly boosting the need for rigid plastic packaging. Specifically, the rising use of PET bottles for packaging bottled water, juices, soft drinks, medicines, household cleaners, and personal care items is a key driver of the plastic packaging market's expansion.

- China's burgeoning pharmaceutical sector is increasingly turning to PET bottles and containers for packaging, further fueling this segment's growth. Data from Policy Circle, a media platform, highlights that in 2023-24, China constituted 43.45% of India's pharmaceutical imports, underscoring the heightened demand for plastic packaging solutions.

- In response to the rising consumer preference for recyclable and reusable packaging, Chinese manufacturers such as Amcor Group prioritise launching sustainable rigid packaging solutions, including beverage bottles. In April 2024, Amcor Group, a Switzerland-based entity with a footprint in China, unveiled a one-liter PET bottle crafted entirely from 100% post-consumer recycled (PCR) content, specifically designed for carbonated soft drinks.

- As a leading hub for plastic product manufacturing, China has seen significant production milestones. ChemAnalyst reported that in December 2023, China's plastic product output reached around 6.98 million tons, marking a 2.8% increase from the previous year. Notably, China exports its plastic products, especially bottles, to the United States and several Asian nations, including Australia, Malaysia, and Japan.

China Plastic Packaging Industry Overview

The plastic packaging market in China exhibits a fragmented landscape. Key players, including Amcor Group, Berry Global Inc., ALPLA Werke Alwin Lehner GmbH & Co KG, Silgan Holdings Inc., and Shangdong Haishengyu Plastic Industry Co. Ltd., are actively enhancing their product portfolios in a bid to capture a larger share of the market. These companies are employing a mix of organic and inorganic strategies, such as mergers and acquisitions, partnerships, expansions, new product launches, and collaborations, to assert their dominance in the Chinese market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Surging Demand for Plastic Packaging in the Food and Beverage Sector

- 5.1.2 Increasing Adoption of Eco-Friendly Packaging Options

- 5.2 Market Challenges

- 5.2.1 Rising Environmental Concerns Over Plastic Packaging

6 INDUSTRY REGULATION, POLICY AND STANDARDS

7 MARKET SEGEMENTATION

- 7.1 By Packaging Type

- 7.1.1 Flexible Plastic Packaging

- 7.1.1.1 By Product Type

- 7.1.1.1.1 Pouches

- 7.1.1.1.2 Bags

- 7.1.1.1.3 Films & Wraps

- 7.1.1.1.4 Other Product Types

- 7.1.1.2 By End-User Industry

- 7.1.1.2.1 Food

- 7.1.1.2.2 Beverage

- 7.1.1.2.3 Healthcare

- 7.1.1.2.4 Cosmetics and Personal Care

- 7.1.1.2.5 Household Care

- 7.1.1.2.6 Other End-User Industries (Industrial, E-Commerce, Among Others)

- 7.1.2 Rigid Plastic Packaging

- 7.1.2.1 By Product Type

- 7.1.2.1.1 Bottles and Jars

- 7.1.2.1.2 Trays and Containers

- 7.1.2.1.3 Caps and Closures

- 7.1.2.1.4 Other Product Types

- 7.1.2.2 By End-User Industry

- 7.1.2.2.1 Food

- 7.1.2.2.2 Beverage

- 7.1.2.2.3 Healthcare

- 7.1.2.2.4 Cosmetics and Personal Care

- 7.1.2.2.5 Household Care

- 7.1.2.2.6 Other End-User Industries (Industrial, Automotive, Among Others)

- 7.1.1 Flexible Plastic Packaging

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Shangdong Haishengyu Plastic Industry Co. Ltd

- 8.1.2 ALPLA Werke Alwin Lehner GmbH & Co KG

- 8.1.3 Amcor Group

- 8.1.4 Berry Global Inc.

- 8.1.5 Silgan Holdings Inc.

- 8.1.6 Taizhou Huangyan Baitong Plastic Co. Ltd

- 8.1.7 Shenyang Powerful Packing, Co., Ltd.

- 8.1.8 Jieshou Tianhong New Material Co. Ltd

- 8.1.9 Qingdao Haoyu Packing Co. Ltd

- 8.1.10 Ningbo Kinpack Commodity Co. Ltd