|

市場調査レポート

商品コード

1550259

米国の軟質プラスチック包装:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)United States Flexible Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の軟質プラスチック包装:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

米国の軟質プラスチック包装市場規模は出荷量ベースで、2024年の508万トンから2029年には581万トンに、予測期間(2024-2029年)のCAGRは2.72%で成長すると予測されます。

主なハイライト

- 軟質プラスチック包装は、より経済的でカスタマイズ可能な製品包装オプションを可能にします。飲食品、パーソナルケア、製薬業界など、汎用性の高い包装を必要とする業界では特に有用です。高い効率性と費用対効果で人気が高まっています。この地域の政府機関は、二酸化炭素排出量とエネルギー消費量を削減するためのプロジェクトに資金を提供しており、これは市場に明るい展望をもたらす可能性があります。

- 米国エネルギー省(DOE)は、エネルギー消費量が少なく二酸化炭素排出量を最小限に抑えたプラスチックを生産するため、1,340万米ドルの資金を投じると発表しました。この投資は、金属廃棄物のリサイクル課題への対応に重点を置いています。軟包装は硬包装よりも材料消費量が少ないため、生産エネルギーが少なくて済み、二酸化炭素排出量の削減に役立ちます。このようなイニシアチブは、軟質プラスチック包装の持続可能な材料としてのバイオプラスチックの開発を促進し、リジッドパッケージングの経済的な代替品としてのフレキシブル・パッケージングを強調するのに役立つと思われます。

- テクノロジーを包装に統合する必要性は、バリア性の向上した包装材料に対する需要の高まり、製品の革新、サプライチェーンのデジタル化の進展によってもたらされます。この地域における食品原料市場の成長は、飲食品産業の成長、乳製品と冷凍乳製品の消費の増加、加工食品と包装食品の需要重視の高まりによってもたらされます。軟質プラスチック包装が一般的な包装材料です。持ち運びに適した食品包装への需要の高まりが、様々な産業で軟質プラスチック包装の使用を促進しています。

- パウチ包装は非常に便利で持ち運びに便利なソリューションであるため、急速に人気を集めています。今日の買い物客の多くは、従来の硬い包装よりも柔軟性のあるスタンドアップパウチを好んでいます。消費者は過去10年間、スタンドアップパウチ(スナック、飲食品、ベビーフード、工業用オイルや潤滑油)の需要を飛躍的に伸ばしました。パッケージング・タイプにおける特定のイノベーションが、市場の持続可能性をさらに後押ししています。

- 例えば、2023年11月、米国を拠点とする包装・材料科学のProAmpac社は、ProActive PCRレトルトパウチと呼ばれる従来のレトルト選択肢に代わる持続可能な選択肢を発表しました。このレトルトパウチは、新しいプラスチックの使用を削減し、重量比で最大30%の消費者使用後のリサイクル材料を組み込むように設計されています。これは、ブランドや小売業者が循環型経済目標を達成するのを支援することを目的としています。ProActive PCRレトルトパウチは、保存可能な調理済みタンパク質のように、優れたバリア性と耐熱性を必要とする製品向けに特別に調整されています。

- 市場プレーヤーは、顧客の高まるニーズを満たすために新製品開発に投資しています。例えば、2023年8月、TC Transcontinentalのパッケージング部門であるTC Transcontinental Packagingは、より耐熱性の高い高性能ポリエチレンフィルムを提供し、先進的なモノマテリアルリサイクル可能な軟質プラスチック包装ソリューションの開発に向けて6,000万米ドルの投資を発表しました。

- 地域のプレーヤーは、市場でのプレゼンスを拡大するために様々な包装会社を買収しています。例えば、2023年2月、SEEはLiquiboxを11億5,000万米ドルで買収したと発表しました。この戦略的投資により、軟包装業界の2つのプレーヤーが統合され、両社の高成長が実現しました。Liquibox社は、生鮮食品、飲食品、消費財、工業用エンドマーケット向けに、持続可能な液体・液体包装、ディスペンサー製品のバッグインボックスの革新と製造を行っています。この買収は、SEEの急成長部門であるCRYOVACブランドの液体・液体事業を加速させます。CRYOVACの技術、規模、市場アクセスは大きな相乗効果をもたらします。

米国の軟質プラスチック包装市場の動向

様々なエンドユーザー産業におけるパウチ包装の需要増加

- パウチは、米国の飲食品、化粧品、ベビーフード、医薬品、エナジードリンク分野で極めて重要な役割を果たしています。利便性に対する消費者の嗜好の高まりと中小企業による採用によって、軟質プラスチック包装市場、特にパウチ包装は大きな成長を遂げようとしています。パウチ包装の需要は、技術の先進化と消費者の嗜好の進化に後押しされ、様々な業界で急増しています。

- ファーストフードチェーン、オーガニック食品、ソフトドリンク、健康補助食品、菓子などを含む米国の飲食品分野は、国内のプラスチックパウチ包装の主要な牽引役となっています。全米菓子協会の報告書によると、米国の菓子売上高は2023年に480億米ドルに達し、2028年には610億米ドルに急増すると予測されています。

- 利便性と保護は、パウチ包装の人気を支える重要な原動力です。小さなものから大きなものまで、そのサイズの多様性により、化粧品業界、特に旅行・観光市場向けの製品に理想的です。さらに、米国の消費者の92%が購入時に鮮度を優先していることから、ポリマーパッケージングで強調されているように、明示的なフィルムを使用したスタンドアップパウチが大きな支持を得ています。

- また、イノベーションと製品開発がパウチ包装の展望を再構築しています。時間に追われる消費者が、電子レンジで簡単に調理できるクイックミールを好む中、メーカーは高度な機能性を備えたパウチを導入することで対応しています。代表的な例は、クラフト・ハインツが2023年に発売した、電子レンジで焼いたチーズをパリッとさせるパウチです。同社の特許技術である360クリスプ・テクノロジーを採用したこの動きは、製品ラインナップにおける革新の先駆者としての同社のコミットメントを示すものです。

- 米国では、消費者とメーカーによる持続可能なパッケージングへの需要が高まっています。メーカーは循環型経済モデルへの移行を進めており、環境に優しいパウチ包装の成長を後押ししています。このシフトはエコ・フレンドリーなパウチを後押しし、より広範なフレキシブル・プラスチック・パッケージング市場に影響を与えています。

- 持続可能な包装のトップメーカーであるAmcor Group GmbHは、オーガニックヨーグルトのトップメーカーであるStonyfield Organic社、スパウト付きパウチで知られるCheer Pack North America社と提携しました。彼らは、初のオールポリエチレン(PE)スパウトパウチを開発しました。この新しいデザインは、Stonyfield Organic社の古い多層パッケージに取って代わり、現在同社の冷蔵ヨーグルト「YoBaby」に使用されており、持続可能性への重要な一歩を示しています。

消費者のライフスタイルの変化に伴い、軟質プラスチック包装の需要が急増

- 食品から化粧品に至るまで、消費者製品は、便利で持ち運び可能なソリューションへの需要に後押しされ、フレキシブル包装への転換がますます進んでいます。このシフトは主に、ペースの速い都市型ライフスタイルに沿った包装の人気が高まっていることによる。

- 消費者が軽量で使いやすいパッケージを求める中、ベンダーは進化する小売情勢の中で競争力を維持するため、革新的なソリューションに軸足を移しています。フレキシブルパウチのような素材を採用することは、このような需要に応え、大幅な省エネのメリットを提供します。

- また、特に一人暮らしが普及するにつれて、電子レンジで温められる小分け食品への動向も高まっています。このシフトはコンビニエンスストアの小売業を強化し、より便利なパッケージング・ソリューションへのニーズを高めています。

- スーパーマーケットやハイパーマーケットは、ペースの速い現代社会における利便性への需要を認識し、簡単に持ち運べる選択肢を提供するようになっています。食品業界では、プラスチックパウチに入った調理済み食品が著しい成長を遂げています。これらのパウチは、完全に調理されたものから、お湯やヒーターで温め直したり、冷めても楽しめるものまで、様々な製品に対応しています。

- 米国国勢調査局のデータによると、スーパーマーケットと食料品店の売上高は顕著に増加しており、2022年の8,236億8,000万米ドルから2023年には8,463億8,000万米ドルに達します。このような堅調な売上高は、国内における軟包装への意欲の高まりを裏付けています。

- この市場の勢いを示すように、2024年1月、持続可能な包装の大手メーカーであるAccredo Packaging Inc.は、テキサス本社の4回目の拡張工事を完了し、1,000万米ドルを投資しました。8万3,000平方フィートのオフィススペースを追加したこの拡張は、リサイクル可能で堆肥化可能な持続可能な包装資材を生産し、スナック菓子、菓子類、焼き菓子などの多様な市場に対応するという同社のコミットメントを強調するものです。

米国の軟質プラスチック包装業界の概要

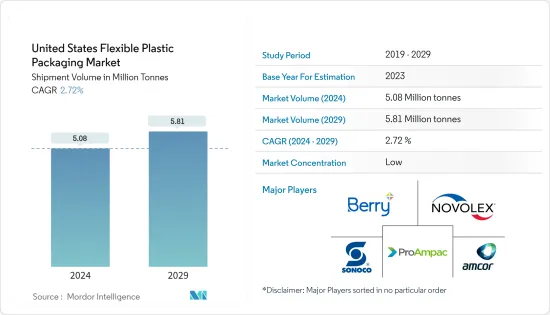

米国の軟質プラスチック包装市場は断片化されています。市場の主要企業には、Berry Global Group、Proampac LLC、Novolex Holdings Inc.、Sonoco Products Company、Amcor Group GmbH、C-P Flexible Packaging、American Packaging Corporation、Sealed Air Corporationが含まれます。市場のプレーヤーは、増大する需要に対応するため、革新的で持続可能な軟質プラスチック包装ソリューションの提供に注力しています。

2024年4月、American Packaging Corporationはペットフード製品向けのRE Design for Recycleフレキシブル包装技術の発売を発表しました。この新技術には、コンポスト、サーキュラー、再生可能コンテンツデザイン、リサイクルフィルムと紙のオプションの追加デザインが含まれます。これにより、同社はリサイクル性に関する業界ガイドラインを満たすことができます。

2023年11月、プロアンパック・エルエルシーは、ポストコンシューマー・リサイクル(PCR)材料を使用したProActive PCRレトルトパウチの発売を発表しました。この製品の発売は、同社が革新的なソリューションを求める小売業者やブランドに対応し、循環経済の目標を達成するのに役立ちます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の想定と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 冷凍食品消費の増加が需要を牽引

- 軽量バリア包装ソリューションの需要増加

- 市場抑制要因

- プラスチック材料の使用に関する規制

第6章 貿易シナリオ

- 製品タイプとプラスチック樹脂に基づくEXIMデータ

- 貿易分析(輸出入上位5カ国、価格分析、主要港など)

第7章 価格動向分析

- プラスチック樹脂(現在の価格と過去の動向)

- 製品タイプ(主な包装形態)

第8章 市場セグメンテーション

- 材料タイプ別

- ポリエチレン(PE)

- 二軸延伸ポリプロピレン(BOPP)

- キャストポリプロピレン(CPP)

- ポリ塩化ビニル(PVC)

- エチレンビニルアルコール(EVOH)

- その他の材料タイプ

- 製品タイプ別

- パウチ

- バッグ

- フィルム・ラップ

- その他の製品タイプ

- エンドユーザー産業別

- 食品

- 焼成食品

- スナック

- 肉・鶏肉・海産物

- キャンディ/菓子

- ペットフード

- その他の食品(乳製品、冷凍食品、果物・野菜などの生鮮食品など)

- 飲料

- パーソナルケアと化粧品

- その他のエンドユーザー産業(製薬、医療、建設、産業アプリケーション、家電パッケージ産業)

- 食品

- 国別

- 米国

- カナダ

第9章 競合情勢

- 企業プロファイル

- Berry Global Group

- Proampac LLC

- Novolex Holdings Inc.

- Sealed Air Corporation

- Sonoco Products Company

- American Packaging Corporation

- C-P Flexible Packaging

- ePac Holdings LLC

- PPC Flex Company Inc.

- Flex Films(USA)Inc.(Uflex Limited)

- Printpack Inc.

- Sigma Plastics Group Inc.

- Amcor Group GmbH

- Constantia Flexibles Group GmbH

- Winpak Co. Limited

- Mondi PLC

- Transcontinental Inc.

第10章 投資分析

第11章 将来の展望

The United States Flexible Plastic Packaging Market size in terms of shipment volume is expected to grow from 5.08 Million tonnes in 2024 to 5.81 Million tonnes by 2029, at a CAGR of 2.72% during the forecast period (2024-2029).

Key Highlights

- Flexible plastic packaging allows more economical and customizable options for packaging products. It is particularly useful in industries requiring versatile packaging, such as the food and beverages, personal care, and pharmaceutical industries. It has grown popular due to its high efficiency and cost-effectiveness. Government agencies in the region fund projects to reduce carbon emissions and energy consumption, which can present a positive outlook in the market.

- The US Department of Energy (DOE) announced it would invest USD 13.4 million in funding to produce plastic with low energy consumption and minimum carbon dioxide emissions. This investment is focused on addressing metal waste recycling challenges. Since flexible packaging consumes less material than rigid packaging, it requires less production energy and helps reduce carbon emissions. Such initiatives will assist in promoting the development of bioplastic as a sustainable material for flexible plastic packaging and highlight flexible packaging as an economical substitute for rigid packaging.

- The need to integrate technology with packaging is driven by rising demand for packaging materials with improved barrier qualities, product innovation, and increasing supply chain digitization. The growth of the food ingredients market in the region is driven by the growth of the food and beverage industry, increasing consumption of dairy and frozen dairy products, and increased focus on demand for processed and packaged foods. Flexible plastic packaging is the common packaging material. The growing demand for portable and suitable food packaging is driving the use of flexible plastic packaging across various industries.

- Pouch packaging is rapidly gaining popularity as it is a highly convenient and portable solution. Many of today's shoppers prefer flexible, stand-up pouches over traditional, rigid packaging. Consumers drove the demand for stand-up pouches (snacks, beverages, baby food, or industrial oils and lubricants) exponentially over the past decade. Specific innovations in the packaging type further drive the market's sustainability.

- For instance, in November 2023, ProAmpac, a US-based packaging and material science, introduced a sustainable alternative to traditional retort options called ProActive PCR retort pouches. These pouches are designed to reduce the use of new plastics and incorporate up to 30% post-consumer recycled material by weight. This aims to assist brands and retailers in achieving their circular economy objectives. The ProActive PCR retort pouches are specifically tailored for products like shelf-stable ready-to-eat proteins that require exceptional barrier properties and heat resistance.

- The market players are investing in new product development to satisfy customers' rising needs. For instance, in August 2023, TC Transcontinental Packaging, the Packaging segment of TC Transcontinental, announced an investment of USD 60 million toward developing advanced mono-material recyclable flexible plastic packaging solutions, providing high-performance polyethylene films with more heat resistance.

- The regional players are acquiring various packaging firms to expand their market presence. For instance, in February 2023, SEE announced that it completed the acquisition of Liquibox for a purchase price of USD 1.15 billion on a money and debt-free basis. This strategic investment unites two players in the flexible packaging industry and aligns with both companies' high-performance growth. Liquibox innovates and manufactures bag-in-box sustainable fluids and liquid packaging, dispensing products for fresh food, beverage, consumer goods, and industrial end-markets. This acquisition accelerates SEE's fastest-growing segment, the CRYOVAC brand Fluids and Liquids business. CRYOVAC technology, scale, and market access provide significant synergies.

United States Flexible Plastic Packaging Market Trends

Increasing Demand for Pouch Packaging among Various End-user Industries

- Pouches play a pivotal role in the food and beverages, cosmetics, baby food, pharmaceuticals, and energy drinks segments in the United States. Driven by a growing consumer preference for convenience and their adoption by small and medium enterprises, the flexible plastic packaging market, especially pouches, is set for significant growth. The demand for pouch packaging has surged across various industries, buoyed by technological advancements and evolving consumer tastes.

- The US food and beverage segment, encompassing fast food chains, organic foods, soft drinks, health supplements, and confectionaries, is a primary driver of the nation's plastic pouch packaging. According to the National Confectioners Association report, confectionary sales in the United States hit USD 48 billion in 2023, with projections soaring to USD 61 billion by 2028.

- Convenience and protection are essential drivers for pouch packaging's popularity. Their versatility in size, from small to large, makes them ideal for the cosmetic industry, especially for products tailored to the travel and tourism markets. Additionally, with 92% of United States consumers prioritizing freshness in their purchases, stand-up pouches with explicit films are gaining significant traction, as highlighted by polymer packaging.

- Also, innovations and product developments are reshaping the pouch packaging landscape. With time-starved consumers favoring microwave-friendly options for quick meals, manufacturers are responding by introducing pouches with advanced functional attributes. A prime example is Kraft Heinz's 2023 launch of a pouch that crisps up a microwaved grilled cheese. This move, featuring their patented 360Crisp technology, showcases the company's commitment to pioneering innovations in its product lineup.

- The United States is seeing a rise in demand for sustainable packaging driven by consumers and manufacturers. Manufacturers are increasingly moving toward circular economic models, boosting the growth of eco-friendly pouch packaging. This shift is helping eco-friendly pouches and affecting the broader flexible plastic packaging market.

- Amcor Group GmbH, a leading sustainable packaging manufacturer, teamed up with Stonyfield Organic, a top organic yogurt producer, and Cheer Pack North America, known for its spouted pouches. They created the first all-polyethylene (PE) spouted pouch. This new design replaces Stonyfield Organic's old multilayered packaging and is now used for its YoBaby refrigerated yogurt, marking a significant step toward sustainability.

Flexible Plastic Packaging Demand Surges as Consumer Lifestyle Shifts

- Consumer products, from food to cosmetics, are increasingly turning to flexible packaging, driven by a demand for convenient, portable solutions. This shift is mainly due to the rising popularity of packaging that aligns with the fast-paced urban lifestyle.

- As consumers seek lightweight, easy-to-use packaging, vendors are pivoting to innovative solutions to stay competitive in the evolving retail landscape. Embracing materials like flexible pouches meet these demands and offer significant energy-saving advantages.

- Also, the trend toward smaller, microwavable portions is gaining traction, especially as single-person households become more prevalent. This shift has bolstered convenience store retailing and heightened the need for more convenient packaging solutions.

- Supermarkets and hypermarkets, recognizing the demand for convenience in today's fast-paced world, increasingly offer easily transportable options. In the food industry, ready-to-eat meals, often housed in plastic pouches, are witnessing remarkable growth. These pouches cater to various products, from fully cooked meals to those that can be reheated with hot water, a heater, or even enjoyed cold.

- Highlighting this trend, data from the US Census Bureau reveals a notable increase in supermarket and grocery store sales, reaching USD 846.38 billion in 2023, up from USD 823.68 billion in 2022. Such robust sales underscore the growing appetite for flexible packaging in the nation.

- Illustrating this market momentum, in January 2024, Accredo Packaging Inc., a leading sustainable packaging manufacturer, completed its fourth expansion at its Texas headquarters, investing a substantial USD 10 million. Adding 83,000 square feet of office space, this expansion underscores the company's commitment to producing recyclable, compostable, and sustainable packaging materials, catering to diverse markets like snacks, confectionery, and baked goods.

United States Flexible Plastic Packaging Industry Overview

The United States flexible plastic packaging market is fragmented. The major players in the market include Berry Global Group, Proampac LLC, Novolex Holdings Inc., Sonoco Products Company, Amcor Group GmbH, C-P Flexible Packaging, American Packaging Corporation, and Sealed Air Corporation. The players in the market are focusing on offering innovative and sustainable flexible plastic packaging solutions to cater to the growing demand.

In April 2024, American Packaging Corporation announced the launch of RE Design for Recycle flexible packaging technology for pet food products. The new technology includes compost, circular, renewable content designs, and additional designs for recycled film and paper options. This would help the company meet industry guidelines for recyclability.

In November 2023, ProAmpac LLC announced the launch of ProActive PCR Retort pouches made using post-consumer recycled (PCR) material. The launch of this product helps the company cater to retailers and brands looking for innovative solutions and meeting circular economy goals.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defination

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Consumption of Frozen Food Products Drives the Demand

- 5.1.2 Rising Demand for Lightweight Barrier Packaging Solution

- 5.2 Market Restraints

- 5.2.1 Regulations over the Usage of Plastic Material

6 TRADE SCENARIO

- 6.1 EXIM Data Based on Product Type and Plastic Resins

- 6.2 Trade Analysis (Top Five Import-Export Countries, Price Analysis, and Key Ports, among others)

7 PRICING TREND ANALYSIS

- 7.1 Plastic Resins (Current Pricing and Historic Trends)

- 7.2 Product Type (Key Packaging Formats)

8 MARKET SEGMENTATION

- 8.1 By Material Type

- 8.1.1 Polyethene (PE)

- 8.1.2 Bi-oriented Polypropylene (BOPP)

- 8.1.3 Cast Polypropylene (CPP)

- 8.1.4 Polyvinyl Chloride (PVC)

- 8.1.5 Ethylene Vinyl Alcohol (EVOH)

- 8.1.6 Other Material Types

- 8.2 By Product Type

- 8.2.1 Pouches

- 8.2.2 Bags

- 8.2.3 Films and Wraps

- 8.2.4 Other Product Types

- 8.3 By End-user Industry

- 8.3.1 Food

- 8.3.1.1 Baked Food

- 8.3.1.2 Snacked Food

- 8.3.1.3 Meat, Poultry, and Sea Food

- 8.3.1.4 Candy/Confections

- 8.3.1.5 Pet Food

- 8.3.1.6 Other Food (Dairy Products, Frozen Food, and Fresh Produces such as Fruits and Vegetables, etc.)

- 8.3.2 Beverage

- 8.3.3 Personal Care and Cosmetics

- 8.3.4 Other End-user Industry (Pharmaceutical, Medical, Construction, Industrial Application, and Consumer Electronics Packaging Industries)

- 8.3.1 Food

- 8.4 By Country

- 8.4.1 United States

- 8.4.2 Canada

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 Berry Global Group

- 9.1.2 Proampac LLC

- 9.1.3 Novolex Holdings Inc.

- 9.1.4 Sealed Air Corporation

- 9.1.5 Sonoco Products Company

- 9.1.6 American Packaging Corporation

- 9.1.7 C-P Flexible Packaging

- 9.1.8 ePac Holdings LLC

- 9.1.9 PPC Flex Company Inc.

- 9.1.10 Flex Films (USA) Inc. (Uflex Limited)

- 9.1.11 Printpack Inc.

- 9.1.12 Sigma Plastics Group Inc.

- 9.1.13 Amcor Group GmbH

- 9.1.14 Constantia Flexibles Group GmbH

- 9.1.15 Winpak Co. Limited

- 9.1.16 Mondi PLC

- 9.1.17 Transcontinental Inc.