|

市場調査レポート

商品コード

1549974

アジア太平洋地域のスマートホーム:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Asia-Pacific Smart Home - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のスマートホーム:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

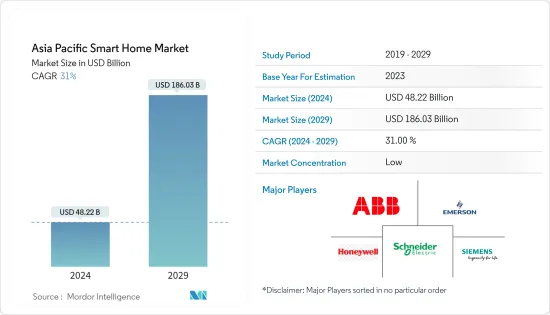

アジア太平洋地域のスマートホーム市場規模は、2024年に482億2,000万米ドルと推定され、2029年には1,860億3,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは31%で成長する見込みです。

主なハイライト

- ホームオートメーションとスマートホームは、様々な監視ソリューション、制御、自動化された機能を広く表しています。基本的なホームオートメーションには、モーターで作動するガレージドアから自動セキュリティシステムまで含まれるが、スマートホームシステムには、コンピュータ化されたシステムと対話するためのユーザーインターフェイスとしてウェブポータルやスマートフォンアプリケーションが含まれます。

- スマートフォンの普及、オンライン・ビジネスの拡大、経済のデジタル化を目指す政府のイニシアティブの高まりなどが、この急成長の主な要因となっています。GSMAの2023年版報告書「アジア太平洋地域のモバイル経済」では、この地域の5G市場の先駆性が強調されており、オーストラリア、日本、シンガポール、韓国などの国々が主流技術として5Gを採用しています。

- さらに、インドは最も急成長している5G市場の1つとして際立っており、2023年だけで数千万台の5G接続が追加されると予測されています。この地域は2030年までに約14億の5G接続を誇り、全モバイル接続の41%を占めると予想されています。

- アジア太平洋地域でも、独自のモバイル加入者が一貫して増加しています。GSMAの予測によると、同地域では今後7年間で約4億の新規加入者が増加します。特に南アジアは、同地域のモバイル加入者総数の約3分の2を占めており、2030年まで新規加入者数でリードし続けると予想されています。このようなスマートフォンの急増は、モバイル・アプリケーションの開発ブームに拍車をかけています。この動向を活用し、一般家庭でもスマートフォンを電子機器と統合して一時的なネットワークを構築するケースが増えています。

- スマートHVACR(暖房、換気、空調、冷蔵)システムは、家の環境制御に関係します。これらは、スマートサーミット、センサー、制御バルブ、スマートアクチュエータ、空調システム、スマートルームヒーターで構成されます。この地域全体では、先進国および新興国全体で政府の規制が増加しているため、新しい建物のほとんどはより高性能な冷暖房システムを必要とし、HVACシステムと市場の成長を増強しています。

- また、人工知能と機械学習の統合は、スマートホーム製品間の相互作用に革命をもたらしています。AIとMLは、スマートホーム製品が天候や時間帯、その他の文脈的要因に基づいて適切なコンテンツを表示することを可能にします。これにより、視聴者はよりパーソナライズされた魅力的な体験をすることができます。5Gネットワークとモノのインターネット(IoT)の展開は、市場にさらなる需要を生み出すと予想されます。

アジア太平洋地域のスマートホーム市場動向

HVACシステムが市場に最も大きく貢献

- アジア太平洋地域のHVAC市場は、地球温暖化による気温の上昇と建設セクターの活況によって急成長しています。その結果、HVACシステムの効率性を高めるための技術的進歩に拍車がかかっています。

- その結果、同市場の主要企業は、インテリジェントで自動化された環境に優しいHVACソリューションの開発に注力しています。例えば、IoTセンサーを統合することで、これらのシステムはリアルタイムのデータを収集し、運用効率を高めることができます。スマートHVACソリューションにおけるIoT技術の採用は、機能性と性能を向上させるこの分野に革命をもたらしています。

- さらに、業界はよりインテリジェントで自動化され、環境に配慮したHVACシステムへと急速に移行しています。AIベースのソリューションの出現とスマートHVACにおけるIoTの統合により、業界はエネルギー効率への顕著なシフトを目の当たりにし、そのようなシステムに対する需要の高まりに対応しています。

- エネルギー効率の高いシステムに対する需要の急増は、HVACセクターの自動化をさらに後押ししています。特に、国際エネルギー機関(IEA)は、東南アジアのAC販売台数が2017年の4,000万台から2040年には3億台に急増し、インドネシアがその半分を占めると予測しています。

- しかし、この成長には課題が伴う。エネルギー効率の高い機器を普及させるための積極的な対策がなければ、この地域の冷房ニーズは2040年までに200GWの追加発電を必要とする可能性があります。冷房需要は、同地域のピーク電力消費の最大30%を占める可能性があります。こうした懸念を認識し、各国政府は省エネルギーへの取り組みにますます力を入れるようになっており、スマートHVACシステムの採用をさらに後押ししています。

中国が市場の主要シェアを占める

- スマートデバイスの波が市場に押し寄せるにつれ、中国の消費者は「スマートホーム」のコンセプトをますます受け入れています。各ブランドは、家電製品の「スマートさ」を重視しています。戦略的な官民パートナーシップと的を絞った技術革新により、中国は多くの大都市でスマートシティインフラを効果的に導入し、その影響を住宅分野にも拡大しています。

- その結果、中国の都市では、スマートフォンや時計と並んで、さまざまなスマートホーム製品や家庭用機器が日常生活にシームレスに溶け込んでいます。これには、スマート・ドアロック、ドアベル、キッチン家電、猫用ゴミ箱、インテリジェントな掃除ロボットや掃除機ロボットなどが含まれます。

- さらに、中国のスマートホーム機器メーカーは、デジタル技術を活用して製品を改良する動きを強めています。例えば、ユーザーの習慣に基づいて部屋の湿度や温度を調整する自己学習機能を備えたエアコンは、今や一般的なものとなっています。

- 注目すべきは、建設部門の台頭により、スマートホーム製品に対する消費者の熱意が依然として高いことです。世界平均が3.5台であるのに対し、中国人は1世帯あたり4.1台と世界で最も多いです。さらに、中国の回答者の3分の1は、5つ以上のスマートホーム製品を持っており、世界全体の27%を占めています。これらすべての要因が、中国におけるスマートホームの前向きな成長見通しを示しています。

アジア太平洋地域のスマートホーム産業の概要

アジア太平洋地域のスマートホーム市場は、大小さまざまなプレーヤーが存在するため断片化しています。大手企業はいずれも大きな市場シェアを占めており、世界の消費者基盤の拡大に注力しています。同市場の主要企業には、Schneider Electric SE、Emerson Electric Corporation、ABB Ltd、Honewell International Inc.、Siemens AGなどがあります。各社は、予測期間中に競争力を獲得するために、複数の提携、パートナーシップ、買収を形成し、新製品の導入に投資することで市場シェアを拡大しています。

2023年12月、ハイアールスマートホームはCarrier Global Corporationの業務用冷蔵庫事業を買収する意向を発表しました。ベンダーは、対象事業を対象会社に再編する意向です。この買収により、同社は業務用冷蔵庫業界において代替冷媒を推進し、環境持続可能性への取り組みに向けた大きな基盤を作りたいとしています。

2023年10月、リンナイ・オーストラリアは、スマートホームとダクト空調制御システムのメーカーであるiZone社の買収を発表しました。iZone社の買収はリンナイ・オーストラリアにとって重要なマイルストーンであり、リンナイのブランドポートフォリオを拡大し、Brivis社やAPAC社など他の有名なオーストラリアのHVACブランドも取り込んでいます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

- COVID-19の後遺症とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- ホームセキュリティと安全性への関心の高まり

- IoT、人工知能、音声制御アシスタントなどの技術の進歩

- 市場抑制要因

- 複雑な設置とセットアップ

- 相互運用性の問題

第6章 市場セグメンテーション

- 製品タイプ別

- 快適性と照明

- 制御と接続性

- エネルギー管理

- ホームエンターテイメント

- セキュリティ

- スマート家電

- HVACコントロール

- 技術別

- Wi-Fi

- Bluetooth

- その他の技術

- 国別

- 中国

- 日本

- インド

- 韓国

- オーストラリアとニュージーランド

第7章 競合情勢

- 企業プロファイル

- Schneider Electric SE

- Emerson Electric Co.

- ABB Ltd.

- Honeywell International Inc.

- Seimens AG

- Signify Holding

- Microsoft Corporation

- Google Inc.

- Cisco Systems Inc.

- General Electric Company

- Dahua Technology

- D-Link Electronics Co. Ltd

第8章 投資分析

第9章 市場の将来

The Asia Pacific Smart Home Market size is estimated at USD 48.22 billion in 2024, and is expected to reach USD 186.03 billion by 2029, growing at a CAGR of 31% during the forecast period (2024-2029).

Key Highlights

- Home automation and smart homes broadly describe various monitoring solutions, controls, and automated functions. While basic home automation can include anything from motor-operated garage doors to automated security systems, smart home systems involve a web portal or smartphone application as the user interface to interact with a computerized system.

- Key drivers of this surge include the rising adoption of smartphones, expanding online business presence, and heightened government initiatives aimed at digitalizing economies. The GSMA's 2023 report, "The Mobile Economy for Asia Pacific," highlights the region's pioneering 5G markets, with countries like Australia, Japan, Singapore, and South Korea embracing 5G as a mainstream technology.

- Moreover, India stands out as one of the fastest-growing 5G markets, projected to add tens of millions of 5G connections in 2023 alone. The region is anticipated to boast approximately 1.4 billion 5G connections by 2030, representing 41% of all mobile connections.

- Asia-Pacific has also witnessed a consistent rise in unique mobile subscribers. As per GSMA forecasts, the region will see an addition of nearly 400 million new subscribers over the next seven years. South Asia, in particular, commands about two-thirds of the region's total mobile subscriber base, and it's expected to continue leading in new subscriber additions through 2030. This surge in smartphone popularity has, in turn, fueled a boom in mobile application development. Leveraging this trend, households increasingly integrate their smartphones with electronic devices to create temporary networks, especially for smart home automation.

- The smart HVACR (heating, ventilation, air conditioning, and refrigeration) systems concern the house's environmental controls. They comprise smart thermites, sensors, control valves, smart actuators, air conditioning systems, and smart room heaters. Across the region, due to the increasing government regulations across developed and developing countries, most of the new buildings need more competent heating and cooling systems, augmenting the growth of HVAC systems and the market.

- Also, integrating artificial intelligence and machine learning is revolutionizing the interaction between smart home products. AI and ML enable smart home products to display relevant content based on the weather, time of day, and other contextual factors. This allows for a more personalized and engaging experience for viewers. The rollout of 5G networks and the Internet of Things (IoT) is expected to create more demand in the market.

Asia-Pacific Smart Home Market Trends

HVAC Systems are Among the Most Significant Contributors to the Market

- The Asia-Pacific HVAC market is surging, driven by rising temperatures due to global warming and the booming construction sector. This, in turn, is spurring technological advancements in HVAC systems to enhance efficiency.

- As a result, key players in the market are largely focusing on developing intelligent, automated, and eco-friendly HVAC solutions. For instance, integrating IoT sensors allows these systems to collect real-time data, boosting operational efficiency. The adoption of IoT technology in smart HVAC solutions is revolutionizing the sector enhancing functionality and performance.

- Moreover, the industry is rapidly moving toward more intelligent, automated, and eco-conscious HVAC systems. With the advent of AI-based solutions and the integration of IoT in smart HVAC, the industry is witnessing a prominent shift towards energy efficiency, meeting the escalating demand for such systems.

- The surging demand for energy-efficient systems further bolsters automation in the HVAC sector. Notably, the International Energy Agency (IEA) predicts a remarkable surge in AC sales in Southeast Asia, from 40 million units in 2017 to 300 million by 2040, with Indonesia accounting for half of this figure.

- However, this growth comes with challenges. Without proactive measures to promote energy-efficient units, the region's cooling needs could necessitate an additional 200 GW of power generation by 2040. Cooling demands may contribute up to 30% of the region's peak electricity consumption. Recognizing these concerns, governments are increasingly focusing on energy-saving initiatives, further propelling the adoption of smart HVAC systems.

China Holds the Major Share of the Market

- Chinese consumers increasingly embrace the concept of 'smart homes' as a wave of smart devices floods the market. Brands are placing a strong emphasis on 'smartness' in their home appliances. Through strategic public-private partnerships and targeted technological innovations, China has effectively implemented smart city infrastructure in numerous major metropolises, extending its impact to the residential sector.

- Consequently, various smart home products and household equipment have seamlessly integrated into daily life in Chinese cities alongside smartphones and watches. These include smart door locks, doorbells, kitchen appliances, cat litter boxes, and intelligent sweeping and vacuum robots.

- Moreover, manufacturers of smart home devices in China are increasingly harnessing digital technologies to revamp their products. For example, air conditioners with self-learning capabilities, adjusting room humidity and temperature based on user habits, are now commonplace.

- Notably, with the rise of the construction sector, consumer enthusiasm for smart home products remains high. As per Yakai, Chinese people have 4.1 per household, the highest in the world, compared with a global average of 3.5. In addition, one-third of Chinese respondents represent 27% globally, as they have five or more such products. All these factors present a positive growth prospect for smart homes in China.

Asia-Pacific Smart Home Industry Overview

The Asia-Pacific smart home market is fragmented due to the presence of various small and large players. All the major players account for a significant market share and focus on expanding the global consumer base. Some of the significant players in the market are Schneider Electric SE, Emerson Electric Corporation, ABB Ltd, Honewell International Inc., and Siemens AG. Companies are increasing their market share by forming multiple collaborations, partnerships, and acquisitions and investing in introducing new products to earn a competitive edge during the forecast period.

In December 2023, Haier Smart Home Co. Ltd announced its intention to acquire the commercial refrigeration business of Carrier Global Corporation. The vendor intends to restructure the Target Business into the Target Company. With this transaction, the company wants to create a significant hold on molding itself towards environmental sustainability initiatives, pushing alternative refrigerants in the commercial refrigeration industry.

In October 2023, Rinnai Australia announced the acquisition of iZone, a manufacturer of smart home and ducted air conditioning control systems. The acquisition of iZone showcases a noteworthy milestone for Rinnai Australia and broadens Rinnai's brand portfolio, which also incorporates other well-known Australian HVAC brands, such as Brivis and APAC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot

- 4.5 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Concern about Home Security and Safety

- 5.1.2 Advances in Technology, such as IoT, Artificial Intelligence, and Voice Controlled Assistants

- 5.2 Market Restraints

- 5.2.1 Complex Installation and Setup

- 5.2.2 Interoperability Issues

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Comfort and Lighting

- 6.1.2 Control and Connectivity

- 6.1.3 Energy Management

- 6.1.4 Home Entertainment

- 6.1.5 Security

- 6.1.6 Smart Appliances

- 6.1.7 HVAC Control

- 6.2 By Technology

- 6.2.1 Wi-Fi

- 6.2.2 Bluetooth

- 6.2.3 Other Technologies

- 6.3 By Country

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 India

- 6.3.4 South Korea

- 6.3.5 Australia and New Zealand

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Emerson Electric Co.

- 7.1.3 ABB Ltd.

- 7.1.4 Honeywell International Inc.

- 7.1.5 Seimens AG

- 7.1.6 Signify Holding

- 7.1.7 Microsoft Corporation

- 7.1.8 Google Inc.

- 7.1.9 Cisco Systems Inc.

- 7.1.10 General Electric Company

- 7.1.11 Dahua Technology

- 7.1.12 D-Link Electronics Co. Ltd