Wi-Fiネットワーク機器の世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

Wi-Fi Network Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1549923

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

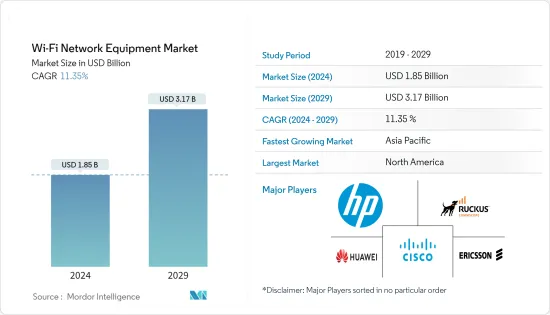

世界のWi-Fiネットワーク機器の市場規模は、2024年に18億5,000万米ドルと推定され、2029年には31億7,000万米ドルに達し、予測期間中(2024年~2029年)にCAGR11.35%で成長すると予測されています。

主なハイライト

- 消費者、商業、産業環境におけるモノのインターネット(IoT)機器の使用の増加は、機器需要の主要な促進要因です。5G技術の台頭により、企業はさらに多くのコネクテッドデバイスを受け入れ、ビジネスデータを活用する能力を強化する態勢が整っています。このようなスマートデバイスやコネクテッドデバイスの導入急増は、世界のWi-Fiネットワーク機器市場の成長を直接後押しします。

- さらに、多くの企業がセキュリティを強化し、データ交換を合理化するためにネットワーク機器をオーバーホールしています。最新のWi-Fi規格であるWi-Fi 6およびWi-Fi 6E接続の採用は、複数のデバイスを同時に処理する際の速度、容量、効率の向上を促進します。これらの進歩は、ビデオ会議、ゲーム、IoT機器など、帯域幅を多用するアプリケーションをサポートする上で極めて重要です。World in Dataによると、2023年にオンライン・インターネットにアクセスできる人口は全体の63%に過ぎません。

- 2023年にはオフィス復帰の指令が牽引役となりましたが、柔軟性を求める声は依然として強くあります。多くの企業はオフィス回帰を企業文化の強化に不可欠なものと考えていますが、オフィス回帰には大きなハードルがあります。コラボレーションでは、対面でのミーティング、バーチャル通話、高度なテクノロジーなど、従来型のオフィス環境を提供しています。そのため、需要に対応するための家庭用Wi-Fiデバイスの需要は依然として伸びています。

- Wi-Fiネットワークは、主にWi-Fi対応デバイスの普及に起因する無数のセキュリティ脅威に遭遇しています。セキュリティ・プロトコルの技術的進歩にもかかわらず、データの安全性と完全性の維持は依然として重要な課題です。特に企業では、機密情報を扱う場合、データ漏洩のリスクが高まります。攻撃者はこれらの脆弱性を悪用し、しばしば不正なデータアクセスを引き起こします。

- COVID-19の大流行後、企業やサービス・プロバイダーは、リモート・ユーザーからの負荷増大に対応するため、ネットワーク・インフラのアップグレードに多額の投資を行いました。既存のWi-Fiネットワークのアップグレードや新技術の導入を計画し、安全で信頼性の高い接続性を確保しました。

Wi-Fiネットワーク機器市場動向

企業向けセグメントが大きなシェアを占める見込み

- 企業は、組織、教育、ヘルスケア、大規模ビジネス通信に不可欠なインフラとサービスを提供する、極めて重要なセグメントを形成しています。企業は、音声、データ、インターネット・サービスをサポートするネットワーク・インフラの展開と保守を監督します。

- 警察、消防、救急などの公共安全機関は、迅速な情報共有、調整、緊急対応のために、これらのWi-Fiネットワーク機器に大きく依存しています。さらに、ヘルスケア分野では、安全な患者データ伝送、遠隔医療、遠隔モニタリング、専門家間のシームレスな医療データ交換のために、これらのネットワークに依存しています。

- さらに、Wi-Fi 6(802.11ax)の採用ニーズが高まっており、その背景には、高密度環境での高速化と性能向上があります。多くの企業がWi-Fi 6へのアップグレードを進めており、帯域幅を必要とする用途のニーズの高まりに対応しています。多くの企業がクラウド管理型Wi-Fiソリューションに移行しており、集中管理、拡張性、容易な配備を可能にしています。

- AIプラットフォームとアプリケーションは、企業の開発者に力を与え、MLの能力を活用して精度を高め、ユーザー体験を向上させ、効率を高めることを可能にします。AIの利用範囲は、エッジからコア、クラウドへと広がっていきます。例えば、2023年12月、Origin AIとエアティーズはWi-Fiセンシング技術を通じてISPの収益と顧客満足度を向上させるために提携しました。この提携は、スマートWi-Fiソリューションの大きな進歩を意味します。この提携を活用し、エアティーズのISPクライアントはブロードバンドサービスに高度な侵入検知機能を盛り込みました。Originの先進技術を統合することで、エアティーズはISPの収益源を強化するだけでなく、顧客離れを防ぎ、ネット・プロモーター・スコア(NPS)を向上させることを目指しています。

- さらに、増加するサイバーセキュリティの脅威は、データを保護し、国ごとの規制に準拠するために、より優れたセキュリティ機能を備えた高度なWi-Fiソリューションを使用することを企業に促しています。IBMのデータによると、2023年には製造業が25.7%、次いで金融・保険業が18.2%と、最大のサイバー脅威にさらされています。

アジア太平洋が大きな成長シェアを占める見込み

- 5GとWi-Fiはしばしば補完的な技術と見なされています。5Gが主に広範なネットワークカバレッジと高速モバイル接続を提供するのに対し、Wi-Fiは大容量で局所的なカバレッジ(特に屋内)を提供します。アジア太平洋では、いくつかの先進市場が5Gの展開で先陣を切っています。韓国は2019年4月に世界初の全国5Gネットワークを開始し、世界のペースを作りました。これに同年末、オーストラリア、フィリピン、中国、ニュージーランドで同様の展開が迅速に続きました。GSMA Intelligenceによると、アジア太平洋は現在、5G展開の第2波を目の当たりにしており、インドネシア、インド、マレーシアなどの国々は、2025年までにアジア太平洋を世界最大級の5G市場に押し上げる構えです。

- 都市部や公共交通機関、会場などで信頼性の高いインターネットアクセスを提供するため、公共Wi-Fiインフラの拡大に向けた投資が拡大しています。この動向は、すべての人の接続性を向上させることを目的とした政府の取り組みや民間投資によって支えられています。シスコによると、世界の公衆Wi-Fiホットスポットのシェアはアジア太平洋が最も高く、2024年には約48%を超えると予想されています。

- AIと機械学習は、ネットワーク管理と自動化をますます形成しつつあります。これらの技術は、ネットワーク設定を自動化し、問題解決を合理化し、使用パターンに基づいてパフォーマンスを向上させます。AIは、ネットワーク・インフラ内のエネルギー消費の最適化において極めて重要な役割を果たし、特に高度な通信ネットワークにおいて、二酸化炭素排出量と運用コストの大幅な削減につながります。CompTIA IT Industry Outlook 2024の調査によると、チャネル企業の30%がすでにAIを業務に組み込んでおり、さらに26%がAIソリューションを積極的に検討しています。

- 高解像度ビデオ、ソフトウェアアップデート、データセットなどのデジタルファイルが増え続ける中、高速かつ広帯域のネットワークは極めて重要です。より高速な転送レートを実現し、ユーザーがオンラインで迅速にファイルをダウンロード、アップロードできるようにします。多くの企業は現在、データ保護を強化するためにクラウドデータベースに移行しています。このような状況において、帯域幅を拡大したWi-Fiは、オンラインデータへの迅速かつ効率的なアクセスを促進する重要なプレーヤーとして浮上しています。

- 特に消費者向けクラウド・ストレージが普及し、大容量のマルチメディア・ファイルのダウンロードがローカルのハードディスク・ドライブから転送するのと同じくらい迅速に行えるようになると、広帯域幅のスピードが不可欠になります。例えば、シスコのレポートによると、アジア太平洋では25Mbpsを超える速度が97%という驚異的な普及率を達成しています。

- いくつかの市場企業は、拡張現実(AR)ユースケース向けの高度なソリューションに対応するため、Wi-Fi技術を強化しています。2024年2月、ファーウェイは、最新のWi-Fi規格に準拠した最先端のソリューションであるエンタープライズ・グレードの「AirEngine Wi-Fi 7」を発表し、先鞭をつけました。この技術は、特に高密度、高帯域幅、低遅延の接続を必要とするシナリオにおいて、より堅牢でシームレスな無線ネットワークを約束します。このようなシナリオには、メタバースへのアクセスや、教育目的での拡張現実/仮想現実(AR/VR)の活用などが含まれます。

Wi-Fiネットワーク機器業界の概要

Wi-Fiネットワーク機器市場は細分化されており、さまざまな企業が存在します。同市場では、多数のベンダーが提携、パートナーシップ、新規立ち上げなど多様な成長戦略に注力しています。注目すべき企業には、シスコシステムズ、ヒューレット・パッカード・エンタープライズ・ディベロップメントLP(Aruba)、コムスコープ(RUCKUS Networks)、テレフォナクティボラゲットLMエリクソン、ファーウェイ・テクノロジーズなどが含まれます。

- 2024年1月、ネットワーク接続で著名なCommScopeは、Wi-Fi Allianceが同社のRUCKUS Wi-Fi 7 APファミリーを厳格なテストの対象に選んだことを明らかにしました。この選択により、RUCKUSデバイスは認証テストベッドにおける唯一の商用アクセスポイントとなり、Wi-Fi CERTIFIED 7デバイスとのシームレスな相互運用性が保証されます。この動きは、次世代デバイスの世界ネットワーク向けにWi-Fi性能を向上させるというCommScopeのコミットメントを強調するものです。

- 2023年11月、ファーウェイはHuawei Connect 2023でオールシナリオWLANソリューションを発表しました。この発表では、エンタープライズ分野でのWi-Fi 7技術の採用にさらに焦点を当て、教育、ヘルスケア、小売、製造などの業界にわたる顧客のネットワーク体験を強化しました。Wi-Fi 7の強化された帯域幅機能の導入により、キャンパス・ネットワークはトラフィックの増加に対応するため、マルチGeキャンパスへの進化に向けて準備を進めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- マクロ経済シナリオの分析(景気後退、ロシア・ウクライナ危機など)

- インターネットサービスに関連する規制状況

- 各国のデータ保護ガイドラインに関する報道

第5章 市場力学

- 市場促進要因

- コネクテッドデバイスの利用拡大とBYOD政策

- 企業におけるデジタルトランスフォーメーションの高まり

- Wi-Fi技術における継続的な技術進歩(Wi-Fi 6規格の実装など)

- 市場抑制要因

- データセキュリティとプライバシーに関する懸念

- 屋外でのWi-Fi導入に関する懸念

- Wi-Fi接続規格に関する洞察

- 802.11b、802.11a、802.11g、802.11n、802.11ac、802.11axをカバー

- ケーススタディ分析

- ゲスト企業向けWi-Fiサービスの導入動向の概要

- 成長促進要因(顧客エンゲージメントとロイヤルティに対するニーズの高まり|企業におけるBYODの動向|信頼性の高いWi-Fiアクセスによる企業資産のサイバーセキュリティ対策強化の必要性)

- エンタープライズWi-Fiホットスポット管理ソリューションの概要と主な機能(分析を含む)

- 業界別の使用事例

- 旅行・ホスピタリティ、IT・通信、小売・eコマース、教育、BFSIなどをカバー

- 主要ベンダーとその製品概要

- Purple WiFi、Noniussoft、AVSystem、Wanaportなどをカバー

第6章 市場セグメンテーション

- 機器タイプ別

- アクセスポイント

- ゲートウェイ

- ルーターとエクステンダー

- その他(ケーブル、インターフェース、モジュールなど)

- エンドユーザー別

- 消費者

- 企業

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- メキシコ

- 北米

第7章 競合情勢

- 企業プロファイル

- Cisco Systems Inc.

- Hewlett Packard Enterprise Development LP(Aruba)

- CommScope(RUCKUS Networks)

- Telefonaktiebolaget LM Ericsson

- Huawei Technologies Co. Ltd

- Extreme Networks

- Ubiquiti Inc.

- D-Link Corporation

- TP-Link Corporation

- NETGEAR Inc.

第8章 市場機会と今後の動向

目次

The Wi-Fi Network Equipment Market size is estimated at USD 1.85 billion in 2024, and is expected to reach USD 3.17 billion by 2029, growing at a CAGR of 11.35% during the forecast period (2024-2029).

Key Highlights

- The increasing use of Internet of Things (IoT) devices in consumer, commercial, and industrial settings is a key driver for equipment demand. With the rise of 5G technology, organizations are poised to embrace even more connected devices, enhancing their ability to leverage business data. This surge in smart and connected device adoption directly fuels the global Wi-Fi network devices market's growth.

- Furthermore, many enterprises are overhauling their network equipment to bolster security and streamline data exchanges. The adoption of the latest Wi-Fi standards, Wi-Fi 6 and Wi-Fi 6E connectivity, facilitates improved speed, capacity, and efficiency in handling multiple devices simultaneously. These advancements are crucial for supporting bandwidth-intensive applications such as video conferencing, gaming, and IoT devices. As per the 'World in Data,' only 63% of the population had access to the online internet in 2023, which provides immense growth potential.

- While return-to-office mandates gained traction in 2023, the call for flexibility remains strong. Many firms view office returns as pivotal for bolstering their culture, yet the shift back poses significant hurdles. Collaboration provides traditional office setups, including in-person meetings, virtual calls, and advanced technology. Thus, there is still growth in the requirement for home Wi-Fi devices to cater to the demand.

- Wi-Fi networks encounter a myriad of security threats, primarily stemming from the prevalence of Wi-Fi-enabled devices. Despite technological advancements in security protocols, maintaining data safety and integrity remains a significant challenge. Particularly in corporate settings, when handling sensitive information, the risk of data breaches increases. Attackers exploit these vulnerabilities, often resulting in unauthorized data access.

- After the COVID-19 pandemic, enterprise and service providers invested heavily in upgrading the network infrastructure to cater to the increasing load that is coming from the remote user. The company planned for upgrading the existing Wi-Fi networks and implementing new technologies to ensure secure and reliable connectivity.

Wi-Fi Network Equipment Market Trends

The Enterprises Segment is Expected to Hold a Major Share

- Enterprises form a pivotal segment, offering the infrastructure and services crucial for organizational, educational, healthcare, and large-scale business communication. They oversee the deployment and maintenance of network infrastructures, supporting voice, data, and internet services.

- Public safety entities, including police, fire, and emergency services, heavily depend on these Wi-Fi network equipment devices for swift information sharing, coordination, and emergency response. Moreover, the healthcare sector relies on these networks for secure patient data transmission, telemedicine, remote monitoring, and seamless medical data exchange among professionals.

- Moreover, there is a growing need for Wi-Fi 6 (802.11 ax) adoption, which is driven by higher speed and better performance in dense environments. Many enterprises are upgrading to Wi-Fi 6, which caters to the increasing need for bandwidth-intensive applications. Many enterprises are moving toward cloud-managed Wi-Fi solutions, which allow centralized management, scalability, and easier deployment.

- AI platforms and applications empower enterprise developers, enabling them to harness ML's capabilities for heightened accuracy, user experience, and efficiency. The reach of AI is set to span from the edge to the core to the cloud. For instance, in December 2023, Origin AI and Airties joined forces to enhance ISP revenue and customer satisfaction through Wi-Fi Sensing Technology. This collaboration marks a significant advancement in Smart Wi-Fi solutions. By leveraging the partnership, Airties' ISP clients included an advanced intrusion detection feature in their broadband offerings. By integrating Origin's advanced technology, Airties aims to not only boost ISPs' revenue streams but also combat customer churn and elevate their Net Promoter Scores (NPS).

- Moreover, increasing cybersecurity threats encourage enterprises to use advanced Wi-Fi solutions with better security features to protect data and remain compliant with country-specific regulations. As per data by IBM, the manufacturing sector was exposed to maximum cyber threats, which were 25.7%, followed by the finance and insurance sector, with 18.2% threats in 2023.

Asia-Pacific is Expected to Hold a Major Growth Share

- 5G and Wi-Fi are often seen as complementary technologies. While 5G primarily provides broad network coverage and high-speed mobile connectivity, Wi-Fi offers high-capacity and localized coverage, especially indoors. Several advanced markets have taken the lead in rolling out 5G in Asia-Pacific. South Korea set the global pace by launching the world's first nationwide 5G network in April 2019. This was swiftly followed by similar deployments in Australia, the Philippines, China, and New Zealand later that same year. According to GSMA Intelligence, the region is now witnessing a second wave of 5G rollouts, with countries like Indonesia, India, and Malaysia poised to propel Asia-Pacific into one of the world's largest 5G markets by 2025.

- There is growing investment in expanding public Wi-Fi infrastructure to provide reliable internet access in urban areas, public transportation, and venues. This trend is supported by government initiatives and private-sector investments that aim to improve connectivity for all. According to Cisco, Asia-Pacific is expected to have the highest share of global public Wi-Fi hotspots, at around more than 48% in 2024.

- AI and machine learning are increasingly shaping network management and automation. These technologies automate network settings, streamline issue resolution, and enhance performance based on usage patterns. AI plays a pivotal role in optimizing energy consumption within network infrastructures, leading to substantial reductions in both carbon footprints and operational costs, especially in advanced telecommunications networks. According to the CompTIA IT Industry Outlook 2024 survey, 30% of channel firms are already integrating AI into their operations, while an additional 26% are actively exploring AI solutions.

- As digital files, including high-definition videos, software updates, and datasets, continue growing, networks with high speeds and greater bandwidth are crucial. They enable faster transfer rates and empower users to download and upload files swiftly online. Many corporations are now gravitating toward cloud databases for enhanced data protection. In this landscape, Wi-Fi with expanded bandwidth emerges as a key player, facilitating swift and efficient access to online data.

- High-bandwidth speeds are becoming imperative, especially as consumer cloud storage gains traction, ensuring that downloading large multimedia files is as swift as transferring them from a local hard drive. For example, a Cisco report highlights that Asia-Pacific has achieved a remarkable 97% penetration rate in delivering speeds exceeding 25 Mbps.

- Several market players are enhancing Wi-Fi technologies to cater to advanced solutions for augmented reality use cases. In February 2024, Huawei set the tone by introducing its enterprise-grade "AirEngine Wi-Fi 7," a cutting-edge solution that adheres to the latest Wi-Fi standards. This technology promises a more robust and seamless wireless network, especially in scenarios demanding high-density, high-bandwidth, and low-latency connections. These scenarios include accessing the metaverse and leveraging augmented reality/virtual reality (AR/VR) for educational purposes.

Wi-Fi Network Equipment Industry Overview

The Wi-Fi network equipment market is fragmented, with various significant players. In the market, numerous vendors are focused toward diverse growth strategies such as collaborations, partnerships, and new launches. Notable players include Cisco Systems Inc., Hewlett Packard Enterprise Development LP (Aruba), CommScope (RUCKUS Networks), Telefonaktiebolaget LM Ericsson, and Huawei Technologies Co. Ltd.

- In January 2024, CommScope, a prominent player in network connectivity, revealed that the Wi-Fi Alliance had chosen a member of its RUCKUS Wi-Fi 7 AP family for rigorous testing. This selection places the RUCKUS device as the sole commercial access point in the certification test bed, ensuring seamless interoperability with Wi-Fi CERTIFIED 7 devices. This move underscores CommScope's commitment to advancing Wi-Fi performance for the global network of next-gen devices.

- In November 2023, At Huawei Connect 2023, Huawei unveiled its All-Scenario WLAN Solution. This launch further focused on the adoption of Wi-Fi 7 technology in the enterprise sector, enhancing network experiences for customers across industries like education, healthcare, retail, and manufacturing. With the deployment of Wi-Fi 7's enhanced bandwidth capabilities, campus networks are gearing up for a multi-Ge campus evolution to handle the increased traffic.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Analysis of Macro-Economic Scenarios (Recession, Russia-Ukraine crisis, etc.)

- 4.3 Regulatory Landscape Related to Internet Services

- 4.3.1 Coverage on Data protection Guidelines in Various Countries

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in the use of connected devices and BYOD policy

- 5.1.2 Rising Digital Transformation in the Enterprises

- 5.1.3 Ongoing Technological Advancements in Wi-Fi Technology (Wi-Fi 6 Standard Implementation, etc.)

- 5.2 Market Restraints

- 5.2.1 Data securities and Privacy Concerns

- 5.2.2 Concerns Related to Wi-Fi Implementation in Outdoor Areas

- 5.3 Insights on Wi-Fi connectivity standards

- 5.3.1 Coverage on 802.11b, 802.11a, 802.11g, 802.11n, 802.11ac, and 802.11ax

- 5.4 Case Study Analysis

- 5.5 Overview of Adoption Trends of Guest Enterprise Wi-Fi Offerings

- 5.5.1 Growth Drivers (Increasing Need for Customer Engagement and Loyalty| Growing Trends of BYOD in Enterprises | Need for Enhanced Cyber Security Measures for Enterprises Assets with Reliable Wi-Fi Access)

- 5.5.2 Overview of Enterprise Wi-Fi Hotspot Management Solution and Key Features (Including Analytics)

- 5.5.3 Industry-wise use cases

- 5.5.3.1 Coverage on Travel and Hospitality, IT and telecom, Retail and E-commerce, Education, BFSI, etc.

- 5.5.4 Brief About Major Vendors and Their Offerings

- 5.5.4.1 Coverage on Purple WiFi, Noniussoft, AVSystem, Wanaport, etc.

6 MARKET SEGMENTATION

- 6.1 By Equipment Type

- 6.1.1 Access Points

- 6.1.2 Gateways

- 6.1.3 Routers and Extenders

- 6.1.4 Others (Cables, Interface, Modules, etc.)

- 6.2 By End User

- 6.2.1 Consumers

- 6.2.2 Enterprises

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.4 Australia and New Zealand

- 6.3.5 Middle East and Africa

- 6.3.5.1 Saudi Arabia

- 6.3.5.2 United Arab Emirates

- 6.3.5.3 South Africa

- 6.3.6 Latin America

- 6.3.6.1 Brazil

- 6.3.6.2 Mexico

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Hewlett Packard Enterprise Development LP (Aruba)

- 7.1.3 CommScope (RUCKUS Networks)

- 7.1.4 Telefonaktiebolaget LM Ericsson

- 7.1.5 Huawei Technologies Co. Ltd

- 7.1.6 Extreme Networks

- 7.1.7 Ubiquiti Inc.

- 7.1.8 D-Link Corporation

- 7.1.9 TP-Link Corporation

- 7.1.10 NETGEAR Inc.

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日