|

|

市場調査レポート

商品コード

1549899

世界のアクティブ光ケーブル(AOC):市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Global Active Optical Cables (AOC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界のアクティブ光ケーブル(AOC):市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

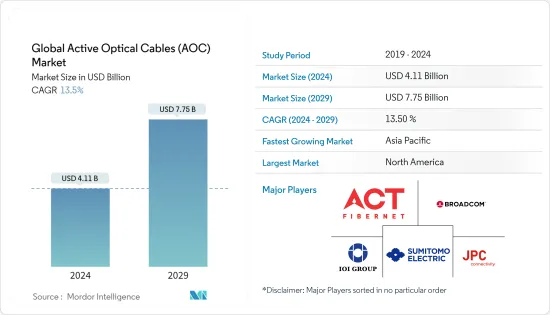

世界のアクティブ光ケーブル(AOC)の市場規模は、2024年に41億1,000万米ドルと推定され、2029年には77億5,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは13.5%で成長する見込みです。

アクティブ光ケーブル市場は、現在力強い成長を遂げており、クラウドベースのサービス、デジタル化、5G、データセンター、その他のアプリケーションの大規模導入により、さらなる成長が見込まれています。

主なハイライト

- アクティブ光ケーブル(AOC)市場は、データセンター、通信、家電など、さまざまな用途で高速データ伝送のニーズが高まっていることが主な要因となっています。様々なアプリケーションを通じたデータニーズの高まりが、AOC市場の需要を牽引すると予想されます。

- データセンター市場は、クラウド技術の大規模な応用、デジタル化、AI/MLに対する需要の高まりによって急成長しています。通信サービスプロバイダーのCloudsceneによると、2023年12月現在、世界には約10,978カ所のデータセンターがあり、その数は急速に増加しています。データセンターは堅牢で高速なインターネット接続を必要とします。したがって、データセンター市場の成長はAOC市場をも牽引すると予想されます。

- 5Gの導入は、デジタル業務の強化に欠かせない効率的な通信に対する需要の高まりに対応する構えです。5Gの広帯域波長は迅速なデータ伝送を可能にする一方で、3Gや4Gに比べると信号の到達距離は限られています。そのため、堅牢な5Gネットワークには、信号伝送用の高速ケーブルに依存するセルタワーを密集させる必要があり、AOC市場の需要を高めています。

- GSMAは、2029年までに5G接続が全モバイル接続の半分以上(51%)を占め、10年後には56%に上昇し、5Gが主要な接続技術として確固たるものになると予測しています。5Gは、その展開においてこれまでのすべてのモバイル世代を凌駕しており、2023年末までに16億接続を超え、2030年には55億接続に達すると予測されています。その結果、5Gが急拡大を続ける中、世界のアクティブ光ケーブル市場は近い将来大きな成長を遂げることになります。

- 光伝送のセキュリティに対する懸念や、機密データアプリケーションにおける潜在的な脆弱性が、AOCの普及を妨げる可能性があります。さらに、AOCは従来の銅ケーブルに比べて、特に迅速なサービス介入が必要な分野では、保守や修理に大きな課題をもたらすことが多いです。

世界のアクティブ光ケーブル(AOC)市場の動向

データセンターにおけるアクティブ光ケーブルの需要増加が市場を牽引

- 世界のアクティブ光ケーブル(AOC)市場は、業界全体の高速データ伝送需要の急増に後押しされ、近年大きな成長を遂げています。技術の進歩に伴い、効率的で信頼性の高い接続ソリューションの重要性がかつてないほど高まっています。アクティブ光ケーブル(AOC)は、レーザーやフォトダイオードなどのアクティブ素子をケーブルアセンブリに直接組み込んだ高速ケーブルソリューションとして際立っています。これらのコンポーネントは、光ファイバーケーブルによる光信号の伝送を促進する極めて重要なものです。データセンターの領域では、「200G AOC」という用語は、特に毎秒200ギガビット(Gbps)のデータレートをサポートするように設計されたケーブルを示します。

- さらに、膨大な計算能力を必要とするハイパフォーマンス・コンピューティング(HPC)環境では、200G AOCがプロセッサとストレージ・ユニット間の迅速なデータ交換を促進します。企業はハイパフォーマンス・コンピューティングを並列処理に活用し、AIやデータ分析などの高度なプログラムの実行を支援しています。特にAIや機械学習を重視するデータセンターは、HPCから大きな利益を得ることができます。

- 組織内でのクラウドコンピューティングの台頭は、データセンター市場を大きく牽引しています。Flexera State of the Cloud Report 2023によると、72%の企業がハイブリッドクラウドを採用しています。しかし、この移行は、従来のプライベートクラウドやパブリッククラウドのインフラを超えることを頻繁に意味します。

- アクティブ光ケーブル(AOC)は、データセンターのケーブルラックとスイッチの接続において極めて重要であり、スイッチとサーバー間のシームレスな通信を可能にします。通常、データセンターではまずスイッチを設置し、次に構造化ケーブリングを導入し、最後にネットワークアクセスに適した相互接続製品を選択します。10Gでは90メートル以下、40Gでは10メートル以下と定義される短距離では、カッパーケーブルが最もコスト効率の高い選択肢です。10Gで500メートル未満、40Gで150メートル未満の中距離では、マルチモードVCSEL(垂直共振器面発光レーザー)トランシーバーが好まれ、多くの場合AOCで補完されます。

- インドのデータセンター市場は大幅に拡大し、2025年には46億米ドルに達すると予測されています。この成長には、国内のインターネット・ユーザー数の増加、クラウド・コンピューティングに対する需要の高まり、デジタル化を推進する政府の取り組み、デジタル・サービス・プロバイダーによるローカライゼーションへのシフトといった要因があります。特筆すべきは、インドのデータセンター部門は、新興国市場と比較して、市場開拓段階でも運用段階でもコスト面で大きな優位性を誇っていることです。現在、データセンターの主要拠点は主にムンバイ、ベンガルール、チェンナイ、デリー(NCR)、ハイデラバード、プネーにあり、カルカッタ、ケララ、アーメダバードにも新たなセンターが誕生しています。データセンターへの投資が拡大するにつれ、インド全土でIT、電気、機械、一般建築をカバーする付帯インフラ・サービスの需要も拡大しています。

北米が大きなシェアを占める

- 北米は世界最大のデータセンター市場を誇り、現在ハイパースケールデータセンターの建設が顕著に増加しています。この急増の主な要因は、クラウドサービスへの需要の高まりとデジタル変革の進行です。Cloudsceneが発表した2024年3月時点の最新データでは、米国が5,381のデータセンターを擁し、世界のリーダーとなっています。ドイツが521、英国が514で、僅差で続いています。歴史的に、銅線ケーブルはサーバ、ルータ、スイッチ間のネットワークリンクに使われてきました。データセンターが拡大するにつれて、この地域のアクティブ銅線ケーブルの需要は増加の一途をたどっています。

- 米国では新しいデータセンタの需要は依然強く、毎週のように新しいプロジェクトが発表されています。2024年 3月、アマゾンはバーウィック原子力発電所に隣接するデータセンターの買収に6億5,000万米ドルという巨額を投じる計画を明らかにしました。この構想は、セーラムタウンシップにあるサスケハナ蒸気電気発電所を運営するタレン・エナジー社が確認したもので、アマゾンのウェブサービス部門が新たなデータセンター開発の陣頭指揮を執ることになります。

- 米国における高速インターネットの開拓も、世界のAOC市場を牽引する大きな要因です。米国農務省(USDA)は、事業者のネットワーク構築を支援するため、総額9,700万米ドルを拠出することを約束しました。これらのネットワークは、2027年までに米国全世帯でダウンロード速度100Mbps、アップロード速度20Mbpsという米国政府の設定目標を下回る、または接続性が不足している地域を対象としています。この取り組みにより、11州にわたる22,000人の加入者のサービスが強化されます。

- グリーンシティのノースイースト・ミズーリ・ルーラル・テレフォン・カンパニーは、6つの交換局を銅線からファイバー・トゥ・ザ・プレミス技術に移行するため、1,370万米ドルの融資を受けました。この取り組みでは、加入者1,063人へのサービス向上を目指し、約500ルートマイルのファイバーを敷設します。

- 2023年10月、米国連邦通信委員会(FCC)は地方のブロードバンド・インフラ強化のため、約182億8,000万米ドルの巨額投資を開始しました。この資金は2024年1月から15年間のプログラムに割り当てられ、70万カ所以上への100/20Mbpsブロードバンド配備を目標としています。さらに、44州にまたがる約200万箇所の既存サービスのアップグレードも目指しています。この野心的なブロードバンド拡大は、AOC市場に大きな影響を与えそうです。

世界のアクティブ光ケーブル(AOC)産業概要

アクティブ光ケーブル(AOC)市場は細分化されています。調査対象となった市場の主な企業は、ACT、Broadcom Inc.、Sumitomo Electric、JPC Connectivityなどです。同市場の企業は、サービス提供を強化し、持続可能な競争優位性を獲得するために、提携、契約、技術革新、買収などの戦略を採用しています。

- 2024年1月光ファイバ・ソリューション分野で著名なOFSは、最新のイノベーション製品であるLaserWaveデュアルバンドOM4+マルチモード光ファイバを発表しました。既に高く評価されているOM4及びOM5のラインナップに加えられたこのマルチモード光ファイバは、帯域幅、減衰及び形状において新たな基準を打ち立てます。LaserWave Dual-Band OM4+は、双方向(BiDi)アプリケーション用に綿密に作られた、プレミアムでありながらコスト効率の高いファイバーとして際立っています。このファイバーは、高密度、低電力のマルチモードリンクを強化するために設計されています。また、850nmと910nmの両方の波長でOM5と同等の性能を発揮することができ、双方向伝送に不可欠です。これは、800G-SR4.2や1.6T-SR8.2を含むテラビットBiDiイーサネットのような最先端アプリケーションに不可欠な指標である、一貫した100メートルの到達距離を保証します。

- 2024年1月Telstra InternationalはTrans Pacific Networks(TPN)と提携し、米国とシンガポールを直接結ぶ初の海底ケーブルとなるEchoケーブルシステムを導入。エコー・ケーブルの最初のセグメントは、グアムと米国を結ぶ専用の光ファイバー回線で、2024年半ばに開通し、その後のセグメントは2025年に開通する予定。完成すれば、カリフォルニア、ジャカルタ、シンガポール、グアムをシームレスに結ぶことになります。テルストラ社は、このシステムは新しいルートを開拓するだけでなく、低遅延、高速、堅牢な耐障害性を特徴とするネットワーク・インフラを約束すると強調しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- マクロ経済シナリオの分析(景気後退、ロシア・ウクライナ危機など)

- COVID-19パンデミックの影響と回復の評価

第5章 市場力学

- 市場促進要因

- 光ネットワークの高速化に向けた電気通信分野の変化

- 広帯域化のニーズの高まり

- データセンターにおけるアクティブ光ケーブルの需要増加

- デジタル化と5G接続の高い普及率

- 市場の課題

- 多大な初期コストと光ネットワーク・セキュリティ・ファイバー・ハッキング

- 消費電力への懸念

- 技術的専門知識の不足

- 価格と技術仕様の分析

- ダイレクトアタッチケーブル(アクティブおよびパッシブ)対アクティブ光ケーブルに関する技術洞察

- 世界貿易分析

- AOCの最も一般的なフォームファクター仕様に関する主な洞察

- AOCの各種プロトコルタイプに関する洞察

第6章 市場セグメンテーション

- 用途別

- データセンター

- 通信

- 高性能コンピューティング(HPC)

- 家庭用電子機

- 産業用用途

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- アジア

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- JPC Connectivity

- Shenzhen Sopto Technology Co. Ltd

- Linkreal Co. Ltd

- Broadcom

- Sumitomo Electric Lightwave Inc.

- Black Box

- ACT

- IOI Technology Corporation

- ETU-Link Technology Co. Ltd

- Amphenol Corporation

第8章 市場機会と今後の動向

The Global Active Optical Cables Market size is estimated at USD 4.11 billion in 2024, and is expected to reach USD 7.75 billion by 2029, growing at a CAGR of 13.5% during the forecast period (2024-2029).

The active optical cables market is currently experiencing robust growth, and it is expected to grow further owing to the large-scale adoption of cloud-based services, digitalization, 5G, data centers, and other applications.

Key Highlights

- The active optical cable (AOC) market is mostly driven by the increasing need for high-speed data transmission in a variety of applications, including data centers, telecommunications, and consumer electronics. The growing need for data through various applications is expected to drive the demand for the AOC Market.

- The data center market is growing rapidly owing to the large-scale application of cloud technologies, digitalization, and growing demand for AI/ML. According to Cloudscene, a telecommunication services provider, there are approximately 10,978 data center locations worldwide as of December 2023, with numbers growing rapidly. Data centers require robust and high-speed internet connectivity. Therefore, the growth in the data center market is anticipated to drive the AOC market as well.

- 5G implementation is poised to meet the escalating demand for efficient communication, which is crucial for enhancing digital operations. While 5G's broader wavelength enables rapid data transmission, its signals are limited in range compared to 3G and 4G. Consequently, a robust 5G network necessitates a dense array of cell towers, each reliant on high-speed cables for signal transmission, thereby bolstering the demand for the AOC market.

- GSMA forecasts that 5G connections will account for over half (51%) of all mobile connections by 2029, climbing to 56% by the decade's end, solidifying 5G as the leading connectivity technology. 5G has outpaced all previous mobile generations in its rollout, exceeding 1.6 billion connections by the end of 2023, and it is projected to reach 5.5 billion by 2030. Consequently, as 5G continues its rapid expansion, the global active optical cables market is poised for significant growth in the near future.

- Concerns over the security of optical transmissions and potential vulnerabilities in sensitive data applications may impede the widespread adoption of AOCs. Additionally, AOCs often pose greater maintenance and repair challenges compared to traditional copper cables, particularly in sectors requiring swift service interventions.

Global Active Optical Cables (AOC) Market Trends

Rising Demand for Active Optical Cable in Data Centers to Drive the Market

- The global active optical cable (AOC) market has witnessed significant growth in recent years, propelled by the surging demand for high-speed data transmission across industries. With technological advancements, the emphasis on efficient and dependable connectivity solutions has never been more critical. Active optical cables (AOCs) stand out as high-speed cabling solutions, incorporating active elements like lasers and photodiodes directly into the cable assembly. These components are pivotal, facilitating the transmission of optical signals through fiber optic cables. In the realm of data centers, the term '200G AOC' specifically denotes cables engineered to support data rates of 200 gigabits per second (Gbps).

- Additionally, in high-performance computing (HPC) settings demanding substantial computational power, the 200G AOC facilitates swift data exchange between processors and storage units. Organizations leverage high-performance computing for parallel processing, empowering them to execute advanced programs like AI and data analytics. Data centers, especially those emphasizing AI and machine learning, stand to gain significantly from HPC.

- The rise of cloud computing within organizations significantly drives the data center market. According to the Flexera State of the Cloud Report 2023, 72% of companies have adopted hybrid clouds. Yet, this transition frequently means moving beyond conventional private and public cloud infrastructures.

- Active optical cables (AOCs) are pivotal in connecting data center cabling racks and switches, enabling seamless communication between switches and servers. Typically, data centers first install switches, then implement structured cabling, and finally, select the appropriate interconnect products for network access. Copper cables are the most cost-effective choice for short distances, defined as under 90 meters for 10G and under 10 meters for 40G. For medium distances spanning under 500 meters for 10G and 150 meters for 40G, multimode VCSEL (vertical cavity surface emitting laser) transceivers are favored, often complemented by AOCs.

- India's data center market is set for a significant uptick, with forecasts pointing to a climb to USD 4.6 billion by 2025. This growth is fueled by several factors: a growing domestic internet user base, rising demands for cloud computing, government initiatives driving digitalization, and a shift toward localization by digital service providers. Notably, India's data center sector boasts a significant cost advantage, both in its development and operational phases, compared to more mature markets. Currently, key data center hubs are primarily located in Mumbai, Bengaluru, Chennai, Delhi (NCR), Hyderabad, and Pune, with emerging centers in Calcutta, Kerala, and Ahmedabad. As investments in data centers expand, so does the demand for ancillary infrastructure services covering IT, electrical, mechanical, and general construction throughout India.

North America to Hold a Major Share

- North America boasts the world's largest data center market, currently experiencing a notable rise in hyperscale data center construction. This surge is primarily fueled by the escalating demand for cloud services and the ongoing digital transformation. Recent data from Cloudscene, as of March 2024, highlights the United States as the global leader, housing 5,381 reported data centers. Germany and the United Kingdom follow closely, with 521 and 514 centers, respectively. Historically, copper cables have been the go-to for networking links between servers, routers, and switches. With the expanding data center landscape, the demand for active copper cables in the region is set to rise.

- The demand for new data centers in the United States remains strong, with fresh projects unveiled almost weekly. In March 2024, Amazon disclosed its plan to invest a hefty USD 650 million in acquiring a data center adjacent to the Berwick nuclear power plant. This initiative, confirmed by Talen Energy, the operator of the Susquehanna Steam Electric Station in Salem Township, will see Amazon's web services arm spearhead the development of the new data center.

- The development of high-speed internet in the United States is also a major factor driving the global AOC market. The US Department of Agriculture (USDA) has pledged a total of USD 97 million to assist operators in establishing networks. These networks are aimed at areas lacking connectivity or falling below the US government's set target of 100 Mbps download and 20 Mbps upload speeds for all American households by 2027. This initiative is set to enhance services for 22,000 subscribers across 11 states.

- Green City's Northeast Missouri Rural Telephone Company secured a USD 13.7 million loan to transition six exchanges from copper to fiber-to-the-premises technology. This initiative involves laying down approximately 500 route miles of fiber, with the aim of enhancing services for 1,063 subscribers.

- In October 2023, the US Federal Communications Commission (FCC) initiated a significant investment of approximately USD 18.28 billion to strengthen rural broadband infrastructure. This funding, allocated for a 15-year program commencing in January 2024, targets the deployment of 100/20 Mbps broadband to over 700,000 locations. Furthermore, it aims to upgrade existing services for approximately 2 million locations spread across 44 states. This ambitious broadband expansion is set to have a profound impact on the AOC market.

Global Active Optical Cables (AOC) Industry Overview

The active optical cables (AOC) market is fragmented in nature. Some major players in the market studied are ACT, Broadcom Inc., Sumitomo Electric, JPC Connectivity, etc. Players in the market are adopting strategies such as partnerships, agreements, innovations, and acquisitions to enhance their service offerings and gain sustainable competitive advantage.

- January 2024: OFS, a prominent figure in the fiber optic solutions realm, unveiled its latest innovation: the LaserWave Dual-Band OM4+ Multimode Optical Fiber. This addition to the lineup, alongside the already esteemed OM4 and OM5 offerings, sets new benchmarks in bandwidth, attenuation, and geometry. The LaserWave Dual-Band OM4+ stands out as a premium yet cost-effective fiber, meticulously crafted for bidirectional (BiDi) applications. It is tailored to bolster the upcoming wave of high-density, low-power multimode links. Its capability to deliver performance akin to OM5 at both 850 nm and 910 nm wavelengths is also noteworthy, which is crucial for bidirectional transmissions. This ensures a consistent 100-meter reach, a vital metric for cutting-edge applications like Terabit BiDi Ethernet, including 800G-SR4.2 and 1.6T-SR8.2.

- January 2024: Telstra International teamed up with Trans Pacific Networks (TPN) to introduce the Echo cable system, marking the inaugural subsea cable directly linking the United States and Singapore. The initial segment of the Echo cable, a dedicated fiber-optic line linking Guam and the United States, is set for a mid-2024 debut, with subsequent segments slated for 2025. Upon completion, the cable will seamlessly link California, Jakarta, Singapore, and Guam. Telstra emphasizes that this system will not only forge a new route but also promise a network infrastructure characterized by low latency, high speeds, and robust resilience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Analysis of Macro-economic Scenarios (Recession, Russia-Ukraine Crisis, etc.)

- 4.3 An Assessment of the Impact of and Recovery from COVID-19 Pandemic

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Change in the Telecom Sector Toward Faster Optical Networks

- 5.1.2 Increased Need for Higher Bandwidth

- 5.1.3 Rising Demand for Active Optical Cable in Data Centers

- 5.1.4 Digitalization and High Adoption of 5G Connectivity

- 5.2 Market Challenges

- 5.2.1 Significant Initial Cost and Optical Network Security Fiber Hacking

- 5.2.2 Significant Power Consumption Concerns

- 5.2.3 Lack of Technical Expertise

- 5.3 Analysis of Pricing and Technical Specifications

- 5.4 Technology Insights on Direct Attach Cables (Active and Passive) vs. Active Optical Cable

- 5.5 Global Trade Analysis

- 5.6 Key Insights into Most Common Form Factor Specifications of AOC

- 5.7 Key Insights into Various Protocol Types of AOC

6 MARKET SEGMENTATION

- 6.1 By Application Area

- 6.1.1 Data Center

- 6.1.2 Telecommunication

- 6.1.3 High-Performance Computing (HPC)

- 6.1.4 Consumer Electronics

- 6.1.5 Industrial Applications

- 6.1.6 Other Applications

- 6.2 By Region

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 Australia and New Zealand

- 6.2.4 Latin America

- 6.2.5 Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 JPC Connectivity

- 7.1.2 Shenzhen Sopto Technology Co. Ltd

- 7.1.3 Linkreal Co. Ltd

- 7.1.4 Broadcom

- 7.1.5 Sumitomo Electric Lightwave Inc.

- 7.1.6 Black Box

- 7.1.7 ACT

- 7.1.8 IOI Technology Corporation

- 7.1.9 ETU-Link Technology Co. Ltd

- 7.1.10 Amphenol Corporation