|

市場調査レポート

商品コード

1694038

欧州、中東、アフリカの周波数制御とタイミング装置:市場シェア分析、産業動向、成長予測(2025~2030年)EMEA Frequency Control And Timing Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州、中東、アフリカの周波数制御とタイミング装置:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 204 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

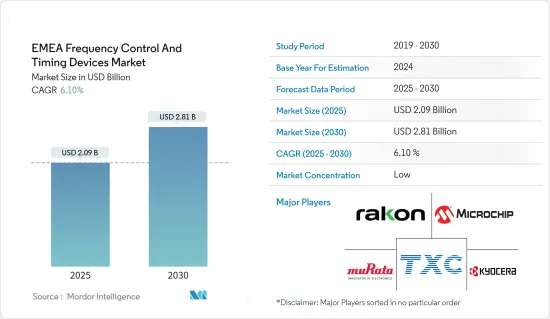

欧州、中東、アフリカの周波数制御とタイミング装置市場規模は2025年に20億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.1%で、2030年には28億1,000万米ドルに達すると予測されます。

周波数制御とタイミング装置市場は、ロシア・ウクライナ紛争と景気減速により大きな混乱に直面しました。インフレと金利の上昇は個人消費を抑制し、半導体需要を減退させ、FCTDの成長を鈍化させました。紛争を受け、欧州は防衛・航空宇宙セグメントに重点を移したため、FCTDの需要が高まり、新たな成長の道が開かれました。

主要ハイライト

- スマートホーム技術の採用拡大が市場成長に明るい展望をもたらします。スマートホームは、スマートサーモスタット、照明システム、防犯カメラ、民生用電子機器製品などの相互接続された装置で構成され、これらの装置は通信してシームレスに動作する必要があります。周波数制御とタイミング装置は、これらの装置の同期を確実にし、データ伝送、制御信号、イベントスケジューリングに正確なタイミング信号を記載しています。

- GSMAのレポートによると、MENA地域におけるスマートフォンの普及率は、2018年の54%から2025年には74%に増加すると予想されています。2025年までに、サハラ以南のアフリカではスマートフォンが全接続の61%を占めるようになります。注目すべきは、5G接続数が2025年までにMENA地域で4,500万、サハラ以南アフリカで4,100万に達する見込みであることです。

- ロボットは、同期動作や時間に敏感な作業のために発振器を使用します。この地域における産業用ロボットの利用は、精度と適応性の向上、製品ダメージの最小化、スピードの向上、最終的な業務効率の最適化などの能力により、多くのエンドユーザーや用途で増加傾向にあります。

- 先進的な自動車用途の台頭は、自動車産業における欧州、中東、アフリカの周波数制御とタイミング装置の成長の大きな原動力となっています。ADASの採用が増加していることも、市場成長に大きく寄与しています。これらのシステムは、自動緊急ブレーキ、車線逸脱警告、アダプティブクルーズコントロールのためのリアルタイムのセンサデータ処理に依存しています。周波数制御装置は、これらのシステムが迅速かつ正確に応答するための正確なタイミングを記載しています。

- 周波数制御とタイミング装置市場は、エレクトロニクス産業の中でも重要なセグメントであり、さまざまな用途に不可欠なコンポーネントを提供しています。しかし、これらの装置を開発・生産するためのコストが高いことが、市場成長の課題となっています。

- GDP成長、政府予算の制約、地政学的要因、財政施策などの要因は、欧州、中東、アフリカの軍事支出に大きな影響を与えます。NATOによると、2023年のスペインの国防支出は191億8,000万米ドルと推定され、2014年以来最高の支出です。前年の支出は149億米ドルと推定されました。このような数字によりスペインはNATO加盟国の中で8番目に高い防衛支出となりました。

欧州、中東、アフリカの周波数制御とタイミング装置市場動向

自動車産業がエンドユーザーとして急成長

- 自動車産業では、周波数制御とタイミング装置は、アダプティブクルーズコントロール、車線支援、衝突回避のためのADAS、スムーズな音楽再生と正確なGPS機能のためのインフォテインメントシステム、リアルタイム追跡とコネクテッドビークルのためのテレマティクスなどに使用されています。また、電気自動車では、電気モーターの動作を調整するために使用されます。

- 自動車セグメントは、欧州、中東、アフリカの周波数制御とタイミング装置市場で事業を展開するベンダーにとって有望な市場です。

- 自律走行、電動化、接続性、シェアード・ビークルが自動車セグメントの市場成長を促進する動向です。今日の自動車には、用途プロセッサからマイクロコントローラ、FPGAに至るまで、デジタルコンポーネントの安定した正確な周波数制御のために精密タイミング技術に依存する高性能電子システムがいくつか搭載されています。周波数制御とタイミング装置の大手プロバイダであるSiTimeによると、一般的な自動車では、電気・電子システムを円滑に動作させるために最大70個のタイミング装置が使用されています。

- 欧州、中東、アフリカの市場成長は、消費者の嗜好の変化、技術の進歩、電気自動車の人気の高まりに起因すると考えられます。自動車産業が電気自動車やコネクテッドカーにシフトしているため、発振器に対する需要が高まると考えられます。このため、メーカーやサプライヤーは、自動車の安全性、性能、競合を確保するために革新的な技術に投資する必要があります。

- 例えば、欧州連合(EU)の自動車市場は2023年に前年比13.9%の大幅な成長を遂げ、通年の総販売台数は1,050万台となりました。このデータは欧州自動車工業会(ACEA)が発表したものです。

- バッテリー電気自動車は、2023年に購入者の間で3番目に人気のある選択肢に浮上しました。12月だけで、その市場シェアは18.5%に急上昇し、通年の全体シェア14.6%に貢献しました。これは、13.6%にとどまったディーゼル車の安定した市場シェアを上回りました。ガソリン車の市場シェアは35.3%で優位を保ち、ハイブリッド電気自動車は25.8%の圧倒的な市場シェアで2位を確保しました。

ドイツが主要市場シェアを占める

- ドイツは、自動化、データ交換、IoT技術が製造業に融合するインダストリー4.0をリードしています。こうした「スマート工場」では、正確なタイミングが重要です。機械、ロボット、センサを同期させ、生産と資源効率を最適化します。インダストリー4.0が定着するにつれ、産業オートメーションとスマート製造における先進的タイミング装置のニーズが急増します。

- ドイツの民生用電子機器・ウェアラブル装置市場は、革新的なガジェットやコネクテッド装置に対する消費者の需要が牽引しています。スマートフォン、ウェアラブル装置、民生用電子機器製品には、クロック同期、データ処理、接続用のタイミング装置が組み込まれていることが多いです。消費者の嗜好がインテリジェントでコネクテッドな装置にシフトするにつれて、最新の民生用電子機器製品の要件を満たす可能性のあるコンパクトで低消費電力のタイミングソリューションに対する需要が絶え間なく高まっています。

- GSMA Intelligenceが提供するデータによると、ドイツは2025年までに、接続数で欧州の主要なスマートフォン市場に浮上し、その市場規模は1億500万米ドルに達すると予測されています。ドイツのスマートフォン普及率は、2021年の80%から2025年には84%に上昇すると予想されています。

- ドイツでは、防衛・航空宇宙セグメントで高性能タイミングソリューションの需要が高まっています。これらのソリューションは、レーダーシステム、通信ネットワーク、衛星ペイロードに応用されています。新たな脅威と戦うための防衛ニーズの進化に伴い、需要は先進的タイミング装置へとシフトしています。これらの装置は、堅牢な性能を提供し、強化された信頼性とセキュリティ機能を誇らなければならないです。タイミングソリューションを専門とするサプライヤーは、これらのミッション・クリティカルな用途の厳しい要求を満たすように製品を調整することで、利益を得ることができます。

- 上記の要約に従えば、防衛産業の発展に向けた政府の過剰投資は、研究市場に新たな成長機会を生み出すことになります。SIPRIによると、2023年、政府は防衛予算に約3.08%を投資しました。

- 同国は、イノベーションと技術開発を推進するため、産・学・研究機関の連携を促進しています。共同研究イニシアチブとパートナーシップは、タイミング装置のサプライヤーが最先端の研究プロジェクトに参加し、新技術を開発し、革新的なソリューションを商業化する機会を創出します。共同ネットワークを通じて利用可能な専門知識とリソースを活用することで、企業は競合を獲得し、先進的なタイミングソリューションの開発と採用を加速することができます。このような動向と取り組みが、予測期間中の市場成長を促進すると期待されます。

欧州、中東、アフリカの周波数制御とタイミング装置産業概要

欧州、中東、アフリカの周波数制御とタイミング装置市場は、Murata Manufacturing、京セラ、Rakon Limited、Microchip Technology Inc.、TXC Corporationなどの主要企業が存在し、細分化されています。市場の主要企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、買収や提携などの戦略を採用しています。

2024年4月、先端電子部品メーカーである京セラAVXは、KYOCERA AVX Components Corporation(Erie)の名称で、高品質・低ノイズの水晶振動子周波数制御製品の新しい製造・設計センターを発表しました。新設された製造施設では、特許を取得した比類のない低消費電力OCXO(オーブン制御水晶発振器)を120万個以上製造できます。また、TCXO(温度制御水晶発振器)とVCXO(電圧制御水晶発振器)も生産します。

2024年2月、Error Exchange OCXO(MercuryXE2)は、ラコンが最近発売したMercury小型IC-OCXOのバージョンです。周波数誤差交換処理とエージング補償を組み込むことにより、ネットワークシンクロナイザ評価ボード上のシステムの電流同期能力を向上させ、ホールドオーバー性能を高めます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響とマクロ経済動向の産業への影響

第5章 市場力学

- 市場の促進要因

- 新興用途の増加(IoT装置、ロボットなど)

- 先進自動車用途からの需要増加

- 市場抑制要因

- 開発コストの高さ

第6章 市場セグメンテーション

- タイプ別

- 水晶振動子

- 発振器

- 温度補償型水晶発振器(TCXO)

- 電圧制御水晶発振器(VCXO)

- オーブン制御水晶発振器(OCXO)

- MEMS発振器

- その他の発振器

- 共振器

- ソー・フィルター

- リアルタイムクロック

- エンドユーザー産業別

- 自動車

- コンピュータと周辺機器

- 通信/サーバー/データストレージ

- コンシューマーエレクトロニクス

- 産業

- 防衛・航空宇宙

- IoT

- その他

- 国別

- 英国

- ドイツ

- フランス

- イタリア

- GCC諸国

- 南アフリカ

第7章 競合情勢

- 企業プロファイル

- Murata Manufacturing Co. Ltd

- Kyocera Corporation

- Rakon Limited

- Microchip Technology Inc.

- TXC Corporation

- Seiko Epson Corporation

- Daishinku Corporation

- Hosonic Technology(group)Co. Ltd

- Nihon Dempa Kogyo Co. Ltd

- Sitime Corporation

- Stmicroelectronics NV

- Texas Instruments Incorporated

- NXP Semiconductors NV

- Abracon Llc

- Jauch Quartz

- IQD Frequency Products Ltd

- Euroquartz Ltd

- Geyer Electronic GmbH

- ACT

第8章 投資分析

第9章 市場機会と今後の動向

The EMEA Frequency Control And Timing Devices Market size is estimated at USD 2.09 billion in 2025, and is expected to reach USD 2.81 billion by 2030, at a CAGR of 6.1% during the forecast period (2025-2030).

The frequency control and timing device market faced significant disruptions due to the Russo-Ukraine conflict and an economic slowdown. Rising inflation and interest rates curtailed consumer spending, dampened semiconductor demand, and slowed the growth of FCTDs. In response to the conflict, Europe has shifted its focus toward the defense and aerospace sectors, leading to heightened demand for these components and opening up new growth avenues.

Key Highlights

- The rising adoption of smart home technologies creates a positive outlook for market growth. Smart homes consist of interconnected devices such as smart thermostats, lighting systems, security cameras, and appliances that need to communicate and operate seamlessly together. Frequency control and timing devices ensure the synchronization of these devices, providing accurate timing signals for data transmission, control signals, and event scheduling.

- According to the GSMA report, smartphone adoption in the MENA region is expected to increase from 54% in 2018 to 74% in 2025. By 2025, smartphones will make up 61% of all connections in Sub-Saharan Africa. Noticeably, the number of 5G connections is expected to reach 45 million and 41 million by 2025 in the MENA and Sub-Saharan African regions, respectively.

- Robots use oscillators for synchronized operation and time-sensitive tasks. The utilization of industrial robots in the region has been on the rise in numerous end-users and applications due to their ability to improve precision and adaptability, minimize product damage, enhance speed, and ultimately optimize operational efficiency.

- The rise of advanced automotive applications is a significant driver for the growth of EMEA frequency control and timing devices in the automotive industry. The increasing adoption of ADAS is a substantial contributor to the market growth. These systems rely on real-time sensor data processing for automatic emergency braking, lane departure warning, and adaptive cruise control. Frequency control devices provide the accurate timing for these systems to respond promptly and accurately.

- The frequency control and timing devices market is a critical segment within the electronics industry, providing essential components for various applications. However, the high costs of developing and producing these devices challenge the market's growth.

- Factors like GDP growth, government budget constraints, geopolitical factors, and fiscal policies significantly impact military spending in EMEA. According to NATO, in 2023, Spain's defense expenditure was estimated at USD 19.18 billion, the highest spending since 2014. The expenditure was estimated to be USD 14.90 billion in the previous year. Such figures gave Spain the eighth-highest defense expenditure among NATO members.

EMEA Frequency Control And Timing Devices Market Trends

Automotive Industry to be the Fastest Growing End User

- In the automotive industry, frequency control and timing devices are used in ADAS for adaptive cruise control, lane assistance, and collision avoidance, infotainment systems for smooth music playback and accurate GPS functionality, telematics for real-time tracking and connected vehicles, and others. They are also used in electric vehicles to coordinate the operations of electric motors.

- The automotive segment presents promising opportunities for vendors operating in the EMEA frequency control and timing devices market, as the importance of these devices has been increasing in modern automobiles.

- Autonomous driving, electrification, connectivity, and shared vehicles are the trends driving market growth in the automotive sector. Automobiles today contain several high-performance electronic systems that rely on precision timing technology for stable, accurate frequency control of digital components, ranging from application processors to microcontrollers to FPGAs. According to SiTime, a leading frequency control and timing device provider, a typical automobile uses up to 70 timing devices to keep the electrical and electronic systems operating smoothly.

- The market growth in the EMEA region may be attributed to changing consumer preferences, technological advancements, and the increasing popularity of electric vehicles. With the automotive sector shifting toward electric and connected vehicles, there will be a growing demand for oscillators. This will require manufacturers and suppliers to invest in innovative technologies to ensure vehicle safety, performance, and competitiveness.

- For instance, the car market in the European Union experienced a significant growth of 13.9% in 2023 compared to the previous year, resulting in a total sales volume of 10.5 million units for the entire year. This data was reported by the European Automobile Manufacturers' Association (ACEA).

- Battery-electric cars emerged as the third most popular choice among buyers in 2023. In December alone, their market share skyrocketed to 18.5%, contributing to an overall share of 14.6% for the entire year. This surpassed the steady market share of diesel cars, which remained at 13.6%. Petrol cars maintained their dominance with a market share of 35.3%, while hybrid-electric cars secured the second position with a commanding market share of 25.8%.

Germany to Hold Major Market Share

- Germany leads the way in Industry 4.0, where automation, data exchange, and IoT technologies converge in manufacturing. In these 'smart factories,' precise timing is crucial. It synchronizes machines, robotics, and sensors, optimizing production and resource efficiency. As Industry 4.0 takes hold, the need for advanced timing devices in industrial automation and smart manufacturing surges.

- Germany's consumer electronics and wearable devices market is driven by consumer demand for innovative gadgets and connected devices. Smartphones, wearables, and consumer electronics often incorporate timing devices for clock synchronization, data processing, and connectivity. As consumer preferences shift towards intelligent and connected devices, there's a continuous demand for compact, low-power timing solutions that may meet the requirements of modern consumer electronics products.

- According to data provided by GSMA Intelligence, Germany is projected to emerge as the leading smartphone market in Europe in terms of the number of connections, with a value of USD 105 million, by 2025. Germany's smartphone adoption rate is expected to rise from 80% in 2021 to 84% in 2025.

- In Germany, the defense and aerospace sectors increasingly demand high-performance timing solutions. These solutions find applications in radar systems, communication networks, and satellite payloads. With evolving defense needs to combat emerging threats, the demand is shifting toward advanced timing devices. These devices must deliver robust performance and boast enhanced reliability and security features. Suppliers specializing in timing solutions stand to benefit by tailoring their offerings to meet the stringent demands of these mission-critical applications.

- Adhering to the above synopsis, the government's excess investments towards advancing its defense industry will create new growth opportunities for the studied market. According to SIPRI, in 2023, the government invested around 3.08% in its defense budget.

- The country fosters collaborations between industry, academia, and research institutions to drive innovation and technology development. Collaborative research initiatives and partnerships create opportunities for suppliers of timing devices to participate in cutting-edge research projects, develop new technologies, and commercialize innovative solutions. By leveraging the expertise and resources available through collaborative networks, companies can gain a competitive edge and accelerate developing and adopting advanced timing solutions. Such trends and initiatives are expected to drive the market growth in the projected period.

EMEA Frequency Control And Timing Devices Industry Overview

The EMEA Frequency Control And Timing Devices Market is fragmented with the presence of key players like Murata Manufacturing Co. Ltd, Kyocera Corporation, Rakon Limited, Microchip Technology Inc., and TXC Corporation. Key players in the market are adopting strategies such as acquisitions and partnerships to enhance their product offerings and gain sustainable competitive advantage.

In April 2024, KYOCERA AVX, a manufacturer of advanced electronic components, unveiled a new manufacturing and design center for high-quality, low-noise quartz crystal frequency control products under the name KYOCERA AVX Components Corporation (Erie). The newly established production facility could manufacture over 1.2 million patented and unparalleled low-power OCXO (oven-controlled crystal oscillators). It would produce a range of TCXO (temperature-computed crystal oscillators) and VCXO (voltage-computed crystal oscillators).

In February 2024, the Error Exchange OCXO (MercuryXE2) is a version of Rakon's recently launched Mercury compact IC-OCXO. It improves the system's current synchronization abilities on a network synchronizer evaluation board by incorporating frequency error exchange processing and aging compensation, thereby increasing the holdover performance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Macro Economic Trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of Emerging Applications (such as IoT Devices, Robotics, etc.)

- 5.1.2 Rising Demand from Advanced Automotive Applications

- 5.2 Market Restraint

- 5.2.1 High Cost of Development

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Crystals

- 6.1.2 Oscillators

- 6.1.2.1 Temperature Compensated Crystal Oscillator (TCXO)

- 6.1.2.2 Voltage-controlled Crystal Oscillator (VCXO)

- 6.1.2.3 Oven-controlled Crystal Oscillator (OCXO)

- 6.1.2.4 MEMS Oscillator

- 6.1.2.5 Other Types of Oscillators

- 6.1.3 Resonators

- 6.1.4 Saw Filters

- 6.1.5 Real Time Clocks

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Computer and Peripherals

- 6.2.3 Communications/Server/Data Storage

- 6.2.4 Consumer Electronics

- 6.2.5 Industrial

- 6.2.6 Defense and Aerospace

- 6.2.7 IoT

- 6.2.8 Other End-user Industries

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 GCC

- 6.3.6 South Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Murata Manufacturing Co. Ltd

- 7.1.2 Kyocera Corporation

- 7.1.3 Rakon Limited

- 7.1.4 Microchip Technology Inc.

- 7.1.5 TXC Corporation

- 7.1.6 Seiko Epson Corporation

- 7.1.7 Daishinku Corporation

- 7.1.8 Hosonic Technology (group) Co. Ltd

- 7.1.9 Nihon Dempa Kogyo Co. Ltd

- 7.1.10 Sitime Corporation

- 7.1.11 Stmicroelectronics NV

- 7.1.12 Texas Instruments Incorporated

- 7.1.13 NXP Semiconductors NV

- 7.1.14 Abracon Llc

- 7.1.15 Jauch Quartz

- 7.1.16 IQD Frequency Products Ltd

- 7.1.17 Euroquartz Ltd

- 7.1.18 Geyer Electronic GmbH

- 7.1.19 ACT