|

市場調査レポート

商品コード

1911828

詰め替え可能で再利用可能な包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Refillable And Reusable Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 詰め替え可能で再利用可能な包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

概要

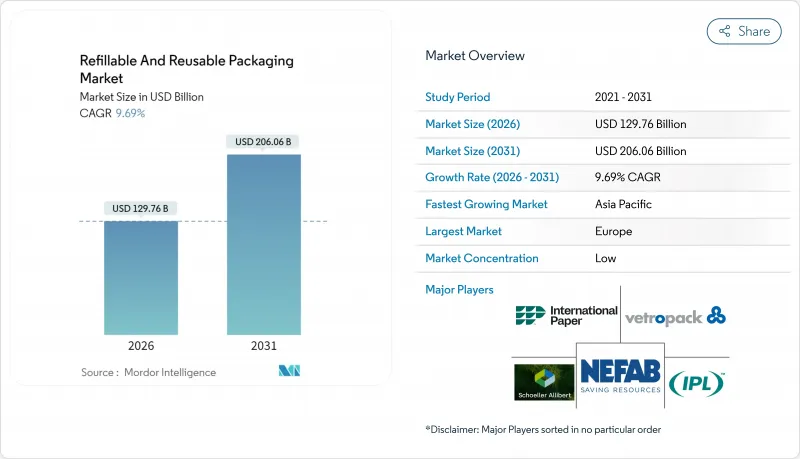

詰め替え可能で再利用可能な包装市場は、2025年の1,183億米ドルから2026年には1,297億6,000万米ドルへ成長し、2026年から2031年にかけてCAGR9.69%で推移し、2031年までに2,060億6,000万米ドルに達すると予測されております。

循環型経済に関する規制、サプライチェーンのコスト圧力、消費者の持続可能性への嗜好が先進国と新興国双方で一致しつつあることから、詰め替え可能かつ再利用可能な包装材市場は加速しています。欧州における法整備の確実性、中国におけるグリーン小包義務化、洗浄・追跡ソリューションの技術的ブレークスルーが、インフラの不足が依然として残る中でも採用を加速させています。企業はリターナブル資産を、物流総費用の削減、原材料価格変動の抑制、ブランド価値強化の手段として位置付けており、投資家は測定可能な廃棄物削減に対して低コスト資本を提供しています。競合活動は、資産活用率とコンプライアンス報告を最大化するため、IoTセンサーの組み込み、予測分析、ターンキー洗浄サービスの提供に焦点を当てています。

世界の詰め替え可能・再利用可能包装市場の動向と洞察

循環型経済義務化に向けた法的推進

拡大生産者責任制度により、企業は製品寿命終了時のコストを内部化することが求められています。欧州連合(EU)は2025年までに65%の材料リサイクル率、2030年までに輸送用包装材の90%再利用を義務付けています。中国の宅配便規制では、物流事業者が市内配送小包の95%で再利用可能包装を達成することが求められており、これによりリターナブルコンテナの潜在市場規模は120億米ドルに拡大します。廃棄費用や炭素価格の上昇に伴い、これらの規制は総所有コストモデルを再利用可能な形式へと導いています。

クローズドループ型サプライチェーンによるコスト削減

運用データにより、再利用可能な資産が運賃、労働時間、償却費を削減することが確認されています。CHEPの自動車向けプログラムでは、トラック稼働率を95%に高め、積載時間を75%削減し、一次サプライヤー各社の年間コストを230万米ドル削減しました。CEVAロジスティクス社は、IoT追跡可能なコンテナが使い捨てカートンに取って代わったことで、排出量を60%削減し、短期間で投資回収を実現したと報告しています。高速循環システムでは、投資は通常18ヶ月以内に回収されます。

高いリバースロジスティクスコスト

返品ネットワークは、特にルート密度が低い地域において、出荷フローと比較して取扱費用を3倍に膨らませる可能性があります。コールドチェーン返品はさらにコストを押し上げ、一部のブランドは再利用プログラムを大都市圏の主要ルートに限定せざるを得ない状況です。

セグメント分析

2025年時点で、プラスチックは再充填可能・再利用可能包装市場の48.85%を占めました。これは、自動化システムとの互換性を保ちながら高サイクル数に耐えるポリプロピレンおよびポリエチレン容器によるものです。軽量設計は貨物排出量と総コストを削減します。ガラスは重量があるもの、高級飲料やスキンケア製品が純度と高級感を重視するため、12.18%のCAGRを記録しています。Vetropack社の軽量フリント技術は、ブランド美観を保護しつつ輸送コストの差を縮めています。金属ドラムやトートは、耐久性が重量を上回る化学品分野で主力であり続け、紙製段ボールは自動車部品輸送において特殊な役割を担っています。

食品接触用再生プラスチックに対する持続可能性の検証により、一部ブランドがガラスや金属へ移行する可能性はありますが、IoTタグを組み込んだ先進ポリマーは高速循環システムにおけるプラスチックの役割を確固たるものにします。結果として、詰め替え可能・再利用可能な包装市場は、材料科学の進歩に伴い、コスト効率、ブランディングの必要性、規制順守のバランスを取っています。

地域別分析

欧州は2025年時点で詰め替え可能・再利用可能包装市場の34.08%を占めており、これは数十年にわたる政策の積み重ねとインフラ投資を反映しています。EUが2030年までに輸送用包装材の90%再利用を義務付ける方針は、企業の長期予算編成の基盤となります。ドイツでは共同利用連合によりクレートの回転期間が2.4日に短縮され、フランスでは高級ブランドと提携し高級ガラス製詰め替えシステムの試験運用が進められています。英国は柔軟性のあるプラスチックのリサイクル能力強化に5,000万米ドルを投入し、国内循環型経済を強化しています。

アジア太平洋地域は2031年までCAGR10.55%で成長を牽引します。中国の都市内小包95%再利用規制により、ラストマイル配送用自転車に適合する折り畳み式トートバッグ市場が120億米ドル規模に拡大します。日本では生産者責任制度の対象を電子機器に拡大し、再利用可能な輸送用包装材の需要を促進。インドでは製造業の拡大に伴い、リターナブル自動車ラックの需要が増加。韓国ではクリーンルーム用コンテナプールにIoTタグとブロックチェーン追跡システムを導入。東南アジアでは地域洗浄拠点への海外投資が流入。

北米では、企業の気候変動対策公約と州レベルの拡大生産者責任法により着実な進展が見られます。ディスパッチ・グッズ社は、レストラン向け容器共有サービスを通じ、3,350億米ドル規模の包装廃棄物問題解決に向けベンチャー資金を調達しました。カナダでは資源産業でリフィル試験事業が推進され、メキシコでは100年以上の歴史を持つガラス瓶循環システムがアプリベースの回収システムへ拡大。ブラジルとメキシコでは飲料用木箱の伝統と都市部の環境意識の高まりを背景に、ラテンアメリカで新たな展開が始まっています。中東・アフリカ地域は未だ発展途上ながら、小売業者がクローズドループ方式のウォータージャグフリートを試験導入する動きに注目が集まっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 循環型経済義務化に向けた立法的推進

- クローズドループ型サプライチェーンによるコスト削減効果

- 持続可能なブランドに対する消費者の嗜好

- 新興のIoT対応型リフィル・オン・ザ・ゴー小売

- ESG連動型ゼロ・ウェイスト企業ファイナンス

- ポリマー間洗浄技術の革新

- 市場抑制要因

- 高いリバースロジスティクスのコスト

- 食品接触再利用基準の曖昧さ

- 熱帯地域における微生物汚染リスク

- 断片化された追跡・トレーサビリティデータプロトコル

- 業界サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 素材別

- プラスチック

- 紙および板紙

- 金属

- ガラス

- 製品別

- ボトルおよび容器

- パレットと木箱

- 中間バルクコンテナ(IBC)

- ドラム缶とバレル

- 箱およびカートン

- 缶およびペール缶

- その他の製品(チューブ、パウチ、袋、サックなど)

- エンドユーザー業界別

- 食品・飲料

- 化粧品およびパーソナルケア

- 家庭用品

- 化学品および石油化学製品

- 建築・建設

- 配送と輸送

- その他のエンドユーザー産業(自動車、製薬など)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- 東南アジア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Schoeller Allibert Services BV

- International Paper

- Nefab Group

- IPL Inc.

- Vetropack Holding Ltd

- Mondi PLC

- Greif Inc.

- IFCO Systems

- Smurfit WestRock

- GWP Group

- Orbis Corporation

- Petainer Ltd

- Refillism

- Amcor PLC

- Bormioli Luigi Corporation

- Jiangmen UA Packaging Co. Ltd

- Loop Industries Inc.

- RePack Oy

- EcoEnclose LLC