|

市場調査レポート

商品コード

1911827

マイクロディスプレイ:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Microdisplay - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| マイクロディスプレイ:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

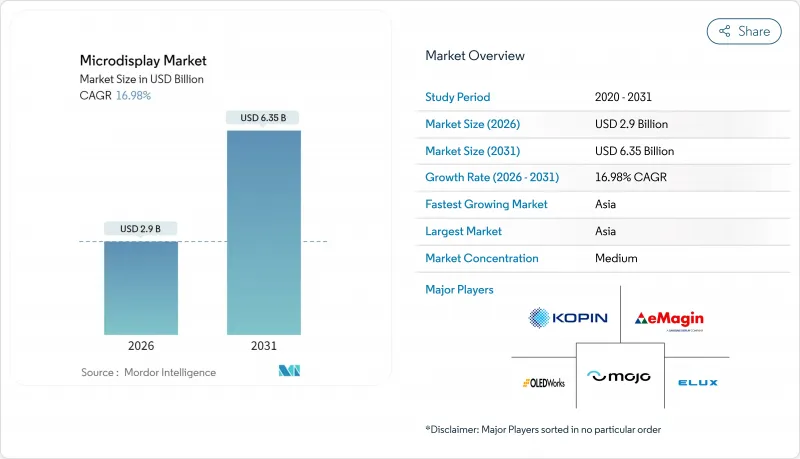

マイクロディスプレイ市場の規模は、2026年には29億米ドルと推定されており、2025年の24億8,000万米ドルから成長が見込まれます。

2031年までの予測では63億5,000万米ドルに達し、2026年から2031年にかけてCAGR16.98%で成長すると見込まれています。

複数の革新サイクルが同時に収束しつつあります。マイクロLEDの大量転写歩留まりがようやく安定化し、AR/VRエコシステムがスケールアップ段階に入り、レベル3以上の運転支援システムが透明ヘッドアップディスプレイをプロトタイプから量産へと推進しています。製造技術の飛躍的進歩、特に5マイクロメートルのMicroLEDチップに対して99.7%の配置精度を達成するレーザー誘導フォワード転写(LIFT)技術により、長らく普及を阻んできたコスト障壁が解消されました。家電大手が専門サプライヤーと提携する競合激化により、実験室での実証から消費者向け発売までの期間が短縮されています。持続的な防衛支出と自動車安全規制は、景気変動を緩和する堅調な最終市場需要をもたらしています。サファイア基板とシリコンバックプレーンの供給制約が主要な事業リスクであり続けますが、継続的な生産能力増強により、これらの逆風は2026年以降緩和される見込みです。

世界のマイクロディスプレイ市場の動向と洞察

アジア全域におけるAR/VRウェアラブル向け超小型ディスプレイの需要急拡大

可処分所得の増加と確立された家電サプライチェーンにより、東アジアは次世代スマートグラスの発射台となりました。上海拠点のJBDは2021年以降100万台以上のMicroLEDエンジンを出荷し、年間50%の出荷台数成長を継続しており、同地域の量産ポテンシャルを実証しています。中国のSidTek社は2024年、8億2,630万米ドルを投じた12インチOLED-on-silicon生産ラインの試運転を開始し、需要急増に対応する現地生産能力を確保しました。地域統合により物流コストと設計サイクルタイムが短縮され、OEMメーカーは競合他社よりも迅速に光学系、導波管、駆動ICの改良を重ねることが可能となりました。この製造集積を背景に部品価格が下落する中、マイクロディスプレイ市場はより広範な消費者層への展開基盤を獲得しています。規模・コスト・普及の好循環により、同地域は今後も世界マイクロディスプレイ市場の成長エンジンとしての地位を維持する見込みです。

自動車メーカー、レベル3+ADAS向けに透明マイクロLED HUDへ移行

自動車メーカー各社は、フロントガラスにドライバー情報と実景を融合させる技術開発を競っています。マイクロLED技術は、直射日光下でも視認性を維持しつつ電力消費を抑えるために必要な輝度余力を提供し、従来のプロジェクター式HUDと比較して20~50倍の効率性を実現します。2025年CESで発表されたAUOの「バーチャルスカイキャノピー」コックピットなどの実証は、曲面・ベゼルレスの視覚表面が量産段階に達していることを証明しています。透明HUDは、視線の高さに警告を表示することで、交通事故の4分の1の原因となる注意散漫も軽減します。この安全性の利点は、特に欧州におけるレベル3自動運転の規制推進と相まって、マイクロLEDHUDを将来の標準装備へと導くでしょう。2026年以降、高級車での導入が始まるにつれ、マイクロディスプレイ市場全体への波及効果は顕著となる見込みです。

RGBマイクロLED量産プロセスにおける歩留まり損失

開発に120億米ドル、買収に24億米ドルを投じたにもかかわらず、量産転写の歩留まりはフルカラーMicroLEDディスプレイのコストの要であり続けています。サブミクロン単位の配置誤差でさえ目に見える不良画素となり、高コストな手直し作業を余儀なくされます。コヒーレント社のLIFTプロセスは重要な前進ですが、ヘッドセットに必要な数百万個のチップに単一パネルの精度をスケールアップすることは、インライン検査と修復ワークフローにとって依然として課題です。オスラムのマレーシア工場拡張とエノスターの台湾工場拡張は、いずれも歩留まりの頭打ちを解消すべく技術者が取り組む中、完成時期が2026年から2027年にずれ込みました。したがって今後2年間が、民生向けマイクロLEDの普及ペースを決定づけることになるでしょう。

セグメント分析

2025年時点で、従来のLCoS、LCD、DLPモジュールがマイクロディスプレイ市場の48.62%を占めておりました。しかしながら、転写歩留まりの向上と競合他社を上回る電力効率により、MicroLEDデバイスは2031年までにCAGR20.85%で拡大が見込まれます。Q-Pixel社は6,800 PPIのMicroLEDアレイを実演し、Apple Vision Proの3,380 PPI基準値を上回り、さらなる視覚精度の向上の余地を証明しました。したがって、MicroLEDのマイクロディスプレイ市場規模は、コスト曲線がOLED-on-Siのそれを上回った時点で急成長する見込みです。欧州では、Aledia社の2億米ドル規模GaN-on-silicon生産ラインが、アジア以外での供給基盤多様化を実現する代替供給源を提供しております。Applied Materials社の試作機が90%を超えるDCI-P3色域を実現した量子ドット・オン・シリコン技術は、絶対的な輝度よりも色均一性を重視するブランド向けのハイブリッドソリューションとして注目されております。

OLED-on-Siは従来技術と新興ソリューションの中間に位置し、成熟した蒸着技術のノウハウを活用しつつ輝度限界への対応を進めています。フォックスコンとポロテックの提携(2025年末までにMicroLEDウエハーラインを立ち上げる計画)は、受託製造企業がOLEDとMicroLEDの両陣営を同時に橋渡ししようとする姿勢を示しています。この二本立て戦略は、マイクロディスプレイ市場においてコスト・輝度・寿命のバランスを追求するブランドが利用できる技術ツールキットの多様化が進んでいることを浮き彫りにしています。

地域別分析

アジア太平洋地域は2025年に売上高の46.62%を占め、2031年までCAGR17.42%を維持する見込みです。これは中国本土における積極的な工場建設と、台湾の堅調な基板エコシステムに牽引されています。シドテック社の12インチOLED-on-Si量産化やJBD社の累計100万台超のMicroLEDエンジン出荷実績は、同地域の生産規模の優位性を示しています。マイクロディスプレイ市場は、導波路光学系、駆動IC、仕上げサービスが緊密に集積されている恩恵を受け、同地域を設計から組立までの一括対応拠点へと変えています。政府のインセンティブ(都市レベルのディスプレイパーク助成金を含む)により、資本回収期間がさらに短縮されています。

北米は重要なシステム統合を担い、防衛調達を主導しています。コピンの米国陸軍契約は国内設計ノウハウを実証していますが、実際のウエハー生産は海外で行われることが多くあります。シリコンバレーの空間コンピューティングソフトウェアへの投資により、使用事例の革新は同地域に定着しています。カナダとメキシコは高度な光学研磨と最終組立でエコシステムを支えていますが、規模は米国の需要に比べ依然として小規模です。

欧州の貢献は技術的差別化に集中しています。アレディア社のグルノーブル工場は欧州を代表するマイクロLEDプロジェクトであり、フル稼働時には週5,000枚のウエハー生産を約束しています。フラウンホーファーIPMS研究所は軽量ARビューアー向け透明OLEDマイクロディスプレイを推進し、産業メンテナンスや外科手術支援シナリオをターゲットとしています。ドイツとスウェーデンの自動車ティア1サプライヤー各社も、厳しい安全基準を満たすHUDモジュールに対する現地需要を支えています。欧州はアジアの生産量には及ばないもの、その研究開発資産と高級自動車市場により、世界のマイクロディスプレイ市場において影響力を維持しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- アジア全域におけるAR/VRウェアラブル向け超小型ディスプレイの需要急増

- 自動車メーカーにおけるレベル3以上ADAS向け透明マイクロLEDヘッドアップディスプレイへの移行

- 低SWaPバイザーディスプレイを指定する防衛近代化プログラム(米国およびNATO)

- ビッグテック企業提携によるメタバース対応スマートグラスの台頭

- ミニファブ委託生産による消費者向けカメラ向けコスト効率的なOLED-on-Siの実現

- シネマティックドローンとマイクロプロジェクターがハイニッツLCoSの採用を牽引

- 市場抑制要因

- RGBマイクロLEDの質量移動プロセスにおける歩留まり損失

- 高輝度OLED-on-Siにおける限定的なウエハー貫通放熱

- 高純度サファイアおよびシリコンバックプレーンのサプライチェーンにおけるボトルネック

- 米国と中国のパネルメーカー間の知的財産訴訟リスク

- 業界エコシステム分析

- 技術概要

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 技術タイプ別

- 従来型(LCoS、LCD、DLP)

- OLED-on-Si

- マイクロLED

- 量子ドット・オン・シリコン

- 解像度別

- 1024 x 768未満

- 1024 x 768から1920 x 1080

- 1920 x 1080以上

- 用途別

- 民生用および自動車用

- 拡張現実/仮想現実ヘッドセット

- 自動車用ヘッドアップディスプレイ

- 従来型用途(プロジェクション/カメラ、その他)

- 防衛

- その他

- 民生用および自動車用

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- 北欧諸国

- その他欧州地域

- 南米

- ブラジル

- その他南米

- アジア太平洋地域

- 中国

- 日本

- インド

- 東南アジア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- GCC

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Sony Semiconductor Solutions Corporation

- JBD(Jade Bird Display)

- Kopin Corporation

- Seiko Epson Corporation

- eMagin Corporation

- LG Electronics

- Himax Technologies Inc.

- BOE Technology Group Co. Ltd.

- Citizen Finedevice Co. Ltd.

- Microoled SA

- VueReal Inc.

- OLiGHTEK Opto-electronic Co. Ltd.

- Syndiant Inc.

- Raontech Co. Ltd.

- Dresden Microdisplay GmbH

- AU Optronics(AUO)

- Universal Display Corp.(UDC)

- eLux Inc.

- Mojo Vision Inc.

- OLEDWorks