|

市場調査レポート

商品コード

1692494

ビデオエンコーダ:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Video Encoder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ビデオエンコーダ:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 157 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

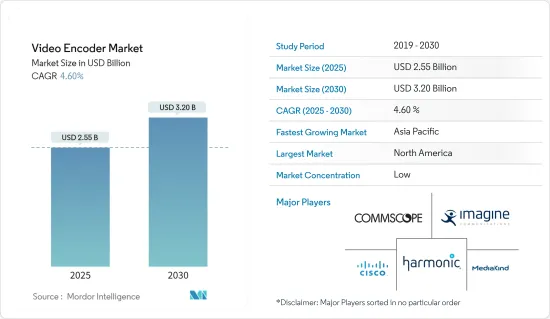

ビデオエンコーダ市場規模は2025年に25億5,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは4.6%で、2030年には32億米ドルに達すると予測されています。

主なハイライト

- ビデオエンコーダ市場は、様々なプラットフォームでの高品質ビデオストリーミングや放送に対する需要の高まりにより、力強い成長を遂げています。ビデオエンコーダは、ビデオ信号をインターネットやその他のネットワークでのトランスミッションに適したデジタルフォーマットに変換します。この市場の拡大には、オンライン・ビデオ・コンテンツの消費の増加、オーバー・ザ・トップ(OTT)サービスの普及、ライブ・ストリーミング活動の急増が寄与しています。動画コンテンツが重要なエンゲージメント・ツールであるソーシャルメディア・プラットフォームの普及が、高度な動画エンコーディング・ソリューションの需要をさらに押し上げています。

- 技術の進歩は、ビデオエンコーダ市場を形成する上で極めて重要です。H.265(HEVC)や新興のAV1コーデックなどの圧縮アルゴリズムの革新は、ビデオの品質を維持しながら圧縮率を高め、効率的なデータ伝送と保存を容易にします。これらの進歩は、より多くの帯域幅とストレージ容量を必要とする4Kおよび8Kビデオ解像度の需要の増加をサポートします。

- さらに、人工知能(AI)と機械学習(ML)を統合したハードウェアエンコーダの開発は、重要な動向を示しています。これらの統合は、リアルタイムのビデオ処理能力を向上させ、ネットワークリソースを最適化します。

- さらに、シスコシステムズ社、ハーモニック社、アクシスコミュニケーションズ社(キヤノン)などの大手企業がビデオエンコーダ市場をリードしています。これらの業界大手と並んで、新興企業も革新的なソリューションで波を起こしています。これらのプレーヤーは、市場での地位を強化するために、合併、買収、提携、製品発表などの戦略を積極的に推進しています。特に、多くの企業がOTTサービスプロバイダーや放送事業者と戦略的提携を結び、シナジー効果の活用と顧客範囲の拡大を図っています。

- ビデオエンコーダ市場は、大きな成長機会とともに非常に有望な見通しを示しています。ビデオ規格の継続的な進化、5Gネットワークの世界の展開、仮想現実(VR)や拡張現実(AR)のような没入型体験に対する需要の高まりが、さらなるイノベーションとアプリケーションの推進力となっています。研究開発を優先し、技術シフトに迅速に対応する企業は、新たな動向を活用し、競争優位性を維持するのに有利な立場にあると思われます。

- ビデオエンコーダ市場は多くの成長促進要因に恵まれているが、ハードウェアビデオエンコーダに関連する高額な初期費用という形で、注目すべきハードルが浮上しています。生映像を放送やストリーミング用のデジタルフォーマットに変換するために重要なこれらのデバイスは、多くの場合、多額の先行投資を必要とします。特に中小企業や新興企業にとって、このような金銭的支出は大きな障害となります。結果として生じる高額なコストは、潜在的な顧客が新しい技術を取り入れたり、既存のセットアップを近代化したりすることを思いとどまらせ、市場の拡大や技術革新の妨げになる可能性があります。さらに、これらの費用は企業の全体的な投資収益率に直接影響する可能性があるため、メーカーがコスト削減策を検討したり、柔軟な資金調達オプションを提供したりして、より広範な導入に拍車をかけることの重要性が浮き彫りになっています。

ビデオエンコーダ市場の動向

ビデオストリーミングプラットフォームの普及が市場成長を牽引

- Netflix、Amazon Prime、YouTubeなどの動画ストリーミングサービスの人気上昇により、高品質で低遅延のストリーミングに対する欲求が高まっています。その結果、この動向が高度なビデオエンコーダの需要を牽引しています。これらのエンコーダは、動画を効率的に圧縮し、品質を維持し、特に4Kや8Kのような要求の厳しい解像度でシームレスな視聴を保証することを任務としています。Inplayerによると、OTTユーザーのうち、18.4%は25~29歳、11.5%は30~36歳です。注目すべきは、OTTユーザーの約15%が17歳以下であることです。

- ユーザー生成コンテンツとプロフェッショナル・コンテンツの台頭により、ストリーミング用ビデオ制作がブームとなっています。その結果、効率的な動画エンコーディング・ソリューションへの需要が高まっています。これらのソリューションは、コンテンツ量の増加、迅速なアップロード、シームレスなストリーミング体験の確保に不可欠です。この動向は、ビデオエンコーダ市場の大きな促進要因となっています。

- さらに、イベント、ゲーム、スポーツ、ソーシャルメディアにおけるライブストリーミングの急増は、リアルタイムビデオエンコーディングソリューションの必要性を高め、ビデオエンコーダ市場を牽引しています。ライブコンテンツを迅速に処理し、遅延を最小限に抑えるエンコーダは、スムーズで魅力的な視聴体験を提供する上で極めて重要です。

- また、スマートフォン、タブレット、スマートTVの動画ストリーミング利用の急増は、アダプティブビデオエンコーディングの必要性を強調しています。多様な画面サイズやネットワーク速度に合わせて動画を調整するために不可欠なエンコーダが、動画エンコーダ市場を牽引しています。

アジア太平洋が最大の市場シェアを占める見込み

- 中国における地上波デジタルテレビ放送の登場は、既存のサービスを改善し、新しいアプリケーションへの道を開いた。DTT放送規格は、HDTVや複数のSDTV番組の広域固定受信を可能にします。新しいサービスには、モバイル、ウェアラブル、高速アプリケーションも含まれます。

- 中国政府も人々の視聴体験の向上に取り組んでおり、中国は主要都市に対し、地上波HDTV放送コンテンツの無料提供を開始するよう奨励しました。これは、地上デジタル放送市場や、高精細フラットパネル、チップセット、送信機、ソフトウェア、コンテンツ制作を含むHDTV産業全体の成長を促進するのに役立ちます。

- Netflix、Amazon、Disney+HotstarのようなOTTサービスがオリジナルコンテンツや買収コンテンツに投資することで、定額制ビデオ・オン・デマンドがOTT収入全体の93%を占めるようになり、2024年までに30.7%に増加し、インドでは27億米ドルに達します。2024年1月までに、YouTubeは4億6,200万人のユーザーを惹きつけ、米国を視聴者数で大きく引き離し、インドの主要な動画プラットフォームに浮上しました。

- 韓国の各企業はビデオエンコーダー・ソリューションを開発し、放送とストリーミング市場を牽引しています。例えば、KT Corp.は、DTH分野での独占とIPTV分野での強い地位により、加入と監督に関して韓国の有料テレビサービス業界を牽引しており、最大のシェアを占めています。

- 近年、技術の進歩により、ハイビジョンテレビ(HDTV)よりも高解像度の4K映像を録画・表示できるカメラ、ディスプレイ、タブレットなどの機器が急速に普及しています。こうした機器の普及に伴い、日本でも放送やネットワーク配信でHD映像を配信するための次世代映像エンコードへの期待が高まっています。4Kテレビは一般家庭にも普及しつつあり、大手テレビメーカーから多くのモデルが発売されています。

ビデオエンコーダ業界の概要

ビデオエンコーダ市場は競争が激しく、Harmonic Inc.、CommScope Holding Company Inc.、MediaKindなどの大手企業が競争力を維持するために継続的に能力を強化しています。これらの企業は戦略的に製品イノベーション、合併、買収、パートナーシップに注力し、製品ポートフォリオを多様化し、世界の足跡を広げています。

- 2024年1月、ボリューメトリック・ビデオ技術の主要企業であるArcturus社は、HoloSuiteツールセットのアップデートを発表しました。このアップデートは斬新なアプローチを導入し、軽量でスケーラブルなボリューメトリック映像をゲームエンジンにシームレスに提供することを可能にします。Arcturusはバーチャルプロダクションチームだけでなく、ゲーム開発者にも力を与えます。ユーザーは、データの品質を犠牲にすることなく、より多くのボリューメトリックキャラクターでデジタルランドスケープを豊かにすることができます。

- 2023年11月、映像・音声コーデック技術のスペシャリストであるMainConcept社は、OTTおよびTV放送ワークフロー向けのリアルタイムエンコーディングアプリケーションの最新バージョンをリリースすることを発表しました。新バージョンのLive Encoder 3.4は、VVC/H.266とMPEG-5 LCEVCコーデックをサポートしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- ビデオコーデックの分析とその進化

- VVC承認企業・法人企業リスト

- VVC規格に貢献している企業のリスト

- COVID-19が市場に与える影響

- 業界の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- ビデオストリーミングプラットフォームの人気の高まり

- ハードウェアエンコーダとビデオカメラの容易な統合

- クラウドビデオエンコーディング技術が需要を牽引

- 市場の課題

- ハードウェアビデオエンコーダーの初期コストの高さ

第6章 市場セグメンテーション

- 用途別

- 有料テレビ

- ケーブルビデオエンコーダー

- 衛星ビデオエンコーダ

- IPTVビデオエンコーダ

- 放送および地上デジタルテレビ(DTT)

- 貢献ビデオ・エンコーダ

- バックホールおよび配信ビデオ・エンコーダ

- DTTビデオエンコーダ

- セキュリティと監視

- 有料テレビ

- 地域別

- 南北アメリカ

- 米国

- カナダ

- ブラジル

- メキシコ

- その他の地域

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- ポーランド

- その他の欧州

- アジア太平洋

- 中国

- インド

- 韓国

- 日本

- その他のアジア太平洋

- 中東・アフリカ

- トルコ

- イスラエル

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 南北アメリカ

第7章 競合情勢

- 企業プロファイル

- Harmonic Inc.

- Commscope Holding Company Inc.

- MediaKind

- Cisco Systems Inc.

- Imagine Communications

- Z3 Technology

- ATEME

- Adtec Digital

- Telairity(VITEC)

- Axis Communications AB(Canon Inc.)

第8章 投資分析

第9章 市場の将来

The Video Encoder Market size is estimated at USD 2.55 billion in 2025, and is expected to reach USD 3.20 billion by 2030, at a CAGR of 4.6% during the forecast period (2025-2030).

Key Highlights

- The video encoder market is witnessing strong growth, driven by the rising demand for high-quality video streaming and broadcasting across various platforms. Video encoders convert video signals into digital formats suitable for transmission over the Internet or other networks. This market's expansion is fueled by the increasing consumption of online video content, the proliferation of over-the-top (OTT) services, and the surge in live-streaming activities. The widespread adoption of social media platforms, where video content is a key engagement tool, further propels the demand for advanced video encoding solutions.

- Technological advancements are pivotal in shaping the video encoder market. Innovations in compression algorithms, such as H.265 (HEVC) and the emerging AV1 codec, enhance compression rates while maintaining video quality, facilitating efficient data transmission and storage. These advancements support the increasing demand for 4K and 8K video resolutions, which require significantly more bandwidth and storage capacity.

- Additionally, the development of hardware encoders that integrate artificial intelligence (AI) and machine learning (ML) represents a significant trend. These integrations improve real-time video processing capabilities and optimize network resources.

- Moreover, major players such as Cisco Systems Inc., Harmonic Inc., and Axis Communications AB (Canon Inc.) lead the pack in the video encoder market. Alongside these industry stalwarts, newer firms are making waves with innovative solutions. These players are actively pursuing strategies like mergers, acquisitions, partnerships, and product launches to bolster their market positions. Notably, many are forging strategic ties with OTT service providers and broadcasters, seeking to tap into synergies and broaden their customer reach.

- The video encoder market exhibits a highly promising outlook with significant growth opportunities. The ongoing evolution of video standards, the global deployment of 5G networks, and the increasing demand for immersive experiences, such as virtual reality (VR) and augmented reality (AR), are set to drive further innovations and applications. Companies prioritizing research and development and swiftly adapting to technological shifts will be well-positioned to capitalize on emerging trends and maintain their competitive advantage.

- While the video encoder market boasts numerous growth drivers, a notable hurdle emerges in the form of the steep initial costs associated with hardware video encoders. These devices, pivotal for transforming raw video into digital formats for broadcasting and streaming, often demand a significant upfront investment. This financial outlay can pose a formidable obstacle, especially for smaller enterprises and startups. The resulting high costs may dissuade potential customers from embracing new technologies or modernizing their existing setups, constraining market expansion and stifling innovation. Moreover, these expenses can directly impact a company's overall return on investment, underscoring the importance for manufacturers to explore cost-cutting measures or offer flexible financing options to spur wider adoption.

Video Encoder Market Trends

Increasing Popularity of Video Streaming Platforms is Expected to Drive the Market Growth

- The rising popularity of video streaming services such as Netflix, Amazon Prime, and YouTube has heightened the appetite for high-quality, low-latency streaming. Consequently, this trend drives the demand for advanced video encoders. These encoders are tasked with compressing videos efficiently, maintaining quality, and guaranteeing seamless viewing, especially at resolutions as demanding as 4K and 8K. According to Inplayer, among OTT users, 18.4% fall in the 25 - 29 age bracket, with 11.5% in the 30 - 36 range. Notably, approximately 15% of OTT users are under 17 years old.

- The rise of user-generated and professional content has led to a boom in video production for streaming. Consequently, there is a growing demand for efficient video encoding solutions. These solutions are crucial for increasing content volume, ensuring swift uploads, and seamless streaming experiences. This trend serves as a significant driver of the video encoder market.

- Moreover, the surge in live streaming across events, gaming, sports, and social media has heightened the need for real-time video encoding solutions, driving the video encoder market. Encoders that can process live content swiftly, ensuring minimal delays, are pivotal for delivering a smooth and engaging viewer experience.

- Also, the surge in smartphone, tablet, and smart TV usage for video streaming has underscored the necessity for adaptive video encoding. Encoders, pivotal for tailoring videos to diverse screen sizes and network speeds, are driving the video encoder market.

Asia-Pacific is Expected to Hold the Largest Market Share

- The advent of terrestrial digital television broadcasting in China has improved existing services and paved the way for new applications. The DTT broadcast standard enables wide-area fixed reception on HDTV and multiple SDTV programs. New services also include mobile, wearable, and high-speed applications.

- The Chinese government is also working to improve people's viewing experience, and China encouraged major cities to start offering free terrestrial HDTV broadcast content. This helps drive growth in the digital terrestrial market and the HDTV industry as a whole, including high-definition flat panels, chipsets, transmitters, software, and content creation.

- Investments by OTT services like Netflix, Amazon, and Disney+ Hotstar in original and acquired content will enable subscription video-on-demand to make up 93% of the total OTT revenue, increasing to 30.7% by 2024, amounting to USD 2.7 billion in India. By January 2024, YouTube emerged as the leading video platform in India, attracting 462 million users, significantly outpacing the United States in viewership.

- South Korean organizations are developing video encoder solutions to drive the broadcasting and streaming market. For example, KT Corp. is driving the pay TV services industry in South Korea regarding subscriptions and supervision, owing to its monopoly in the DTH segment and strong position in the IPTV segment, where it has the greatest share.

- In recent years, technological advances have led to the rapid spread of devices such as cameras, displays, and tablets that can record and display 4K video in higher resolution than high-definition televisions (HDTVs). With the proliferation of these devices, expectations are rising for next-generation video encoding for delivering HD video over broadcast and network delivery in Japan. 4K TVs are becoming increasingly popular in the home, and many models are available from major TV manufacturers.

Video Encoder Industry Overview

The video encoder market is highly competitive, with major players like Harmonic Inc., CommScope Holding Company Inc., and MediaKind continuously enhancing their capabilities to maintain a competitive edge. These companies strategically focus on product innovations, mergers, acquisitions, and partnerships to diversify their product portfolios and expand their global footprint.

- In January 2024, Arcturus, a key player in volumetric video technology, unveiled an update for its HoloSuite toolset. This update introduces a novel approach, enabling the seamless delivery of lightweight, scalable volumetric video to game engines. Arcturus empowers not just virtual production teams but also game developers. Users can now enrich their digital landscapes with more volumetric characters without compromising on data quality.

- In November 2023, MainConcept, a video and audio codec technology specialist, announced the release of the latest version of its real-time encoding application for OTT and TV broadcasting workflows. The new version, Live Encoder 3.4, supports VVC/H.266 and MPEG-5 LCEVC codecs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Analysis of Video Codecs and Their Evolution

- 4.3 List of VVC-approved and Incorporated Companies

- 4.4 List of Companies Contributing to the VVC Standard

- 4.5 Impact of COVID-19 on the Market

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Popularity of Video Streaming Platforms

- 5.1.2 Easy Integration of Hardware Encoders with Video Cameras

- 5.1.3 Cloud Video Encoding Technology to Drive the Demand

- 5.2 Market Challenges

- 5.2.1 High Initial Cost of Hardware Video Encoder

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Pay TV

- 6.1.1.1 Cable Video Encoder

- 6.1.1.2 Satellite Video Encoder

- 6.1.1.3 IPTV Video Encoder

- 6.1.2 Broadcast and Digital Terrestrial Television (DTT)

- 6.1.2.1 Contribution Video Encoder

- 6.1.2.2 Backhaul and Distribution Video Encoder

- 6.1.2.3 DTT Video Encoder

- 6.1.3 Security and Surveillance

- 6.1.1 Pay TV

- 6.2 By Geography

- 6.2.1 Americas

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.1.3 Brazil

- 6.2.1.4 Mexico

- 6.2.1.5 Rest of the Americas

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Russia

- 6.2.2.5 Poland

- 6.2.2.6 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 South Korea

- 6.2.3.4 Japan

- 6.2.3.5 Rest of Asia-Pacific

- 6.2.4 Middle East and Africa

- 6.2.4.1 Turkey

- 6.2.4.2 Israel

- 6.2.4.3 United Arab Emirates

- 6.2.4.4 Saudi Arabia

- 6.2.4.5 South Africa

- 6.2.4.6 Rest of Middle East and Africa

- 6.2.1 Americas

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Harmonic Inc.

- 7.1.2 Commscope Holding Company Inc.

- 7.1.3 MediaKind

- 7.1.4 Cisco Systems Inc.

- 7.1.5 Imagine Communications

- 7.1.6 Z3 Technology

- 7.1.7 ATEME

- 7.1.8 Adtec Digital

- 7.1.9 Telairity (VITEC)

- 7.1.10 Axis Communications AB (Canon Inc.)