|

|

市場調査レポート

商品コード

1549724

PLMソフトウェア:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)PLM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| PLMソフトウェア:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

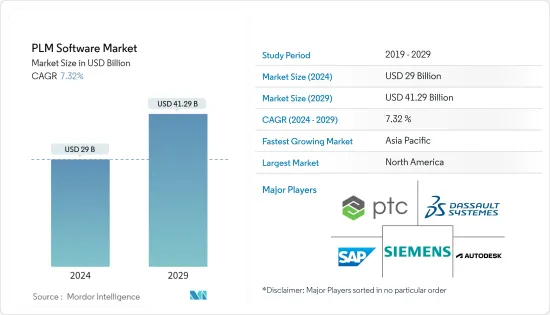

PLMソフトウェア市場規模は、2024年に290億米ドルと推定・予測され、2029年には412億9,000万米ドルに達し、予測期間(2024-2029年)のCAGRは7.32%で成長すると予測されます。

PLMソフトウェア市場規模は、2024年に290億米ドルを占めると推定されます。業界における堅牢なデータ分析ソフトウェアプラットフォームに対する需要の高まりにより、予測期間(2024-2029年)のCAGRは7.32%を記録し、2029年には412億9,000万米ドルに達すると予測されます。さらに、製造業界全体でIoTの導入が進んでいることも、こうした動向を後押ししています。PTCのWindchillは、IoT機能を求めるディスクリート製造業者向けのアナリティクスを組み込んだPLMソフトウェアの一例です。このソフトウェアは、PLMソリューションの柔軟性を高めることができます。

主なハイライト

- 各業界の企業は、効率性を向上させ、イノベーションを加速させるために、製品開発プロセスの合理化にますます注力しています。PLMソフトウェアによって、企業はアイデア出しから廃棄、効率化まで、製品ライフサイクル全体を管理できるようになり、市場での需要が高まっています。

- 世界規模で事業を展開し、チームがさまざまな場所に分散しているため、コミュニケーションとデータ共有を促進するコラボレーションツールの必要性が高まっています。PLMソフトウェアは、地理的な場所に関係なく、チームがシームレスにコラボレーションできる一元化されたプラットフォームを提供します。

- 生産プロセスにおける産業用IoT(IIoT)の採用増加は、ソフトウェアアプリケーションの市場需要を後押ししており、IIoTの採用は予測期間中に急増すると予想されます。例えば、GSMA Intelligenceによると、IIoTに接続されたオブジェクトの数は2025年までに137億個に達すると予想されています。

- しかし、各社が市場競争に取り組むために異なる製品や製品群を提供し続けているため、相互運用性の問題が生じ、ソフトウェア企業にとっては常に最適化が求められます。ソフトウェア製品の継続的な改良が進めば、企業の既存の製品ラインアップにソフトウェアを導入することが合理化され、管理しやすくなり、より良い結果が出やすくなります。

- 多くの製造業がCOVID-19の大流行の影響を受け、サプライチェーンに大きなギャップが生じ、遅れが生じました。このため、多くの業界がインダストリー4.0やデジタルトランスフォーメーションの導入を急がざるを得なくなり、必要な成長率を高めるためにPLMソフトウェアの需要が高まった。パンデミック後にソフトウェアの普及が進んだことも、市場の成長を後押ししています。

PLMソフトウェア市場動向

自律走行車の生産増加が市場成長を牽引

- 自律走行車の普及に伴い、自律走行車の開発に携わる開発者はますます複雑な課題に直面しています。これらの課題を克服するためには、既存のプロセスやツールセットを再評価する必要があります。このため、こうした課題の克服を支援するソリューションに対する需要が高まっており、これが市場の飛躍的な成長に拍車をかけています。

- さらに、完全に機能する自律走行システムには、センサーからの情報、クラウドからの交通データ、他のインフラや車両からのデータなど、さまざまなデータフィードを組み合わせ、そのすべてを自動車の機械的・電子的コンポーネントに結びつけ、ユーザーの入力や修正を必要とせずにすべてが確実に連動する車載システムの広大なネットワークを構築するために、自動車メーカーがこれまでに直面したことのない複雑で洗練されたソフトウェアの実装が必要となります。

- さらに、codeBeamer ALMのような統合ALM(アプリケーション・ライフサイクル管理)と製品開発プラットフォームは、製品の複雑化と自律走行車分野における高度なソフトウェア・アプリケーションへの依存の高まりがもたらす課題を克服するために、開発プロセスを近代化する上で重要な役割を果たすと思われます。

- デジタル製造の利用の高まりと自律走行車の需要の増加は、予測期間中に自動車分野のPLMソフトウェア市場を牽引すると予想される主要動向です。

北米が大きなシェアを占める

- 北米は、その強固な財務基盤により、特に先進的な技術やソリューションへの大規模な投資が可能であり、市場競争において優位性を発揮しています。さらにこの地域には、IBM Corp.、PTC Inc.、Oracle Corporationなど、製品ライフサイクル管理ソフトウェアの主要ベンダーが複数存在します。そのため、市場競争は熾烈を極めています。

- 北米の自動車産業全体は急速なペースで成長しています。PLMソフトウェアは、主に製品開発段階で活用されており、自動車業界では製造が始まるずっと前から始まっています。PLMソフトウェアは、自動車の高度な安全機能、電子機器、組み込みソフトウェアの内容を保証します。そのため、この地域の自動車産業の上昇に伴い、市場は予測期間を通じてさまざまな有利な成長機会を得られると期待されています。

- その他の製造業や市場では、製造・生産プロセスを強化するためにPLMソフトウェアを導入するメリットが模索されています。例えば、2023年4月、シーメンスとマイクロソフトは、主に工業企業が製品のエンジニアリング、設計、製造、運用ライフサイクル全体で効率化とイノベーションを推進できるよう、ジェネレーティブ人工知能の総合的な協調力を活用しました。また、機能横断的なコラボレーションを強化するため、両社はシーメンスの製品ライフサイクル管理用ソフトウェアTeamcenterとマイクロソフトのコラボレーションプラットフォームTeams、Azure OpenAI Serviceの言語モデル、その他さまざまなAzure AI機能の統合に注力しています。

- 例えば、PTCは、主にクラウドネイティブなOnshape製品開発ソリューションとArena製品ライフサイクル管理ソリューションを接続する新機能、Onshape-Arena Connectionの提供を宣言しました。この接続により、ArenaソリューションとOnshapeソリューションの間で、ボタンをクリックするだけで製品データを即座に共有できるようになり、企業は製品開発プロセスを強化し、サプライチェーンパートナーとのコラボレーションを簡素化することができます。

- このようなコラボレーションは、市場全体のシナリオを強化し、PLMソフトウェアを有効にするために他の競合他社やベンダーを刺激し、広大なPLM実装のための北米市場全体を形成します。それゆえ、製品サプライチェーンのいくつかの側面を通じて徹底的な実装は、進化するインダストリー4.0の動向に北米企業を積極的に支援しています。

PLMソフトウェア市場産業概要

製品ライフサイクル管理(PLM)ソフトウェア市場は、主に数多くの世界プレーヤーの存在により、非常に細分化され競合が激しいです。さまざまな市場プレーヤーが最新のソフトウェア技術を駆使して研究開発に取り組んでおり、市場全体で高い競争力を構築しています。主なプレーヤーとしては、Dassault Systemes Deutschland GmbH、Siemens、Autodesk Inc.、ANSYS Inc.、Infor Inc.などが挙げられます。各社は、さまざまなパートナーシップを結び、プロジェクトに投資し、市場に新製品を投入することで、市場シェアを最大化しています。

- 2023年2月、Hexagon傘下でコラボレーションと設計ソリューションの世界的プロバイダーであるBricsysは、WIPRO傘下のITI Technegroup傘下のMechWorksと提携し、SiemensのTeamcenterソフトウェアとBricsCADの統合を提供することを宣言しました。このソリューションは主に、BricsCADのプロセスをより迅速に接続し、設計者が製品開発に集中できるよう、業界最高の機能を提供します。

- 2023年10月、エンジニアリングソフトウェアとPLMの主要企業であるPTCは、製品とソフトウェアのバリアント管理を専門とするドイツのソフトウェア会社Pure-systemsの買収を発表しました。Pure-systems社のウェブサイトの免責事項にあるように、買収はすでに行われていました。この買収により、エンジニアや製品設計者が製品やソフトウェアのバリエーションを管理するためのツールpure::variants(バリアント管理ツール)がPTCのポートフォリオに加わることになります。PTCとpure-systemsは以前、pure::variantsをPTCのアプリケーション・ライフサイクル管理(ALM)ソフトウェアCodebeamerに統合するために提携していました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19が製品ライフサイクル管理ソフトウェア市場に与える影響

第5章 市場力学

- 市場促進要因

- 生産性向上のためのデジタル化の導入

- 情報集約のためのクラウド技術のイントロダクション

- 市場抑制要因

- 異なる製品バージョン間の相互運用性の欠如

第6章 市場セグメンテーション

- 導入タイプ別

- オンプレミス

- クラウド

- プロフェッショナル・サービス

- エンドユーザー産業別

- エレクトロニクス、産業機器、ハイテク

- 航空宇宙・防衛

- 自動車

- アーキテクチャ、エンジニアリング、建設(AEC)

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- その他アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Siemens AG

- Dassault Systems Deutschland GmbH

- Autodesk Inc.

- PTC Inc.

- SAP SE

- ANSYS Germany GmbH

- Oracle Corporation

- Aras Corporation

- Arena Solutions

- Infor Inc.

第8章 投資分析

第9章 市場の将来

The PLM Software Market size is estimated at USD 29 billion in 2024, and is expected to reach USD 41.29 billion by 2029, growing at a CAGR of 7.32% during the forecast period (2024-2029).

The PLM software market size is estimated to account for USD 29 billion in 2024. It is expected to reach USD 41.29 billion by 2029, registering a CAGR of 7.32% during the forecast period (2024-2029), owing to the growing demand for robust data analytics software platforms in the industry. Moreover, the increasing adoption of IoT across the manufacturing industry has augmented these trends. PTC's Windchill is an instance of the PLM software embedded with analytics for discrete manufacturers looking for IoT capabilities. This software can boost the PLM solution to sprint with flexibility.

Key Highlights

- Companies across industries are increasingly focused on streamlining their product development processes to improve efficiency and accelerate innovation. PLM software enables organizations to manage the entire product lifestyle, from ideation to disposal and efficiency, thereby increasing the demand in the market.

- With businesses operating on a global scale and teams dispersed across various locations, there is a growing need for collaboration tools that facilitate communication and data sharing. PLM software provides a centralized platform for teams to collaborate seamlessly regardless of geographic location.

- The increased adoption of Industrial IoT (IIoT) in the production process is aiding the market demand for software applications, and IIoT adoption is expected to skyrocket during the forecast period. For instance, according to GSMA Intelligence, the number of IIoT-connected objects is expected to reach 13.7 billion by 2025.

- However, as the companies continue to provide different products and product ranges to tackle market competitiveness, it creates interoperability issues, a matter of constant optimization for the software companies. As continuous improvements continue in the software products, the software implementation in a company's existing product line-up becomes streamlined and manageable, facilitating better results.

- Many manufacturing industries were affected by the COVID-19 pandemic, creating significant supply chain gaps and leading to delays. This forced many industries to hasten the adoption of Industry 4.0 and digital transformation initiatives, boosting the demand for PLM software to bolster the required growth rates. The increased software penetration after the pandemic has boosted market growth.

PLM Software Market Trends

Increasing Production of Autonomous Vehicles to Drive Market Growth

- As the use of autonomous vehicles becomes more widespread, the developers working on these vehicles are encountering increasingly complex challenges. To overcome these challenges, they need to re-evaluate their existing processes and toolsets. This has led to a rising demand for solutions that can help them overcome these challenges, which is fueling the market's growth exponentially.

- Moreover, the fully functional autonomous driving systems need some of the most complex and sophisticated software implementations that carmakers have ever faced for combining a variety of data feeds, like information from sensors, traffic data from the cloud, data coming from other infrastructure or vehicles, and tying it all into the automobiles's mechanical and electronic components to create a vast network of onboard systems that all work together reliably without the need for user input or correction.

- Furthermore, integrated ALM (application lifecycle management) and product development platforms, such as codeBeamer ALM, will play a significant role in modernizing development processes to overcome the challenges posed by the growing complexity of products and the increasing dependence on sophisticated software applications in the autonomous vehicle sector.

- The rising usage of digital manufacturing and the increasing demand for autonomous cars are key trends that are expected to drive the PLM software market in the automotive sector during the forecast period.

North America to Account for a Significant Share

- North America's strong financial position allows it to invest massively, especially in advanced technologies and solutions that have offered a strong competitive edge within the market. Moreover, the region has a robust presence of several significant product lifecycle management software vendors like IBM Corp., PTC Inc., and Oracle Corporation. Hence, there lies intense competition among the market players.

- The entire automotive industry in North America is growing at a rapid pace. PLM software is primarily utilized in the product development stage, which starts long before manufacturing begins in the automotive industry. It ensures the vehicles' advanced safety features, electronics, and embedded software content. Hence, with the rise in the automotive industry within the region, the market is expected to have various lucrative growth opportunities throughout the forecast period.

- Other manufacturing industries and markets explore the benefits of deploying PLM software to augment manufacturing and production processes. For instance, in April 2023, Siemens and Microsoft harnessed the overall collaborative power of generative artificial intelligence mainly to help industrial companies drive efficiency and innovation across the engineering, design, manufacturing, and operational lifecycle of the products. Also, to enhance cross-functional collaboration, the companies are focused on integrating Siemens' Teamcenter software for product lifecycle management with Microsoft's collaboration platform, Teams, and its language models in Azure OpenAI Service, as well as various other Azure AI capabilities.

- For instance, PTC declared the availability of the Onshape-Arena Connection, a new functionality that mainly connected its cloud-native Onshape product development and Arena product lifecycle management solutions. The connection allowed the product data to be shared instantly between the Arena and Onshape solutions with the single click of a button, assisting the companies in augmenting the product development process and simplifying collaboration with the supply chain partners.

- Such collaborations enhance the entire market scenario, stimulating other competitors and vendors to enable PLM software and shaping the whole North American market for vast PLM implementation. Hence, the in-depth implementation throughout several aspects of the product supply chain is actively helping North American businesses with the evolving Industry 4.0 trends.

PLM Software Market Industry Overview

The product lifecycle management (PLM) software market is highly fragmented and competitive, mainly due to the presence of numerous global players. Various market players are moving in R&D with the latest software techniques, building a high level of competitiveness throughout the market. The key players include Dassault Systemes Deutschland GmbH, Siemens, Autodesk Inc., ANSYS Inc., and Infor Inc. The companies are thus maximizing their market share by forming various partnerships, investing in projects, and introducing new products in the market.

- In February 2023, global provider of collaboration and design solutions Bricsys, part of Hexagon, declared its partnership with MechWorks, part of ITI Technegroup, a WIPRO company, to offer an integration between Siemens' Teamcenter software and BricsCAD. The solution primarily provides industry-best features to connect BricsCAD's processes faster and enable designers to focus on its product development.

- In October 2023, PTC, a leading engineering software and PLM provider, announced its acquisition of pure-systems, a German software company that specializes in product and software variant management. The acquisition had already taken place, as indicated by the disclaimer on pure-systems' website. The acquisition will bring pure::variants, a tool designed to help engineers and product designers manage product and software variation, to PTC's portfolio. PTC and pure-systems had previously partnered to integrate pure::variants into PTC's Codebeamer application lifecycle management (ALM) software.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Product Lifecycle Management Software Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Adoption of Digitalization to Improve Production

- 5.1.2 Introduction of Cloud Technology to Consolidate the Information

- 5.2 Market Restraints

- 5.2.1 Lack of Interoperability among Dissimilar Product Versions

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.1.3 Professional Services

- 6.2 By End-user Industry

- 6.2.1 Electronics, Industrial Equipment, and High-tech

- 6.2.2 Aerospace and Defense

- 6.2.3 Automotive

- 6.2.4 Architecture, Engineering, and Construction (AEC)

- 6.2.5 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siemens AG

- 7.1.2 Dassault Systems Deutschland GmbH

- 7.1.3 Autodesk Inc.

- 7.1.4 PTC Inc.

- 7.1.5 SAP SE

- 7.1.6 ANSYS Germany GmbH

- 7.1.7 Oracle Corporation

- 7.1.8 Aras Corporation

- 7.1.9 Arena Solutions

- 7.1.10 Infor Inc.