前臨床CRO:市場シェア分析、業界動向・統計、成長予測(2024年~2029年)

Preclinical CRO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1537721

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

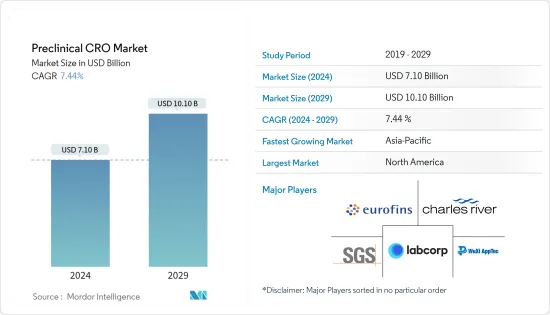

前臨床CRO市場規模は2024年に71億米ドルと推定・予測され、2029年には101億米ドルに達し、予測期間(2024-2029年)のCAGRは7.44%で成長すると予測されます。

調査された市場成長の主な要因は、世界の研究開発(R&D)支出の増加、前臨床試験中の医薬品数の増加、2024年から2029年にかけての慢性疾患患者による医薬品取り込み需要の高さです。

ライフサイエンス分野での研究開発費の増加や、この分野への公的・民間資金投入が市場の成長を後押ししています。例えば、インド科学技術省は、2023年から2024年の連邦予算において、インド生物工学局(DBT)に400億インドルピー(4億2,720万米ドル)の予算を割り当てています。資金が大幅に増加したのは、主に国内の研究開発費の増加によるものです。したがって、研究開発費の増加は、医薬品開発プロセスの全体的なコストを削減するために、前臨床CROサービスの採用を増加させると予想されます。

同様に、欧州製薬団体連合会(EFPIA)の2022年の医薬品研究開発費は440億米ドルに達し、2021年と比較して4.6%増加しました。したがって、欧州における研究開発費の増加は、2024年から2029年にかけて支出を削減するために前臨床CROサービスの需要を増加させると予想されます。

さらに、前臨床段階にある医薬品数の増加も、開発コストを削減し、臨床試験を実施するための医薬品承認の可能性を高めるために、前臨床サービスのアウトソーシング需要を増加させると予想されます。例えば、ClinicalTrials.gov 2024の更新データによると、2024年1月現在、世界全体で47万9,000件近くの臨床試験が登録されています。この臨床試験の大幅な増加は、前臨床試験を経て新薬承認申請(NDA)を受けた治療薬や医療機器の数を反映しています。したがって、前臨床試験中の医薬品数の増加が、2024年から2029年にかけて調査対象市場を牽引すると予想されます。

しかし、標準化の欠如、モニタリングの問題、厳しい規制方針が市場の成長を妨げると予想されます。

前臨床CRO市場の動向

毒性試験セグメントは2024~2029年に大幅な成長が予測される

毒性試験は、化学物質や医薬化合物が生体に及ぼす潜在的な悪影響を評価するものです。有害性や毒性を引き起こす可能性を含め、これらの物質の安全性プロファイルを評価するためのさまざまな手法が含まれます。医薬品研究開発のダイナミックな状況において、医薬品開発業務受託機関(CRO)が提供する前臨床毒性試験サービスに対する需要が大幅に増加しています。この急増は、製薬企業とCROの協力関係の拡大や、毒性試験プロセスの効率と精度を高める技術の進歩など、さまざまな要因に起因しています。

製薬企業とCROのパートナーシップの拡大は、毒物検査サービスの需要を促進します。製薬企業が医薬品開発の取り組みを強化する中、前臨床毒性試験の実施に不可欠なCROの専門知識とインフラを求めています。例えば、Immuterは2023年5月、自己免疫疾患に対応する自社開発候補薬IMP761のGLP(Good Laboratory Practice)毒性試験を実施するため、Charles River Laboratoriesと提携しました。同様に、2024年3月、Badvus ResearchはSouthern Researchと戦略的提携を結び、前臨床毒性試験と薬事承認プロセスに注力しています。これらの提携は、包括的な毒性学的評価を通じて医薬品開発イニシアチブを支援し、規制コンプライアンスを確保する上で、CROが極めて重要な役割を担っていることを強調するものです。

前臨床CROにおける毒性試験は、製薬企業が候補化合物の安全性プロファイルを評価し、開発パイプラインの進行に関して十分な情報に基づいた意思決定を行うことを可能にする、医薬品開発プロセスの重要な要素としての役割を果たしています。それゆえ、製薬企業とCROの垂直的な協力関係の強化は、市場の成長を促進すると考えられます。

北米が2024年から2029年にかけて市場で大きなシェアを占めると予想される

北米の前臨床CRO市場は、自社での医薬品開発・探索コストの上昇、慢性疾患の有病率の上昇、臨床試験の複雑化、開発パイプラインにある多数の治験薬候補から恩恵を受けると予想されます。

心血管疾患、糖尿病、がん、神経疾患などの慢性疾患の有病率の上昇により、新たな治療法や治療法の開発が必要となっています。このような慢性疾患の負担が大きくなりつつあるため、製薬企業はこれらの疾患に対する有望な候補薬を調査するために前臨床試験を外注せざるを得なくなり、これが調査期間中の同国市場の成長を促進すると予測されています。例えば、米国がん協会によると、同国では肺がんの有病率が増加しており、2022年には23万6,740人の肺がん患者が報告されたのに対し、2023年には23万8,340人の肺がん患者が報告されました。このデータは、同国におけるがん罹患率の急激な増加を示しており、2024年から2029年にかけて、がん罹患率はさらに増加すると予測されています。したがって、同国におけるがん罹患率の増加は、先進的な治療薬に対する需要に拍車をかけると予測され、ひいては前臨床試験活動を促進し、調査期間中の同国市場の成長を支援すると予測されています。

加えて、自社での創薬・開発コストが高いことから、製薬企業は臨床試験に伴うコスト負担や複雑さを軽減するために、前臨床試験活動をアウトソーシングしやすくなっています。このように、創薬開発コストは、必要なインフラをすべて備えている前臨床試験受託機関(CRO)の臨床試験実施需要を促進すると予想されます。例えば、世界保健機関(WHO)が2022年に実施した調査によると、新薬開発にかかる平均コストは4,340万米ドルから420万米ドルです。このように、新薬開発に伴う多額のコストは、製薬会社に代わって臨床試験やその他の研究活動を行う前臨床CROの需要を促進すると予想されます。CROは研究サービスを実施するための優れた経験とインフラを持っているためです。このように、研究活動を実施する前臨床CROへの高い需要が、調査期間中の同国市場の成長を支えると予測されます。

したがって、慢性疾患の高い有病率と自社での創薬・市場開拓コストの高さが、2024年から2029年にかけて北米の研究市場を牽引すると予想されます。

前臨床CRO業界の概要

前臨床CRO市場は、世界的に有名な様々なサービスプロバイダーが存在するため、競争が激しく、細分化されています。主要な市場プレイヤーは、ソリューションとサービスの範囲を拡大することで、互いに競争しています。現在、市場を独占している企業は数社です。主要企業は、世界市場での地位を確保するために、買収、提携、高度なサービスの開始など、さまざまな戦略的提携を行っています。これらの企業には、Eurofins Scientific、Charles River Laboratories、WuXi Apptec、Labcorp Drug Development、SGS SAなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 世界の研究開発費の増加

- 前臨床試験中の医薬品数の増加

- 慢性疾患患者による医薬品需要の増加

- 市場抑制要因

- 標準化とモニタリングの欠如

- 厳しい規制政策

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(金額ベース市場規模-米ドル)

- サービス別

- 毒性試験

- バイオアナリシスおよび薬物代謝・薬物動態試験

- 安全性薬理学

- その他のサービス

- モードタイプ別

- 患者由来オルガノイド(PDO)モデル

- 患者由来異種移植片(PDX)モデル

- エンドユーザー別

- バイオ製薬会社

- 研究機関および大学

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Charles River Laboratories

- Labcorp Drug Development

- Thermo Fisher Scientific Inc.(Pharmaceutical Product Development(PPD))

- NorthEast BioAnalytical Laboratories LLC

- Parexel International Corporation

- Medpace

- Eurofins Scientific

- WuXi App Tec

- ICON PLC

- SGS SA

- PharmaLegacy Laboratories

- Altasciences Company Inc.

第7章 市場機会と今後の動向

目次

The Preclinical CRO Market size is estimated at USD 7.10 billion in 2024, and is expected to reach USD 10.10 billion by 2029, growing at a CAGR of 7.44% during the forecast period (2024-2029).

The studied market growth is primarily attributed to increasing research and development (R&D) expenditure worldwide, increasing the number of drugs in preclinical trials, and high demand for medicines uptake by chronically ill patients between 2024 and 2029.

The increasing research and development expenditure in life sciences and substantial public and private funding spending in the sector boosts market growth. For instance, the Indian Ministry of Science and Technology allocated a budget of INR 40 billion (USD 427.20 million) for the Department of Biotechnology (DBT) of India in the Union Budget for the year 2023-2024. The significant increase in funding is primarily due to the increasing R&D expenditure in the country. Hence, the rising research and development expenditure is expected to increase the adoption of preclinical CRO services to decrease the overall cost of the drug development process.

Similarly, the European Federation of Pharmaceutical Industries and Association (EFPIA) pharmaceutical research and development expenditure in 2022 reached USD 44 billion, which grew by 4.6% compared to the 2021 expenditure. Hence, the increasing R&D expenditure in Europe is expected to increase the demand for preclinical CRO services to reduce the expenditure from 2024 to 2029.

Additionally, the increasing number of drugs in preclinical stages is also expected to increase the demand for outsourcing preclinical services to reduce the cost of development and increase the chances of drug approval for conducting clinical trials. For instance, according to the ClinicalTrials.gov 2024 updated data, as of January 2024, nearly 479 thousand clinical studies were registered globally. This significant increase in clinical trials reflects the number of therapeutics and medical devices that have undergone preclinical trials and received New Drug Application Approval (NDA). Hence, the increasing number of drugs in the preclinical trials is expected to drive the studied market between 2024 and 2029.

However, a lack of standardization, monitoring issues, and stringent regulatory policies are expected to hamper the market's growth.

Preclinical CRO Market Trends

The Toxicology Testing Segment is Predicted to Witness Significant Growth Between 2024 and 2029

Toxicology testing involves the evaluation of the potential adverse effects of chemical substances or pharmaceutical compounds on living organisms. It encompasses a range of methodologies to assess these substances' safety profile, including their potential to cause harm or toxicity. In the dynamic landscape of pharmaceutical research and development, the demand for preclinical toxicology testing services offered by contract research organizations (CROs) is witnessing a significant upsurge. This surge can be attributed to various factors, including the increasing collaboration between pharmaceutical companies and CROs and technological advancements enhancing the efficiency and accuracy of toxicology testing processes.

The expanding partnership between pharmaceutical companies and CROs drives the demand for toxicology testing services. As pharmaceutical companies intensify their drug development efforts, they seek CROs' expertise and infrastructure to conduct essential preclinical toxicology studies. For instance, in May 2023, Immuter partnered with Charles River Laboratories to conduct a good laboratory practice (GLP) toxicology study for its proprietary candidate IMP761 to address autoimmune diseases. Similarly, in March 2024, Badvus Research forged a strategic alliance with Southern Research, focusing on preclinical toxicology testing and regulatory approval processes. These collaborations underscore the pivotal role of CROs in supporting drug development initiatives and ensuring regulatory compliance through comprehensive toxicology assessments.

Toxicology testing in preclinical CROs serves as a vital component of the drug development process, enabling pharmaceutical companies to evaluate the safety profiles of their candidates and make informed decisions regarding their progression in the development pipeline. Hence, increasing the vertical collaboration between pharma companies and CROs is likely to enhance the segmental growth of the market.

North America is Expected to Hold a Significant Share of the Market Between 2024 and 2029

The North American preclinical CRO market is expected to benefit from higher in-house drug development and discovery costs, rising prevalence of chronic diseases, increasing complexity in clinical trials, and a high number of investigational candidates in the development pipeline.

The higher prevalence of chronic diseases like cardiovascular diseases, diabetes, cancer, and neurological disorders necessitates the development of new therapies and treatments. Such a high and evolving burden of chronic diseases forces pharma companies to outsource preclinical trials to investigate promising candidates against those diseases, which is projected to foster the country's market growth over the study period. For instance, according to the American Cancer Society, the prevalence of lung cancer is increasing in the country, and the country reported 238,340 lung cancer cases in 2023 compared to 236,740 in 2022. This data shows a rapid increase in the incidence of cancer cases in the country, and between 2024 and 2029, the incidence of cancer will further increase; thus, the escalating burden of cancer cases in the country is projected to spur the demand for advanced therapeutics and which is in turn projected to foster preclinical trial activities and is anticipated to support country's market growth over the study period.

In addition, the higher in-house drug discovery and development costs facilitate pharmaceutical companies to outsource preclinical trial activities to reduce the cost burden and increased complexity associated with clinical trials. Thus, drug discovery and development costs are anticipated to foster demand for preclinical contract research organizations (CROs) to conduct clinical trials as they have all the required infrastructures. For instance, according to a study conducted by the World Health Organization (WHO) in 2022, the average cost to develop a new drug ranges from USD 43.4 million to USD 4.2 million. Thus, the significant cost associated with new drug development is expected to facilitate the demand for preclinical CROs to perform clinical trials and other research activities on behalf of pharmaceutical companies, as CROs have a better experience and infrastructure to conduct research services. Thus, the high demand for preclinical CROs to conduct research activities is projected to support the country's market growth over the study period.

Hence, the high prevalence of chronic diseases and the higher in-house drug discovery and development costs are expected to drive the studied market in North America between 2024 and 2029.

Preclinical CRO Industry Overview

The preclinical CRO market is highly competitive and fragmented in nature, with the presence of various well-known service providers globally. Major market players compete against each other by expanding their range of solutions and services. There are a few companies that are currently dominating the market. Key players have been involved in various strategic alliances such as acquisitions, collaborations, and the launch of advanced services to secure their position in the global market. These companies include Eurofins Scientific, Charles River Laboratories, WuXi Apptec, Labcorp Drug Development, and SGS SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Research and Development (R&D) Expenditure Worldwide

- 4.2.2 Increase in Number of Drugs in Preclinical Trials

- 4.2.3 High Demand for Medicines Uptake by Chronically Ill Patients

- 4.3 Market Restraints

- 4.3.1 Lack of Standardization and Monitoring Issue

- 4.3.2 Stringent Regulatory Policies

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Service

- 5.1.1 Toxicology Testing

- 5.1.2 Bioanalysis and Drug Metabolism and Pharmacokinetics Studies

- 5.1.3 Safety Pharmacology

- 5.1.4 Other Services

- 5.2 By Mode Type

- 5.2.1 Patient Derived Organoid (PDO) Models

- 5.2.2 Patient Derived Xenograft (PDX) Models

- 5.3 By End Users

- 5.3.1 Biopharmaceutical Companies

- 5.3.2 Research Institutes and Universities

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Charles River Laboratories

- 6.1.2 Labcorp Drug Development

- 6.1.3 Thermo Fisher Scientific Inc. (Pharmaceutical Product Development (PPD))

- 6.1.4 NorthEast BioAnalytical Laboratories LLC

- 6.1.5 Parexel International Corporation

- 6.1.6 Medpace

- 6.1.7 Eurofins Scientific

- 6.1.8 WuXi App Tec

- 6.1.9 ICON PLC

- 6.1.10 SGS SA

- 6.1.11 PharmaLegacy Laboratories

- 6.1.12 Altasciences Company Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日