海軍ミサイルとミサイル発射システム:市場シェア分析、産業動向、成長予測(2024年~2029年)

Naval Missiles And Missile Launch Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1537667

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

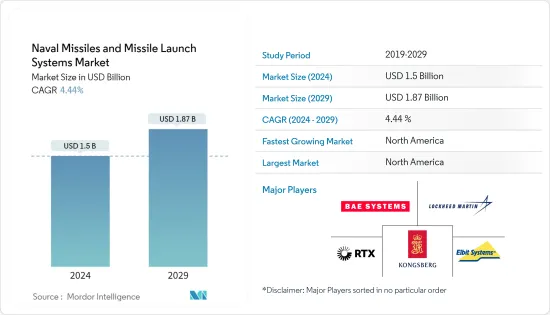

海軍ミサイルとミサイル発射システム市場規模は2024年に15億米ドルと推定され、2029年には18億7,000万米ドルに達し、予測期間(2024-2029年)のCAGRは4.44%で成長すると予測されます。

主なハイライト

- 南シナ海と地中海における各国間の海洋紛争の激化が、新型艦艇の調達と配備に向けた投資を促進しています。海軍は現在、既存の艦艇をアップグレードしたり、老朽化した艦艇を新世代の艦艇に置き換えたりすることで、艦艇の近代化を進めています。新型艦艇に対する需要の高まりは、今後数年間におけるミサイルおよびミサイル発射システムの需要を促進すると予想されます。

- また、世界のさまざまな国が、海上や地上の脅威を追跡して無力化するために、位置ベースの誘導システムを使って標的を正確に排除できる新世代ミサイル・システムの調達に投資しています。同様に、海軍も水上艦船や潜水艦のミサイル発射システムの近代化を進めています。これは、予測期間中の市場の成長を促進すると予想されます。

- ミサイル市場は、その市場開発伴う高コストのために制限に直面する可能性があります。ミサイルに必要な高度な誘導システムやロケットは複雑な技術を必要とするため、全体的な費用がかさみます。さらに、ミサイルは一度発射されると方向を変えることができないため、対ミサイルシステムによる迎撃の影響を受けやすく、市場に悪影響を及ぼす可能性があります。

- しかし、軍や海軍における先端技術の導入の増加は、市場に有利な機会をもたらすと予想されます。例えば、海軍ミサイルとミサイル発射システムにおける人工知能(AI)の統合は、市場の成長を加速させると予想されます。海軍ミサイルとミサイル発射システムのAIは、過去のデータを分析し、海軍司令官に強化された意思決定能力を装備するために様々なシナリオを評価することができます。予測期間中、この市場の需要を促進するのは、検索要因か、またはその両方であると予想されます。

海軍ミサイルとミサイル発射システムの市場動向

予測期間中はミサイルセグメントが市場シェアを独占

- 同市場では現在、ミサイルセグメントが市場を独占しており、ミサイル発射システムに比べて納入数が比較的多いことから、今後もその支配が続くと予想されます。

- このセグメントの成長は、世界の主要国による軍事費の増加と様々な近代化努力によって増加すると予想されます。例えば、2022年の世界の軍事費は2兆2,400億米ドルに達し、これは2021年から6%の成長でした。

- このような巨額の防衛費投資により、さまざまな国々が高度な巡航ミサイルや弾道ミサイルの武器庫を急速に拡大し、増大する艦艇群に強化された攻撃能力を装備しようとしています。例えば、インド国防省は2023年12月、インド海軍の水上プラットフォーム用に450基の中距離対艦ミサイル(MRAShM)の調達資金を承認しました。MRAShMは軽量の地対地ミサイルで、インド海軍の艦船に搭載され、主要な攻撃兵器となります。このターボジェット推進ミサイルの射程は約300kmで、IIRシーカーまたはRFシーカーを装備することができます。

- 同様に2023年12月、スペイン海軍はコングスベルグ・デフェンス&エアロスペース社に3億3,400万米ドルの契約を発注し、海軍攻撃ミサイル(NSM)を納入しました。このミサイルは、ナバンティアが現在建造中のF-110級フリゲートNSMに搭載される予定です。

- さらに、海軍能力を強化し、さまざまなタイプの海洋脅威に効果的に対応するため、人工知能(AI)のような最先端技術の開発を進めている国もあります。例えば、イランは2023年12月、海軍の軍艦にアブ・マハディ巡航ミサイルを装備したと発表しました。このミサイルは、人工知能や空中で進路を変更するためのコマンドガイダンスなどの技術を搭載しており、射程は1000kmを超えます。このような海軍向けの新型ミサイルの開発は、予測期間中の同分野の成長を促進すると予想されます。

予測期間中、北米が市場シェアを独占

- 北米地域が市場シェアを独占している主な理由は、米国の多額の軍事費であり、これが海軍の開発・調達プログラムを支えています。例えば、2022年の米国軍事防衛費は8,770億米ドルに上り、2021年と比較して9%の成長でした。

- この莫大な国防費を背景に、米国は主に海軍と海兵隊の艦隊近代化に投資しており、バランスの取れた海軍力で海上支配力を確立・維持し、あらゆる領域で殺傷力を高めることを目的としています。これらの調達プログラムは、世界な海洋環境における複雑化する脅威に対処するために実施されています。

- 例えば、2024年度予算要求案の一部として、米国海軍は9隻の戦闘艦の調達のために328億米ドルの投資を計画しています。この要求には、2隻目のコロンビア級潜水艦、2隻のブロックVバージニア級高速攻撃型潜水艦、4隻の将来のSSN、2隻のアーレイ・バーク級駆逐艦、2隻のコンステレーション級誘導ミサイルフリゲート艦の先行調達資金が含まれています。

- このような強力な海軍艦隊と誘導プログラムにより、新たな先進ミサイル・システムの需要が発生することが予想されます。例えば、2024年度予算案では、米国海軍は13基の海軍攻撃ミサイル(NSM)、125基の標準ミサイル-6(SM-6)、120基のRAMブロックIIミサイル、147基の進化型シースパローミサイル(ESSM)、海兵隊は90基のNSMミサイルと34基のブロックV戦術トマホーク(TACTOM)ミサイルを調達する計画を発表しています。

海軍ミサイルとミサイル発射システム産業概要

海軍ミサイルとミサイル発射システムの市場は、ごく少数の企業が市場の大半のシェアを占めており、統合されています。海軍ミサイルとミサイル発射システム市場の著名な企業には、RTX Corporation、Lockheed Martin Corporation、BAE Systems plc、Elbit Systems Ltd.、Kongsberg Gruppen ASAなどがあります。

RTX Corporationは、世界中の海軍にミサイルシステムを提供している大手企業です。国際的な企業に加え、国防研究開発機構(DRDO)、ROKETSAN A.S.など、市場開拓を進める地元企業も多いです。現在、各国で国産防衛装備品の開発が重視されるようになっており、市場開発における地元企業の存在感が強まると予想されます。さらに、市場シェアを拡大するため、各社は世界中の軍隊向けに艦艇に搭載する新しいミサイルシステムを開発しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- システム別

- ミサイル

- 発射システム

- 用途別

- 水上艦艇

- 潜水艦

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Lockheed Martin Corporation

- RTX Corporation

- Elbit Systems Ltd.

- MBDA

- Kongsberg Gruppen ASA

- Saab AB

- Rafael Advanced Defense Systems Ltd.

- BAE Systems plc

- ROKETSAN A.S.

- Rostec State Corporation

- IAI

- Defense Research and Development Organization(DRDO)

第7章 市場機会と今後の動向

目次

The Naval Missiles And Missile Launch Systems Market size is estimated at USD 1.5 billion in 2024, and is expected to reach USD 1.87 billion by 2029, growing at a CAGR of 4.44% during the forecast period (2024-2029).

Key Highlights

- The growing maritime disputes in the South China Sea and the Mediterranean Sea among various countries are propelling the investments towards procurement and deployment of new naval vessels. The naval forces are currently modernizing their naval fleet by upgrading their existing naval fleets or replacing their aging fleets with newer-generation vessels. The growing demand for new naval vessels is expected to propel the demand for missile and missile launch systems in the coming years.

- Various countries globally are also investing in the procurement of new-generation missile systems that can precisely eliminate the targets using a position-based guidance system to track and neutralize seaborne and ground-based threats. Similarly, the naval forces are also modernizing the missile firing systems on surface ships and submarines. This is anticipated to drive the growth of the market during the forecast period.

- The market for missiles may face limitations due to the high cost associated with their development. The sophisticated guidance systems and rockets required for missiles necessitate complex technologies that add to their overall expense. Furthermore, the inability of missiles to change direction once launched can make them susceptible to interception by anti-missile systems, which could have an adverse impact on the market.

- However, the increasing implementation of advanced technologies in military and naval forces is expected to bring forth a lucrative opportunity in the market. For instance, the integration of artificial intelligence (AI) in naval missiles and missile launch systems is anticipated to accelerate market growth. AI in naval missiles and missile launch systems is capable of analyzing historical data and assessing various scenarios to equip naval commanders with enhanced decision-making capabilities. Search factors or expected to drive the demand for this market during the forecast period.

Naval Missiles and Missile Launch Systems Market Trends

Missiles Segment To Dominate Market Share During the Forecast Period

- The missiles segment of the market currently dominates the market and is expected to continue its dominance primarily due to their relatively higher deliveries compared to missile launching systems.

- The growth of this segment is expected to increase due to rising military expenditure and various modernization efforts by major global powers. For instance, in 2022, the global military expenditure reached USD 2,240 billion; this was a growth of 6% from the year 2021.

- With this huge investment in defense expenditure, various countries are rapidly expanding their arsenal of advanced cruise and ballistic missiles to equip their growing naval vessel fleet with enhanced attack capabilities. For instance, in December 2023, the Indian MoD approved the funds for the procurement of 450 Medium Range Anti-Ship Missiles (MRAShM) for surface platforms of the Indian Navy. The MRAShM is a lightweight Surface-to-Surface Missile that will be equipped onboard Indian Naval Ships as a primary offensive weapon. The turbojet-propelled missile will have a range of about 300 km, and it can be equipped with an IIR seeker or RF seeker.

- Similarly, in December 2023, the Spanish Navy awarded a USD 334 million contract to Kongsberg Defence & Aerospace to deliver Naval Strike Missiles (NSM). The missiles are planned to be equipped with NSM, a F-110 class frigate, which is currently under construction by Navantia.

- Furthermore, several nations are making progress in developing cutting-edge technologies like artificial intelligence (AI) to enhance their naval capabilities and effectively respond to different types of maritime threats. For instance, in December 2023, Iran announced that it had equipped its naval warships with Abu Mahdi cruise missiles. These missiles feature technologies such as artificial intelligence and command guidance for changing their course mid-air with a range of over 1,000 kilometers. Such developments of new naval missiles for the naval forces are anticipated to drive the growth of the segment during the forecast period.

North America to Dominate Market Share During the Forecast Period

- The North American region dominates market share primarily due to the large military spending of the United States, which in turn supports the development and procurement programs for naval forces. For instance, in 2022, the US military defense expenditure rose to USD 877 billion, with a growth of 9% compared to 2021.

- With this huge defense spending, the US is investing in naval fleet modernization of the Navy and Marine Corps primarily to establish and maintain maritime dominance with a balanced naval force and by employing increased lethality across all domains. These procurement programs are carried out to address increasingly complex threats in the global maritime environment.

- For instance, as part of the FY2024 proposed budget request, the US Navy plans to invest USD 32.8 billion for the procurement of nine battle force ships. The request includes funds for the second Columbia class submarine, two Block V Virginia class fast attack submarines, and advance procurement funds for four future SSNs, two Arleigh Burke-class destroyers, and two Constellation class guided missile frigates.

- With this robust naval fleet and induction programs, it is anticipated to generate demand for new advanced missile systems. For instance, in the FY2024 budget document, the US Navy announced that it plans to procure 13 Naval Strike Missile (NSM) missiles, 125 Standard Missile-6 (SM-6), 120 RAM Block II missiles, 147 Evolved Sea Sparrow Missile (ESSM) and the Marine Corps will procure 90 NSM missiles and 34 Block V Tactical Tomahawk (TACTOM) missiles.

Naval Missiles and Missile Launch Systems Industry Overview

The market of naval missiles and missile launch systems is consolidated with very few players accounting for the majority share in the market. Some of the prominent players in the naval missiles and missile launch systems market are RTX Corporation, Lockheed Martin Corporation, BAE Systems plc, Elbit Systems Ltd., and Kongsberg Gruppen ASA.

RTX Corporation is a major provider of missile systems to naval forces around the world. In addition to the international, there are many local players in the market, such as the Defence Research and Development Organisation (DRDO) and ROKETSAN A.S., among others. Currently, the increasing emphasis on developing local defense equipment in various countries is expected to strengthen local players' presence in the market. Further to increase their share in the market, the companies are developing new missile systems onboard naval vessels for the armed forces around the world.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Systems

- 5.1.1 Missiles

- 5.1.2 Launch Systems

- 5.2 Application

- 5.2.1 Surface Vessels

- 5.2.2 Submarines

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Lockheed Martin Corporation

- 6.2.2 RTX Corporation

- 6.2.3 Elbit Systems Ltd.

- 6.2.4 MBDA

- 6.2.5 Kongsberg Gruppen ASA

- 6.2.6 Saab AB

- 6.2.7 Rafael Advanced Defense Systems Ltd.

- 6.2.8 BAE Systems plc

- 6.2.9 ROKETSAN A.S.

- 6.2.10 Rostec State Corporation

- 6.2.11 IAI

- 6.2.12 Defense Research and Development Organization (DRDO)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日