|

市場調査レポート

商品コード

1537664

航空機用カメラ:市場シェア分析、産業動向と統計、成長予測(2024~2029年)Aircraft Cameras - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機用カメラ:市場シェア分析、産業動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年08月14日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

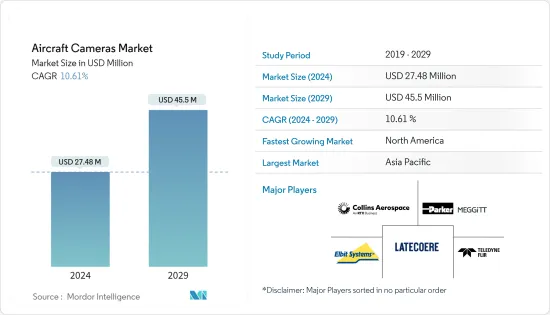

航空機用カメラ市場規模は2024年に2,748万米ドルと推定・予測され、2029年には4,550万米ドルに達し、予測期間中(2024-2029年)のCAGRは10.61%で成長すると予測されています。

航空機用カメラは、航空機内外で多くの機能を果たします。これらの用途は、地上操縦や機内監視から外部セキュリティ対策まで多岐にわたります。航空機カメラは、給油、監視、照準など軍事作戦において重要な役割を果たし、観察、識別、自己防衛を支援します。

旅客輸送量の増加が民間航空機の需要を牽引しており、今後数年間で多くの納入が見込まれます。同時に、世界各国が軍事力の近代化に注力するなか、次世代軍用機への関心も高まっています。このような民間機と軍用機の急増は、航空機用カメラの需要を直接的に押し上げます。

しかし、カメラ画像技術のコストが高く、危険な事象による損傷を受けやすいという課題があります。これらの課題は、特に小規模の航空会社にとっては、このような技術の経済的な実行可能性を妨げる可能性があります。このようなハードルがあるにもかかわらず、解像度の向上、低照度性能の向上、洗練されたデザインなど、カメラ技術の進歩は続いており、この市場は有望です。このような技術革新をリードするメーカーは、航空機向けに最先端のカメラ・ソリューションを提供することで、競争優位に立つ態勢を整えています。

航空機用カメラ市場動向

市場シェアを独占する軍用機セグメント

- 軍用機は、監視や状況認識から照準や自己防衛に至るまで、無数の機能においてカメラに依存しています。2023年、世界の軍事費は2兆4,400億米ドルに達しました。現代の軍用機、特に最新世代の軍用機は、その多様な運用のために画像センサに大きく依存しています。軍用機に対する需要の高まりは、軍用機パイロットの状況認識強化の必要性と相まって、この市場セグメントの成長を後押ししています。2023年8月、米国政府は5億米ドルの対外軍事販売契約に基づき、F-16ファイティング・ファルコン用赤外線捜索・追跡(IRST)技術の台湾への販売を承認しました。高度なカメラとISRツールであるこのIRSTは、台湾の空中支配を確保する上で極めて重要です。

- さらに、大手OEMは、最先端のマルチスペクトルIRレーザーベースの対策システムの開発の先頭に立っています。これらのシステムは、大型の固定翼から回転翼まで、幅広い航空機を赤外線誘導ミサイルの脅威から守るために設計されています。例えば、2023年8月、Elbit SystemsはDALO Days 2023で、指向性IR対策(DIRCM)を含む一連のソリューションを発表しました。展示されたDIRCMソリューションは、高度なレーザー技術と高フレームレートのサーマルカメラを搭載し、迅速かつ正確な脅威検知と妨害に優れています。Elbit SystemsのDIRCMソリューションは、イスラエル空軍、NATO、ドイツ空軍、イタリア空軍、ブラジル空軍など、軍用機やヘリコプターを守るための著名な組織から信頼を得ています。このような進歩は、今後数年間、このセグメントの成長を促進するものと思われます。

アジア太平洋地域が最大の市場シェアを占める見込み

- 予測期間中、アジア太平洋地域は、軍用機と民間機の両方に対する需要の高まりに牽引され、航空機用カメラの支配的な市場として台頭する見込みです。同地域の国際旅客数は堅調に回復しており、民間航空セクターを強化することになります。

- 注目すべきは、2023年6月にエア・インディアがエアバス社およびボーイング社と契約を締結し、それぞれ250機と220機を発注したことです。ボーイングのB777Xのラインナップは、パイロットの機首とメインギア付近の視界を補助する地上操縦カメラシステム(GMCS)を備えているのが特徴です。2023年12月、エア・インディアはエアバスとA350-900型機20機とA350-1000型機20機の契約を締結し、保有機をさらに増強しました。大手航空機メーカー各社は、航空機の安全性、特に着陸時の安全性を高めるため、カメラシステムの開発に力を入れています。例えばエアバスは、2023年1月にDragonFly飛行システムの試験を開始し、特に緊急時にコンピュータ・ビジョンと複数のカメラを使用して航空機を自律的に着陸させる能力を披露しました。

- 軍事分野では、カメラは軍用機のISR作戦において極めて重要な役割を果たしています。特に、アジア太平洋のいくつかの国では、偵察機を高度なEO/IRカメラでアップグレードしています。2023年3月の注目すべき動きとして、タイ海軍はゼネラル・アトミクス・エアロテック・システムズ(GA-ATS)に2機のドルニエ228の大規模な近代化とメンテナンスを依頼し、360°ミッション・レーダーと電子光学/赤外線カメラを装備しました。このような発展は、世界中で市場の成長を牽引しています。

航空機用カメラ産業概要

航空機用カメラ市場は半固定的であり、少数のプレイヤーのみが主要な市場シェアを占めています。Elbit Systems Ltd、LATECOERE SA、Meggitt Ltd、Teledyne FLIR LLC、Collins Aerospace(RTX Corporation)が市場の著名なプレーヤーです。市場参入企業は、航空機用カメラ製品を強化するために研究開発投資を大幅に増やしています。状況認識を高め、新たな顧客層を獲得するのが狙いです。

さらに、これらのプレーヤーは航空機OEMとの契約延長を戦略的に追求しています。このような契約は持続的な収益を約束し、航空機プログラムの期間が複数年に及ぶことから、非常に有利です。さらに、特に軍用分野では、国産化を推進する政府のイニシアチブに後押しされ、新規参入企業が急増しています。こうした新規参入により、今後数年間は市場競争が激化することが予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途別

- 民間航空機

- 軍用機

- タイプ別

- 内部カメラ

- 外部カメラ

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- KID-Systeme GmbH

- LATECOERE SA

- Meggitt Ltd

- Teledyne FLIR LLC

- Collins Aerospace(RTX Corporation)

- AD Aerospace Ltd

- Kappa optronics GmbH

- Cabin Avionics Limited

- Eirtech Aviation Services Limited

- Elbit Systems Ltd

- L3Harris Technologies Inc.

- THALES

第7章 市場機会と今後の動向

The Aircraft Cameras Market size is estimated at USD 27.48 million in 2024, and is expected to reach USD 45.5 million by 2029, growing at a CAGR of 10.61% during the forecast period (2024-2029).

Aircraft cameras serve a multitude of functions both within and outside aircraft. These applications range from ground maneuvering and cabin surveillance to external security measures. They play a crucial role in military operations, including refueling, surveillance, and targeting, aiding in observation, identification, and self-protection.

Rising passenger traffic is driving the demand for commercial aircraft, with many deliveries expected in the upcoming years. Simultaneously, as nations globally focus on modernizing their military capabilities, there is a heightened interest in next-gen military aircraft. This surge in commercial and military aircraft directly boosts the demand for aircraft cameras.

However, the high cost of camera imaging technology and its susceptibility to damage from hazardous events present challenges. These challenges could impede such technology's economic viability, particularly for smaller airlines. Despite these hurdles, ongoing advancements in camera technology, like improved resolution, better low-light performance, and sleeker designs, paint a promising picture for the market. Manufacturers leading these innovations are poised to gain a competitive edge by providing state-of-the-art camera solutions for aerial vehicles.

Aircraft Cameras Market Trends

Military Aircraft Segment to Dominate Market Share

- Military aircraft rely on cameras for myriad functions, from surveillance and situational awareness to targeting and self-protection. In 2023, global military expenditure reached a substantial USD 2.44 trillion. Modern military aircraft, especially the latest generations, heavily lean on imaging sensors for their diverse operations. The rising demand for military aircraft, coupled with the imperative for heightened situational awareness among military pilots, is propelling the growth of this market segment. In August 2023, the US government, under a USD 500 million Foreign Military Sales agreement, approved the sale of infrared search and track (IRST) technology to Taiwan for its F-16 Fighting Falcon fleet. This IRST, a sophisticated camera and ISR tool, is pivotal in securing aerial dominance for Taiwan.

- Furthermore, leading OEMs spearhead the development of cutting-edge multi-spectral IR laser-based countermeasure systems. These systems are designed to shield a broad spectrum of aircraft, ranging from large fixed to rotary wings, from the threat of infrared-guided missiles. For instance, in August 2023, Elbit Systems unveiled its suite of solutions, including the Directed IR Countermeasures (DIRCM), at DALO Days 2023. The showcased DIRCM solution, equipped with advanced laser technology and a high frame-rate thermal camera, excels in swift and precise threat detection and jamming. Elbit Systems' DIRCM solutions have garnered the trust of several prominent entities, such as the Israel Airforce, NATO, and the German, Italian, and Brazilian Air forces, for safeguarding their military aircraft and helicopters. These advancements are poised to fuel the segment's growth in the coming years.

Asia-Pacific Expected to Hold Largest Market Share

- During the forecast period, Asia-Pacific is poised to emerge as the dominant market for aircraft cameras, driven by escalating demands for both military and commercial aircraft. The region's robust rebound in international passenger traffic is set to bolster its commercial aviation sector.

- Notably, in June 2023, Air India inked deals with Airbus and Boeing, ordering 250 and 220 aircraft, respectively, with a subset of 10 B777X jets. Boeing's B777X lineup notably features a Ground Maneuver Camera System (GMCS), aiding pilots with views of the nose and main gear areas. In December 2023, Air India further bolstered its fleet by reaching a contract with Airbus for 20 A350-900s and 20 A350-1000s, highlighting the A350's tail cameras, designed to assist pilots during ground maneuvers. Major aircraft OEMs have intensified their focus on developing camera systems to enhance aircraft safety, particularly during landings. Airbus, for instance, initiated tests in January 2023 with its DragonFly flight system, showcasing its ability to autonomously land aircraft using computer vision and multiple cameras, especially in emergencies.

- In the military, cameras play a pivotal role in ISR operations on military aircraft. Notably, several countries in the Asia-Pacific are upgrading their surveillance aircraft with advanced EO/IR cameras. In a notable move in March 2023, the Royal Thai Navy enlisted General Atomics AeroTec Systems (GA-ATS) for extensive modernization and maintenance on two Dornier 228s, equipping them with a 360° mission radar and electro-optical/infrared camera. Such developments are driving the market's growth across the globe.

Aircraft Cameras Industry Overview

The aircraft cameras market is semi-consolidated, as only a few players account for a major market share. Elbit Systems Ltd, LATECOERE SA, Meggitt Ltd, Teledyne FLIR LLC, and Collins Aerospace (RTX Corporation) are prominent players in the market. Market players are significantly increasing their R&D investments to enhance their aircraft camera products. They aim to boost situational awareness and entice a fresh customer base.

Moreover, these players are strategically pursuing extended contracts with aircraft OEMs. Such agreements promise sustained revenues and are incredibly lucrative given the multi-year duration of aircraft programs. Additionally, a surge of new entrants, particularly in the military segment, is being witnessed, spurred by governmental initiatives favoring indigenization. This influx is poised to intensify market competition in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Commercial Aircraft

- 5.1.2 Military Aircraft

- 5.2 By Type

- 5.2.1 Internal Cameras

- 5.2.2 External Cameras

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 KID-Systeme GmbH

- 6.2.2 LATECOERE SA

- 6.2.3 Meggitt Ltd

- 6.2.4 Teledyne FLIR LLC

- 6.2.5 Collins Aerospace (RTX Corporation)

- 6.2.6 AD Aerospace Ltd

- 6.2.7 Kappa optronics GmbH

- 6.2.8 Cabin Avionics Limited

- 6.2.9 Eirtech Aviation Services Limited

- 6.2.10 Elbit Systems Ltd

- 6.2.11 L3Harris Technologies Inc.

- 6.2.12 THALES