|

市場調査レポート

商品コード

1910879

鉱物処理設備:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Mineral Processing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 鉱物処理設備:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

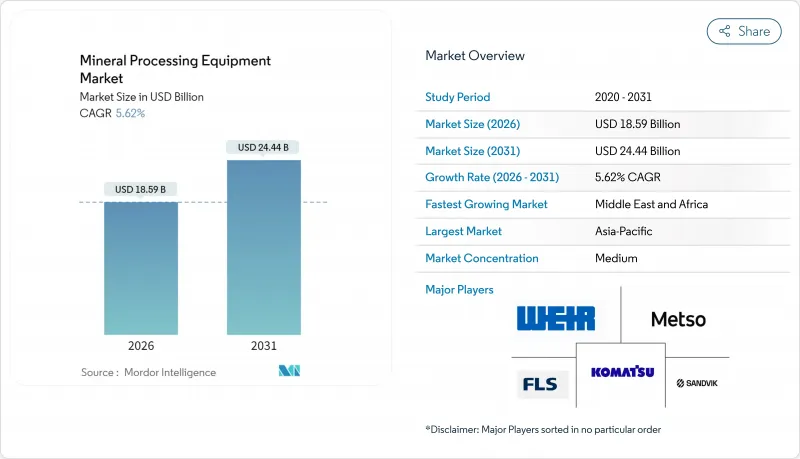

鉱物処理設備市場は、2025年に176億1,000万米ドルと評価され、2026年の185億9,000万米ドルから2031年までに244億4,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは5.62%と見込まれます。

鉱石品位の継続的な低下、エネルギー転換金属の需要急増、環境基準の強化が相まって、高容量でデジタル技術を活用したプラントを重視する複数年にわたる投資サイクルが強化されています。リチウム、ニッケル、希土類元素への需要拡大により、微粉砕、精密分離、高度な粉塵抑制システム向けの設備受注が増加しています。生産者はトン当たりコストとスコープ1排出量の削減を優先し、高圧粉砕ロール(HPGR)やカラム浮選などの技術を採用しています。遠隔地鉱山運営者が稼働時間の保証と予知保全を求める中、アフターマーケットサービスは戦略的重要性を増しています。サプライチェーンのナショナリズムにより、北米・欧州・アジアにおける国内処理能力の拡充が急務となり、鉱物処理設備市場の機会はさらに拡大しています。

世界の鉱物処理設備市場の動向と展望

EV・バッテリー用金属ブーム(リチウム、ニッケル)

電池グレード原料の需要急増が鉱物処理設備市場に顕著な変化をもたらしています。リチウムプロジェクトでは99.5%以上の純度を達成可能な特殊な焙焼・浸出・結晶化回路が必要となり、メッツォ社のpCAMおよびカルシナーパッケージの新規受注を促進しています。ニッケルラテライト処理においても、大型オートクレーブ、硫酸浸出反応器、下流の溶媒抽出装置が同様に恩恵を受けています。高温・高圧設計の実績を有するOEMメーカーは、オーストラリア、インドネシア、チリにおける統合型電池金属ハブの投資家による迅速な推進に伴い、高利益率を維持しております。この結果生じた生産能力の拡大は、バルク商品への支出が抑制される局面においても、二桁の設備需要を持続させております。サプライヤー各社はまた、電池金属1トン当たりの製造過程における排出量を遡及的に追跡するESG報告モジュールを統合しております。

高品位鉱石への移行が高容量クラッシャーを牽引

銅、金、鉄鉱石の原鉱品位は低下を続けており、金属生産量を維持するためにはプラントがより多くのトン数を処理する必要が生じています。HPGR回路は20~40%の省エネルギー効果と微細な製品粒度分布を実現し、下流の浮選回収率を向上させます。これはウィアグループのENDURON導入事例(オーストラリアおよびチリの鉱山)で実証されており、同鉱山では2万トン/時の定格能力を持つ一次破砕機を改造し、制御ループを閉じるリアルタイム粒子径分析装置を補完的に導入しています。この連鎖効果により、高スラリー量に対応したスクリーン、サイクロン、脱水装置の需要が高まっています。粉砕から分級までの統合パッケージを提供するサプライヤーは、付加的なサービス収益を獲得し、鉱物処理機器市場における高処理量・低比エネルギーソリューションへの注力を強化しています。

新規鉱山開発におけるESG主導の資本配分

機関投資家が厳格なESGフィルターを適用した結果、新規鉱山の認可が遅延し、関連プラントの受注も後退しております。カナダのグリーンフィールド鉄鉱石・銅プロジェクトでは、カーボンニュートラルな処理設計が事前要件となり、設置コストが最大20%増加する状況です。許可取得サイクルの長期化により、粉砕機や粉砕ミルに対する短期的な需要は縮小する一方、粉塵抑制システムや水リサイクルシステムの改造注文は増加しています。OEMメーカーは、土地の改変を最小限に抑え、環境審査期間を短縮するモジュール式で移動可能なプラントで対応し、鉱物処理機器市場において小規模で迅速な購買注文のパイプラインを維持しています。

セグメント分析

2031年までのリチウムの驚異的な13.58%のCAGRは、鉱物処理設備市場における構造的変化を浮き彫りにしています。2025年時点では「その他」に分類されるバルク商品が依然として鉱物処理設備市場規模の89.55%を占めていましたが、電池用金属プラントでは、超低不純物閾値に対応した焼成キルン、溶媒抽出ミキサー、結晶化装置が指定されています。鉱物処理装置市場は、自動車メーカーが安全で追跡可能なサプライチェーンを求める中、投資家の関心を集めております。従来の鉄鉱石や銅の流通量は依然として膨大ですが、その一桁台の成長率は、重要鉱物回路における二桁の拡大と鮮明な対照をなしております。

銅・金鉱石の品位低下が続く中、HPGR(ハイパープレーン加圧研削)、微粉砕、フラッシュ浮選装置への設備投資サイクルは長期化しています。処理量は少ないもの、希土類元素回路は複雑な多段階分離を必要とし、高単価を実現することで利益率向上に寄与しています。このためサプライヤーは、従来型バルク商品への依存と高成長の特殊分野とのバランスを取るべく、湿式冶金法や選択的浸出技術への研究開発を重点的に進めています。

2025年時点では粉砕機・粉砕装置が鉱物処理設備市場規模の最大シェア32.72%を占めましたが、高度な浮選セルは2031年までに5.88%という最速のCAGRを記録しました。複雑な鉛・亜鉛鉱石やニッケル鉱石を処理するプラントでは、品位維持のため自動化されたエアフローシステムやフロスカメラシステムが採用されています。統合型スキッドマウント式浮選モジュールは納期を6ヶ月に短縮し、迅速なリチウムプロジェクトに適しています。

下流工程では、高率増粘装置およびペースト充填プラントが尾鉱ダムのリスクに対応し、摩耗性能センサー付きスマートスラリーポンプがオーバーホール間隔を延長します。したがって、鉱物処理装置の市場シェア構成は、水資源管理と価値回収の優先度向上を反映し、分離処理と尾鉱処理へと徐々に移行しています。

地域別分析

2025年の売上高の67.92%を占めるアジア太平洋地域は、鉱物処理設備市場の中核であり続けております。中国の巨大な製錬・精製基盤は、比類のない規模でクラッシャー、ミル、ろ過パッケージを吸収しております。豪州の鉄鉱石大手は年間7億トン超の生産能力を確約し、高圧輻圧管(HPGR)や選別設備のアップグレードを継続。一方、インドネシアのニッケルラテライトプロジェクトではオートクレーブや酸プラントの連携が指定されています。インドの重要鉱物向け生産連動型奨励制度(PLI)と鉱業法改正は、2025年から2030年にかけての設備需要増加を支える新規リチウム・グラファイト開発を促進します。

中東・アフリカ地域は2031年までCAGR9.82%と最も高い伸びを示し、サウジアラビア、ナミビア、アンゴラでは国家資本を投入し、リン酸塩、銅、希土類資源の収益化を進めています。太陽光発電による海水淡水化プラントが水を大量に消費する濃縮プラントに供給され、単位あたりの運用コストを削減します。マアデンの大規模リン酸塩複合施設は、鉱山から肥料までの統合フローの好例であり、ポンプ、増粘装置、ロータリー乾燥機向けのサービス契約を獲得しています。ダーバン、マスカット、テマに設置された地域メンテナンス拠点は物流遅延を軽減し、現地技術者への投資を行うOEMメーカーに有利に働きます。北米と欧州では、サプライチェーンの安全保障政策を背景に、中程度の単一桁成長率を記録しています。米国連邦政府の助成金は国内水酸化リチウム精製所の早期稼働を促進し、焼成装置や結晶化装置の専門メーカーに利益をもたらしています。EUの重要原材料法は希土類分離とバッテリーリサイクルを補助し、カラム浮選装置や湿式製錬プラントの受注を押し上げています。南米のリチウム三角地帯は勢いを維持していますが、アンデス高地の用水制限により、より少ない塩水を消費する直接リチウム抽出(DLE)モジュールの採用が促進されています。地政学、ESG要件、資源ナショナリズムが相まって地域の設備調達パターンを再構築し、鉱物処理設備市場の幅広い成長を持続させています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EV用バッテリー金属ブーム(リチウム、ニッケル)

- 高品位鉱石への移行が高容量クラッシャー需要を牽引

- アフリカにおける重要鉱物プロジェクトの設備投資急増

- プラント全体の最適化に向けたデジタルツインの導入

- グリーン・スチール構想によるペレット化需要の増加

- AIを活用した鉱石選別による下流工程のエネルギー消費削減

- 市場抑制要因

- グリーンフィールド鉱山におけるESG主導の資本配分

- 粒子状物質排出基準の強化

- 遠隔地域における熟練労働力の不足

- 主要スペアパーツにおける地政学的サプライチェーン・ナショナリズム

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額(米ドル))

- 鉱物採掘セクター別

- ボーキサイト

- 銅

- 鉄

- リチウム

- ニッケル

- 希土類元素

- 金および貴金属

- その他

- 機器別

- 粉砕機および粉砕装置

- スクリーンおよび分離機

- フィーダーおよびコンベヤ

- ドリルおよびブレーカー

- 増粘と清澄化

- 浮選セル

- 磁気分離機および重力分離機

- ポンプおよびバルブ

- ろ過および脱水

- 製造工程別

- 粉砕および粉砕

- 選別と分類

- 濃縮(浮選/分離)

- 脱水処理

- マテリアルハンドリング

- エンドユーザー業界別

- 鉱物・鉱石採掘企業

- 受託加工プラント

- リサイクルおよび二次金属

- 骨材・建設資材

- 地域

- 北米

- 米国

- カナダ

- その他北米地域

- 南米

- ブラジル

- チリ

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- オーストラリア

- 日本

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- トルコ

- エジプト

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- FLSmidth A/S

- Metso Corporation

- Komatsu Ltd.

- Sandvik AB

- The Weir Group PLC

- ThyssenKrupp AG

- TAKRAF GmbH

- CITIC Heavy Industries Co., Ltd.

- Terex Corporation

- Wirtgen GmbH

- Multotec(Pty)Ltd

- FEECO International, Inc.

- McLanahan Corporation

- Tenova S.p.A.

- Haver & Boecker Niagara GmbH

- Derrick Corporation

- Eriez Manufacturing Co.

- Astec Industries, Inc.

- Sotecma S.L.