スリップ添加剤:市場シェア分析、産業動向・統計、成長予測(2024~2029年)

Slip Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1537608

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

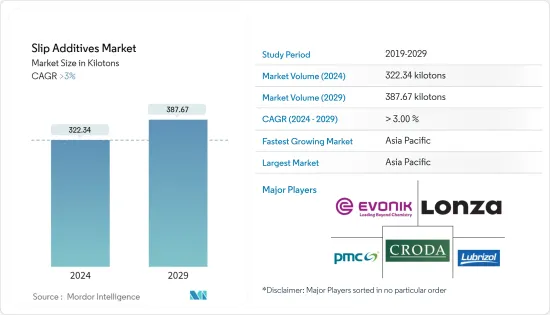

世界のスリップ添加剤の市場規模は、2024年に322.34キロトンに達し、2024~2029年の予測期間中にCAGR 3%超の成長率で推移し、2029年には387.67キロトンに達すると予測されています。

COVID-19パンデミックはスリップ添加剤市場にプラスの影響を与えました。封鎖期間中、消費財、医薬品、食品・飲料などのオンライン販売が包装製品の需要を増加させたため、スリップ添加剤の市場見通しは明るいものとなった。COVID-19の大流行後、包装用途と非包装用途の需要増加により、市場はさらに成長率を記録しました。

食品・飲料包装産業からの需要の増加と、代替品に比べ低価格で入手できることが、シリコーンコーティング市場を牽引すると予想されます。

プラスチックの使用に関する厳しい環境規制が市場の成長を妨げると予想されます。

バイオベースのスリップ添加剤の市場開拓と、医療用途におけるプラスチックフィルムの需要増は、予測期間中に市場にチャンスをもたらすと予想されます。

アジア太平洋が市場を独占すると予想されます。また、包装用途および非包装用途におけるスリップ添加剤の需要増加により、予測期間中に最も高いCAGRで推移することが予想されます。

スリップ添加剤の市場動向

包装用途が市場を独占

- スリップ添加剤の需要が増加している主な要因は、食品・飲料産業における使用量の増加です。プラスチック包装は、包装された製品の貯蔵寿命を延ばし、食品の漏れを減らすのに役立ちます。

- 包装産業の重要な動向のひとつに、製品の安全性と衛生を損なうことなく包装廃棄物を削減するために、使い捨てプラスチックの使用が禁止されていることが挙げられます。これらの要因によって、ポリオレフィンプラスチック包装用フィルムの需要は増加すると思われます。スリップ添加剤は摩擦を減少させるために使用され、包装材料に望ましい特性を持たせるのに役立つと思われます。

- 包装分野は、スリップ添加剤の最も広範な用途になると予想されます。ポリマーフィルムは、主に包装やラベリングに使用される。ポリエチレンフィルムやキャストフィルムの製造におけるスリップ添加剤の重要な役割は、フィルム表面にスリップ特性を付与することです。

- 食品包装市場は、今後数年間で大きな成長率を記録する可能性が高いです。Foodservice Packaging Associationによると、世界の食品包装市場の売上は2022年に3億6,380万米ドルを記録し、2026年には4億5,830万米ドルに達すると予測されています。したがって、食品包装市場の成長は、現在の研究市場を牽引すると思われます。

- 医薬品産業では、ポリエチレンとポリプロピレン包装が一次包装材料として広く使用されています。これらの包装材料は汎用性が高く、高性能であり、医療・製薬用途で使用されています。プラスチックフィルムは、酸素や臭気、湿気、水蒸気透過、汚染、バクテリアから医薬品を保護します。プラスチックフィルムは、スポイト、注射器など様々なプラスチック包装製品に使用されています。世界の医薬品市場は近年大きく成長しています。2022年、世界の医薬品市場は前年比4.2%の成長率で1兆4,800億米ドルを記録しました。

- このように、食品・飲料包装と医薬品包装用途の需要拡大が、スリップ添加剤の需要を牽引することになります。

アジア太平洋が市場を独占する

- アジア太平洋は、世界最大のスリップ添加剤市場です。中国、インド、および日本が、この地域のスリップ添加剤の最大市場です。

- アジア太平洋では、中間層人口の増加、急速な工業化、包装製品の使用量の増加などの要因が包装産業を牽引し、スリップ添加剤市場にさまざまな成長見通しをもたらしていると予想されます。

- 中国とインドは、この地域最大の食品・飲料市場です。中国国家軽工業委員会によると、年間売上高が280万米ドルを超える主要な食品製造企業は、2022年に1兆5,300億米ドルを超える収益を報告しました。2021年と比較すると、総収入は前年比5.6%増を記録し、食品産業の力強い成長を示しています。したがって、食品・飲料産業の成長により、食品・飲料包装用途に使用されるスリップ添加剤の需要が増加すると予想されます。

- 同様に、医薬品包装用途でもスリップ添加剤の需要が増加しています。インドは世界の医薬品ハブであり、200カ国以上に医薬品を輸出しています。2023年度上半期には、医薬品産業への外国直接投資流入額が25%増加しました。IBEFによると、製薬産業の収益は2024年までに650億米ドルに達すると予想されています。したがって、医薬品市場の拡大が現在の研究市場を牽引することになります。

- 日本は現在、世界で3番目に著名なeコマース市場です。日本のeコマース市場の収益は、2023年までに2,322億米ドルを生み出し、さらに2027年までに3,554億米ドルに達すると予想されています。また、日本の化粧品市場で商品を購入する消費者は、より選択的になり、価値への意識が高まっています。そのため、eコマース市場の拡大が日本での包装用途を促進し、スリップ添加剤市場を牽引することになります。

- 上記の要因から、アジア太平洋のスリップ添加剤市場は予測期間中に大きく成長すると予測されます。

スリップ添加剤産業の概要

スリップ添加剤市場は、その性質上、部分的に断片化されています。同市場の主要企業には、Croda International Plc、Evonik Industries AG、Lonza、PMC Group, Inc.、The Lubrizol Corporationなどが挙げられます(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 食品・飲料包装産業からの需要増加

- 代替品と比較した低価格での入手可能性

- その他の促進要因

- 抑制要因

- プラスチックの使用に関する厳しい環境規制

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模:数量ベース)

- キャリア樹脂

- ポリエチレン

- ポリプロピレン

- その他のキャリア樹脂

- タイプ

- 脂肪アミド

- ワックス・ポリシロキサン

- その他のタイプ

- 用途

- 包装

- 食品・飲料

- 消費財

- ヘルスケア

- 非包装

- 包装

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- 合併・買収、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Afron

- ALTANA

- BASF SE

- Croda International Inc.

- Emery Oleochemicals

- Evonik Industries AG

- Fine Organics

- Honeywell International

- Lonza

- The Lubrizol Corporation

- PMC Group, Inc.

第7章 市場機会と今後の動向

- バイオベースのスリップ添加剤の開発

- 医療用途におけるプラスチックフィルム需要の増加

目次

The Slip Additives Market size is estimated at 322.34 kilotons in 2024, and is expected to reach 387.67 kilotons by 2029, growing at a CAGR of greater than 3% during the forecast period (2024-2029).

The COVID-19 pandemic had a positive impact on the slip additives market. During the lockdown, the online sales of consumer goods, pharmaceuticals, food, and beverage products increased the demand for packaged products, thus creating a positive market outlook for slip additives. Post-COVID-19 pandemic, the market further registered a growth rate due to rising demand from packaging and non-packaging applications.

Increasing demand from the food and beverage packaging industry and the availability at low prices compared to substitutes are expected to drive the market for silicone coatings.

The stringent environmental regulations on the use of plastics are expected to hinder the market's growth.

The development of bio-based slip additives and the increasing demand for plastic films in medical applications are expected to create opportunities for the market during the forecast period.

The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to rising demand for slip additives in packaging and non-packaging applications.

Slip Additives Market Trends

Packaging Application to Dominate the Market

- The increasing demand for slip additives is majorly attributed to the growing usage in the food & beverage industry. Plastic packaging helps increase the shelf life of the products packed and reduces leakages of food products.

- One of the significant trends in the packaging industry is the ban on the usage of single-use plastic to reduce packaging waste without compromising the safety and hygiene of the products. These factors will increase the demand for polyolefin plastic packaging films. The slip additives are used to decrease friction and will likely help to get the desired properties in the packaging material.

- The packaging segment is anticipated to be the most extensive application of slip additives. Polymer films are mainly preferred in the packaging industry for packing and labeling. The critical function of slip additives in the production of polyethylene and cast film is to deliver slip properties to the film surface.

- The food packaging market is likely to register a significant growth rate in the coming years. According to the Foodservice Packaging Association, the global food packaging market revenue is recorded at USD 363.8 million in 2022, and it is projected to reach USD 458.3 million by 2026. Thus, the growth in the food packaging market will drive the current studied market.

- In the pharmaceutical industry, polyethylene and polypropylene packaging are widely used as primary packaging materials. These packaging materials are versatile, high-performance, and used in medical and pharmaceutical applications. The plastic films protect the pharmaceutical product against oxygen and odor, moisture, water vapor transmission, contamination, and bacteria. They are used in various plastic packaging products, including eyedroppers, syringes, and others. The global pharmaceutical market has grown significantly in recent years. In 2022, the global pharmaceutical market registered at USD 1.48 trillion, at a growth rate of 4.2% compared to the previous year.

- Thus, the growing demand for food and beverage packaging and pharmaceutical packaging applications will drive the demand for slip additives.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific is the largest market for slip additives in the world. China, India, and Japan are the largest markets for slip additives in the region.

- In the Asia-Pacific region, factors such as the growing middle-class population, rapid industrialization, and the increasing usage of packed products are expected to drive the packaging industry, providing various growth prospects to the slip additives market.

- China and India are the largest food and beverage markets in the region. According to the China National Light Industry Council, major food manufacturing companies with an annual turnover of over USD 2.8 million reported revenues of over USD 1.53 trillion in 2022. Compared to 2021, the total revenue registered a year-on-year growth of 5.6%, indicating strong growth in the food industry. Thus, the growth of the food and beverage industries is expected to increase the demand for slip additives used in food and beverage packaging applications.

- Similarly, the demand for slip additives is increasing in pharmaceutical packaging applications. India is a global pharmaceutical hub, exporting pharmaceuticals to over 200 countries. In the first half of FY 2023, foreign direct investment inflows into the pharmaceutical industry increased by 25%. According to IBEF, the pharmaceutical industry revenue is expected to reach USD 65 billion by 2024. Thus, the increasing market for pharmaceuticals will drive the current studied market.

- Japan is currently the world's third most prominent e-commerce market in the world. Revenue in the e-commerce market in Japan was expected to generate USD 232.20 billion by 2023 and is further expected to reach USD 355.40 billion by 2027. Also, consumers purchasing goods within the cosmetics market in Japan are becoming more selective and value-conscious. Thus, the increasing e-commerce market will drive the packaging application in the country, thereby driving the market for slip additives.

- Owing to the factors mentioned above, the slip additives market in the Asia-Pacific is projected to grow significantly during the forecast period.

Slip Additives Industry Overview

The slip additives market is partially fragmented in nature. Some of the major players in the market include (not in any particular order) Croda International Plc, Evonik Industries AG, Lonza, PMC Group, Inc., and The Lubrizol Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Food & Beverage Packaging Industry

- 4.1.2 Availability at Low Price Compared to Substitutes

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations on The Use of Plastics

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Carrier Resin

- 5.1.1 Polyethylene

- 5.1.2 Polypropylene

- 5.1.3 Other Carrier Resins (Polyvinyl Chloride, Polyamide,etc.)

- 5.2 Type

- 5.2.1 Fatty Amides

- 5.2.2 Waxes and Polysiloxanes

- 5.2.3 Other Types (Esters, Salts, etc.)

- 5.3 Application

- 5.3.1 Packaging

- 5.3.1.1 Food and Beverage

- 5.3.1.2 Consumer Goods

- 5.3.1.3 Healthcare

- 5.3.2 Non-Packaging

- 5.3.1 Packaging

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Afron

- 6.4.2 ALTANA

- 6.4.3 BASF SE

- 6.4.4 Croda International Inc.

- 6.4.5 Emery Oleochemicals

- 6.4.6 Evonik Industries AG

- 6.4.7 Fine Organics

- 6.4.8 Honeywell International

- 6.4.9 Lonza

- 6.4.10 The Lubrizol Corporation

- 6.4.11 PMC Group, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Bio-based Slip Additives

- 7.2 The Increasing Demand for Plastic Films in Medical Applications

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日