磁性材料:市場シェア分析、産業動向・統計、成長予測(2024~2029年)

Magnetic Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1537605

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

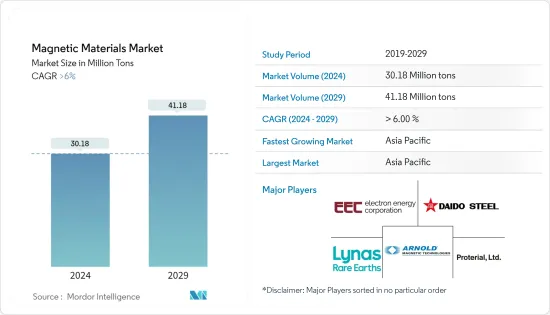

世界の磁性材料の市場規模は、2024年に3,018万トンに達し、2024~2029年にかけてCAGR 6%超で成長し、2029年には4,118万トンに達すると予測されています。

磁性材料市場は、COVID-19パンデミックの影響を受け、いくつかの国で全国的な封鎖措置がとられ、厳しい社会的距離を置く措置がとられたため、自動車や電子部品の生産が停止し、磁性材料市場に悪影響を及ぼしました。しかし、COVID-19パンデミック後は、ほとんどの工業生産施設と自動車メーカーが操業を再開し、磁性材料市場の復活につながった。近年、自動車、エレクトロニクス、発電産業からの需要増加により、市場は大きな成長率を記録しました。

発電産業における磁性材料の採用率の上昇と、電子機器エンドユーザー産業における使用量の増加が、現在の研究市場を牽引すると予想されます。

その反面、希土類材料の抽出コストが高いことが市場の成長を妨げると予想されます。

ハイブリッド電気自動車における磁性材料の需要の高まりは、予測期間中に市場に機会を創出すると予想されます。

アジア太平洋が市場を独占すると予想されます。また、自動車、エレクトロニクス、発電産業における磁性材料の需要の高まりにより、予測期間中に最も高いCAGRで推移することが予想されます。

磁性材料の市場動向

発電セクターからの需要増加

- 磁性材料は発電分野での使用が増加しています。これらの材料は、発電や送電のためのモーターに使用されています。磁性材料は、モーター、発電機、変圧器、アクチュエーターなどの機器に応用されています。

- 電気機械は硬質磁性材料でできており、磁束を供給するという一つの主要な機能のために使用されます。アード磁性材料は、電気回路からの減磁や高温下での熱減磁に耐える高い保磁力を持っています。

- エネルギー資源研究所によると、世界の発電能力は2021年の2万8,520テトラワット時に対し、2022年は2万9,165テトラワット時と2.26%の成長率で登録されています。このように、発電能力の増加が磁性材料市場を牽引すると予想されます。

- 米国は、発電能力に関して中国に次いで第2位を占めています。2022年には、米国の公益事業規模の発電施設で約4兆2,430億キロワット時(kWh)が発電されたました。この発電の約60%は、化石燃料である石炭、天然ガス、石油、その他のガスによるものです。

- さらに、風力発電所では磁性材料の需要が増加しています。中国は過去2年間に風力発電容量を増やしました。2022年、中国は風力発電所を増設し、欧州より46%多く風力発電を行った。IEAによると、中国の陸上風力発電は2022年に30.9GWを記録し、2023年末には59GWに達すると予想されています。

- このため、予測期間中は発電用途分野が磁性材料市場を独占すると予想されます。

市場を独占するアジア太平洋

- アジア太平洋は、中国とインドで発電セクターが高度に発展していることに加え、エレクトロニクスと自動車産業を発展させるための投資が長年にわたって継続されていることから、世界市場を独占すると予想されます。

- さらに、アジア太平洋における環境問題の高まりは、内燃エンジン車に対する政府の規制を強めています。このため、この地域では電気自動車のニーズが高まり、さまざまな用途での磁性材料の消費を支えています。

- 中国では、消費者のバッテリー駆動車への志向が高まっているため、自動車産業が転換傾向を示しています。さらに、中国政府は2025年までに電気自動車生産の普及率が20%になると予測しています。これは、2022年に過去最高を記録した同国の電気自動車販売動向に反映されています。

- 中国乗用車協会によると、2022年に同国で販売されたEVとプラグインは567万台で、2021年に達成した販売台数のほぼ2倍です。同国では潤滑油添加剤に対するニーズが減少することが予想されるため、同市場は現在のペースで販売を維持する構えです。

- 同様にインドでも、温室効果ガス排出量削減のため、電気自動車に焦点が移りつつあります。政府は、2023年までにインドの新車販売台数の30%を電気自動車にすると約束しています。さらに、電気自動車の生産台数を増やすため、さまざまな企業が国内に電気自動車製造施設を設立しています。

- 例えば、NissanとRenaultは2023年2月、乗用車と電気自動車の市場シェアを拡大するため、今後3~5年間でインドに6億米ドルを投資する計画を発表しました。これは電気自動車市場を押し上げ、磁性材料の需要を促進します。

- 上記の要因から、磁性材料の需要は予測期間中に同地域で増加する可能性が高いです。

磁性材料産業の概要

磁性材料市場は部分的に統合されています。市場の主要企業(順不同)には、Arnold Magnetic Technologies, Daido Steel, Electron Energy Corporation, PROTERIAL, Ltd., Lynas Rare Earths Ltd.などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 発電産業における磁性材料の採用増加

- エレクトロニクス分野での用途拡大

- その他の促進要因

- 抑制要因

- レアアースの採掘コストが高い

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模:数量ベース)

- タイプ

- 硬質磁性材料

- 軟磁性材料

- 半硬質磁性材料

- エンドユーザー産業

- 自動車

- エレクトロニクス

- 発電

- 産業用

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- 合併・買収、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Adams Magnetic Products

- Arnold Magnetic Technologies

- Daido Steel Co., Ltd.

- Dexter Magnetic Technologies

- Electron Energy Corporation

- GKN Powder Metallurgy

- Lynas Rare Earths Ltd.

- Molycorp Inc

- PROTERIAL, Ltd.

- Quadrant.

- Shin-Etsu Chemical Co., Ltd.

- Steward Advanced Materials LLC.

- TDK Corporation

- Tengam

- Toshiba Materials Co., Ltd.

第7章 市場機会と今後の動向

- ハイブリッド電気自動車における磁性材料需要の高まり

- その他の機会

目次

The Magnetic Materials Market size is estimated at 30.18 Million tons in 2024, and is expected to reach 41.18 Million tons by 2029, growing at a CAGR of greater than 6% during the forecast period (2024-2029).

The magnetic materials market was negatively affected by the COVID-19 pandemic due to nationwide lockdowns in several countries and strict social distancing measures, which resulted in production halts of automotive vehicles and electronic components, thereby affecting the market for magnetic materials. However, post-COVID-19 pandemic, most of the industrial manufacturing facilities and automotive manufacturers resumed their operations, which helped to revive the market for magnetic materials. In recent years, the market registered a significant growth rate due to increasing demand from the automotive, electronics, and power generation industries.

The rising adoption of magnetic materials in the power generation industry and the increasing usage in the electronics end-user industry are expected to drive the current studied market.

On the flip side, the high cost of extracting rare earth materials is expected to hinder the growth of the market.

The rising demand for magnetic materials in hybrid electric vehicles is expected to create opportunities for the market during the forecast period.

The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to the rising demand for magnetic materials in the automotive, electronics, and power generation industries.

Magnetic Materials Market Trends

Growing Demand from Power Generation Sector

- Magnetic Materials have been increasingly used in the power generation sector. These materials are used in motors to generate power and transmission of electricity. Magnetic materials are applied in equipment such as motors, generators, transformers, and actuators, amongst others.

- Electric machines are made of hard magnetic materials and are used for one primary function, which is to provide magnetic flux. Ard magnetic materials have high coercivity to resist demagnetization from the electric circuit and thermal demagnetization under high operating temperatures.

- According to the Energy and Resource Institute, the global electricity generation capacity is registered at 29,165 tetra watt-hours in the year 2022 at a growth rate of 2.26% as compared to 28,520 tetra watt-hours of electricity generated in the year 2021. Thus, the increasing electricity generation capacity is anticipated to drive the market for magnetic materials.

- The United States occupies second place after China regarding power generation capacity. In 2022, about 4,243 billion kilowatt hours (kWh) of electricity were generated at utility-scale electricity generation facilities in the United States.1 About 60% of this electricity generation was from fossil fuels-coal, natural gas, petroleum, and other gases.

- Furthermore, the demand for magnetic materials is increasing in wind power stations. China added more wind generation capacity in the past two years. In 2022, China generated 46% more wind power than Europe by installing more wind power stations. According to the IEA, the onshore wind electricity generation in China registered at 30.9 GW in 2022, and it is expected to reach 59 GW by the end of 2023.

- Thus, the power generation applications segment is anticipated to dominate the market for magnetic materials during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the global market owing to the highly developed power generation sector in China and India, coupled with continuous investments in the region to advance the electronics and automotive industry through the years.

- Moreover, the growing environmental issues in the Asia-Pacific region have increased government regulations on combustion engine vehicles. This has increased the need for electric cars in the area, supporting the consumption of magnetic materials in various applications.

- In China, the automotive industry is witnessing switching trends as the consumer inclination toward battery-operated vehicles is higher. Moreover, the government of China estimates a 20% penetration rate of electric vehicle production by 2025. This is reflected in the electric vehicle sales trend in the country, which went to a record-breaking high in 2022.

- As per the China Passenger Car Association, the country sold 5.67 million EVs and plug-ins in 2022, almost double the sales figures achieved in 2021. Anticipating a decline in the nation's need for lubricant additives, the market is poised to sustain sales at the current pace.

- Similarly, in India, the focus is shifting to electric vehicles to reduce greenhouse gas emissions. The government has committed that 30% of the new vehicle sales in India will be electric by 2023. Furthermore, various companies are establishing electric vehicle manufacturing facilities in the country to increase the production volume of electric vehicles.

- For instance, in February 2023, Nissan and Renault announced their plan to invest USD 600 million in India over the next 3-5 years to expand their market share in passenger cars and electric vehicles. It will boost the market for electric vehicles, thereby driving the demand for magnetic materials.

- Due to the factors above, the demand for magnetic materials will likely increase in the region during the forecast period.

Magnetic Materials Industry Overview

The magnetic materials market is partially consolidated in nature. Some of the major players in the market (not in any particular order) include Arnold Magnetic Technologies, Daido Steel Co., Ltd, Electron Energy Corporation, PROTERIAL, Ltd., and Lynas Rare Earths Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 The Rising Adaption of Magnetic Materials in Power Generation Industry

- 4.1.2 Increasing Applications in Electronics

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost in Extracting Rare Earth Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Hard Magnetic Materials

- 5.1.2 Soft Magnetic Materials

- 5.1.3 Semi-Hard Magnetic Materials

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Electronics

- 5.2.3 Power Generation

- 5.2.4 Industrial

- 5.2.5 Other End-user Industries (Consumer Goods, Communication and Technology, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Adams Magnetic Products

- 6.4.2 Arnold Magnetic Technologies

- 6.4.3 Daido Steel Co., Ltd.

- 6.4.4 Dexter Magnetic Technologies

- 6.4.5 Electron Energy Corporation

- 6.4.6 GKN Powder Metallurgy

- 6.4.7 Lynas Rare Earths Ltd.

- 6.4.8 Molycorp Inc

- 6.4.9 PROTERIAL, Ltd.

- 6.4.10 Quadrant.

- 6.4.11 Shin-Etsu Chemical Co., Ltd.

- 6.4.12 Steward Advanced Materials LLC.

- 6.4.13 TDK Corporation

- 6.4.14 Tengam

- 6.4.15 Toshiba Materials Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Demand for Magnetic Materials in Hybrid Electric Vehicles

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日