|

市場調査レポート

商品コード

1852112

ベースオイル:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Base Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ベースオイル:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年08月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

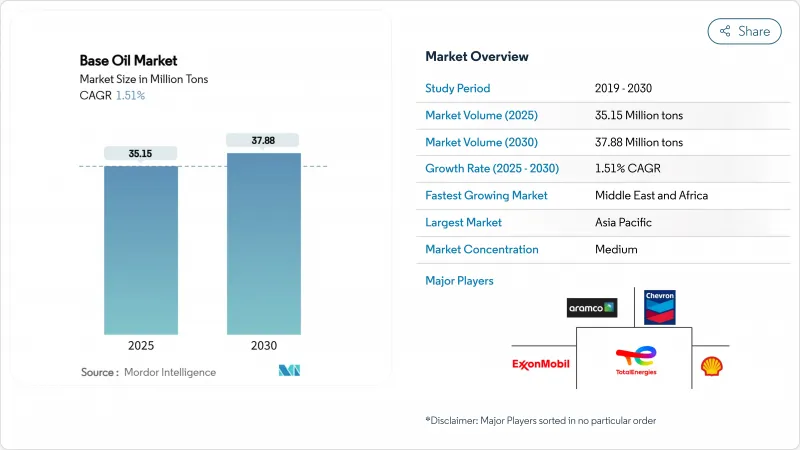

ベースオイル市場規模は2025年に3,515万トンと推定・予測され、予測期間(2025-2030年)のCAGRは1.51%で、2030年には3,788万トンに達すると予測されます。

ベースオイル市場の成長は、グループIから高性能のグループIIおよびIIIへの移行、世界的な排出規制の強化、電気自動車(EV)のドライブトレインにおける合成配合物の役割の拡大という3つの力によって支えられています。アジア太平洋地域が販売量をリードしているが、中東・アフリカ地域が最も急速に拡大しており、これはサプライチェーンが原油有利地域へと徐々に再編成されていることを示しています。石油精製業者は、ブレント・ドゥバイ間のスプレッド縮小と触媒アップグレードのための設備投資の増加によるマージン圧力に直面しています。データセンター向けの液浸冷却流体や、循環型経済目標に適合するクローズドループ再精製イニシアティブにビジネスチャンスが生まれます。

世界のベースオイル市場の動向と洞察

APACの生産クラスターにおける急速な工業化

アジア太平洋の製造業ブームは、ベースオイル市場の需要増の大きな部分を支えています。中国は2024年に日量1,480万バレルの原油を処理し、金属加工油剤と油圧作動油の堅調な需要を創出します。製油所と石油化学の統合コンプレックスのネットワークが拡大することで、操業の柔軟性が増し、生産者は最も収益性の高いベースストック・グレードに歩留まりをシフトできるようになります。PETRONASは、2025~2027年の見通しで日量200万バレルの石油換算生産量を見込んでおり、2028年のバイオリファイナリー・スタートアップに支えられた特殊化学品への川下プッシュがあります。これらの投資は、この地域のベースオイル市場における優位性を確固たるものにし、従来のグループiの生産能力の置き換えを加速させる。

ユーロ7と中国VIIの排ガス規制強化がグループIII/IVの需要を押し上げる

Euro 7基準の採用により、自動車メーカーはすべての小型ガソリンエンジンにパティキュレート・フィルター・システムの装着を義務付けられ、超低揮発性のグループIIIの需要が高まる。中国のChina VIIの並行枠組みは、低SAPS潤滑油への要求を強める一方、2022年から2026年にかけて承認された44の精製プロジェクトは、現地での供給を強化する態勢を整えています。2025年3月31日に発効するILSAC GF-7は、燃費を10%向上させることを要求しており、ブレンダーをより高品質の基油へと誘導している[ORONITE.COM]。そのため、水素化分解装置と水素化異性化装置が資本を集め、ベースオイル市場のプレミアム化が加速しています。

変動するブレントードバイ原油スプレッドがマージンを圧迫

2024年にはブレント・ドゥバイ間のスプレッドがマイナスに転じることがあり、これはVGOベースのベースオイル供給に不可欠なミディアムサワーバレルの不足を示唆しています。クウェート、オマーン、ナイジェリアの新しい製油所によって世界的な生産能力が向上したため、マージンが低下し、2025年初頭までに精製から撤退する事業者(ロンデルバセル・ヒューストンなど)も出てきました。ベースオイル市場の独立系企業は、操業の縮小や古い資産の閉鎖を迫られています。

セグメント分析

2024年のベースオイル市場シェアは、性能とコストのバランスのとれた方程式と確立された流通網により、グループIIが42.89%を占め、首位を維持した。シェルがヴェッセリングで30万トンの転換を行ったことは、水素化分解油に対する信頼の持続を裏付けています。グループIIIは、絶対ベースでは小さいもの、超低揮発性と高耐酸化性を求めるユーロ7とEV冷却義務に後押しされ、2030年までCAGR 4.22%で前進します。したがって、グループIIIの市場規模は、予測期間中、他のどのグレードよりも急速に拡大する見込みです。

iグループは、ゴム加工油や金属加工油など溶解性が要求される一部の分野で存続しているが、経済性の悪化に伴い閉鎖が続いています。グループVは、バイオ潤滑油用の二次ポリオールエステルを含む多様な化学物質で、技術革新の道を切り開きます。全体として、ベースオイル市場は、より厳しいOEM仕様と持続可能性の目標を満たすために、より高いAPIグループへと移行しています。

ベースオイルレポートは、ベースストックタイプ(グループi、グループII、グループIII、グループIV、その他)、用途(エンジンオイル、トランスミッション・ギアオイル、金属加工油、作動油、グリース、その他用途)、地域(アジア太平洋、北米、欧州、南米、中東・アフリカ)で区分されています。市場予測は数量(百万トン)で提供されます。

地域別分析

アジア太平洋は2024年の販売量の46.78%を占め、これは中国の記録的な日量1,480万バレルの原油生産と、2025年までに完了予定のインドの190~220億インドルピー規模の拡張計画に支えられています。ベースオイル市場は、燃料、化学品、ベースストックを利幅に応じて切り替えられる垂直統合型コンビナートの恩恵を受けています。日本と韓国はエレクトロニクスの熱管理用に精密合成技術を供給し、東南アジア諸国は地域の産業需要に対応するために生産能力を増強します。

中東・アフリカの2030年までのCAGRは3.48%で、世界最速です。ADNOCの35億米ドルのRuwais Crude Flexibility Projectは、より重いサワー原油の処理を可能にし、グループIIとIIIの生産量を最適化します。欧州は、2026年までにトタルエナジーズのグランプイッツをゼロ・クルード・プラットフォームに転換するなど、マージン圧縮と脱炭素化の軸に取り組んでいます。

北米はシェールオイルの経済性に支えられ、特殊PAOとグループIIIのプロジェクトに投資しています。シェブロンのパサデナのアップグレードは、ジェット燃料の柔軟性を高めると同時に、処理能力を日量12万5,000バレルまで引き上げます。南米はブラジルの石油化学統合により緩やかなアップサイドを享受しているが、マクロのボラティリティは大規模な投資を抑制しています。全体として、地理的なダイナミクスは、原油に有利で需要の豊富な地域への生産能力の漸進的な拡散を反映しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- APACの生産クラスターにおける急速な工業化

- ユーロ7と中国VIIの排ガス規制強化がグループIII/IVの需要を押し上げる

- EVの熱管理システムで高性能潤滑油の需要が高まる

- データセンター用液浸冷却液(新規合成ベースストック)の拡大

- サーキュラー・エコノミー義務化におけるクローズドループ再精製の経済性

- 市場抑制要因

- グループIの生産能力からの急速な代替

- ブレントとドバイの原油価格差の変動がマージンを圧迫

- EU(ECHA)におけるPAOのマイクロプラスチック分類の差し迫り

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- ベースストック別

- グループI

- グループII

- グループIII

- グループIV

- その他

- 用途別

- エンジンオイル

- トランスミッション・ギアオイル

- 金属加工油剤

- 作動油

- グリース

- その他の用途

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- マレーシア

- インドネシア

- ベトナム

- タイ

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- 南アフリカ

- ナイジェリア

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- ADNOC

- Chevron Corporation

- China Petrochemical Corporation(SINOPEC)

- CNOOC Limited

- Exxon Mobil Corporation

- Formosa Petrochemical Corporation

- Gazprom Neft PJSC

- GS Caltex Corporation

- Hindustan Petroleum Corporation Limited

- Indian Oil Corporation Ltd

- LUKOIL

- Nynas AB

- Petrobras

- PetroChina

- PETRONAS Lubricants International

- Philips 66 Company

- Repsol

- Saudi Arabian Oil Co.

- Sepahan Oil Company

- Shandong Qingyuan Group Co. Ltd.

- Shell plc

- SK Innovation Co. Ltd.

- TotalEnergies