|

市場調査レポート

商品コード

1536931

軍用フリゲート艦:市場シェア分析、産業動向と統計、成長予測(2024~2029年)Military Frigates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 軍用フリゲート艦:市場シェア分析、産業動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年08月14日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

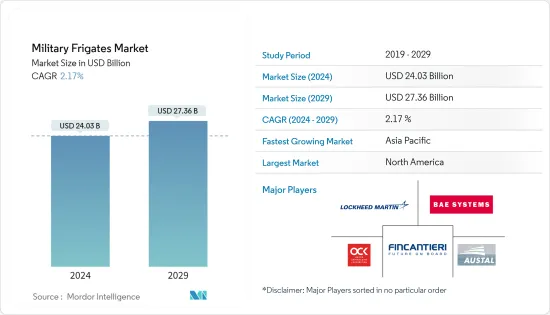

軍用フリゲート艦市場規模は2024年に240億3,000万米ドルと推定され、2029年には273億6,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは2.17%で成長する見込みです。

主なハイライト

- 海上での国境問題や領土紛争の増加により、新型フリゲート艦の開発・調達はここ数年で重要性を増しています。世界の地政学的緊張の高まりは、海軍力の戦略的重要性を浮き彫りにし、軍用フリゲート艦に対する需要の高まりを助長しています。各国は、重要な航路を確保し、領海を守り、進化する地政学的課題に効果的に対応するため、海洋能力を強化しようとしており、それがフリゲート艦の調達を後押ししています。

- 海洋安全保障の重視の高まりは、軍用フリゲート艦の需要を増幅させています。これらの艦船はパトロール活動の要として機能し、各国が自国の海岸線、排他的経済水域(EEZ)、海上国境を監視・保護することを可能にします。多様な海洋安全保障上の懸念に対応するフリゲート艦の多用途性は、安全な海洋環境の維持における極めて重要な役割を強化しています。老朽化した現在の戦闘艦船群を、対艦、対潜、防空能力を備えたフリゲート艦に装備された近代的な探知・兵器システムに置き換えるため、さまざまな国で進行中の更新プログラムが市場の成長を後押ししています。

- 軍事近代化イニシアチブの急増は、軍用フリゲート艦の市場を牽引する極めて重要な役割を果たしています。各国が防衛力のアップグレードを優先する中、フリゲート艦は包括的な海軍近代化プログラムの不可欠な構成要素として浮上しています。最新鋭フリゲート艦の導入は、より広範な軍事戦略に合致しており、市場の持続的需要に寄与しています。

軍用フリゲート艦市場の動向

哨戒フリゲート艦が軍用フリゲート艦市場で最大の市場シェアを占める見込み

- フリゲート艦はパトロール任務に優れており、海上国境の監視と安全確保、海賊対処作戦の実施、海上法の執行のための多目的プラットフォームを提供します。多様な作戦シナリオに適応できるフリゲート艦は、包括的な海上安全保障ソリューションを求める国々にとって不可欠な存在となっています。先進的なセンサーと監視システムを搭載したフリゲートは、その優れた監視能力で際立っています。この機能により、広大な海域を効果的に監視することが可能となり、潜在的な脅威を早期に発見し、積極的かつ戦略的なパトロールに貢献することができます。

- 哨戒カテゴリーは、海上でのテロ対策において最も重要な位置を占めています。フリゲートは、その迅速な対応能力により、潜在的な海洋の脅威を阻止し、無力化する上で重要な役割を果たし、海洋環境におけるテロ/海賊活動から身を守る上で不可欠な資産となっています。例えば、中華民国海軍は2023年5月、台湾海軍に12隻のフリゲート艦を導入する道を開くため、鍾欣造船集団に2隻の次世代国産軽フリゲート艦を発注しました。2,500トンの新型軽フリゲートは「二級艦」に分類され、台湾海軍の主力艦として日々の哨戒任務を担う。

アジア太平洋地域が予測期間中に最も高い成長を遂げる見込み

- 予測期間中、アジア太平洋地域が最も高い成長を遂げると予想されます。この地域の国家間の緊張の高まりは、各国が軍事費を増加させる要因となっています。そのため、予測期間中の市場成長を後押ししています。韓国、オーストラリア、インド、中国、インドネシアなどの国々は、この地域で新しいフリゲート艦の開発、建造、調達に投資しています。

- アジア太平洋の市場シェアが大きいのは、この地域の地政学的重要性に起因しています。南シナ海やその他の重要な水路における影響力をめぐる競合が激化するなか、アジア太平洋の国々は、海上での優位性を主張し、重要な権益を守るために、戦略的に先進的なフリゲート艦に投資しています。

- さらに、中国、インド、日本といった主要国の積極的な海軍近代化努力は、アジア太平洋における軍用フリゲート艦の需要急増に大きく寄与しています。これらの国々は、強力な海軍プレゼンスを維持することの必要性を認識しており、包括的な防衛戦略の一環として最新のフリゲート艦隊への投資に拍車をかけています。さらに、Austal、中国国家造船公司、現代重工業(HHI)のような造船会社の存在も、この地域におけるフリゲート艦の成長を支えています。例えば、2021年10月、ロシアはインド海軍のために国内で建造中の2隻のクリヴァク級またはタルワール級ステルスフリゲート「トゥシル」の最初の1隻を進水させました。このフリゲート艦は、インドがロシアと契約した4隻の後続フリゲート艦の一部であり、うち2隻はロシアが建造中、2隻は技術移転によりインドで建造中です。

- 同様に、2023年10月、インド国防省は、M/S Cochin Shipyard Limited(CSL)と、「INS Beas」のライフ・アップグレードとリパワリングの契約を、総費用3,760万米ドルで締結しました。INS Beasはブラフマプトラ級フリゲートで、蒸気推進からディーゼル推進に変更されます。INS Beasは、近代化された武器一式とアップグレードされた戦闘能力を備え、2026年にインド海軍の現役艦隊に加わる予定です。

軍用フリゲート艦産業の概要

軍用フリゲート艦市場は細分化されており、多くの企業が市場シェアを獲得しようと競い合っています。市場で著名な企業には、ロッキード・マーチン・コーポレーション、オースタル・リミテッド、ユナイテッド・シップビルディング・コーポレーション、フィンカンティエリS.p.A.、BAEシステムズplcなどがあります。各社が直面している主な問題は、地理的プレゼンスが限られていることです。例えば、BAE Systems plcは英国とオーストラリアのフリゲート艦プログラムをサポートし、Austal Limitedはオーストラリアと米国のフリゲート艦をサポートし、United Shipbuilding Corporationは主にロシアのプログラムをサポートしています。このように地理的プレゼンスが限られているため、市場は非常に断片化されており、多くの企業がシェアの一部を占めています。海軍のフリゲート艦開発プログラムをサポートするための企業間の協力やパートナーシップは、企業が市場で強力かつ主導的な地位を獲得するのに役立つ可能性があります。

例えば、米国海軍は2021年5月、コンステレーション・クラスの次期フリゲート艦の建造を開始するため、フィンカンティエリ・マリネット・マリーンに5億5,400万米ドルの契約を発行しました。この契約は、コンステレーション・クラスの2番目の船体であるUSSコングレス(FFG-63)に対するものです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途別

- パトロール

- 護衛

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- イタリア

- 英国

- スペイン

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 台湾

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- メキシコ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- トルコ

- エジプト

- サウジアラビア

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- BAE Systems plc

- Fincantieri S.p.A.

- Naval Group

- Damen Shipyards Group

- Fr. Lurssen Werft GmbH & Co. KG

- thyssenkrupp AG

- United Shipbuilding Corporation

- Rosoboronexport

- General Dynamics Corporation

- Lockheed Martin Corporation

- Austal Limited

- China Shipbuilding Industry Trading Co., Ltd.

第7章 市場機会と今後の動向

The Military Frigates Market size is estimated at USD 24.03 billion in 2024, and is expected to reach USD 27.36 billion by 2029, growing at a CAGR of 2.17% during the forecast period (2024-2029).

Key Highlights

- Development and procurement of new frigates have gained importance in the past few years due to the increasing border issues and territorial conflicts at sea. Escalating geopolitical tensions globally underscores the strategic importance of naval forces, fostering a heightened demand for military frigates. Nations seek to bolster their maritime capabilities to secure vital sea routes, protect territorial waters, and respond effectively to evolving geopolitical challenges, thereby driving the procurement of frigates.

- The increasing emphasis on maritime security amplifies the demand for military frigates. These vessels serve as linchpins in patrolling activities, enabling nations to monitor and safeguard their coastlines, Exclusive Economic Zones (EEZs), and maritime borders. The versatility of frigates in addressing diverse maritime security concerns reinforces their pivotal role in maintaining a secure maritime environment. The ongoing replacement programs in various countries to replace the current aging fleet of combat ships with modern detection and weapon systems equipped with frigates that have anti-ship, anti-submarine, and air-defense capabilities are propelling the growth of the market.

- The surge in military modernization initiatives plays a pivotal role in driving the market for military frigates. As nations prioritize upgrading their defense capabilities, frigates emerge as integral components of comprehensive naval modernization programs. The incorporation of state-of-the-art frigates aligns with broader military strategies, contributing to sustained demand in the market.

Military Frigates Market Trends

Patrol Frigates are Expected to Have the Largest Market Share of the Military Frigates Market

- Frigates excel in patrol duties, providing a versatile platform for monitoring and securing maritime borders, conducting anti-piracy operations, and enforcing maritime laws. Their adaptability in diverse operational scenarios makes them indispensable for nations seeking comprehensive maritime security solutions. Frigates, equipped with advanced sensors and surveillance systems, stand out for their superior surveillance capabilities. This feature enables effective monitoring of vast oceanic areas, allowing for early detection of potential threats and contributing to proactive and strategic patrolling.

- The patrol category holds paramount importance in counter-terrorism efforts at sea. Frigates, with their swift response capabilities, play a critical role in intercepting and neutralizing potential maritime threats, making them integral assets in safeguarding against terrorist/pirate activities in maritime environments. For instance, in May 2023, the Republic of China (ROC) Navy gave a contract to Jong Shyn Shipbuilding Group for two next-generation domestic Light Frigates paving the road to introduce 12 frigates for the Taiwanese Navy. The new 2,500-ton Light Frigates are classified as "Second class ships" and will act as the workhorses of the Taiwanese Navy, taking over the day-to-day patrol missions.

Asia-Pacific Expected to Witness Highest Growth During the Forecast Period

- The Asia-Pacific region is anticipated to have the highest growth during the forecast period. The escalated tensions between the countries in this region have led to countries increasing their military spending. Thus, this is boosting the growth of the market during the forecast period. Countries like South Korea, Australia, India, China, and Indonesia are investing in the development, building, and procurement of new frigates in this region.

- Asia-Pacific's substantial market share can be attributed to the geopolitical significance of the region. With increasing competition for influence in the South China Sea and other critical waterways, nations in the Asia-Pacific are strategically investing in advanced frigates to assert maritime dominance and protect vital interests.

- Moreover, the proactive naval modernization efforts of key countries like China, India, and Japan significantly contribute to the burgeoning demand for military frigates in Asia Pacific. These nations recognize the imperative of maintaining a robust naval presence, spurring investments in modern frigate fleets as part of comprehensive defense strategies. Additionally, the presence of shipbuilding companies, like Austal, China State Shipbuilding Corporation, and Hyundai Heavy Industries (HHI), is also supporting the growth of frigates in this region. For instance, in October 2021, Russia launched the first of two Krivak or Talwar-class stealth frigates, Tushil, being built in the country for the Indian Navy. The frigate is part of four follow-on frigates contracted by India from Russia, of which Russia is building two, and two are under construction in India through the transfer of technology.

- Similarly, in October 2023, the Indian Ministry of Defense signed a contract for the life Upgrade and Re-Powering of "INS Beas" with M/S Cochin Shipyard Limited (CSL) at an overall cost of USD 37.60 million. INS Beas is a Brahmaputra Class Frigate to be re-powered from Steam to Diesel Propulsion. INS Beas will join the active fleet of the Indian Navy with a modernized weapon suite and upgraded combat capability in 2026.

Military Frigates Industry Overview

The military frigates market is fragmented, with many companies competing to gain market share. Some of the prominent players in the market are Lockheed Martin Corporation, Austal Limited, United Shipbuilding Corporation, Fincantieri S.p.A., and BAE Systems plc. The major issue faced by the companies is limited geographical presence. For instance, BAE Systems plc supports the frigate programs of the United Kingdom and Australia, Austal Limited supports frigates in Australia and the United States, and United Shipbuilding Corporation majorly supports the programs of Russia. Due to such a limited geographical presence, the market is highly fragmented, with many companies taking a part of the share. The collaborations and partnerships between the players to support the frigate development programs of the naval forces may help the companies gain a strong and leading position in the market.

For instance, in May 2021, the US Navy issued a USD 554 million contract to Fincantieri Marinette Marine to start building the next frigate in the Constellation class. The award is for the future USS Congress (FFG-63), which is the second hull in the Constellation class.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Patrol

- 5.1.2 Escort

- 5.1.3 Other Applications

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Italy

- 5.2.2.2 United Kingdom

- 5.2.2.3 Spain

- 5.2.2.4 France

- 5.2.2.5 Germany

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Taiwan

- 5.2.3.3 India

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Mexico

- 5.2.4.2 Brazil

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Turkey

- 5.2.5.2 Egypt

- 5.2.5.3 Saudi Arabia

- 5.2.5.4 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 BAE Systems plc

- 6.2.2 Fincantieri S.p.A.

- 6.2.3 Naval Group

- 6.2.4 Damen Shipyards Group

- 6.2.5 Fr. Lurssen Werft GmbH & Co. KG

- 6.2.6 thyssenkrupp AG

- 6.2.7 United Shipbuilding Corporation

- 6.2.8 Rosoboronexport

- 6.2.9 General Dynamics Corporation

- 6.2.10 Lockheed Martin Corporation

- 6.2.11 Austal Limited

- 6.2.12 China Shipbuilding Industry Trading Co., Ltd.