|

市場調査レポート

商品コード

1939680

消化器系治療薬:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Gastrointestinal Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 消化器系治療薬:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

概要

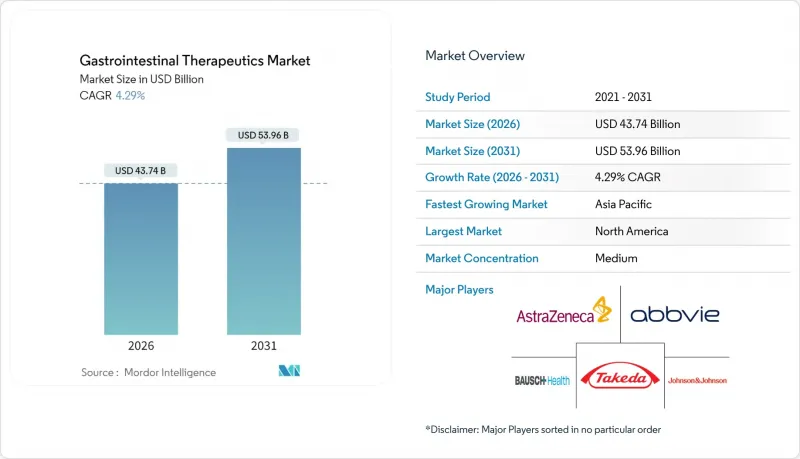

消化器系治療薬市場は、2025年の419億4,000万米ドルから2026年には437億4,000万米ドルへ成長し、2026年から2031年にかけてCAGR4.29%で推移し、2031年までに539億6,000万米ドルに達すると予測されています。

堅調な需要は、消化器疾患の負担増加、生物学的製剤およびバイオシミラーの採用拡大、ならびにマイクロバイオームに基づくパイプラインへの継続的な投資に起因しています。多くの国々、特に地方地域における専門医不足は、遠隔医療やAIガイド型診断ツールへの依存度を高めており、一方、バイオシミラーの代替可能性に対する規制面の支援は価格競争を加速させています。先進的な医薬品プラットフォームとデジタルヘルスサービスを組み合わせた企業は市場アクセスを強化し、大容量皮下投与システムは注射剤を従来の経口療法に代わる有力な選択肢として位置づけています。一方、ヘルスケアインフラの整備と食生活の西洋化に牽引されたアジア太平洋地域での拡大は、北米および欧州における価格圧力を相殺し、消化器系治療薬市場を多様なポートフォリオにとって魅力的な長期投資対象としています。

世界の消化器系治療薬市場の動向と洞察

消化器疾患の有病率増加

米国では大腸がん検診対象年齢が45歳に引き下げられ、年間数百万件の検査が増加し、診断法と治療薬の両方に対する需要が高まっています。急速な都市化が進むアジア地域における炎症性腸疾患の発生率上昇は、酸分泌抑制薬を上回る有効性を持つ先進的な生物学的製剤の必要性を浮き彫りにしています。中国とインドにおける全国的な検診プログラムの拡大により、より多くの患者が治療経路に流入し、早期発見が長期的な治療遵守率の向上につながっています。予防的大腸内視鏡検査に対する政府の償還制度は、抗痙攣薬や消化管運動促進剤の処方量をさらに押し上げています。これらの要因が相まって、治療対象患者の増加と治療期間の延長により、消化器治療薬市場を押し上げています。

高齢化と生活習慣の変化

日本では既に65歳以上の人口比率が29.1%に達しており、欧州や北米でも同様の傾向が見られます。これにより逆流症管理のためのプロトンポンプ阻害薬(PPI)の慢性使用が増加しています。座りがちな生活習慣や加工食品の摂取は機能性胃腸障害を悪化させ、消化管運動促進薬や腸内細菌叢調節薬の普及を促進しています。肥満は胃食道逆流症(GERD)の有病率を高め、後発医薬品による価格下落にもかかわらずPPIの持続的な処方需要を支えています。生活習慣に起因するストレスは過敏性腸症候群と関連し、低用量抗うつ薬の併用療法や抗痙攣薬の需要を後押ししています。全体として、人口動態と行動パターンの収束が治療期間を延長させ、消化器治療薬市場における安定した収益源を創出しています。

高コストな生物学的製剤治療

年間生物学的製剤治療費は5万米ドルを超える場合があり、公的・民間保険者双方に負担を強いるため、事前承認のハードルが次第に高まっています。価値に基づく契約では償還が実臨床成果に連動するため、メーカーは市販後調査への資金提供を迫られています。専門薬局は統合により大幅な割引交渉を実現し、粗利益率を低下させる一方、自己負担軽減プログラムを通じて患者へのアクセスを拡大しています。新興市場諸国の政府は単価引き下げのため共同調達を検討していますが、予算制約により低分子医薬品と比較して生物学的製剤の導入が遅れています。バイオシミラーが救済策となる可能性はあるもの、先発メーカーは高濃度製剤などのライフサイクル管理戦略で対抗することが多く、価格の硬直性を長引かせています。

セグメント分析

2025年においてもプロトンポンプ阻害薬(PPI)は収益の柱であり、胃食道逆流症の広範な管理や潰瘍予防を背景に、消化器治療薬市場の23.78%を占めました。急性出血時に速効性のある静注製剤が必要な病院処方箋では、ブランドPPIが依然として高価格を維持していますが、一般用医薬品は小売チャネルで主流となっています。PPIに起因する消化器治療薬市場規模は、長期的な有害作用を最小限に抑えるための段階的減量療法を推奨するガイドライン改訂により、頭打ちになると予想されます。一方、生物学的製剤セグメントは抗TNF剤、IL-12/23阻害剤、JAK阻害剤を通じて支出増加分を獲得していますが、2025年以降はバイオシミラーによる浸食に直面します。リファキシミンを筆頭とする抗生物質は、適応拡大の支援を受け、肝性脳症や小腸細菌過剰増殖症におけるニッチな用途を維持しています。

マイクロバイオーム療法は、ベースは低いもの4.33%のCAGRで最も成長が速い薬剤クラスであり、VOWST社の商業的牽引力や免疫不全患者向けSER-155などの有望なパイプラインの恩恵を受けています。生体治療製品の標準化とスケーラブルな嫌気性製造プロセスにより生産コストが削減され、従来型バイオ医薬品との価格差が縮小しています。ネスレ・ヘルスサイエンスが示すように、製薬と食品のクロスセクター連携により、定着率を高めるプレバイオティクス補助剤など、食事関連技術が導入されています。予測期間中、再発性クロストリジウム・ディフィシル感染症における再発率低下の実世界エビデンスが支払者側に受け入れられるにつれ、マイクロバイオーム製品の消化器系治療薬市場規模は拡大が見込まれます。

地域別分析

北米は2025年に世界収益の38.61%を占め、69.3%の郡で顕著な専門医不足があるにもかかわらず、高い生物学的製剤普及率と支援的な償還環境が牽引しました。遠隔消化器病学ネットワークとカプセル内視鏡診断センターがアクセスを拡大していますが、選択的大腸内視鏡検査の待機リストは依然として臨床医のキャパシティを圧迫しています。相互交換性規則の更新後、バイオシミラーの採用が加速し、支払者側の処方薬リストは迅速にコスト削減オプションを優先しています。

アジア太平洋地域はCAGR5.12%で最も急速に成長しており、中国とインドの高齢化人口が政府の保険制度拡大と相まって市場を牽引しています。都市部の食生活変化が潰瘍性大腸炎およびクローン病の発生率を押し上げ、シンガポールと韓国の生物学的製剤製造施設への投資を促進しています。一方、日本の超高齢社会ではPPI(プロトンポンプ阻害薬)と消化管運動促進薬の需要が安定して続きますが、厳格なHTA(医療技術評価)による価格抑制が価格上昇を抑制しています。デジタルヘルススタートアップはスマートフォンの普及を活用し、マイクロバイオーム追跡アプリを提供。病院のEMR(電子医療記録)システムとシームレスに連携し、個別化治療を導きます。

欧州はバランスの取れた見通しを維持しており、ドイツ、英国、フランスが合わせて地域売上の過半数を占めます。HTA機関による積極的な価格上限交渉がバイオシミラーの急速な普及を促し、患者アクセスを拡大する一方で利益率を圧迫しています。南欧諸国では、スカンジナビアのパイロットプログラムを模倣し、高コスト生物学的製剤に対する成果連動型支払いモデルの導入を検討中です。南米および中東・アフリカ地域では、ブラジルとサウジアラビアが内視鏡資本設備と生物学的製剤の導入を主導し、官民連携を活用して病院インフラの近代化を推進しています。しかしながら、支払者の分散化と輸入関税が普及を遅らせ、これらの地域は消化器治療薬市場の発展曲線において初期段階にとどまっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 消化器疾患の有病率増加

- 高齢化と生活習慣の変化

- 生物学的製剤およびバイオシミラーの進歩

- 低侵襲スマートカプセル技術の拡大

- マイクロバイオームに基づく生体治療薬パイプライン

- 希少消化器疾患に対するAIガイド型薬剤転用

- 市場抑制要因

- 生物学的製剤の高コスト

- 厳格な償還ハードル

- 2026年以降の特許切れによる価格下落圧力

- 新興国における専門医の不足

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 薬剤クラス別

- プロトンポンプ阻害薬(PPI)

- H2受容体拮抗薬

- 制酸剤・アルギン酸塩製剤

- 促動剤

- 下剤

- バルク形成

- 浸透圧

- 興奮剤

- 潤滑剤/皮膚軟化剤

- 制吐剤

- 5-HT3受容体拮抗薬

- NK1拮抗薬

- ドーパミン拮抗薬

- 抗痙攣薬

- 生物学的製剤およびバイオシミラー

- 抗TNF製剤

- 抗インテグリン剤

- IL-12/23阻害剤

- JAK阻害剤(低分子)

- S1Pモジュレーター

- 抗生物質(例:リファキシミン)

- GLP-2およびGLP-1アナログ

- マイクロバイオームに基づく治療法

- その他(胆汁酸吸着剤、酵素製剤)

- 疾患適応症別

- 胃食道逆流症(GERD)

- 消化性潰瘍疾患

- 機能性消化不良

- 過敏性腸症候群(IBS)

- 慢性特発性便秘(CIC)

- 潰瘍性大腸炎

- クローン病

- クロストリジオイデス・ディフィシル感染症

- 短腸症候群

- 消化器がん

- 消化管運動障害(例:胃不全麻痺)

- その他(好酸球性食道炎など)

- 投与経路別

- 経口

- 即効性

- 遅延性/腸溶性コーティング

- 徐放性製剤

- 注射剤

- 静脈内投与

- 皮下投与

- 直腸

- 坐薬

- フォーム剤/浣腸剤

- 静脈内輸液ポンプ

- その他(経皮吸収型、経鼻型)

- 経口

- 流通チャネル別

- 病院薬局

- 小売薬局

- オンライン薬局

- 専門クリニック/点滴センター

- その他(在宅医療環境)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- GCC

- 南アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- AbbVie Inc.

- Takeda Pharmaceutical Company Limited

- Johnson & Johnson(Janssen Biotech, Inc.)

- Pfizer Inc.

- AstraZeneca plc

- Eli Lilly and Company

- Bristol Myers Squibb Company

- Amgen Inc.

- GlaxoSmithKline plc

- Sanofi

- Novartis AG

- Ironwood Pharmaceuticals, Inc.

- Dr. Falk Pharma GmbH

- Ferring Pharmaceuticals SA

- Eisai Co., Ltd.

- Merck & Co., Inc.

- Bayer AG

- Boehringer Ingelheim International GmbH

- Gilead Sciences, Inc.

- Theravance Biopharma, Inc.