自動車用ギア:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

Automotive Gears - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

- 発行日

- ページ情報

- 英文 80 Pages

- 納期

- 2~3営業日

- 商品コード

- 1536883

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

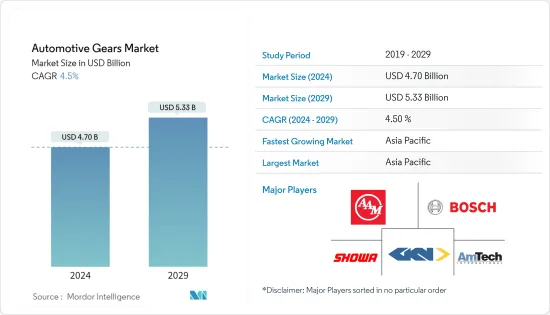

自動車用ギア市場規模は2024年に47億米ドルと推定・予測され、2029年には53億3,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは4.5%で成長します。

自動車用ギア市場は、2022年に46億7,000万米ドルと評価され、2027年には53億8,000万米ドルに達すると予測されています。自動車用ギア市場は予測期間中(2023-2028年)に5.5%以上のCAGRで推移すると予測されています。

COVID-19パンデミックは市場の成長を阻害しました。ロックダウンや旅行制限により、自動車の需要は減少しました。その結果、自動車産業における自動車部品の成長も過去2年間で低下しました。この動向は、自動車産業に関連するすべてのセグメントで見られました。

長期的には、自動車の生産台数は先進国でも新興諸国でも年々増加しています。これは自動車用ギア市場の成長につながります。自動車市場では、スムーズなギアシフトと加速の向上という点で、より強化された運転体験へのシフトが増加しています。

しかし、排ガス規制の高まりによる電気自動車の需要の増加など、さまざまな要因がギア市場の成長を抑制しています。電気自動車は最小限のギアしか使用しません。トランスミッションシステムが少なく、ディファレンシャルの使用も少なく、ギアボックスがほとんど不要なため、ギアの数は全体的に大幅に少なくなっています。

アジア太平洋地域は自動車生産が盛んであるため、自動車用ギア市場をリードする可能性が高く、次いで欧州と北米が続く。これらの地域の市場成長は、乗用車と小型商用車の需要と、今後数年間の車両効率の改善とカーボンフットプリントの削減を達成するための研究開発に対する既存のギアメーカーの継続的な投資によって支えられそうです。

自動車用ギヤ市場の動向

予測期間中、パラレルギアシャフトが市場を独占する見込み

パラレルシャフトギアモータは、パラレルシャフトギアボックスとも呼ばれ、入力軸と出力軸が平行でありながらオフセットしている設計が特徴です。

この設計により、同心ギアボックスよりも高いトルク容量と包括的なギア比の範囲が可能になり、より高いトルクと速度能力を必要とするアプリケーションに適しています。

平行軸ギアモーターとは、ギアボックス減速機の出力軸の位置のことです。モーターシャフトと減速機の出力シャフトが平行な平面上にある場合、"平行軸"と見なされます。この位置は、インライン位置決めと相まって、ギアモーターが限られたスペースで成功することを可能にします。コンパクトなサイズは、軽量化、低騒音化、低振動化、そして顧客満足につながります。

多くのエンジンシステムでは、コンポーネント間の動力伝達のために平行軸が使用されます。例えば、内燃機関では、一方のシャフトがクランクシャフトに接続され、ピストンからの動力を伝達します。一方、もう一方のシャフトはカムシャフトに接続され、バルブタイミングと動作を制御します。

平行軸は、エンジンのバランス調整に利用することができます。平行なシャフト上で2つの逆回転するマスを回転させることで、エンジンは動的バランスを達成し、振動を低減し、全体的な動作の滑らかさを向上させることができます。これは、ボクサーエンジンのような特定のエンジン構成で一般的に採用されています。

予測期間中、アジア太平洋地域が市場を独占する見込み

アジア太平洋地域は自動車用ギヤ市場を独占する可能性が高く、中国が市場の成長に大きく貢献しています。アジア太平洋は自動車用ギアの主要市場です。インドや中国などの国々で自動車生産台数が増加しており、メーカーが生産能力の増強に注力していることから、自動車用ギアの需要は大きく伸びると予想されます。例えば、複数のレポートによると、中国は、これらのIC自動車が依然として支配的なシェアを占めているため、今後数年間で年間8,000万台の内燃機関を販売すると予想されています。

さらに、低燃費車と軽量自動車部品へのニーズの高まりが、市場の成長を後押ししています。加えて、軽量で耐久性の高いアルミとコンポジットのギアは、推定・予測期間中により高い人気を獲得すると思われます。例えば、NORDはSK 920072.1 2段ヘリカルベベルギアモータ(NORDモータ搭載)を発売しました。高強度で軽量な設計が特徴です。

上記の要因とアジア太平洋の様々な国々の市場開拓は、予測期間中の市場の成長を高めると予想されます。

自動車用ギア業界の概要

自動車用ギア市場の主要メーカーには、American Axle &Manufacturing Holdings Inc.、AmTech International、Bharat Gears Ltd、GKN PLC、Robert Bosch GmbH、Gleason Plastic Gears、Showa Corporation、Universal Auto Gears LLPなどがあります。

- ジヤトコは2021年6月、環境性能と 促進要因ビリティを向上させた中・大型FF車用の新型無段変速機「CVT-X」を開発しました。CVTでは難しいとされていた伝達効率90%以上を達成したといいます。

- ゼット・エフ社は北米での商用車用トランスミッション製造に2億米ドルを投資すると発表しました。2023年、ZFはサウスカロライナ州グレイコートにある最新鋭の製造施設で、ZFパワーライン8速オートマチック・トランスミッションの生産を計画しました。2021年7月、ゼット・エフ社はミシガン州メアリスビルの施設において、2027年までピックアップトラック用のビームアクスルとアクスルドライブを納入する約60億米ドルのアクスル契約を獲得しました。

- 2019年3月、Dana IncorporatedはOerlikon GroupのDrive Systems部門の買収を完了したと発表しました。この買収により、小型商用車市場向けの高精度ヘリカルギアを中心に、ダナの技術ポートフォリオが拡大しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- ポジション別

- スキューシャフトギア

- ハイポイドギア

- ウォームギア

- 交差軸ギア

- ストレートベベルギア

- スパイラルベベルギア

- 平行軸ギア

- 平ギア

- ラック&ピニオンギヤ

- ヘリングボーンギヤ

- ヘリカルギア

- スキューシャフトギア

- 材料別

- 鉄

- 非鉄金属

- その他(複合材料・プラスチック)

- 用途別

- ステアリングシステム

- ディファレンシャルシステム

- トランスミッションシステム

- マニュアル

- オートマチック

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- American Axle & Manufacturing Holdings Inc.

- AmTech International

- Bharat Gears Ltd

- Cone Drive

- Dynamatic Technologies Limited

- Franz Morat Group

- GKN PLC

- Gleason Plastic Gears

- IMS Gear SE & Co. KGaA

- Robert Bosch GmbH

- RSB Global

- Showa Corporation

- Taiwan United Gear Co. Ltd

- Universal Auto Gears LLP

- ZF Friedrichshafen AG

第7章 市場機会と今後の動向

目次

The Automotive Gears Market size is estimated at USD 4.70 billion in 2024, and is expected to reach USD 5.33 billion by 2029, growing at a CAGR of 4.5% during the forecast period (2024-2029).

The automotive gears market was valued at USD 4.67 billion in 2022 and is expected to reach USD 5.38 billion by 2027. The automotive gears market is anticipated to register a CAGR of over 5.5% during the forecast period (2023-2028).

The COVID-19 pandemic disrupted market growth. With lockdowns and travel restrictions, the demand for vehicles had declined. As a result, the growth of automotive parts in the automotive industry also fell in the past two years. This trend was seen in all segments related to the automotive industry.

Over the long term, vehicle production has increased yearly in developed and developing countries. This will lead to growth in the automotive gear market. In the automotive market, a shift toward a more enhanced driving experience in terms of smooth gear shifting & improved acceleration has been increased.

However, various factors are restraining the growth of the gear market, such as the growing demand for electric vehicles due to rising emission regulations. Electric vehicles use minimal gear. The overall number of gears is significantly less due to fewer transmission systems, lesser use of differentials, and near elimination of gearboxes.

Asia-Pacific is likely to lead the automotive gears market, as the region is a significant vehicle producer, followed by Europe and North America. The market growth across these regions will likely be supported by demand for passenger cars and light commercial vehicles and continuous investments by established gear manufacturers in research and development to achieve improved vehicle efficiency and reduced carbon footprint in the coming years.

Automotive Gear Market Trends

Parallel Gear Shaft is Expected to Dominate the Market during Forecast Period

Parallel shaft gear motors, also called parallel shaft gearboxes, feature a design in which the input and output shafts are parallel but offset.

This design allows for higher torque capacity and a more comprehensive range of gear ratios than concentric gearboxes, making them suitable for applications that require higher torque and speed capabilities.

A parallel shaft gear motor refers to the position where the gearbox reducer's output shaft sits. If the motor shaft and the speed reducer output shaft are on parallel planes, it is considered a "parallel shaft." This position, coupled with the inline positioning, enables the gear motor to succeed in limited-space areas. Compact size leads to less weight, less sound, less vibration, and a happy customer experience.

In many engine systems, parallel shafts are used for power transmission between components. For example, in an internal combustion engine, one shaft may be connected to the crankshaft to transmit power from the pistons. In contrast, the other shaft may be connected to the camshaft to control valve timing and operation.

Parallel shafts can be utilized for balancing purposes in engines. By rotating two counter-rotating masses on parallel shafts, the engine can achieve dynamic balance, reducing vibrations and improving the overall smoothness of operation. This is commonly employed in specific engine configurations, such as boxer engines.

Asia-Pacific is Expected to Dominate the Market During the Forecast Period

Asia-Pacific is likely to dominate the automotive gears market, with China being a key contributor to the market's growth. Asia-Pacific is the leading market for automotive gear. With the increasing vehicle production in countries such as India and China and the manufacturers' focus on increasing production capacity, the demand for automotive gear is anticipated to grow significantly. For instance, according to several reports, China is expected to sell 80 million internal combustion engines annually in the coming years as these IC vehicles are still occupying the dominant share.

Additionally, the increasing need for fuel-efficient vehicles and lightweight automotive parts drive the market's growth. In addition, lightweight and highly durable aluminum and composite gears are estimated to gain higher popularity during the forecast period. For instance, NORD launched the SK 920072.1 two-stage helical bevel gear motor (mounted with a NORD motor), a drive solution for a wide range of light-duty conveying, processing, and manufacturing applications. It is identified by its high-strength and lightweight design.

The factors above and developments across various countries in Asia-Pacific are expected to enhance the market's growth during the forecast period.

Automotive Gears Industry Overview

Some of the major manufacturers in the automotive gear market include American Axle & Manufacturing Holdings Inc., AmTech International, Bharat Gears Ltd, GKN PLC, Robert Bosch GmbH, Gleason Plastic Gears, Showa Corporation, and Universal Auto Gears LLP.

- In June 2021, JATCO developed a new continuously variable transmission, "CVT-X," for medium and large FWD vehicles with improved environmental performance and drivability. It is said to have achieved more than 90% transmission efficiency, which was considered difficult for a CVT.

- ZF announced investing USD 200 million in commercial vehicle transmission manufacturing in North America. In 2023, ZF planned to produce the ZF Powerline 8-speed automatic transmission at the company's state-of-the-art manufacturing facility in Gray Court, SC. In July 2021, ZF secured a nearly USD 6 billion axle contract for the Marysville, Michigan, facility to deliver beam axles and axle drives for pick-up trucks until 2027.

- In March 2019, Dana Incorporated announced that it completed the acquisition of the Drive Systems segment of the Oerlikon Group. This acquisition has expanded Dana's technology portfolio, especially in high-precision helical gears for the light- and commercial-vehicle markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD billion)

- 5.1 By Position

- 5.1.1 Skew Shaft Gears

- 5.1.1.1 Hypoid Gears

- 5.1.1.2 Worm Gears

- 5.1.2 Intersecting Shaft Gears

- 5.1.2.1 Straight Bevel Gears

- 5.1.2.2 Spiral Bevel Gears

- 5.1.3 Parallel Shaft Gears

- 5.1.3.1 Spur Gears

- 5.1.3.2 Rack and Pinion Gears

- 5.1.3.3 Herringbone Gears

- 5.1.3.4 Helical Gears

- 5.1.1 Skew Shaft Gears

- 5.2 By Material

- 5.2.1 Ferrous Metals

- 5.2.2 Non-ferrous Metals

- 5.2.3 Other Materials (Composites and Plastics)

- 5.3 By Application

- 5.3.1 Steering Systems

- 5.3.2 Differential Systems

- 5.3.3 Transmission Systems

- 5.3.3.1 Manual

- 5.3.3.2 Automatic

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Mexico

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 American Axle & Manufacturing Holdings Inc.

- 6.2.2 AmTech International

- 6.2.3 Bharat Gears Ltd

- 6.2.4 Cone Drive

- 6.2.5 Dynamatic Technologies Limited

- 6.2.6 Franz Morat Group

- 6.2.7 GKN PLC

- 6.2.8 Gleason Plastic Gears

- 6.2.9 IMS Gear SE & Co. KGaA

- 6.2.10 Robert Bosch GmbH

- 6.2.11 RSB Global

- 6.2.12 Showa Corporation

- 6.2.13 Taiwan United Gear Co. Ltd

- 6.2.14 Universal Auto Gears LLP

- 6.2.15 ZF Friedrichshafen AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 80 Pages

- 納期

- 2~3営業日