|

市場調査レポート

商品コード

1851447

自動車用スイッチ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Automotive Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用スイッチ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月07日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

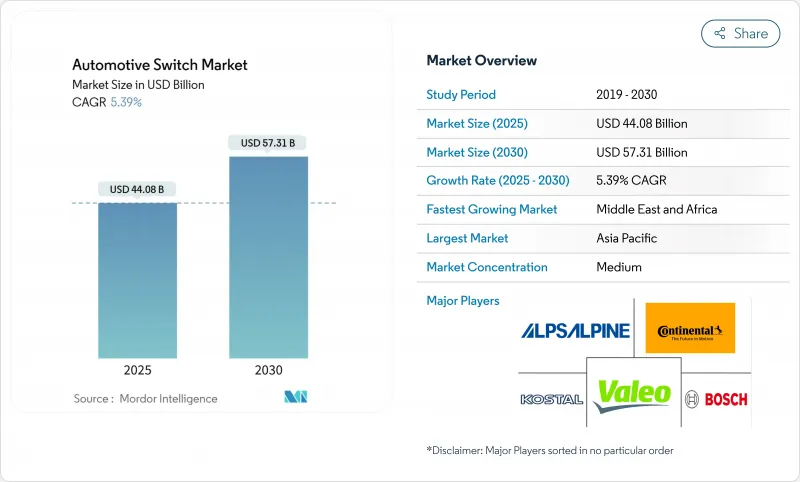

自動車用スイッチ市場規模は2025年に440億8,000万米ドル、2030年には573億1,000万米ドルに達し、CAGR 5.39%で成長すると予測されています。

この成長は、機械的な感覚と電子的なインテリジェンスをつなぐ最前線のヒューマン・マシン・インターフェースとしてスイッチが機能する、ソフトウェア定義の自動車への幅広い移行を反映しています。バッテリー電気自動車は、燃焼式に比べ、銅と高電圧回路をはるかに多く必要とするためです。インフォテインメントやADASの内容の充実、豪華なイルミネーション・キャビンの推進、ISO 26262の安全規則の厳格化、これらすべてが、すべてのスイッチに求められる機能的な期待を高めています。競争企業間の敵対関係は、触覚技術や静電容量技術が機械的な現状に課題するにつれて激化し、銅やレアアースをめぐるサプライチェーン・ショックは、メーカーに調達、コストヘッジ、生産地域のフットプリントの再考を迫る。

世界の自動車用スイッチ市場の動向と洞察

自動車の電動化の台頭

バッテリー管理、回生ブレーキ、熱最適化など、電動パワートレインには独自の制御ニーズがあり、触覚的な反応を維持しながら高電圧に耐える専用スイッチが必要です。パナソニック・オートモーティブの集中型ECUアーキテクチャは、燃焼ハードウェアを取り除くと、エレクトロニクスの内容がどのように膨れ上がるかを示しています。ブラジルのプラグイン販売台数は2024年に90%増の17万7,360台に急増し、需要パターンの変化がいかに速いかが明らかになりました。2026年までに100%国産チップを使用した自動車を発売するという中国の計画は、部品調達経路をさらに再構築すると思われます。これらの力は、数量とスイッチ機能の多様性の両方を拡大することにより、自動車用スイッチ市場を押し上げます。

先進インフォテインメントとADAS機能の成長

クアルコムのSnapdragonプラットフォームで構築されたクラウドリンクコックピットには、車外センサー、音声アシスタント、無線アップデートバックエンドと通信できる多機能コントローラが必要です。コンチネンタルのプログラマブル・ハプティック・ノブは、1つのダイヤルでさまざまなディテントを模倣できるため、次世代ダッシュボードのスペースとスタイリングの目標を満たすことができます。セーフティクリティカルなADASレイヤーは、ISO 26262の認証を受けたスイッチを要求し、レーンキープなどの機能の冗長作動を保証します。後付けADASアフターマーケットは10億米ドルに近づいており、新しい安全機能を求める古い車の間で対応可能な需要を拡大しています。

銅とレアアースの価格変動

銅価格は2024年2月以降20%近く上昇し、2025年には1トン当たり1万5,000米ドルを超えようとしており、高純度接点を使用するすべての機械式スイッチの材料費を押し上げています。中国のレアアース輸出の並行規制により、スズキやフォードなどのOEMはすでに短期間の生産休止を余儀なくされています。スイッチメーカーは、自動車用スイッチ市場のマージンを守るために、材料コストをヘッジし、接点レイアウトを再設計し、低質量合金を評価しています。

セグメント分析

メカニカルデザインは2024年の売上高の93.82%を維持し、極端な温度、埃、振動に対する信頼性が証明されました。ボタンは高頻度のユーザータスクを処理し、ロッカーユニットはバイナリ機能を制御し、パドルはステアリングに取り付けられたコマンドを管理します。機械式スイッチの自動車用スイッチ市場規模は、ディスプレイが成長しても着実に拡大すると予測されます。

タッチ式スイッチの市場規模は、現在わずかであるが、高級車やマスプレミアムのトリムがフラッシュライト式パネルに移行するにつれて、2030年までのCAGRは8.17%となります。コンチネンタルの静電フィードバックノブはギアなしで機械的なディテントを再現し、スナップトロンのはんだ付け可能な触覚ドームは年間生産能力を2倍にすることができます。ハイブリッドモジュールは、薄いプラスチックキャップの下に静電容量式センシングをバンドルしながらもクリック感を発生させ、OEMにスタイリングの自由を与えながら、自動車用スイッチ市場で期待されるレガシー感を維持します。

インジケータ・コントロールは2024年の売上高の25.11%を占めたが、これはすべての司法管轄区で、ターン、ハザード、警告機能のための強固な信号伝達が義務付けられているためです。インジケータアプリケーションの自動車用スイッチ市場規模は、完全デジタル化されたコックピットにおいても、スクリーンが故障した際に外部照明コマンドが機能する必要があるため、引き続き安全です。

HVACインターフェースは、電気自動車のレンジセンシティブサーマルロジックのおかげで、CAGR最速の5.57%を獲得しています。東海理化のインモールド塗装プロセスは、すでにトヨタのハイエースに採用されており、製造時のエネルギー使用量を削減すると同時に、傷のつきにくい外観を実現します。気候制御はタッチスクリーンに完全に消えることはなく、ユーザーは脱湿や霜取りのためにすぐに触覚でアクセスする必要があり、自動車用スイッチ市場全体の需要を支えています。

地域分析

アジア太平洋地域が自動車用スイッチ市場の先陣を切っており、2024年の売上高は49.88%で、現在最大の市場となっています。中国、日本、韓国、インドに強固な供給クラスターが形成され、さらにEVに対するインセンティブが充実しているため、グローバルOEMが現地生産を拡大する中、この地域は常に先頭を走っています。タイ初の電動ピックアップ・プログラムとインドネシアのニッケル豊富なバッテリー回廊は、APACのリーダーシップを強化しています。

中東・アフリカは、規模は小さいもの、2030年までのCAGRは最速の7.58%を記録します。サウジアラビアでは、セアの13億米ドルのEV複合施設を含む29億米ドルの自動車プロジェクト・パイプラインと、2025年までに計画されている5万基の公共充電器が、湾岸経済全体のスイッチ需要を加速させています。2030年までに4万2,000台のEVを導入するというドバイの目標は、成長ギャップをさらに広げています。

北米と欧州は、プレミアム・ネームプレートを高コンテンツのADASやインフォテインメント・システムと組み合わせることで、強力なポジションを維持しています。南米は、ブラジルの300億レアル(60億米ドル)のStellantisプログラムが地域の製造を確保することで、着実な地歩を固めています。最終組立拠点に近い場所で生産が可能なサプライヤーは、進化する貿易とコンプライアンスの圧力に対応できる最良の立場にあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 自動車の電動化の進展

- 先進インフォテインメントとADAS機能の成長

- 新興国における自動車生産台数の増加

- 照光式スイッチと静電容量式スイッチのプレミアムインテリア需要

- ハプティック/フォースタッチスイッチ技術の採用

- 機能安全(ISO 26262)冗長スイッチ設計の必要性

- 市場抑制要因

- 銅とレアアース投入価格の変動

- ディスプレイベースのタッチインターフェースへのシフト

- 触覚ドーム用サブコンポーネントの供給ボトルネック

- EMC規制強化で検証コストが上昇

- バリューチェーン分析

- テクノロジーの展望

- 規制情勢

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- スイッチタイプ別

- メカニカルスイッチ

- ノブ

- ボタン

- ロッカー

- トグル/パドル

- タッチ式スイッチ

- 静電容量式タッチパッド

- 触覚フィードバック

- 多機能/コンビネーションモジュール

- メカニカルスイッチ

- 用途別

- インジケータシステムスイッチ

- HVACコントロール

- パワーウインドー・ドアロックスイッチ

- ステアリングホイールコントロールスイッチ

- シートおよびインテリアコンフォートスイッチ

- 照明およびワイパースイッチ

- エンジン管理(EMS)スイッチ

- 車両タイプ別

- 乗用車

- 小型商用車

- 中・大型商用車

- 販売チャネル別

- OEM

- アフターマーケット

- 地域別

- 北米

- 米国

- カナダ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- トルコ

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Alps Alpine Co. Ltd

- Robert Bosch GmbH

- Continental AG

- HELLA GmbH & Co KGaA

- Omron Corporation

- Panasonic Holdings Corp

- Tokai Rika Co. Ltd

- Minda Corporation Ltd

- ZF Friedrichshafen AG

- Leopold Kostal GmbH & Co. KG

- Valeo SA

- Toyodenso Co Ltd

- TE Connectivity Ltd

- LS Automotive

- Denso Corporation

- Nidec Mobility

- Joyson Electronics