|

市場調査レポート

商品コード

1523396

航空救急サービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Air Ambulance Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空救急サービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

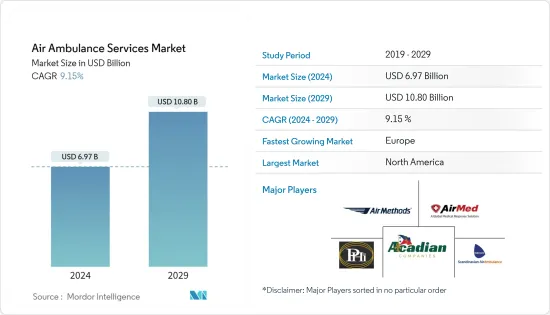

航空救急サービス市場規模は2024年に69億7,000万米ドルと推定され、2029年には108億米ドルに達し、予測期間中(2024~2029年)にCAGR 9.15%で成長すると予測されています。

救急機は現在、健康問題に苦しむ患者の搬送にますます利用されるようになっています。事故や、心臓発作、脳卒中、その他の医療緊急事態などの脅威の増加が、航空救急サービスの需要を生み出しています。政府とヘリコプター救急医療サービス(HEMS)プロバイダーとのパートナーシップの増加が、市場の成長を後押ししています。航空救急サービスの技術的進歩も進んでいます。例えば、救急ヘリには必要な医療機器や付属品が装備されており、患者に初期救急医療を提供する訓練を受けた熟練した医療クルーもいます。

さらに、救急機は従来の路上救急サービスよりも優れており、移動時間の長さや遠隔地へのアクセスの制限といった問題を軽減することができます。高度な人工呼吸器システムや心臓監視システムなどの新技術により、患者が安全に最寄りの病院に搬送されるまで生存できる可能性が高まります。さらに、通信システムの面でも先進技術は、患者のリアルタイムのデータを病院に転送し、医師が患者を救うために必要な措置を認識できるようにします。

しかし、運用上の制約、高コスト、航空事故発生などの要因が、このセグメントの成長を抑制すると予測されています。このような要因にもかかわらず、より良い救急医療を提供し、より収益性の高いリターンを生み出すために、救急機の資産を最大限に活用する必要性は、予測期間中にセグメントの収益を促進すると予測されています。

航空救急サービス市場の動向

予測期間中、回転翼航空機セグメントが市場を独占

航空救急サービス市場は、生存率の向上、迅速で快適な搬送、短時間で広大な範囲をカバーできるなど、いくつかの利点があるため増加傾向にあります。こうした利点から、回転翼ヘリコプターは救急医療搬送の有力な選択肢となっています。例えば、2019年から2023年の間に、世界全体で合計268機のヘリコプターが様々な救急・医療サービスを実施するために運用されていました。航空救急サービスを実施するためのヘリコプターは、相手先ブランド製造業者(OEM)によって軽量化されています。こうしたヘリコプターの設計に炭素繊維を導入することで、機体が軽量化され、緊急時の迅速な着陸・離陸が可能になるなど、多くのメリットがもたらされています。また、ヘリコプターのモデルに炭素繊維構造を採用したことで、ヘリコプターの寿命が延び、長年にわたって使用できるようになった。また、飛行輸送中に発生する損傷に対する耐久性も向上しています。このような進歩により、さまざまな国や軍隊、その他の航空救急サービスを提供する企業は、航空救急サービスを提供するために、新型で先進的なヘリコプターを調達する必要に迫られています。

例えば、2023年11月、ノルウェー航空救急隊は、デンマークでヘリコプターによる救急医療サービスを実施するため、3機のH135と2機の5枚羽根のH145を納入する契約をエアバスに発注しました。同様に2023年12月、ガマ・アビエーションはウェールズ航空救急チャリティーのためにヘリコプター救急医療サービス(HEMS)を開始しました。7,000万米ドルの契約により、エアバスH145ヘリコプター4機が運航・整備され、その拠点は同慈善団体の既存施設となります。このように、相手先ブランド製造業者(OEM)によるこのような技術的進歩により、ロータークラフト分野は予測期間中に目覚ましい成長を見せると思われます。

予測期間中、北米が最大の市場シェアを占める

現在、北米が航空救急サービス市場で最も高いシェアを占めています。この優位性は、多数の航空救急サービスプロバイダーが存在し、ヘルスケア分野での支出が増加していることによる。例えば、2023年8月、航空医療サービス協会は、米国では毎年55万人以上の患者が航空救急サービスを利用していると発表しました。Air Methods Corporation、Acadian Companies、PHI Inc.などの主要プレイヤーの存在が、地域全体の市場成長を後押ししています。例えば、2024年1月に米国心臓協会が発表したところによると、米国では毎年、約60万5,000件の心臓発作が新たに発生し、20万件の発作が再発します。また、過去10年間で、高血圧による年齢調整死亡率は65.6%増加し、実際の死亡者数は91.2%増加しました。高血圧は心臓病や脳卒中の主要な危険因子です。このような要因により、全国的に航空救急サービスの需要が高まっています。したがって、さまざまな航空救急サービスプロバイダーが、緊急航空救急サービスを提供するために、より新しいモデルのヘリコプターを調達しています。

航空救急サービス産業の概要

航空救急サービス市場は細分化されており、さまざまな種類の救急医療サービスを提供する複数の事業者によって特徴づけられています。著名な市場参入企業には、Air Methods Corporation、Acadian Companies、PHI Group, Inc、Babcock International Group、Global Medical Response, Incなどがあります。ヘリコプターに高度な医療機器が搭載され、救急治療や搬送が可能になったことで、市場の成長はさらに加速すると予想されます。また、炭素繊維などの複合材料を使用することで、救急機の寿命を延ばし、強い衝撃を受けた際の保護性能を高めるなど、救急機の設計にさまざまな進歩が見られ、救急機で搬送される患者をさらに保護する可能性があり、これが予測期間中の市場の成長につながると考えられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- サービス事業者

- 病院系

- 独立系

- 政府系

- 航空機タイプ

- 固定翼

- 回転翼

- サービスタイプ

- 国内線

- 国際線

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- エジプト

- イスラエル

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Air Methods Corporation

- AirMed International(Global Medical Response, Inc.)

- Acadian Companies

- PHI Group, Inc.

- REVA Inc.

- European Air Ambulance

- Babcock Scandinavian Air Ambulance(Babcock International Group)

- Air Charter Services Group

- Gulf Helicopters

- CareFlight

第7章 市場機会と今後の動向

The Air Ambulance Services Market size is estimated at USD 6.97 billion in 2024, and is expected to reach USD 10.80 billion by 2029, growing at a CAGR of 9.15% during the forecast period (2024-2029).

Air ambulances are now being increasingly used for the transportation of patients suffering from health issues. An increase in the number of accidents and other threats such as heart attacks, strokes, and other medical emergencies creates demand for air ambulance services. Increasing partnerships between governments and helicopter emergency medical services (HEMS) providers boost the market's growth. There have been increasing advancements in terms of technology for air ambulance services. For instance, air ambulance helicopters are equipped with the required medical equipment and accessories, along with skilled medical crew trained in providing initial emergency medical care to patients.

In addition, air ambulance provides advantages over conventional road ambulance services, as the former helps mitigate the issue of prolonged travel durations and limited access to remote areas. New technologies such as advanced ventilator systems and heart monitoring systems increase the chances of patients' survival until they are safely transported to the nearest hospital. Additionally, advanced technology in terms of communication systems leads to the transfer of real-time data of patients to the hospitals so that the doctors are aware of the necessary steps to be taken to save the patient.

However, factors like operational constraints, high costs, and air ambulance accident incidences are projected to restrain the growth of the segment. Despite this factor, the need for maximizing the use of air ambulance assets to offer better emergency care and the generation of more profitable returns is anticipated to propel the revenues of the segment during the forecast period.

Air Ambulance Services Market Trends

The Rotary-Wing Aircraft Segment Dominates the Market During the Forecast Period

The market for air ambulance services is on the rise owing to several benefits, such as increased survival rates, swift and comfortable transportation, and a vast coverage range in a shorter time. These advantages make rotary-wing helicopters a compelling choice for emergency medical transportation. For instance, during 2019-2023, a total of 268 helicopters were in operation performing various emergency and medical services globally. Helicopters for carrying out air ambulance services have been made lightweight by original equipment manufacturers (OEMs). The introduction of carbon fiber while designing such helicopters has provided many benefits by making the craft lighter in weight and thus adding the benefit of quick landings and take-offs during emergencies. Making use of a carbon fiber structure for the helicopter model has also led to increasing the life of the helicopter so that it can be used in service for many years. It has also made the helicopters more durable towards damages occurring during flight transportation. Such advancements are compelling various countries, militaries, and other air ambulance service-providing companies to procure new and advanced helicopters to provide air ambulance services.

For instance, in November 2023, the Norwegian Air Ambulance awarded a contract to Airbus to deliver three H135s and two five-bladed H145s to carry out helicopter emergency medical service missions in Denmark. Similarly, in December 2023, Gama Aviation launched its Helicopter Emergency Medical Services (HEMS) for the Wales Air Ambulance Charity. Under a USD 70 million contract, a fleet of four Airbus H145 helicopters will be operated and maintained, with their base of operations being the charity's existing sites. Thus, such technological advancements being made by the original equipment manufacturers or OEMs will lead to the rotor-craft segment showing impressive growth during the forecast period.

North America to Exhibit the Largest Market Share During the Forecast Period

Currently, North America holds the highest shares in the air ambulance market. The dominance is due to the presence of a large number of air ambulance service providers and rising spending in the healthcare sector. For instance, in August 2023, the Association of Air Medical Services published that more than 550,000 patients in the U.S. use air ambulance services every year. The presence of key players such as Air Methods Corporation, Acadian Companies, PHI Inc., and others drives the growth of the market across the region. In addition, the demand for air ambulance services in the region is driven by the presence of the U.S. For instance, in January 2024, the American Heart Association published that every year, there are about 605,000 new heart attacks and 200,000 recurrent attacks in the U.S. And the past 10 years, the age-adjusted death rate from high blood pressure increased by 65.6%, and the actual number of deaths rose by 91.2%. High blood pressure is a leading risk factor for heart disease and stroke. Such factors are driving the demand for air ambulance services across the country. Hence, various air ambulance service providers are procuring newer helicopter models to provide emergency air ambulance services.

For instance, in February 2023, Bell Textron Inc. was awarded a contract by Global Medical Response (GMR) to deliver three additional Bell 407GXi aircraft. The delivery happened at the end of 2023, and the three Bell 407GXis have joined GMR's exclusive 220 Bell helicopter fleet used for emergency medical operations throughout North America. Similarly, in May 2023, Ascent Helicopters, a Canadian company based in Parksville, was awarded a contract by the provincial government to provide the B.C. Emergency Health Services (BCEHS) with six new air ambulances for USD 544.4 million. By 2025, six new air ambulances are expected to be added to the fleet for B.C. Emergency Health Services. Growing investments by various original equipment manufacturers as well as companies in the North American region to better develop air ambulance services at times of medical requirements are expected to fuel the market growth in the region.

Air Ambulance Services Industry Overview

The market of air ambulance services is fragmented in nature and is characterized by several operators who provide various types of emergency medical services. Some of the prominent market players include Air Methods Corporation, Acadian Companies, PHI Group, Inc., Babcock Scandinavian Air Ambulance (Babcock International Group), and AirMed International (Global Medical Response, Inc.). The market growth is anticipated to receive a boost with the incorporation of sophisticated medical equipment in helicopters that enable emergency treatment and transportation. In addition, various advances to the design of air ambulances by making use of composite materials such as carbon fiber to increase the life of the air ambulance in service, as well as offer better protection during heavy impact, may provide additional protection to the patient being transported by the air ambulance and this is likely to lead to the growth of the market during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Service Operator

- 5.1.1 Hospital-based

- 5.1.2 Independent

- 5.1.3 Government

- 5.2 Aircraft Type

- 5.2.1 Fixed-Wing

- 5.2.2 Rotary-Wing

- 5.3 Service Type

- 5.3.1 Domestic

- 5.3.2 International

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Mexico

- 5.4.4.3 Rest of Latin America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Egypt

- 5.4.5.3 Israel

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Air Methods Corporation

- 6.2.2 AirMed International (Global Medical Response, Inc.)

- 6.2.3 Acadian Companies

- 6.2.4 PHI Group, Inc.

- 6.2.5 REVA Inc.

- 6.2.6 European Air Ambulance

- 6.2.7 Babcock Scandinavian Air Ambulance (Babcock International Group)

- 6.2.8 Air Charter Services Group

- 6.2.9 Gulf Helicopters

- 6.2.10 CareFlight