高温用コーティングの世界市場:市場シェア分析、産業動向・統計、成長予測(2024~2029年)

High Temperature Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1523350

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

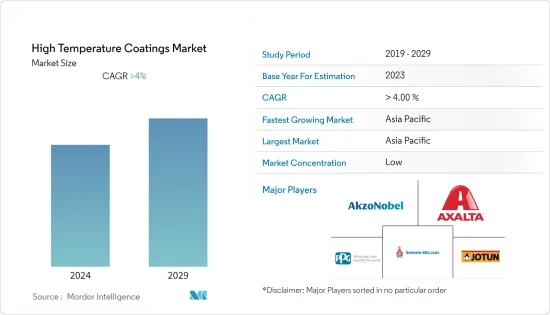

世界の高温用コーティングの市場規模は、2024年に37億1,000万米ドルに達し、2024~2029年の予測期間中にCAGR 4%以上で成長し、2029年には47億3,000万米ドルに達すると予測されています。

高温用コーティング市場は、COVID-19の大流行によってマイナスの影響を受けました。いくつかの国では全国的な封鎖措置がとられ、厳しい社会的避難措置が建築・建設、自動車、石油化学産業に悪影響を及ぼしました。しかし、COVID-19パンデミック後は、建築建設活動や自動車製造工場が操業を再開し、高温用塗料市場の復活につながりました。

主なハイライト

- 石油化学産業からの需要の増加と無溶剤高温用コーティングへの嗜好の変化が、現在の研究市場を牽引すると予想されます。

- 反面、厳しい環境規制と原料価格の変動が市場の成長を妨げると予想されます。

- 新興経済とインフラプロジェクトの成長は、予測期間中に市場に機会をもたらすと予想されます。

- アジア太平洋が市場を独占すると予想されます。また、中国、インド、日本などの国々からの消費の増加により、予測期間中に最も高いCAGRで推移することが予想されます。

高温用コーティング市場の動向

石油化学産業からの需要拡大

- 石油化学産業は、侵食、腐食、ケミカルアタック、摩耗、機械的損傷などの問題に常に直面しており、これらは時間の経過とともにインフラや設備の劣化を引き起こします。

- 高温用コーティングは、150℃から800℃までの温度に耐えるように設計されています。熱損失を最小限に抑え、断熱材下の腐食を抑制し、熱疲労を維持し、効率を維持するのに役立ちます。

- エネルギー産業と石油化学産業は、加熱処理装置、分離器、炉、加熱材料の輸送の使用により、重要な消費者のひとつとなっています。高温用コーティングはエネルギー損失を減らし、非生産時間を短縮するのに役立ちます。

- アジア太平洋では、石油化学プラントの新設に伴い耐熱コーティングの需要が増加しています。例えば、中国には305の石油化学プラントが計画・発表されており、2030年までに総生産能力は約1億5,240万トンとなります。また、同期間の資本支出は915億米ドルに達すると予想されています。

- 同様に北米でも、様々なエンドユーザー産業からの石油化学製品需要の増加により、石油化学産業は著しい成長率を記録しました。オンショア/オフショア探査・生産活動の成長、石油精製所と石油化学プラントの高成長、その他の化学プラント(医薬品を含む)の建設と近代化が、同地域の高温用コーティング需要を押し上げました。

- さらにVCIの統計によると、石油化学製品の輸出額は増加しており、耐熱コーティング市場を牽引しています。中国は2022年に673億米ドル相当の石油化学製品を輸出し、世界の主要輸出国となった。米国とオランダが2位と3位に続き、輸出額は438億米ドルと364億米ドルでした。

- 上記の要因から、石油化学産業からの高温用コーティングの需要は予測期間中に増加すると予想されます。

市場を独占するアジア太平洋

- アジア太平洋は、高温用コーティングの最大かつ最も急成長している市場です。高い経済成長率、製造業の成長、低コストの労働力、外国投資の増加、エンドユーザー産業からの需要の増加、先進国から新興国への世界の生産シフトなどが、同地域の市場成長をもたらしている主な要因です。

- 同地域における建設、石油化学、自動車産業の成長の高まりは、同地域における高温用コーティングの需要をさらに押し上げています。自動車産業と石油化学産業では、高温塗料は保護塗料として使用されています。

- 中国はアジア太平洋で最大の建設市場のひとつです。中国国家統計局によると、同国の建設工事生産額は2021年の29兆3,100億人民元(4兆840億米ドル)に対し、2022年には31兆2,000億人民元(4兆3,400億米ドル)に達します。さらに、投資物件として使用される住宅への需要も高まっています。中国は2030年までに約13兆米ドルを建築物に投じると予想されており、高温用塗料にとって明るい市場展望を生み出しています。

- 中国はこの地域最大の自動車メーカーです。OICA(The Organisation Internationale des Constructeurs d'Automobiles)によると、中国の自動車生産台数は2022年に2,702万台に達し、同時期の前年比3%増となった。

- インドは同地域で第2位の自動車メーカーとなった。OICAによると、2022年の自動車生産台数は545万台に達し、2021年の439万台から24%増加しました。このため、自動車生産台数の増加が自動車用コーティングの需要を押し上げ、高温用コーティング市場を牽引すると予想されます。

- インドでも同様に、石油化学産業が近年著しい成長を遂げています。化学・石油化学省によると、インドの化学・石油化学(CPC)産業は2022年に1,780億米ドルを記録し、2025年には3,000億米ドルに達すると予想されています。このように、化学・石油化学産業の成長は、同国における高温用コーティングの需要を促進すると予想されます。

- 以上のような要因から、アジア太平洋における高温用コーティングの需要は、予測期間中に大きく伸びると予想されます。

高温用コーティング産業の概要

高温用コーティング市場は部分的に細分化されています。同市場の主要企業(順不同)には、Akzo Nobel N.V.、Axalta Coating Systems、Jotun、PPG Industries Inc.、The Sherwin-Williams Companyなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 石油化学産業からの需要拡大

- 無溶剤高温用コーティングへの嗜好の変化

- その他の促進要因

- 抑制要因

- 厳しい環境規制

- 原材料価格の変動

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模:金額)

- タイプ

- エポキシ

- シリコーン

- ポリエステル

- アクリル

- アルキド

- その他のタイプ(ポリウレタン、ビニルエステルなど)

- 技術

- 水性

- 溶剤ベース

- パウダー

- エンドユーザー産業

- 航空宇宙・防衛

- 自動車

- 石油化学

- 建築・建設

- その他のエンドユーザー産業(海洋、水処理など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- ナイジェリア

- カタール

- エジプト

- UAE

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Akzo Nobel N.V.

- Aremco

- Axalta Coating Systems

- Carboline

- Chemcote PTY LTD

- GENERAL MAGNAPLATE CORPORATION

- Hempel A/S

- Jotun

- PPG Industries Inc.

- The Sherwin-Williams Company

- Valspar

第7章 市場機会と今後の動向

- 新興経済国の成長とインフラプロジェクト

- その他の機会

目次

The High Temperature Coatings Market size is estimated at USD 3.71 billion in 2024, and is expected to reach USD 4.73 billion by 2029, growing at a CAGR of greater than 4% during the forecast period (2024-2029).

The high temperature coatings market had negatively affected by the COVID-19 pandemic. Due to nationwide lockdowns in several countries, strict social distancing measures negatively affected the building and construction, automotive, and petrochemical industries. However, post-COVID pandemic, the building construction activities and automotive manufacturing plants resumed their operations, which helped to revive the market for high-temperature coatings.

Key Highlights

- The growing demand from petrochemical industries and the shift in preference towards solvent-free high-temperature coatings is expected to drive the current studied market.

- On the flip side, the stringent environmental regulations and the volatility in raw material prices are expected to hinder the growth of the market.

- The growth of emerging economies and infrastructure projects is expected to create opportunities for the market during the forecast period.

- The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period owing to the increasing consumption from countries such as China, India, and Japan.

High Temperature Coatings Market Trends

Growing Demand from Petrochemical Industry

- The petrochemical industry is constantly faced with problems like erosion, corrosion, chemical attack, wear, abrasion, and mechanical damage, which cause deterioration of infrastructure and equipment over time.

- High-temperature coatings are designed to withstand temperatures from 150°C to 800°C. It helps minimize heat losses, keep corrosion under insulation in check, maintain thermal fatigue, and maintain efficiency.

- Energy and Petrochemical industries are among the critical consumers owing to the use of heater-treaters, separators, furnaces, and the transport of heated materials. High-temperature coatings help decrease energy losses and reduce non-productive time.

- In the Asia-Pacific region, the demand for heat-resistant coatings is increasing with the development of new petrochemical plants. For instance, China has 305 planned and announced petrochemical plants, with a total capacity of about 152.4 mtpa by 2030. China is also expected to reach a capital expenditure of USD 91.5 billion over the same period.

- Similarly, in North America, the petrochemical industry registered a significant growth rate due to rising demand for petrochemicals from various end-user industries. The growth in onshore/offshore exploration and production activities, high growth observed in oil refineries and petrochemical plants, and the building and modernization of other chemical plants (which include pharmaceuticals) boosted the demand for high-temperature coatings in the region.

- Furthurmore according to VCI statistics the export value of petrochemicals is rising therbey driving the market for heat resistant coatings. China exported over USD 67.3 billion worth of petrochemicals in 2022, becoming the world's major exporting country. The United States and the Netherlands followed second and third, with an export value of USD 43.8 billion and USD 36.4 billion.

- Owing to the above-mentioned factors, the demand for high-temperature coatings from the petrochemical industry is expected to increase over the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region represents the largest and fastest-growing market for high-temperature coatings. High economic growth rate, growing manufacturing industries, low-cost labor, increasing foreign investments, increasing demand from end-user industries, and the global shift in production from developed countries to emerging countries in the region are some of the major factors leading to the growth of the market in the region.

- The escalating growth of the construction, petrochemical, and automotive industries in the region is further driving the demand for high-temperature coatings in the region. In the automotive and petrochemical industries the high temperature coatings are used as protective coatings.

- China is one of the largest construction markets in the Asia-Pacific region. According to the National Bureau of Statistics of China, the output value of construction works in the country accounted for CNY 31.2 trillion (USD 4.34 trillion) in 2022, as compared to CNY 29.31 trillion (USD 4.084 trillion) in 2021. Additionally, demand is increased for residences that are used as investment properties. China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive market outlook for high temperature coatings.

- China is the largest automotive vehicle manufacturer in the region. According to OICA (The Organisation Internationale des Constructeurs d'Automobiles), automotive vehicle production in China reached a total of 27.02 million units in 2022, an increase of 3% over the previous year for the same period.

- India has become the second-largest automotive vehicle manufacturer in the region. According to OICA, the total production volume of automotive vehicles reached 5.45 million units in 2022, indicating a growth of 24% as compared to 4.39 million units registered in 2021. Thus, the increase in the production of automotive vehicles is expected to drive the demand for automotive coatings, thereby driving the market for high temperature coatings.

- Similarly in India the petrochemical industry registered a significant growth in recent years. According to the Department of Chemicals & Petrochemicals, India's chemical and petrochemical (CPC) industry registered USD 178 billion in 2022, and it is expected to reach USD 300 billion by 2025. Thus the growth in chemical and petrochemical industries is expected to drive the demand for high temperature coatings in the country.

- Owing to the above mentioned factors, the demand for high-temperature coatings in Asia-Pacific region is expected to grow considerably over the forecast period.

High Temperature Coatings Industry Overview

The high-temperature coatings market is partially fragmented in nature. Some of the major players in the market (not in any particular order) include Akzo Nobel N.V., Axalta Coating Systems, Jotun, PPG Industries Inc., and The Sherwin-Williams Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Petrochemical Industry

- 4.1.2 Shift in Preference Toward Solvent-Free High Temperature Coatings

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations

- 4.2.2 Volatility in Raw Material Prices

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Epoxy

- 5.1.2 Silicone

- 5.1.3 Polyester

- 5.1.4 Acrylic

- 5.1.5 Alkyd

- 5.1.6 Other Types (Polyurethane, Vinyl Ester, etc.)

- 5.2 Technology

- 5.2.1 Water based

- 5.2.2 Solvent based

- 5.2.3 Powder

- 5.3 End-user Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Automotive

- 5.3.3 Petrochemical

- 5.3.4 Building and Construction

- 5.3.5 Other End-user Industries (Marine, Water Treatment, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Nigeria

- 5.4.5.2 Qatar

- 5.4.5.3 Egypt

- 5.4.5.4 UAE

- 5.4.5.5 Saudi Arabia

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Aremco

- 6.4.3 Axalta Coating Systems

- 6.4.4 Carboline

- 6.4.5 Chemcote PTY LTD

- 6.4.6 GENERAL MAGNAPLATE CORPORATION

- 6.4.7 Hempel A/S

- 6.4.8 Jotun

- 6.4.9 PPG Industries Inc.

- 6.4.10 The Sherwin-Williams Company

- 6.4.11 Valspar

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Growth of Emerging Economies and Infrastructure Projects

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日