合わせガラス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

Laminated Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1523348

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

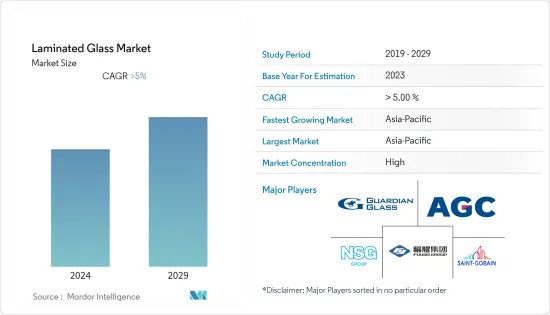

合わせガラス市場規模は2024年に206億2,000万米ドルと推計され、2029年には268億3,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは5%を超えると予測されます。

COVID-19は合わせガラス市場に悪影響を及ぼしました。多くの産業と同様に、合わせガラス市場もパンデミックの初期段階で減速を経験しました。これはサプライチェーンの混乱、労働力不足、建設活動の減少が原因でした。封鎖措置が緩和され、建設活動が再開されると、合わせガラスの需要は回復しました。パンデミックにより延期または中断された建設プロジェクトが再開され、住宅、商業施設、インフラプロジェクトで使用される合わせガラスを含むガラス製品の需要が増加しました。

主なハイライト

- 建築分野でレンガを構造用ガラスに置き換える合わせガラスの用途が増加していることと、技術の進歩が合わせガラス市場を牽引している主な要因です。

- 合わせガラスは製造工程が多いため、他の一般的な窓ガラスよりも高価であり、これが市場成長の妨げになる可能性が高いです。

- また、途上諸国における急速な都市化や、自動車分野からの合わせガラス需要の高まりは、市場関係者に様々な機会を提供すると予想されます。

- 中国、インド、日本などは合わせガラスの重要な消費国であるため、アジア太平洋地域は高い成長率を示しています。

合わせガラス市場の動向

市場を独占する自動車セグメント

- 合わせガラスは車室内への騒音透過を低減し、乗員の快適性を向上させます。消費者が快適さと静かな運転体験を優先するようになっているため、自動車メーカーは合わせガラスを利用して遮音性を高めています。

- 合わせガラスにはUVカット機能を持つ中間膜を組み込むことができ、内装材の色あせを抑え、有害な紫外線から乗員を守ります。この機能は日差しの強い地域には不可欠です。

- 電気自動車(EV)の人気の高まりは、合わせガラスメーカーにチャンスを提供しています。EVメーカーは、安全性、快適性、エネルギー効率のために合わせガラスを使用するなど、製品を差別化するために先進的な機能や技術を優先することが多いです。

- 国際エネルギー機関(IEA)が発表した推計によると、2022年のバッテリー電気自動車の販売台数は730万台に達し、2021年の約460万台から増加します。持続可能な輸送に対する消費者の関心の高まりや、直接的な大気汚染の削減を目的とした政府の法規制などの要因が、BEVの販売台数の増加につながった。

- さらに、IEAが発表した推計によると、2022年には、世界の電気自動車の約84.76%が販売され、その結果、電気自動車の国内生産が増加しました。これは、同年の国際貿易による販売台数160万台に対し、約900万台の販売に相当します。

- 経済分析局(BEA)が発表した最新の推計によると、2023年の米国の乗用車年間販売台数は312万台で、2022年の286万台から増加しました。

- その結果、同市場は上記の要因から予測期間中に成長を記録すると予想されます。

アジア太平洋地域が市場を独占する

- アジア太平洋地域は急速な人口増加と都市化が進んでおり、建設やインフラ整備の需要を牽引しています。合わせガラスは、アジア太平洋地域の商業施設、住宅、施設などの建物のファサード、窓、ドア、天窓などに広く使用されています。

- 同地域は世界で最も経済成長が著しい地域の一つであり、建設プロジェクトに多額の投資が行われています。合わせガラスは、その安全性、防犯性、審美性から建築家や建設業者に好まれています。上海、北京、シンガポール、ムンバイなどの都市における高層ビル、ショッピングモール、ホテル、集合住宅の建設は、合わせガラスの需要を促進しています。

- さらに、中国国家統計局が発表した最新の推計によると、2022年、中国の建設産業は31兆人民元以上の生産高をあげています。

- アジア太平洋は世界最大の自動車市場であり、自動車の生産と販売でリードしています。合わせガラスは、安全性と騒音低減のために自動車のフロントガラスに主に使用されています。同地域の自動車産業の成長は、合わせガラスの需要にさらに貢献しています。

- 中国汽車工業協会(CAAM)が発表した最新の推計によると、2022年4月現在、中国の商用車生産台数は約21万台、乗用車生産台数は約99万6,000台となっています。同業界は同月中に合計120万台を生産しました。

- 日本の経済産業省(経産省)が発表した推計によると、2022年の日本の自動車産業による自動車生産額は約19兆2,900億円(1,300億米ドル)で、前年の約17兆6,500億円(1,200億米ドル)から増加しました。

- 今後数年間は、これらすべてがこの地域の市場成長に大きな影響を与えると予想されます。

合わせガラス産業の概要

合わせガラス市場は部分的に統合されています。同市場の主要企業(順不同)には、Saint-Gobain、 AGC Glass Europe、Guardian Industries Holdings、Nippon Sheet Glass、Fuyao Glass Industry Groupが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- レンガから構造用ガラスへの置き換え用途の増加

- 技術の進歩

- 抑制要因

- 製造コストの高さ

- その他の阻害要因

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- タイプ別

- ポリビニルブチラール(PVB)

- セントリーグラス・プラス(SGP)

- エチレンビニルアセテート(EVA)

- その他(イオノプラスト、防火合わせガラス)

- エンドユーザー産業別

- 自動車

- 建築・建設

- エレクトロニクス

- その他(セキュリティ・防衛)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- タイ

- マレーシア

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- トルコ

- ロシア

- 北欧諸国

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- エジプト

- カタール

- アラブ首長国連邦

- その他中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AGC Inc.

- Asahi India Glass Limited

- CARDINAL GLASS INDUSTRIES INC.

- Central Glass Co. Ltd

- Fuyao Group

- GSC GLASS LTD

- Guardian Industries Holdings

- Nippon Sheet Glass Co. Ltd

- Saint-Gobain

- Stevenage Glass Company Ltd

- Taiwan Glass Ind. Corp.

第7章 市場機会と今後の動向

目次

The Laminated Glass Market size is estimated at USD 20.62 billion in 2024, and is expected to reach USD 26.83 billion by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

COVID-19 had a detrimental effect on the laminated glass market. Like many industries, the laminated glass market experienced a slowdown in the early stages of the pandemic. This occurred due to disruptions in supply chains, labor shortages, and decreased construction activity. As lockdown measures eased and construction activities resumed, the demand for laminated glass picked up. Construction projects that were delayed or put on hold due to the pandemic restarted, driving demand for glass products, including laminated glass, for use in residential, commercial, and infrastructure projects.

Key Highlights

- The increasing application of laminated glass in replacing bricks with structural glass in the construction sector and the advancement in technology are the key factors that are driving the laminated glass market.

- Laminated glass is more expensive than other regular windows because of the number of steps taken to produce it, which is likely to hamper market growth.

- Also, the rapid urbanization in developing countries and the rising demand for laminated glasses from the automotive sector are expected to provide various opportunities to market players.

- Due to the fact that countries like China, India, and Japan are critical consumers of laminated glass, Asia-Pacific has a high growth rate.

Laminated Glass Market Trends

Automotive Segment to Dominate the Market

- Laminated glass helps reduce noise transmission into the vehicle cabin, enhancing comfort for passengers. As consumers increasingly prioritize comfort and a quieter driving experience, automakers utilize laminated glass to improve acoustic insulation.

- Laminated glass can incorporate interlayers that provide UV protection, reducing the fading of interior materials and protecting occupants from harmful UV radiation. This feature is essential for regions with intense sunlight exposure.

- The increasing popularity of electric vehicles (EVs) offers opportunities for laminated glass manufacturers. EV manufacturers often prioritize advanced features and technologies to differentiate their products, including the use of laminated glass for safety, comfort, and energy efficiency.

- According to the estimate released by the International Energy Agency (IEA), in 2022, sales of battery electric vehicles reached 7.3 million, up from around 4.6 million in 2021. Factors such as increased consumer interest in sustainable transport and governmental legislation that aims to reduce direct air pollution have led to a rise in the sale of BEVs.

- Further, according to the estimate released by the IEA, in 2022, around 84.76% of global electric vehicles were sold, resulting from the domestic production of these vehicles. This represented nearly 9 million sales, compared to 1.6 million units sold from international trade that year.

- According to the latest estimate published by the Bureau of Economic Analysis (BEA), the annual passenger car sales in the United States were 3.12 million units in 2023, which increased from 2.86 million units in 2022.

- Consequently, the market is expected to register growth during the forecast period due to the abovementioned factors.

Asia-Pacific to Dominate the Market

- Asia-Pacific has experienced rapid population growth and urbanization, driving demand for construction and infrastructure development. Laminated glass is widely used in building facades, windows, doors, and skylights in commercial, residential, and institutional buildings across the region.

- It is home to some of the world's fastest-growing economies, leading to significant investments in construction projects. Laminated glass is a preferred choice for architects and builders due to its safety, security, and aesthetic properties. The construction of skyscrapers, shopping malls, hotels, and residential complexes in cities like Shanghai, Beijing, Singapore, and Mumbai fuels the demand for laminated glass.

- Furthermore, according to the latest estimate published by the National Bureau of Statistics of China, in 2022, the construction industry in China generated an output of over CNY 31 trillion.

- Asia-Pacific is the largest automotive market globally, leading in automobile production and sales. Laminated glass is majorly used in automotive windshields for safety and noise reduction. The region's automotive industry's growth further contributes to the demand for laminated glass.

- According to the latest estimate published by the China Association of Automobile Manufacturers (CAAM), China produced approximately 210,000 commercial vehicles and 996,000 passenger cars as of April 2022. The industry produced a total of 1.2 million vehicles during the month.

- According to the estimate released by the Ministry for Economy, Trade, and Industry (Meti), Japan, in 2022, the production value of motor vehicles by the automotive industry in Japan was approximately JPY 19.29 trillion (USD 0.13 trillion), increasing from around JPY 17.65 trillion (USD 0.12 trillion) in the previous year.

- In the coming years, all of this is expected to have a significant impact on the growth of the region's market.

Laminated Glass Industry Overview

The laminated glass market is partially consolidated in nature. Some of the major players in the market (not in any particular order) include Saint-Gobain, AGC Glass Europe, Guardian Industries Holdings, Nippon Sheet Glass Co. Ltd, and Fuyao Glass Industry Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Application in Replacement of Bricks with Structural Glass

- 4.1.2 Advancements in Technology

- 4.2 Restraints

- 4.2.1 High Cost of Manufacturing

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Type

- 5.1.1 Polyvinyl Butyral (PVB)

- 5.1.2 Sentryglas Plus (SGP)

- 5.1.3 Ethylene-vinyl Acetate (EVA)

- 5.1.4 Other Types (Ionoplast, Fire-Rated Laminated Glass)

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Building and Construction

- 5.2.3 Electronics

- 5.2.4 Other End-user Industries (Security and Defense)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Egypt

- 5.3.5.5 Qatar

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AGC Inc.

- 6.4.2 Asahi India Glass Limited

- 6.4.3 CARDINAL GLASS INDUSTRIES INC.

- 6.4.4 Central Glass Co. Ltd

- 6.4.5 Fuyao Group

- 6.4.6 GSC GLASS LTD

- 6.4.7 Guardian Industries Holdings

- 6.4.8 Nippon Sheet Glass Co. Ltd

- 6.4.9 Saint-Gobain

- 6.4.10 Stevenage Glass Company Ltd

- 6.4.11 Taiwan Glass Ind. Corp.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Urbanization in Developing Countries

- 7.2 Rising Demand from the Automotive Sector

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日