|

|

市場調査レポート

商品コード

1521878

アデノ随伴ウイルス(AAV)CDMO-市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Adeno-Associated Virus (AAV) CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アデノ随伴ウイルス(AAV)CDMO-市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

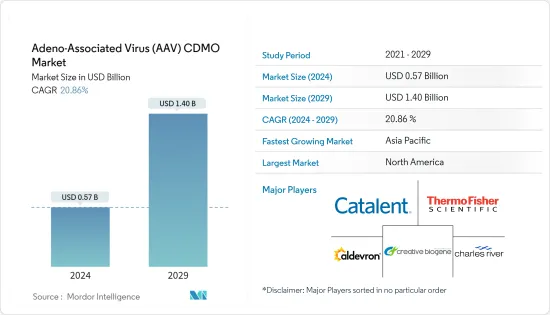

アデノ随伴ウイルス(AAV)CDMO市場規模は2024年に5億7,000万米ドルと推定され、2029年には14億米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは20.86%で成長する見込みです。

アデノ随伴ウイルス(AAV)CDMO市場の成長を促す主要要因には、遺伝子治療の利用拡大、AAVベクターの進歩、AAVベクター製造のアウトソーシング増加などがあります。

AAV開発セグメントで事業を展開する企業は、新技術を開発し、市場に利益をもたらす戦略的活動に取り組んでいます。例えば、Thermo Fisher Scientificは2022年11月、ギブコCTSアデノ随伴ウイルス(AAV)MAXヘルパーフリー生産システムを発表しました。CTS AAV-MAXシステムには、哺乳類細胞、細胞培養培地、トランスフェクション・キット、バッファーなどのコンポーネントが含まれています。

2022年2月、Mirus Bioは、細胞・遺伝子治療用途の大規模ウイルスベクター生産用のTransit-VirusGEN SELECTトランスフェクション・キットを発売しました。このキットは前臨床とプロセス開発活動をサポートし、TransIT-VirusGENトランスフェクション試薬、複合体形成溶液、エンハンサーで構成されています。従って、AAV技術の採用はその需要を増加させると予想され、生産は予測期間中CDMOサービスの需要を押し上げると考えられます。

さらに、生命を脅かす疾患の治療における遺伝子治療の重要性を明らかにする調査の増加が、市場の成長を後押ししています。例えば、2022年2月にRadiology and Oncology Journalに掲載された研究では、がん治療にアデノ随伴ウイルスベクターを使用することで、腫瘍学の領域を変える可能性があると主張されています。特にウイルスベクターは、効果的な遺伝子導入と抗腫瘍反応のための免疫系関与というユニークな組み合わせを記載しています。このような研究により、がん治療法の設計におけるAAV受託製造の採用が増加し、市場成長の原動力になると予想されます。

しかし、生産能力の課題や規制上の問題が、長期的には市場成長の妨げになると予想されます。

アデノ随伴ウイルス(AAV)CDMO市場動向

細胞・遺伝子治療開発は予測期間中に急成長が見込まれる

細胞・遺伝子治療開発は、最も急速に発展しているセグメントの一つです。細胞治療と遺伝子治療のセグメントでは、いくつかの開発が行われており、それがセグメントの成長を牽引しています。例えば、2023年6月、インドの製薬会社の1つであるLaurus Labs Ltdは、AAVベクターを使用した新規遺伝子治療資産を導入し、市場に投入するための覚書をIIT Kanpur(IITK)と締結しました。

同様に2022年12月、Merckは日本における遺伝子治療開発を強化するため、神戸大学からスピンオフしたSynplogenと提携しました。この提携は、MerckのCTDMOの専門知識とシンプロジェンの能力を融合させ、遺伝子治療の開発、製造、試験の合理化プロセスを促進するものです。

2022年8月、Polyplusは、ウイルスベクター生産に特化した画期的なトランスジーンプラスミドエンジニアリングサービスを発表しました。ポリプラスのプラスミドサービスは、次世代ウイルスベクターや遺伝子治療の製造に包括的な選択肢を提供するものです。これらのサービスは、単独で利用することも、業界標準のPEIproやFectoVIR-AAV試薬・キットと組み合わせて利用することも可能です。2022年5月、AGCバイオロジクスはコロラド州ロングモントの施設を拡大し、ウイルスベクター懸濁技術と遺伝子治療の開発と製造をサポートする能力を追加しました。2022年第3四半期に稼働を開始したこれらの新機能は、同施設の既存のウイルスベクターと細胞治療サービスを強化するものでした。

その結果、細胞・遺伝子治療への企業の関与が急増していることや、企業間の強固な協力関係などの要因により、細胞・遺伝子治療セグメントは今後大きく成長する展望です。

予測期間中、北米が市場を独占する見込み

北米は、製薬・バイオテクノロジー産業が確立されていること、地域全体で受託製造への注目が高まっていることなどの要因から、市場を独占すると予想されます。

企業は遺伝子治療の研究開発に投資しています。例えば、2022年10月、アステラス製薬は、レット症候群と巨大軸索神経障害(GAN)に対するAAV遺伝子治療の2つの取り組みへのアクセスを得るために、Taysha Gene Therapies Inc.に5,000万米ドルを投資しました。同様に、2022年3月に更新されたデータ別の国立がん研究所(NIC)には、2022年連結歳出法により69億米ドルが与えられました。これは2021年度より3億5,300万米ドルの純増でした。2022年度の配分には、キャンサームーンショットへの1億9,400万米ドルと小児がんデータイニシアチブへの5,000万米ドルの資金が含まれていました。このように、国全体で精密医療アプローチを可能にするための投資が増加していることが、予測期間中の市場を牽引すると予想されます。

このセグメントで事業を展開する企業は、がん治療のための先進的で効果的な治療の研究開発や新製品の上市に多額の投資を行っており、調査対象市場のがんセグメントの成長をさらに押し上げると予想されます。

2022年11月、米国食品医薬品局は、血友病Bまたは生命を脅かす歴史的出血を有する成人、または重篤で重度の自然出血エピソードを繰り返す成人の治療として、アデノ随伴ウイルスベクターを用いた遺伝子治療Hemgenixを承認しました。

北米市場は、企業による投資の増加と、同地域に確立された製薬産業が存在することから成長を遂げています。

アデノ随伴ウイルス(AAV)CDMO産業概要

AAV CDMOの市場競争は中程度で、複数の企業が世界に事業を展開しています。各社は主に、共同研究、合併、買収、提携などの戦略的活動に注力し、市場での地位を維持しています。市場に参入している主要企業には、Thermo Fischer Scientific Inc.、Creative Biogene、Catalent Inc.、Charles River Laboratories International Inc.、Danaher(Aldevron)などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブ概要

第4章 市場力学

- 市場概要

- 市場促進要因

- 遺伝子治療の利用拡大

- AAVベクターの進歩

- AAVベクター製造のアウトソーシングの増加

- 市場抑制要因

- 生産能力の課題

- 規制の問題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドルベース)

- ワークフロー別

- 上流工程

- ダウンストリーム処理

- 培養タイプ別

- 付着培養

- 懸濁培養

- 用途別

- 細胞・遺伝子治療開発

- ワクチン開発

- バイオ医薬品・創薬

- バイオメディカル研究

- エンドユーザー別

- 製薬・バイオ医薬品企業

- 学術・研究機関

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Aldevron

- Charles River Laboratories Inc.

- Forge Biologics

- Creative Biogene

- Genezen

- VIRALGEN

- Catalent Inc.

- Merck KGaA

- ViroCell Biologics Ltd

- Biovian Oy

- Thermo Fisher Scientific Inc.

第7章 市場機会と今後の動向

The Adeno-Associated Virus CDMO Market size is estimated at USD 0.57 billion in 2024, and is expected to reach USD 1.40 billion by 2029, growing at a CAGR of 20.86% during the forecast period (2024-2029).

The key factors driving the growth of the adeno-associated virus CDMO market include the increasing use of gene therapy, advancements in AAV vectors, and rising outsourcing of AAV vector manufacturing.

Companies operating in the AAV development field are developing new technologies and engaging in strategic activities that benefit the market. For instance, in November 2022, Thermo Fisher Scientific introduced the Gibco CTS adeno-associated virus (AAV) MAX Helper Free production system, which it claims can save time and reduce costs by 50%. The CTS AAV-MAX system includes several components: mammalian cells, a cell culture medium, a transfection kit, and a buffer.

In February 2022, Mirus Bio launched Transit-VirusGEN SELECT Transfection Kits for large-scale viral vector production for cell and gene therapy applications. The kits support pre-clinical and process development activities and consist of the TransIT-VirusGEN Transfection Reagent, a complex formation solution, and an enhancer. Hence, the introduction of AAV technologies is expected to increase its demand, and production is likely to boost the demand for CDMO services over the forecast period.

Furthermore, growing research identifying the importance of gene therapy in treating life-threatening diseases is propelling market growth. For instance, the study published in the Radiology and Oncology Journal in February 2022 claimed that the use of adeno-associated viral vectors to treat cancer had the potential to change the area of oncology. Virus vectors, in particular, provide a unique mix of effective gene delivery and immune system engagement for anti-tumour responses. Such studies are expected to increase the adoption of AAV contract manufacturing in designing cancer therapies, driving market growth.

However, production capacity challenges and regulatory issues are expected to hinder market growth in the long run.

Adeno-Associated Virus (AAV) CDMO Market Trends

Cell and Gene Therapy Development is Expected to Witness Rapid Growth Over the Forecast Period

Cell and gene therapy development is one of the most rapidly evolving segments. Several developments are occurring in the cell and gene therapy space that are driving segmental growth. For instance, in June 2023, Laurus Labs Ltd, one of the pharma companies in India, inked a memorandum of agreement (MoA) with IIT Kanpur (IITK) for in-licensing novel gene therapy assets using AAV vectors and bringing them to market.

Similarly, in December 2022, Merck partnered with Synplogen, a Kobe University spin-off, to enhance gene therapy development in Japan. This collaboration combined Merck's CTDMO expertise with Synplogen's capabilities, facilitating streamlined processes for gene therapy development, manufacturing, and testing.

In August 2022, Polyplus unveiled its groundbreaking Transgene Plasmid Engineering Services tailored specifically for viral vector production. The expansion of Polyplus' plasmid services provided a comprehensive range of options for next-generation viral vector and gene therapy manufacturing. These services can be utilized independently or in conjunction with the industry-standard PEIpro and FectoVIR-AAV reagents and kits. In May 2022, AGC Biologics expanded its Longmont, Colorado facility, adding viral vector suspension technology and capacity to support the development and manufacturing of gene therapies. These new capabilities, which were launched online in the third quarter of 2022, enhanced the site's existing viral vector and cell therapy services.

Consequently, due to factors such as the burgeoning involvement of companies in cell and gene therapy and robust collaborations among them, the cell and gene therapy segment is poised for significant growth in the future.

North America is Expected to Dominate the Market During the Forecast Period

North America is expected to dominate the market due to factors such as the well-established pharmaceutical and biotechnology industry and the rising focus on contract manufacturing across the region.

The companies are investing in research and development of gene therapy. For instance, in October 2022, Astellas invested USD 50 million in Taysha Gene Therapies Inc. in order to gain access to two of its AAV gene therapy initiatives for Rett syndrome and giant axonal neuropathy (GAN). Similarly, the National Cancer Institute (NIC), based on data updated in March 2022, was given USD 6.9 billion by the Consolidated Appropriations Act 2022. This was a net increase of USD 353 million over FY 2021. The FY 2022 allocation included USD 194 million in funding for the Cancer Moonshot and USD 50 million for the Childhood Cancer Data Initiative. Thus, increasing investments in enabling a precision medicine approach across the country are expected to drive the market during the forecast period.

Companies operating in the area are investing heavily in the research and development of advanced and effective therapeutics for cancer treatment and launching new products, which is expected to further boost the growth of the cancer segment in the market studied.

In November 2022, the US Food and Drug Administration approved Hemgenix, an adeno-associated virus vector-based gene therapy for treating adults with Hemophilia B or life-threatening historical hemorrhage or who have repeated, serious, severe spontaneous bleeding episodes.

The North American market is experiencing growth as a result of increasing investments by companies and the presence of a well-established pharmaceutical industry in the region.

Adeno-Associated Virus (AAV) CDMO Industry Overview

The market for AAV CDMO is moderately competitive, with several companies operating globally. The companies are mainly focusing on strategic activities such as collaboration, mergers, acquisitions, and partnerships to sustain themselves in the market. Some of the key players operating in the market include Thermo Fischer Scientific Inc., Creative Biogene, Catalent Inc., Charles River Laboratories International Inc., and Danaher (Aldevron).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Use of Gene Therapy

- 4.2.2 Advacements in AAV Vector

- 4.2.3 Rising Outsourcing of AAV Vector Manufacturing

- 4.3 Market Restraints

- 4.3.1 Production Capacity Challenges

- 4.3.2 Regultory Issues

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size - Value in USD)

- 5.1 By Workflow

- 5.1.1 Upstream Processing

- 5.1.2 Downstream Processing

- 5.2 By Culture Type

- 5.2.1 Adherent Culture

- 5.2.2 Suspension Culture

- 5.3 By Application

- 5.3.1 Cell & Gene Therapy Development

- 5.3.2 Vaccine Development

- 5.3.3 Biopharmaceutical & Pharmaceutical Discovery

- 5.3.4 Biomedical Research

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biopharmaceutical Companies

- 5.4.2 Academic & Research Institutes

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aldevron

- 6.1.2 Charles River Laboratories Inc.

- 6.1.3 Forge Biologics

- 6.1.4 Creative Biogene

- 6.1.5 Genezen

- 6.1.6 VIRALGEN

- 6.1.7 Catalent Inc.

- 6.1.8 Merck KGaA

- 6.1.9 ViroCell Biologics Ltd

- 6.1.10 Biovian Oy

- 6.1.11 Thermo Fisher Scientific Inc.