輸液製剤:市場シェア分析、産業動向・統計、成長予測(2024~2029年)

Infused Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1521787

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

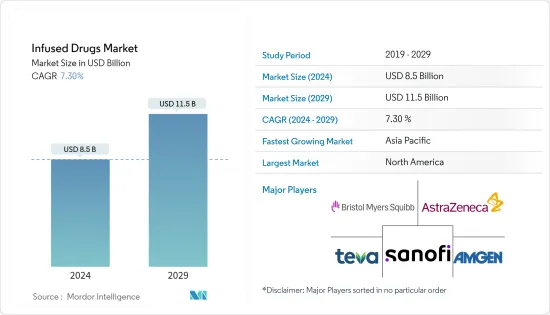

輸液製剤市場規模は2024年に85億米ドルと推定され、2029年には115億米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは7.30%で成長する見込みです。

輸液製剤市場の成長を促す主要要因は、慢性疾患の蔓延、ドラッグデリバリーシステムの進歩、高齢者人口の増加です。例えば、2022年のアジア太平洋の60歳以上の人口は約6億7,000万人で、およそ7人に1人を占めています。2050年には、その数は倍増して13億人になると予測されています。国連アジア太平洋経済社会委員会の報告書によると、アジアの高齢者人口のうち、女性は54%を占めており、平均寿命が長いため、年齢とともに増加する傾向にあります。高齢者人口の増加は、予測期間中の市場の牽引役となることが期待されます。

主要ハイライト

- さらに、心血管疾患、腫瘍性疾患、糖尿病などの慢性疾患の有病率の増加が市場の成長に寄与しています。例えば、英国心臓財団(BHF)が2023年4月に発表した報告書によると、2022年には英国で760万人以上が心臓・循環器疾患を抱えて生活しており、高齢化、出生率の低下、他の慢性疾患からの生存率の上昇により、さらに増加すると予測されています。したがって、慢性疾患の有病率の上昇は、これらの疾患を効果的に管理するための輸液製剤に対する需要を増加させ、最終的に研究市場を牽引すると予想されます。

- さらに、買収や製品上市などの戦略的活動の増加も市場を牽引すると予想されます。例えば、Bristol Myers Squibbは2024年3月、再発または難治性の慢性リンパ性白血病(CLL)成人患者の治療として、CD19指向性キメラ抗原受容体(CAR)T細胞療法である生物製剤「Breyanzi」の承認を米国食品医薬品局から取得しました。Breyanziは、CAR陽性の生存T細胞を含む1回投与量の点滴静注で終了する治療プロセスを通じて投与されます。このような製品の上市は、予測期間中、市場を牽引すると予想されます。

- しかし、輸注薬に関連する副作用、厳しい規制、輸注薬の製造・市場開拓の高コストが、輸注薬市場の成長を制限する可能性があります。

輸液製剤市場の動向

予測期間中、がん領域が大きな市場シェアを占める見込み

- がんの有病率の増加は、がん患者への迅速な作用から輸液製剤の需要を増加させると予想されています。例えば、2023年1月にSpanish Network Of Cancer Registriesが発表した報告書によると、2023年にスペインで報告された新規症例は約29万5,675件で、2022年と比較して1.96%増加しています。がんの有病率の増加は、輸注薬の需要を促進すると予想されます。

- さらに、がん領域における新薬の研究開発のための資金も増加しています。例えば米国では、米国国立衛生研究所(NIH)ががんに関連する研究活動に2022年の76億3,500万米ドルに対し、2023年には80億7,800万米ドルを投資しています。このようながん領域での市場開拓活動により、同市場における新規注入型抗がん剤の増加が期待されます。

- さらに、製品上市などの戦略的活動の増加は、がん領域の成長を促進すると予想されます。例えば、2022年10月に米国食品医薬品局は再発/難治性多発性骨髄腫の治療としてTeclistamab-cqvy(Tecvayli)を承認しました。

- したがって、がんの有病率の上昇と製品上市の増加は、予測期間中の同セグメントの成長を促進すると予想されます。

北米が大きな市場シェアを占める

- 北米の輸液製剤市場は、がんや感染症などの慢性疾患の有病率の上昇、研究開発活動への投資の増加などの要因により、予測期間中に成長すると見込まれます。また、主要企業による製品上市や買収などの戦略的活動の増加も、同地域の市場を牽引すると予想されます。

- がんなどの慢性疾患の有病率の上昇は、腫瘍学で使用される特殊治療の需要を増加させると予想されます。例えば、米国がん協会が2023年に更新したデータによると、米国では肺がんの罹患率が増加しており、2022年には23万6,740人の肺がん患者が報告されたのに対し、2023年には23万8,340人の肺がん患者が報告されました。同様に、カナダがん協会が2024年1月に更新したデータによると、2023年には男性約12万4,200人、女性約11万4,900人ががんと診断されたと推定されています。前立腺がんは、2023年における男性の新規がん症例の5分の1(20%)を占めています。従って、北米におけるがん患者の大幅な有病率は、輸液製剤の需要に拍車をかけると予測されます。

- 政府や民間組織による研究開発への投資の増加も、北米市場を牽引すると予想されます。例えば、2023年11月、全米多発性硬化症協会は、新たな研究プロジェクトに440万米ドルを投資し、「治療への道(Pathways to Cure)」のロードマップに概説された有望セグメントに世界のMS研究を誘導する戦略に合致させました。さらに、米国では2023年3月、Bayer AGが医薬品の研究開発に10億米ドルの投資を計画しています。このような研究開発への莫大な投資は、新規性の高い製品の上市につながる可能性があります。

- したがって、がん患者の有病率の上昇と政府と民間組織による研究開発投資の増加は、予測期間にわたって北米市場を牽引すると予想されます。

輸液製剤産業概要

輸液製剤市場の競争は中程度です。主要企業は、市場での地位を強化するために、製品の発売、製品サービスの新地域への拡大、合併、買収、新たなパートナーシップや提携の締結など、さまざまな戦略を採用しています。主要企業には、AstraZeneca、Sanofi SA、Teva Pharmaceutical Industries Ltd、Amgen, Inc.、Bristol-Myers Squibb Companyなどが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブ概要

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患の有病率の増加

- 高齢者人口の増加

- 市場抑制要因

- 投薬に伴う副作用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- 医薬品タイプ別

- 低分子医薬品

- 生物製剤

- 治療領域別

- がん領域

- 消化器疾患

- 関節リウマチ

- 免疫不全

- 心臓病学

- 神経学

- 糖尿病

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- AstraZeneca

- Sanofi SA

- Pfizer Inc.

- Weefsel Pharma

- Parenteral Drugs (India) Limited

- Bristol-Myers Squibb Company

- Regeneron Pharmaceuticals Inc.

- Eisai Co. Ltd

- Amgen Inc.

- Teva Pharmaceutical Industries Ltd

第7章 市場機会と今後の動向

目次

The Infused Drugs Market size is estimated at USD 8.5 billion in 2024, and is expected to reach USD 11.5 billion by 2029, growing at a CAGR of 7.30% during the forecast period (2024-2029).

The key factors driving the growth of the infused drugs market are the growing prevalence of chronic diseases, advancements in drug delivery systems, and the rising geriatric population. For instance, in 2022, there were approximately 670 million people aged 60 years or older in Asia-Pacific, which accounted for roughly one in every seven people in the region. By 2050, the number is projected to be doubled to 1.3 billion. Among the elderly population in Asia, women comprise 54%, and this tends to increase with age due to their long life expectancy, according to a report by the United Nations Economic and Social Commission for Asia and the Pacific. The rising geriatric population is expected to drive the market over the forecast period.

Key Highlights

- Moreover, the increasing prevalence of chronic conditions such as cardiovascular diseases, oncology diseases, and diabetes contribute to the market's growth. For instance, according to the report published by the British Heart Foundation (BHF) in April 2023, more than 7.6 million people were living with heart and circulatory diseases in the United Kingdom in 2022, which is further projected to increase with the aging population, decreasing fertility rates, and increasing survivability from other chronic diseases. Hence, the rising prevalence of chronic diseases is expected to increase the demand for infused drugs to effectively manage these diseases, ultimately driving the market studied market.

- Furthermore, increasing strategic activities such as acquisitions and product launches are also expected to drive the market. For instance, in March 2024, Bristol Myers Squibb received approval from the United States Food and Drug Administration for a biological product, Breyanzi, a CD19-directed chimeric antigen receptor (CAR) T cell therapy, for the treatment of adult patients with relapsed or refractory chronic lymphocytic leukemia (CLL). Breyanzi is delivered through a treatment process that culminates in a one-time infusion with a single dose containing CAR-positive viable T cells. Such product launches are expected to drive the market over the forecast period.

- However, the side effects associated with infusion drugs, strict regulations, and the high cost of manufacturing and developing infusion drugs may restrict the growth of the infused drugs market.

Infused Drugs Market Trends

Oncology is Expected to Have Significant Market Share During the Forecast Period

- The rising prevalence of cancer is expected to increase the demand for infused drugs because of their rapid action in cancer patients. For instance, according to the report published by the Spanish Network Of Cancer Registries in January 2023, about 295,675 new cases were reported in Spain in 2023, which represented 1.96% more compared to 2022. The increasing prevalence of cancer is expected to drive the demand for infused drugs.

- Moreover, the funding for research and development of novel medicines in oncology is increasing. For instance, in the United States, the National Institute of Health (NIH) invested USD 8,078 million in 2023 compared to 7,635 million in 2022 for its research activities associated with cancer. Such development activities in oncology are expected to increase the novel infused anti-cancer medicines in the market.

- Furthermore, the increasing strategic activities, such as product launches, are expected to drive the growth of the oncology segment. For instance, in October 2022, the United States Food and Drug Administration approved the Teclistamab-cqvy (Tecvayli), for the treatment of relapsed/refractory multiple myeloma.

- Therefore, the rising prevalence of cancer and increasing product launches are expected to drive the growth of the segment over the forecast period.

North America Holds Significant Market Share

- The North American infused drugs market is expected to grow over the forecast period owing to factors such as the rising prevalence of chronic diseases, such as cancer and infectious diseases, coupled with the increasing investment in research and development activities. Increasing strategic activities such as product launches and acquisitions by key players are also expected to drive the market in the region.

- The rising prevalence of chronic diseases such as cancer is expected to increase the demand for specialty therapeutics that are used in oncology. For instance, according to the American Cancer Society's updated data in 2023, the incidence of lung cancer is increasing in the United States, and the country reported 238,340 lung cancer cases in 2023 compared to 236,740 in 2022. Similarly, as per the Canadian Cancer Society's updated data from January 2024, it was estimated that in 2023, around 124,200 males and 114,900 females were diagnosed with cancer. Prostate cancer accounts for one-fifth (20%) of all new cancer cases in males in 2023. Hence, the significant prevalence of cancer cases in North America is projected to spur the demand for infused drugs.

- The increasing investments in research and development by governments and private organizations are also expected to drive the market in North America. For instance, in November 2023, the National Multiple Sclerosis Society invested USD 4.4 million in new research projects, aligning with the strategy to guide global MS research toward promising areas outlined in the Pathways to Cure's roadmap. Furthermore, in March 2023, in the United States, Bayer AG planned to invest USD 1.0 billion in the research and development of drugs. Such huge investments in research and development can lead to novel infusing product launches.

- Hence, the rising prevalence of cancer cases and increasing investments in research and development investments by governments and private organizations are expected to drive the market in North America over the forecast period.

Infused Drugs Industry Overview

The infused drugs market is moderately competitive. The key players are adopting various strategies such as product launches, expansion of the products and services into new regions, mergers, acquisitions, and entering new partnerships and collaborations to strengthen their position in the market. The key players include AstraZeneca, Sanofi SA, Teva Pharmaceutical Industries Ltd, Amgen, Inc., and Bristol-Myers Squibb Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in the Prevalence of Chronic Diseases

- 4.2.2 Increasing Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Side Effects Associated with the Medications

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Drug Type

- 5.1.1 Small Molecules

- 5.1.2 Biologics

- 5.2 By Therapeutic Area

- 5.2.1 Oncology

- 5.2.2 Gastrointestinal Diseases

- 5.2.3 Rheumatoid Arthritis

- 5.2.4 Immune Deficiencies

- 5.2.5 Cardiology

- 5.2.6 Neurology

- 5.2.7 Diabetes

- 5.2.8 Other Therapeutic Areas

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AstraZeneca

- 6.1.2 Sanofi SA

- 6.1.3 Pfizer Inc.

- 6.1.4 Weefsel Pharma

- 6.1.5 Parenteral Drugs (India) Limited

- 6.1.6 Bristol-Myers Squibb Company

- 6.1.7 Regeneron Pharmaceuticals Inc.

- 6.1.8 Eisai Co. Ltd

- 6.1.9 Amgen Inc.

- 6.1.10 Teva Pharmaceutical Industries Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日