|

市場調査レポート

商品コード

1521778

橈骨動脈圧迫デバイス:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Radial Artery Compression Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 橈骨動脈圧迫デバイス:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

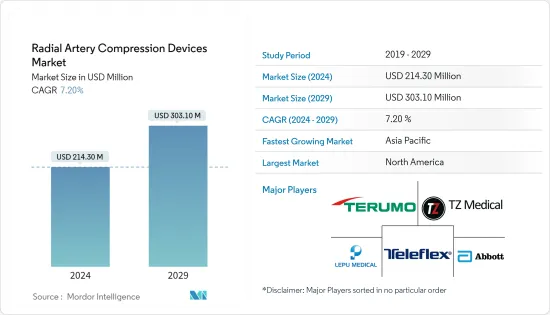

橈骨動脈圧迫デバイスの市場規模は、2024年に2億1,430万米ドルと推計され、2029年には3億310万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは7.20%で成長する見込みです。

橈骨動脈圧迫デバイスは、橈骨動脈アクセスを通じて行われる診断的処置またはインターベンション処置の後に、止血(出血を止めること)を達成し、橈骨動脈穿刺部位の圧力を維持します。これらの器具は、制御された圧迫を行い、橈骨動脈の密閉を確実にするよう特別に設計されています。手術件数の増加や革新的な製品の発売は、市場を牽引する要因のひとつです。

主なハイライト

- 末梢動脈疾患のような心血管疾患は世界の健康問題です。例えば、2023年11月にNational Center for Chronic Disease Prevention and Health Promotionが発表したデータによると、2022年には世界全体で推定5億2,300万人が心血管疾患(CVD)を抱えて生活しており、喫煙や飲酒などの様々なライフスタイルの変化により、今後数年間で増加すると予測されています。このように、心血管疾患患者の負担増は、心血管インターベンション中の橈骨動脈アクセス処置に伴う出血性合併症の軽減に役立つことから、橈骨動脈圧迫デバイスの需要を促進すると予想されます。

- さらに、橈骨動脈圧迫デバイスの需要が増加し続けているため、企業は世界中の患者の増加する要求に応えるために製造施設を設置することで、新製品開発や地理的拡大などのさまざまな戦略を採用しています。例えば、テルモ・メディカル・コーポレーションは2024年2月、プエルトリコのカグアスに新たな製造施設を開設し、同社の血管閉鎖装置Angio-Sealの需要増に対応するため生産を拡大しました。製造施設の拡張は製品量を押し上げ、市場で入手可能なデバイスの数を増加させる。これは、デバイスの需要の増加に対応し、市場を牽引すると期待されます。

- したがって、心血管疾患患者の継続的な増加と市場製品の様々な製造施設の拡大は、今後数年間の市場の成長を促進すると予測されます。しかし、国によって償還政策にばらつきがあることや、血腫のような身体のアクセス部位での潜在的な合併症は、予測期間中の市場成長を妨げると予想されるいくつかの要因です。

橈骨動脈圧迫デバイス市場の動向

外科手術への用途が大きく成長すると予測

- 橈骨動脈圧迫デバイスは、主に心臓カテーテル治療と関連しています。心臓カテーテル検査が増加するにつれて、橈骨動脈圧迫デバイスの利用は外科的介入で増加すると予想され、予測期間中の同分野の成長を後押しする可能性が高いです。

- 心臓病のような慢性疾患は、世界的に罹患率の重要な原因のひとつであり続けています。例えば、英国心臓財団が2024年3月に発表したデータによると、英国では2022年に約760万人が心臓病を患っています。これは心臓病の負担が大きいことを示しており、心臓カテーテル検査の需要を増加させ、それによって橈骨動脈圧迫デバイスの需要を増加させています。

- 外科的介入セグメントの成長は、心臓病にかかりやすく外科的介入を必要とする高齢者の世界の増加によって牽引されると予想されます。これにより、外科的介入における橈骨動脈圧迫デバイスの使用が増加します。United Nations World Population Prospects 2022が発表したデータによると、世界の老人人口は急速に増加しています。2022年には、65歳以上の高齢者は世界で7億7,100万人以上となり、世界人口の約9.3%を占める。また、2050年には65歳以上の人口は約15億人に達し、世界人口の約16.0%を占めると予測しています。このように、心血管疾患を抱える高齢化人口の増加は、外科的介入分野で今後数年間に大きな成長が見込まれる主な要因の一つです。

北米が大きな市場シェアを占めると予想される

- 北米は、心血管手術の症例数の増加、ヘルスケアインフラの開拓、新製品の発売、同地域における既存企業の存在などの要因により、市場で大きなシェアを占めると予想されます。

- 米国は、全国的に心臓血管外科手術の件数が増加しているため、同地域の市場を独占すると予測されています。例えば、Current Cardiology Reviewsが2023年5月に発表した論文によると、米国ではここ数年、経放射線心臓カテーテル治療(TRA)が大幅に増加しています。

- 米国では心臓移植の件数も増加しています。例えば、ロチェスター大学医療センター・ロチェスターは2024年1月、ストロング記念病院では2023年に40件の救命心臓移植手術が行われ、前年(2022年)より82%増加したと発表しました。さらに、シダーズ・サイナイが2022年1月に発表したデータによると、冠動脈バイパス移植手術(CABG)は、冠動脈バイパス手術またはバイパス手術とも呼ばれ、米国では依然として一般的な心臓外科手術であることが明らかになった。さらに、米国では毎年30万人以上がバイパス手術を受けています。したがって、橈骨圧迫装置は効果的な心臓手術において重要な役割を果たしています。

- さらに、この地域の主要企業による新製品の発売が市場を押し上げると予想されています。例えば、2022年3月、Medical Ingenuities社は、米国Lakewood Ranch Medical Centerにおいて、特許止血を達成するための革新的な橈骨止血バンドシステム、PH Bandによる商業的症例を実施しました。すべての症例が成功し、他の橈骨バンドと比較してPHバンド独自の利点が実証されました。したがって、外科的介入を必要とする心血管系疾患の負担が増加していることと、先進的な橈骨動脈圧迫デバイスの採用により、調査された市場は北米で大きく成長すると予想されます。

橈骨動脈圧迫デバイス産業の概要

橈骨動脈圧迫デバイス市場は、世界的および地域的に事業を展開する複数の企業の存在によって断片化されています。競合情勢には、市場シェアを握る国際企業や地域企業の分析が含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 心血管疾患の増加

- 橈骨動脈アクセスへの嗜好の高まり

- 市場抑制要因

- 償還政策のばらつき

- アクセス部位での合併症の可能性

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-金額)

- 製品別

- バンド/ストラップ型

- ノブベース

- プレートベース

- 用途別

- 交換可能デバイス

- 再利用可能デバイス

- 用途別

- 手術介入

- 診断

- エンドユーザー別

- 病院

- 外来手術センター

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Terumo Corporation

- Abbott

- Teleflex Incorporated

- Semler Technologies Inc.

- VYGON

- Merit Medical Systems

- Beijing Demax Medical Technology

- Forge Medical

- TZ Medical, Inc.

- Lepu Medical Technology(Beijing)Co. Ltd

- Advin Health Care

第7章 市場機会と今後の動向

The Radial Artery Compression Devices Market size is estimated at USD 214.30 million in 2024, and is expected to reach USD 303.10 million by 2029, growing at a CAGR of 7.20% during the forecast period (2024-2029).

Radial artery compression devices achieve hemostasis (stop bleeding) and maintain pressure at the radial artery puncture site following diagnostic or interventional procedures performed through radial artery access. These devices are specifically designed to provide controlled compression and ensure the seal of the radial artery. An increase in the number of surgeries and innovative product launches are some factors that drive the market.

Key Highlights

- Cardiovascular diseases, like peripheral artery disease, are global health concerns. For instance, as per the data published by the National Center for Chronic Disease Prevention and Health Promotion in November 2023, globally, an estimated 523 million were living with cardiovascular diseases (CVD) in 2022, and this is expected to increase over the coming years due to the various lifestyle changes such as smoking, alcohol consumption, etc. Thus, the rising burden of cardiovascular disease cases is expected to drive the demand for radial artery compression devices as the device helps reduce bleeding complications associated with radial artery access procedures during cardiovascular interventions.

- Furthermore, as the demand for radial artery compression devices continues to rise, companies are adopting different strategies, such as new product development and geographical expansion, by setting up manufacturing facilities to cater to the increasing requirements of patients worldwide. For instance, in February 2024, Terumo Medical Corporation opened a new manufacturing facility in Caguas, Puerto Rico, to expand production to meet the growing demand for the company's Angio-Seal vascular closure device. The expansion of the manufacturing facility boosts product volume, increasing the number of devices available in the market. This is expected to meet the growing requirement of the devices and drive the market.

- Therefore, the continuous increase in cardiovascular disease cases and the expansion of various manufacturing facilities of market products are projected to drive the market's growth over the coming years. However, variability in reimbursement policies across countries and potential complications at the body's access site, like hematoma, are some factors expected to hinder the market's growth during the forecast period.

Radial Artery Compression Devices Market Trends

Surgical Intervention Application is Expected to Have Significant Growth

- Radial artery compression devices are primarily associated with cardiac catheterization procedures. As the procedures of cardiac catheterization increase, the utilization of radial artery compression devices is expected to increase in surgical intervention, which is likely to boost the segment's growth over the forecast period.

- Chronic diseases like heart disease continue to be some of the significant causes of morbidity globally. For instance, as per the data published by the British Heart Foundation in March 2024, in the United Kingdom, around 7.6 million individuals suffered from heart disease in 2022. This shows the high burden of heart disease, which increases the demand for cardiac catheterization, thereby increasing the demand for radial artery compression devices.

- The surgical intervention segment's growth is expected to be driven by the rising number of elderly individuals worldwide, who are more susceptible to cardiac diseases and need surgical intervention. This increases the use of radial artery compression devices in the surgical intervention. According to the data published by the United Nations World Population Prospects 2022, the global geriatric population is rapidly increasing. In 2022, over 771.0 million individuals aged 65 years or older lived worldwide, accounting for approximately 9.3% of the global population. The report also predicts that by 2050, the population aged 65 years or older is likely to reach approximately 1.5 billion, representing around 16.0% of the global population. Thus, the increasing aging population with cardiovascular disease is one of the major factors that is expected to witness significant growth in the surgical intervention segment in the upcoming years.

North America is Expected to Hold Significant Market Share

- North America is expected to have a significant share of the market owing to factors such as increasing cases of cardiovascular surgeries, developed healthcare infrastructure, new product launches, and the presence of established players in the region.

- The United States is projected to dominate the market in the region due to the increasing number of cardiovascular surgeries nationwide. For instance, an article published by the Current Cardiology Reviews in May 2023 stated that trans-radial cardiac catheterization (TRA) witnessed a significant rise in the United States during the last few years.

- The number of heart transplants in the United States is also increasing. For instance, the University of Rochester Medical Center Rochester stated in January 2024 that the Strong Memorial Hospital had 40 life-saving heart transplantation surgeries in 2023, an 82% increase over the previous year (2022). Additionally, the data released by Cedars-Sinai in January 2022 revealed that coronary artery bypass graft surgery (CABG), alternatively referred to as coronary artery bypass or bypass surgery, remains the prevailing cardiac surgical procedure in the United States. Additionally, over 300,000 individuals in the United States undergo successful bypass surgery annually. Hence, radial compression devices play an important role in effective cardiac surgeries.

- Furthermore, new product launches by the key companies from the region are expected to boost the market. For instance, in March 2022, Medical Ingenuities conducted commercial cases with a transformational radial hemostasis band system, PH Band, to achieve patent hemostasis at Lakewood Ranch Medical Center, United States. All cases were successful and demonstrated the unique benefits of the PH Band compared to other radial bands. Hence, owing to the increasing burden of cardiovascular disease that requires surgical intervention and the adoption of advanced radial compression devices, the market studied is anticipated to grow significantly in North America.

Radial Artery Compression Devices Industry Overview

The radial artery compression devices market is fragmented due to the presence of several companies operating globally and regionally. The competitive landscape includes an analysis of a few international and local companies holding market shares. Some of the key market players include Terumo Corporation, Abbott, Teleflex Incorporated, Lepu Medical Technology (Beijing) Co. Ltd, and TZ Medical Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevelance of Cardiovascular Diseases

- 4.2.2 Growing Preference for Radial Artery Access

- 4.3 Market Restraints

- 4.3.1 Variability in Reimbursement Policies

- 4.3.2 Potential Complications at the Access Site

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product

- 5.1.1 Band/Strap Based

- 5.1.2 Knob-based

- 5.1.3 Plate-based

- 5.2 By Usage

- 5.2.1 Replaceable Device

- 5.2.2 Resuable Device

- 5.3 By Application

- 5.3.1 Surgical Intervention

- 5.3.2 Diagnostics

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Terumo Corporation

- 6.1.2 Abbott

- 6.1.3 Teleflex Incorporated

- 6.1.4 Semler Technologies Inc.

- 6.1.5 VYGON

- 6.1.6 Merit Medical Systems

- 6.1.7 Beijing Demax Medical Technology

- 6.1.8 Forge Medical

- 6.1.9 TZ Medical, Inc.

- 6.1.10 Lepu Medical Technology (Beijing) Co. Ltd

- 6.1.11 Advin Health Care