|

市場調査レポート

商品コード

1521711

無菌注射剤受託製造:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Sterile Injectable Contract Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 無菌注射剤受託製造:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

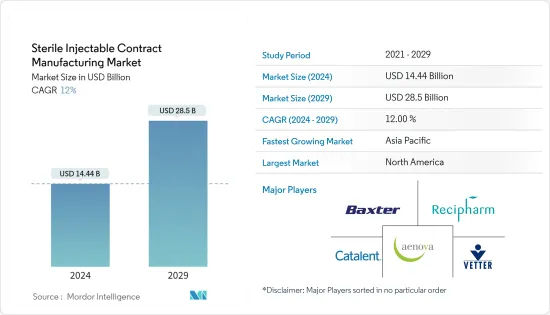

無菌注射剤受託製造の市場規模は2024年に144億4,000万米ドルと推定・予測され、2029年には285億米ドルに達し、予測期間中(2024~2029年)のCAGRは12%で成長すると予測されます。

注射薬のパイプラインの増加と承認が、無菌注射剤受託製造市場の大きな促進要因となっています。製薬会社は、作用発現の速さ、正確な投与、患者のコンプライアンス向上などの利点から注射剤の開発を進めています。例えば、2023年1月に発表されたFDAの報告書によると、CDERは2022年に、新薬承認申請(NDA)に基づく新規分子生物学的製剤(NME)として、または生物製剤承認申請(BLA)に基づく新規治療用生物学的製剤として、37の新規医薬品を承認しました。これらの医薬品には注射剤も含まれるため、強力なパイプラインによって商業目的および研究目的での受託製造の需要が増加し、市場の成長に寄与すると予想されます。

細胞治療や遺伝子治療に対する需要の急増は、市場の拡大を後押しします。これらの治療法のパイプラインが拡大するにつれて、製造受託機関(CMO)による専門的な製造能力へのニーズが高まっています。例えば、ClinicalTrials.govによると、2024年3月現在、北米では581以上の臨床試験が様々な疾患の治療に対する細胞療法や関連アプローチの可能性を調査しています。したがって、細胞ベースの治療法の臨床開発における研究量の多さが、予測期間中の製造受託を後押しすると予想されます。

さらに、無菌製造施設の拡張、提携、パートナーシップといった市場プレイヤーの戦略的活動が、予測期間中の市場成長に寄与するとみられます。例えば、2023年11月、プライベート・エクイティ企業であるNorthEdge社は、Torbay and Devon NHS Foundation Trust社からTorbay Pharmaceuticals社の無菌注射剤受託製造業者およびライセンス保有者を買収した後、国際的な成長の次の段階をサポートするために投資しました。2023年3月、PCIファーマサービスはイリノイ州ロックフォードの無菌注射剤製造拠点で5,000万米ドルの拡張計画を発表しました。このプロジェクトでは、20万平方フィートの施設を増設し、注射剤とデバイスの組み合わせ製品の生産能力を増強します。

したがって、製品パイプラインにおける細胞・遺伝子治療の需要の高まりと無菌製造施設の拡張が、予測期間中の市場成長を押し上げると予想されます。しかし、品質管理に関する課題や高い運用コストが市場の成長を抑制すると予想されます。

無菌注射剤受託製造市場の動向

がん領域が予測期間中に大きなシェアを占める見込み

がん治療には、薬剤の安定性と有効性を保証する綿密な製造技術が必要です。複雑な製剤や生物製剤の取り扱いに精通した無菌注射剤受託製造業者は、がん治療薬特有の課題に対応するのに有利な立場にあります。多くのがん治療には、複雑な生物製剤や新規の治療アプローチが含まれます。無菌注射剤は、このような高度な治療薬を送達するための信頼性が高く効果的な手段を提供し、無菌注射剤受託製造市場の拡大に貢献しています。

カナダがん協会(CCS)の2023年報告書では、カナダではがんが大きなヘルスケア負担となっており、その罹患率は着実に上昇していることが強調されています。従って、がんの高い負担は、同国において新たな無菌注射剤CMOの機会を生み出し、同分野の成長を牽引しています。同じ情報源によると、カナダでは2023年に239,100人のがん患者が報告されています。このように、がんの負担増は製造受託サービスの需要を創出し、同セグメントの成長に寄与すると予想されます。

アウトソーシングの堅調な伸びは、予測期間を通じてセグメントの拡大を促進すると予測されます。がん領域を含む製薬企業は、業務の合理化、コスト削減、製造委託先の専門的能力の活用を目的として、製造業務のアウトソーシングをますます進めています。こうした動向は、がん領域における無菌注射剤受託製造市場の成長に寄与しています。

したがって、がん罹患率の増加とアウトソーシングの増加傾向は、予測期間中の同分野の成長を後押しすると予想されます。

予測期間中、北米が大きな市場シェアを占める見込み

北米では、受託製造施設の設立、慢性疾患の増加、高度な生物製剤の開発により、無菌注射剤受託製造市場の成長が見込まれています。無菌注射剤は複雑な治療を提供するために不可欠であり、受託製造はこの需要を満たすための拡張性のあるソリューションを提供します。

無菌注射製剤を必要とすることが多い生物製剤やバイオシミラーが重視されるようになっていることが、受託製造市場の成長に大きく寄与しています。例えば、2023年3月に発表された食品医薬品局の報告書によると、2022年には15の生物製剤が承認され、このうち6つは多様ながんの治療に適応があった。予測される生物製剤の承認急増は、予測期間中の市場成長を後押しすると予測されます。

製造施設の拡張、提携、パートナーシップ、買収といった市場参入企業による戦略的活動は、予測期間中の市場成長を押し上げると予想されます。例えば、シャープは2023年10月、臨床用および商業用の無菌注射剤を提供するマサチューセッツ州の開発・製造受託機関(CDMO)であるBerkshire Sterile Manufacturing(BSM)を買収しました。さらに2022年3月、サンド・カナダはケベック州ブーシェビルの製造工場をCMOのデルファームに売却完了を発表しました。この工場はカナダ最大の無菌注射剤製造施設であり、カナダと米国のヘルスケアシステム(主に病院)に戦略的で命を救う可能性のある医薬品を提供しています。

このように、この地域のCMOとの提携やCMOへの製造委託は、市場全体の成長に寄与しています。

無菌注射剤受託製造業界の概要

無菌注射剤受託製造市場は統合されており、少数の大手企業で構成されています。市場シェアでは、現在特定の大手企業が市場を独占しています。市場競争力を維持するため、市場参入企業は製造施設の拡大、提携、提携など様々な戦略を採用しています。現在市場を独占している企業には、バクスター、Catalent Inc.、Vetter Pharma、Recipharm AB、Aenova Groupなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 注射剤のパイプラインと承認の増加

- 生物製剤とバイオシミラーの需要拡大

- 新規治療薬開発のための研究開発投資の増加

- 市場抑制要因

- 品質管理に関する課題

- 高い運用コスト

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-金額)

- 分子タイプ別

- 低分子

- 大型分子

- 治療領域別

- がん

- 糖尿病

- 心血管疾患

- 中枢神経系疾患

- 感染症

- 筋骨格系

- 抗ウイルス

- その他

- 投与経路別

- 皮下(SC)

- 静脈内投与

- 筋肉内(IM)

- その他

- エンドユーザー別

- 製薬会社およびバイオ製薬会社

- 研究機関

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- その他欧州

- アジア太平洋

- インド

- 日本

- 中国

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Baxter

- Catalent Inc.

- Vetter Pharma

- Recipharm AB

- Aenova Group

- Fresenius Kabi

- Unither Pharmaceuticals

- Famar

- Cipla Inc.

- NextPharma Technologies

第7章 市場機会と今後の動向

The Sterile Injectable Contract Manufacturing Market size is estimated at USD 14.44 billion in 2024, and is expected to reach USD 28.5 billion by 2029, growing at a CAGR of 12% during the forecast period (2024-2029).

The increasing pipeline and approvals of injectable drugs are significant drivers of the sterile injectable contract manufacturing market. Pharmaceutical companies are developing injectable drugs due to their advantages, including faster onset of action, precise dosing, and improved patient compliance. For instance, according to the FDA report published in January 2023, CDER approved 37 novel drugs, either as new molecular entities (NMEs) under New Drug Applications (NDAs) or as new therapeutic biological products under Biologics License Applications (BLAs) in 2022. These drugs include injectables, and hence, a strong pipeline is expected to increase the demand for contract manufacturing for commercial and research purposes, thereby contributing to market growth.

The burgeoning demand for cellular and genetic treatments propels the expansion of the market. As the pipeline of these therapies expands, there is a growing need for specialized manufacturing capabilities, which contract manufacturing organizations (CMOs). For instance, according to ClinicalTrials.gov, as of March 2024, more than 581 clinical trials were investigating the potential of cell therapies and related approaches for treating various diseases in North America. Therefore, the high amount of research in clinical development for cell-based therapy is expected to boost contract manufacturing over the forecast period.

Moreover, strategic activities by the market players, such as the expansion of sterile manufacturing facilities, collaboration, and partnership, are expected to contribute to the market growth over the forecast period. For instance, in November 2023, private equity firm NorthEdge invested in a Torbay Pharmaceuticals sterile injectable contract manufacturer and license holder to support its next phase of international growth after acquiring it from Torbay and Devon NHS Foundation Trust. In March 2023, PCI Pharma Services unveiled plans for a USD 50 million expansion at its Rockford, Illinois, sterile injectables site. The project will add a 200,000-square-foot facility to boost the plant's capacity for injectable drug-device combination products.

Hence, the growing demand for cell and gene therapy in the product pipeline and the expansion of sterile manufacturing facilities are expected to boost market growth over the forecast period. However, challenges related to quality control and high operational costs are anticipated to restrain the market's growth.

Sterile Injectable Contract Manufacturing Market Trends

The Cancer Segment is Expected to Hold a Significant Share Over the Forecast Period

Cancer therapies necessitate meticulous manufacturing techniques that guarantee drug stability and effectiveness. Sterile injectable contract manufacturers with expertise in handling complex formulations and biologics are well-positioned to meet the unique challenges of oncology drugs. Many cancer treatments involve complex biologics and novel therapeutic approaches. Sterile injectables provide a reliable and effective means of delivering these advanced therapies, contributing to the expansion of the sterile injectable contract manufacturing market.

The Canadian Cancer Society's (CCS) 2023 report highlighted that cancer poses a significant healthcare burden in Canada, with its incidence steadily rising. Thus, the high burden of cancer is creating opportunities for new sterile injectables CMO in the country, driving the segment's growth. The same source stated that 239,100 cancer cases were reported in Canada in 2023. Thus, the growing burden of cancer is expected to create demand for contract manufacturing services, likely contributing to segmental growth.

The robust growth in outsourcing practices is projected to fuel segment expansion throughout the forecast period. Pharmaceutical companies, including those focused on oncology, are increasingly outsourcing manufacturing activities to streamline operations, reduce costs, and leverage the specialized capabilities of contract manufacturers. This trend has contributed to the growth of the sterile injectable contract manufacturing market within the cancer segment.

Hence, growing cancer prevalence and the increasing trend of outsourcing are expected to boost the segment's growth over the forecast period.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

In North America, the sterile injectable contract manufacturing market is expected to grow due to the establishment of contract manufacturing facilities, the rise in chronic diseases, and the development of advanced biologics. Sterile injectables are crucial for delivering complex therapies, and contract manufacturing provides a scalable solution for meeting this demand.

The increasing emphasis on biologics and biosimilars, which often require sterile injectable formulations, contributes significantly to the growth of the contract manufacturing market. For instance, according to a report by the Food and Drug Administration published in March 2023, 15 biologics were approved in 2022; of this, six were indicated for the treatment of a diversity of cancers. An anticipated surge in biologics drug approvals is projected to boost market growth during the forecast period.

Strategic activities by the market players, such as manufacturing facility expansion, collaboration, partnerships, and acquisitions, are expected to boost the market's growth over the forecast period. For instance, in October 2023, Sharp acquired Berkshire Sterile Manufacturing (BSM), a contract development and manufacturing organization (CDMO) in Massachusetts that offers clinical and commercial sterile injectable products. Additionally, in March 2022, Sandoz Canada announced the completion of the sale of its Boucherville, Quebec, manufacturing plant to Delpharm, a CMO. This plant is Canada's largest sterile injectable production facility and provides strategic and potentially lifesaving medicines to the Canadian and US healthcare systems, primarily hospitals.

Thus, collaborations with or outsourcing manufacturing to CMOs in the region contribute to the overall growth of the market.

Sterile Injectable Contract Manufacturing Industry Overview

The sterile injectable contract manufacturing market is consolidated and consists of a few major players. In terms of market share, certain major players currently dominate the market. Market players adopt various strategies such as expanding manufacturing facilities, collaborating, and partnering to stay competitive. Some of the companies currently dominating the market are Baxter, Catalent Inc., Vetter Pharma, Recipharm AB, and Aenova Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Pipeline and Approvals of Injectables

- 4.2.2 Growing Demand for Biologics and Biosimilars

- 4.2.3 Rise in Investment Across Research and Development Activities for the Development of Novel Therapeutics.

- 4.3 Market Restraints

- 4.3.1 Challenges Related to Quality Control

- 4.3.2 High Operational Costs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Molecule Type

- 5.1.1 Small Molecule

- 5.1.2 Large Molecule

- 5.2 By Therapeutic Area

- 5.2.1 Cancer

- 5.2.2 Diabetes

- 5.2.3 Cardiovascular Diseases

- 5.2.4 Central Nervous System Diseases

- 5.2.5 Infectious Disorders

- 5.2.6 Musculoskeletal

- 5.2.7 Anti-viral

- 5.2.8 Others

- 5.3 By Route of Administration

- 5.3.1 Subcutaneous (SC)

- 5.3.2 Intravenous (IV)

- 5.3.3 Intramuscular (IM)

- 5.3.4 Others

- 5.4 End User

- 5.4.1 Pharmaceutical and Biopharmaceutical Companies

- 5.4.2 Research Institutes

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Italy

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 Japan

- 5.5.3.3 China

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of the Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Baxter

- 6.1.2 Catalent Inc.

- 6.1.3 Vetter Pharma

- 6.1.4 Recipharm AB

- 6.1.5 Aenova Group

- 6.1.6 Fresenius Kabi

- 6.1.7 Unither Pharmaceuticals

- 6.1.8 Famar

- 6.1.9 Cipla Inc.

- 6.1.10 NextPharma Technologies