バイオアセトン:市場シェア分析、産業動向、成長予測(2024~2029年)

Bio-Acetone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1521709

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

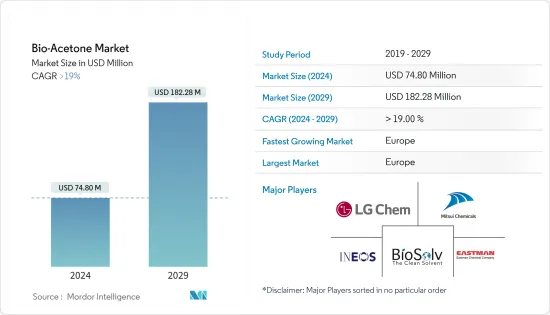

バイオアセトン市場規模は、2024年に7,480万米ドルと推定・予測され、2029年には1億8,228万米ドルに達し、予測期間中(2024~2029年)のCAGRは19%以上で成長すると予測されます。

COVID-19のパンデミックは、各国による閉鎖や制限により市場の需要にマイナスの影響を与えました。しかし、市場は2021年に回復し、2022年と2023年には様々な産業での用途の増加によりパンデミック以前の水準に戻った。

短期的には、バイオアセトンの需要は、塗料やコーティング剤など様々な産業からのバイオベース製品の需要によって促進されます。

逆に、様々な代替品が入手可能であることが、今後の市場成長の妨げになると予想されます。

バイオベース製品を製造する技術の増加は、予測期間中にバイオアセトン市場に機会を創出すると予想されます。

バイオアセトン市場動向

バイオベースの塗料とコーティングの需要拡大

- バイオアセトンは、通常のアセトンの再生可能なバージョンであり、アセトンと同じ化学的特性を持っています。

バイオアセトンの利点は以下の通り:

- 安全で発がん性はありません。高性能溶剤であり、様々な塗料やコーティング剤に使用できます。

- 再生可能な資源から作られており、生物分解性があります。ポリウレタン塗料、UV硬化塗料、エナメル、ワニスに有効です。

- 塗料やコーティング剤の製造ではシンナーとして使用されます。塗料やコーティング剤は、自動車、建築、包装、家具、繊維など様々な用途で使用されています。

- 多くの産業が揮発性有機化合物(VOC)の低い製品を使い始めており、VOC規制の強化が最近の市場の需要増加につながっています。バイオアセトンはトウモロコシなどの植物由来の原料から製造されるため、バイオ溶剤は主に低VOCベースの塗料やコーティング製品に使用されています。

- 自動車産業では、様々なVOC規制のためにバイオベースの塗料への需要が増加しています。バイオアセトンはバイオベースコーティングの溶剤として使用され、ダッシュボード、ステアリングホイール、ドアトリム、その他の自動車など様々な用途に適用されます。

OICA(International Organization Of Motor Vehicle Manufacturers:国際自動車工業会)が発表した最新データによると、2021年に8,000万台だった自動車の総生産台数は、2022年には約8,500万台となりました。

- また、各国で電気自動車の製造が増加しており、自動車産業におけるバイオベースコーティングの需要をさらに押し上げています。

- 各国のVOC規制の高まりにより、バイオベースの塗料とコーティング剤の需要は増加傾向にあり、予測期間中の市場需要にプラスの影響を与えると予想されます。

欧州が最大の消費者に

- 欧州は、再生可能ベースの製品に関する様々な規制により、バイオアセトンの最大消費国の一つになると予想されます。

- 塗料産業から排出されるVOCは、様々な環境問題や人体の健康問題を引き起こしています。このため、様々な国がコーティング産業において欧州連合が定めた指令に従うようになりました。

- 欧州連合(EU)は、塗料・コーティング産業を含む産業活動から排出されるVOCを削減するため、VOC溶剤排出指令(SED)の実施を開始しました。

- SEDはVOCの排出規制値を定め、塗料やコーティング剤製造などの業界に対し、製造工程で低VOCまたはゼロVOCベースの溶剤を使用するよう求めています。

- 化粧品業界では、バイオアセトンはアセトンに比べて優れた特性を持ち、毒性が低いため、マニキュアの除光液として使用されています。

- パーソナルケア協会のコスメティクス・欧州によると、化粧品業界の2022年の市場規模は880億ユーロ(約949億米ドル)です。

- この地域で最大の化粧品市場は、ドイツ、フランス、イタリア、英国、ポーランドです。これらすべての国が、この地域の化粧品市場全体の67%以上を占めています。

- これら全ての要因が、予測期間中に欧州各国におけるバイオアセトンの需要を促進すると予想されます。

バイオアセトン産業概要

世界のバイオアセトン市場は統合されています。主要参入企業(順不同)には、LG Chem、Mitsui Chemicals、INEOS、Bio Brands LLC、Eastman Chemical Companyなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブ概要

第4章 市場力学

- 促進要因

- 様々な産業用途におけるバイオベース原料の需要拡大

- VOC規制の増加

- その他の促進要因

- 抑制要因

- 代替品の入手可能性

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(金額ベース))

- 種類

- 純度99%以下

- 純度99以上

- 用途

- プラスチック

- ゴム

- 塗装

- その他(除光液、洗浄剤、化学中間体など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- トルコ

- ロシア

- 北欧諸国

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア**/ランキング分析

- Stratergies Adopted by Leading players

- 企業プロファイル

- INEOS

- Bio Brands LLC

- Celtic Renewables

- Circular Industries

- Eastman Chemcial Company

- LanzaTech

- LG Chem

- Mitsui Chemcials

- Sigma Aldrich(Merck KGaA)

- Vertec BioSolvents Inc.

第7章 市場機会と今後の動向

- バイオベースのアセトン製造技術の増加

- その他の機会

目次

The Bio-Acetone Market size is estimated at USD 74.80 million in 2024, and is expected to reach USD 182.28 million by 2029, growing at a CAGR of greater than 19% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted demand in the market due to lockdowns and restrictions imposed by various countries. However, the market recovered in 2021 and returned to pre-pandemic levels in 2022 and 2023 with the rise in applications in various industries.

Over the short term, the demand for bio-acetones is propelled by the demand for bio-based products from various industries, such as paints and coatings.

Conversely, the availability of various alternatives is expected to hinder the market's growth in the future.

The increasing technology for producing bio-based products is expected to create opportunities for the bio-acetone market during the forecast period.

Bio-Acetone Market Trends

Growing Demand For Bio-Based Paints and Coatings

- Bio-acetone is a renewable version of regular acetone and has the same characteristics as acetone with identical chemical properties.

Some of the advantages of bio-acetones include:

- They are safe and non-carcinogenic. They are high-performance solvents and can be used in various paints and coatings.

- They are made of renewable sources and are bio-degradable. They are effective in polyurethane paints, UV-curable coatings, enamels, and varnishes.

- They are used as thinners in paints and coatings manufacturing. Paints and coatings are used in various applications, including automotive, construction, packaging, furniture, textiles, and other applications.

- Many industries have started using products with low volatile organic compounds (VOC), and the increase in VOC regulations has led to a rise in demand in the market in recent times. Since bio-acetones are manufactured from plant-based raw materials such as corn, bio-solvents are used mainly in lower VOC-based paints and coating products.

- In the automotive industry, the demand for bio-based coatings is increasing owing to various VOC regulations. Bio acetone is used as a solvent in bio-based coatings and is applied to various applications such as dashboards, steering wheels, door trims, and other automotive vehicles.

According to the latest data released by the International Organization Of Motor Vehicle Manufacturers (OICA), the total number of vehicles manufactured in 2022 was around 85 million units compared to 80 million in 2021.

- In addition, there has been a rise in electric vehicle manufacturing in various countries, further propelling the demand for bio-based coatings in the automotive industry.

- Due to the rise in VOC regulations in various countries, the demand for bio-based paints and coatings is on the rise, which is expected to positively impact the demand in the market during the forecast period.

Europe To Become the Largest Consumer

- Europe is expected to be one of the largest consumers of bio-acetone due to various regulations set up for renewable-based products.

- The VOC emission from the coatings industry has raised various environmental and human health issues. This has led various countries to follow the directives laid by the European Union in the coatings industry.

- The European Union has started the implementation of the VOC solvents emission directive (SED) to reduce VOC emissions from industrial activities, including the paints and coatings industry.

- The SED has set up emission limits for VOCs and requires industries such as paints and coatings manufacturing to use low-VOC or zero-VOC-based solvents in the manufacturing process.

- In the cosmetics industry, bio-acetone is used as a nail polish remover owing to its superior characteristics and low toxicity compared to acetones.

- According to Cosmetics Europe, the personal care association, the cosmetics industry was valued at EUR 88 billion (~USD 94.9 billion) in 2022.

- The largest cosmetics markets in the region are Germany, France, Italy, the United Kingdom, and Poland. All these countries account for more than 67% of the total cosmetics market in the region.

- All these factors are expected to drive the demand for bio-acetones in various European countries during the forecast period.

Bio-Acetone Industry Overview

The global bio-acetone market is consolidated. Some major players (not in any particular order) include LG Chem, Mitsui Chemicals, INEOS, Bio Brands LLC, and Eastman Chemical Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Bio Based Raw Materials in Various Industrial Applications

- 4.1.2 Increase in VOC Regulations

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Availability of Alternatives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 Type

- 5.1.1 Purity <99%

- 5.1.2 Purity >99%

- 5.2 Application

- 5.2.1 Plastics

- 5.2.2 Rubber

- 5.2.3 Painting

- 5.2.4 Other Applications (Nail Polish Remover, Cleaning Agent, Chemicals Intermediaries, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Nigeria

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market share**/Ranking Analysis

- 6.3 Stratergies Adopted by Leading players

- 6.4 Company Profiles

- 6.4.1 INEOS

- 6.4.2 Bio Brands LLC

- 6.4.3 Celtic Renewables

- 6.4.4 Circular Industries

- 6.4.5 Eastman Chemcial Company

- 6.4.6 LanzaTech

- 6.4.7 LG Chem

- 6.4.8 Mitsui Chemcials

- 6.4.9 Sigma Aldrich (Merck KGaA)

- 6.4.10 Vertec BioSolvents Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Technologies for Bio Based Acetone Production

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日