|

市場調査レポート

商品コード

1521701

コラーゲン創傷被覆材:市場シェア分析、産業動向&統計、成長予測(2024~2029年)Collagen Dressings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| コラーゲン創傷被覆材:市場シェア分析、産業動向&統計、成長予測(2024~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

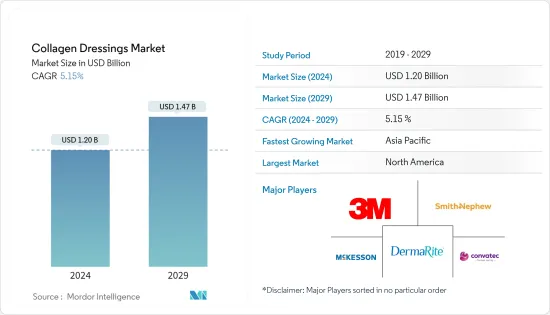

コラーゲン創傷被覆材の市場規模は2024年に12億米ドルと推定され、2029年には14億7,000万米ドルに達すると予測され、予測期間中(2024-2029年)にCAGR 5.15%で成長する見込みです。

コラーゲン創傷被覆材の需要を牽引しているのは、急性・慢性創傷の増加や世界の外科手術の増加です。例えば、2023年7月にNational Center for Biotechnology Informationに掲載された記事によると、世界中で年間約1,860万人が糖尿病性足潰瘍に罹患しており、米国では160万人が罹患しています。2023年5月に更新されたInterburns Organizationの記事によると、毎年約1,100万人が熱傷に罹患しています。このような創傷の高い有病率は、効果的な治療オプションの必要性を促し、それによって市場の成長を促進しています。

コラーゲン創傷被覆材は、熱傷、ただれ、糖尿病性潰瘍、静脈性潰瘍、褥瘡などの潰瘍を管理する上で極めて重要です。世界の糖尿病患者数の増加により、糖尿病性足潰瘍の患者は世界的に増加しています。例えば、2022年6月に更新された米国疾病予防管理センター(Centers for Disease Control and Prevention)の報告書によると、糖尿病患者の12.0%が生涯を通じて糖尿病性足潰瘍を発症しています。多くのヘルスケア専門家が糖尿病性足潰瘍を治癒するためにコラーゲン創傷被覆材を使用しており、これが今後数年間のコラーゲン創傷被覆材市場の需要をさらに促進すると予想されます。

さらに、高齢者人口の増加により、静脈性下腿潰瘍を患う患者数が増加すると予想され、コラーゲン・ドレッシング市場の促進が期待されています。例えば、2022年11月にJournal of Vascular Surgeryに掲載された調査研究によると、静脈性下腿潰瘍は人口の1.0%~2.0%が罹患しており、65歳以上では有病率が4.0%増加しています。さらに、スコットランドのNational Health Information Serviceによる2023年2月の更新によると、静脈性下腿潰瘍は英国でほぼ500人に1人が罹患すると予測されており、その割合は年齢とともに増加すると予測されています。同調査では、2022年には80歳以上の50人に1人が静脈性下腿潰瘍に罹患すると述べています。したがって、これらの要因がコラーゲン創傷被覆材の需要を増加させ、市場成長に影響を与えています。

政府のイニシアチブの高まりと慢性創傷に対する安全な治療オプションに対する需要の増加は、今後5年間に市場に数多くの成長機会をもたらす可能性があります。しかし、フォームドレッシングやハイドロコロイドドレッシングのようなコラーゲン創傷被覆材の代替治療オプションへの高いアクセシビリティと、従来の創傷被覆材と比較した高コストが、予測期間中の市場成長を抑制する可能性があります。

コラーゲン創傷被覆材市場の動向

牛用セグメントが予測期間中に著しい成長を遂げる見込み

- 牛コラーゲン創傷被覆材は、牛由来のゲル、パウダー、シートです。創傷治癒プロセスにおいて重要な役割を果たします。ほとんどのコラーゲン創傷被覆材製品が牛由来であるため、牛コラーゲン創傷被覆材セグメントは予測期間中に急成長すると予測されています。ジェル、パウダー、シートが最も一般的な牛コラーゲン創傷被覆材材です。さらに、これらは褥瘡、糖尿病性潰瘍、静脈性潰瘍、擦り傷、外傷性創傷、火傷、剥離した外科的創傷の創傷被覆管理に日常的に使用されています。したがって、このような創傷の症例の増加が、この分野の成長を促進すると予測されます。

- 2023年に更新された褥瘡治療のための労働安全衛生ガイドラインによると、米国では年間250万人以上が褥瘡を発症しています。さらに、高齢者が褥瘡を発症するリスクが高いことも報告されています。さらに、世界の外科手術の増加は、手術中の傷を治すために牛コラーゲン創傷被覆材材が使用されることから、セグメントの成長に大きく影響しています。例えば、国際美容整形外科学会(ISAPS)が2022年に実施した年次世界調査によると、2022年には世界中で1,490万件以上の外科手術が行われました。したがって、この分野は手術件数の多さから成長する可能性が高いです。

- さらに、新製品の発売と牛コラーゲン創傷被覆材セグメントで事業を展開する大手企業の存在は、製品の入手可能性と需要を増加させる。さらに、主要企業による戦略的な取り組みにより、市場製品の販売促進が行われ、会議の手配や展示会への参加により、その他の特典に関する認知度が向上し、セグメントの成長を後押ししています。例えば、2023年7月、FORYOU MEDICALは2023 Florida International Medical Expo展示会でLUOFUCON Collagen Dressing、LUOFUCON Silver Wound Gel、LUOFUCON Extra Silver Gelling Fiber Dressingなどの新製品を発表しました。このような取り組みは、コラーゲン創傷被覆材の用途を強調し、セグメントの成長に影響を与えています。

- したがって、人口の間で急性および慢性創傷の発生率が上昇していること、世界的に外科手術の数が増加していること、新製品の発売などの要因が予測期間中のセグメントの成長に寄与しています。

北米が予測期間中に大きなシェアを占める見込み

- 北米は、企業によるコラーゲン創傷被覆材の市場開拓と承認の増加により、コラーゲン創傷被覆材市場で大きなシェアを占めています。例えば、2022年6月、コラーゲン・マトリックス社(リジェニティ)は、新しいフィブリル・コラーゲン創傷被覆材の510(k)認可を取得しました。フィブリラーコラーゲン創傷被覆材は、創傷治療や軽度の出血抑制に使用される吸収性ミクロフィブリルマトリックスです。良好な規制環境、堅調なヘルスケアセクター、医療費支出が、この地域における市場の成長をさらに後押ししています。

- さらに、同地域における火傷、糖尿病、外科手術の有病率の上昇が主に市場を牽引しています。例えば、カナダ糖尿病協会が発表した記事によると、2023年7月、カナダでは1,190万人以上が糖尿病を患っています。このような糖尿病の例は、糖尿病性足潰瘍や手術部位感染につながります。コラーゲン創傷被覆材は、手術部位感染症に広く使用されています。従って、糖尿病患者の大幅な増加は、手術部位感染を増加させ、コラーゲン・ドレッシングの需要に貢献し、市場の成長を促進すると考えられます。

- 競合の存在、強力な製品ポートフォリオ、提携、買収、合併は、この地域における市場の成長を後押しします。例えば、2023年8月、慢性創傷およびスキンケア市場における臨床転帰の改善に焦点を当てた医療技術企業であるSanara MedTech Inc.は、Applied Nutritionals LLCからコラーゲン製品に属する特定の資産を買収しました。この買収により、同社の製品ポートフォリオと地理的プレゼンスが拡大しました。したがって、手術部位感染症の蔓延の増加、強力な製品ポートフォリオ、共同研究、買収、合併に向けた主要プレイヤーの焦点の増加が、この地域での市場研究を後押しすると予測されます。

コラーゲン創傷被覆材産業の概要

コラーゲン創傷被覆材市場は、主要企業の強力な製品ポートフォリオと強固な販売網により断片化されています。有力企業は研究開発活動に多額の投資を行い、新製品の発売につなげています。さらに、M&Aによるパートナーシップの形成、政府認可の確保、協力関係の促進など、さまざまな成長戦略の実施に注力することで、市場での存在感を高めています。主な市場参入企業は、3M、Smith+Nephew、DermaRite Industries, LLC、Coloplast Corp.、McKesson Medical-Surgical Inc.、Convatec Group PLC、Organogenesis Inc.などです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 人口における急性創傷および慢性創傷の発生率の増加

- コラーゲン創傷被覆材製品の研究開発活動と技術的進歩

- 世界の外科手術件数の増加

- 市場抑制要因

- コラーゲン創傷被覆材材の代替治療オプションの利用可能性

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-金額)

- 由来別

- 牛

- 豚

- その他の由来

- 形態別

- ゲル

- パウダー

- シート

- その他の形態

- 用途別

- 急性創傷

- 慢性創傷

- エンドユーザー別

- 病院および診療所

- 外来手術センター

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- 3M

- Smith+Nephew

- HARTMANN USA Inc.

- SANARA MEDTECH INC.

- DermaRite Industries LLC

- L&R Group

- Coloplast Corp.

- McKesson Medical-Surgical Inc.

- Convatec Group PLC

- DeRoyal Industries Inc.

- Hollister Incorporated

- Organogenesis Inc.

第7章 市場機会と今後の動向

The Collagen Dressings Market size is estimated at USD 1.20 billion in 2024, and is expected to reach USD 1.47 billion by 2029, growing at a CAGR of 5.15% during the forecast period (2024-2029).

The rising cases of acute and chronic wounds among individuals and a growing number of surgical procedures worldwide mainly drive the demand for collagen dressings. For instance, according to an article published in the National Center for Biotechnology Information in July 2023, around 18.6 million people worldwide are affected by diabetic foot ulcers yearly, including 1.6 million people in the United States. As per the updated article in May 2023 by Interburns Organization, around 11.0 million people are affected with burns each year. Such a high prevalence of wounds drives the need for effective treatment options, thereby propelling market growth.

Collagen dressings are crucial in managing burns, sores, and ulcers such as diabetic, venous, and pressure ulcers. The cases of diabetic foot ulcer patients are increasing globally owing to the rise in the number of diabetic patients worldwide. For instance, as per the Centers for Disease Control and Prevention report, updated in June 2022, 12.0% of people who have diabetes develop diabetic foot ulcers over their lifetime. Many healthcare professionals use collagen dressing to heal diabetic foot ulcers, which is further anticipated to drive the demand for collagen dressings market in the coming years.

Furthermore, the rise in the elderly population is expected to increase the number of patients suffering from venous leg ulcers, which is anticipated to propel the market for collagen dressings. For instance, according to a research study published in the Journal of Vascular Surgery in November 2022, venous leg ulcers affect 1.0% to 2.0% of the population, with the prevalence increasing by 4.0% for those aged more than 65 years. Additionally, as per the update in February 2023 by Scotland's National Health Information Service, venous leg ulcers are anticipated to affect nearly one in 500 people in the United Kingdom, and the rate is projected to increase with age. The same study stated that one in 50 people over 80 years old were affected with venous leg ulcers in 2022. Thus, these factors have increased the demand for collagen dressings, influencing market growth.

A rise in government initiatives and increased demand for safe treatment options for chronic wounds can create numerous growth opportunities for the market in the next five years. However, the high accessibility to alternative treatment options for collagen dressings, such as foam and hydrocolloid dressings, and the high cost compared to conventional wound dressings may restrain market growth during the forecast period.

Collagen Dressings Market Trends

Bovine Segment is Expected to Witness Significant Growth During the Forecast Period

- Bovine collagen dressings are gels, powders, and sheets derived from bovine. They play a crucial role in the wound-healing process. The bovine collagen dressings segment is projected to experience rapid growth over the forecast period as most collagen dressings products are derived from bovine. Gels, powder, and sheets are the most common bovine collagen dressings. Furthermore, these are used routinely to manage wound dressings for pressure ulcers, diabetic ulcers, venous ulcers, abrasions, traumatic wounds, burns, and dehisced surgical wounds. Hence, increasing cases of such wounds are projected to drive segmental growth.

- According to the Work Health and Safety guidelines for treating pressure ulcers, updated in 2023, more than 2.5 million people in the United States develop pressure ulcers yearly. Further, it also reported that older adults are at high risk of developing pressure ulcers. Additionally, the growing number of surgical procedures worldwide greatly influences segmental growth as bovine collagen dressings are used to heal wounds during surgeries. For instance, the annual global survey conducted by the International Society of Aesthetic Plastic Surgery (ISAPS) in 2022 stated that more than 14.9 million surgical procedures were performed worldwide in 2022. Hence, the segment is likely to grow owing to the high number of surgical procedures.

- Furthermore, new product launches and the presence of major players operating in the bovine collagen dressings segment increase the availability and demand of the product. In addition, strategic initiatives by key players to promote their market products and raise awareness about their benefits by arranging conferences and attending exhibitions boost segmental growth. For instance, in July 2023, FORYOU MEDICAL launched its new products, such as LUOFUCON Collagen Dressing, LUOFUCON Silver Wound Gel, and LUOFUCON Extra Silver Gelling Fiber Dressing in the 2023 Florida International Medical Expo exhibition. Such initiatives highlight the applications of collagen dressings, influencing segmental growth.

- Hence, factors such as the rising incidence of acute and chronic wounds among the population, the growing number of surgical procedures worldwide, and new product launches contribute to the segment's growth during the forecast period.

North America is Expected to Hold a Significant Share During the Forecast Period

- North America accounts for a major share of the collagen dressings market, owing to the increased developments and approvals for collagen dressings by companies. For instance, in June 2022, Collagen Matrix Inc. (Regenity) received 510(k) clearance for its new fibrillar collagen wound dressing. The fibrillar collagen wound dressing is an absorbent microfibrillar matrix used to treat wounds and control mild bleeding. The favorable regulatory environment, robust healthcare sector, and medicare spending are further driving the market's growth in the region.

- Furthermore, the market is mainly driven by a rise in the prevalence of burns, diabetes, and surgeries in the region. For instance, according to an article published by the Canadian Diabetes Association, in July 2023, more than 11.9 million people in Canada suffered from diabetes. Such instances of diabetes lead to diabetic foot ulcers and surgical site infections. Collagen dressing is widely used in cases of surgical site infection. Thus, significant high cases of diabetes are likely to increase surgical site infections and contribute to the demand for collagen dressings, thereby propelling the market's growth.

- The presence of competition, strong product portfolios, collaborations, acquisitions, and mergers boost the market's growth in the region. For instance, in August 2023, Sanara MedTech Inc., a medical technology company focused on improving clinical outcomes in chronic wound and skincare markets, acquired certain assets belonging to collagen products from Applied Nutritionals LLC. The acquisition expanded its product portfolio and geographical presence. Hence, the growing prevalence of surgical site infections, strong product portfolios, and increasing focus of key players toward collaborations, acquisitions, and mergers are projected to boost the market studied in the region.

Collagen Dressings Industry Overview

The collagen dressings market is fragmented due to a strong product portfolio and robust distribution network of major players. Prominent players invest significantly in research and development activities, leading to new product launches. Furthermore, focusing on implementing various growth strategies such as forming partnerships through mergers and acquisitions, securing government approvals, and fostering collaborations are expanding their presence in the market. Some key market players are 3M, Smith+Nephew, DermaRite Industries, LLC, Coloplast Corp., McKesson Medical-Surgical Inc., Convatec Group PLC, and Organogenesis Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Acute and Chronic Wounds Among Population

- 4.2.2 R&D Activities and Technological Advancements in Collagen Dressing Products

- 4.2.3 Growing Number of Surgical Procedures Worldwide

- 4.3 Market Restraints

- 4.3.1 Availability of Alternative Treatment Options for Collagen Dressings

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Source

- 5.1.1 Bovine

- 5.1.2 Porcine

- 5.1.3 Other Sources

- 5.2 By Form

- 5.2.1 Gel

- 5.2.2 Powder

- 5.2.3 Sheet

- 5.2.4 Other Forms

- 5.3 By Application

- 5.3.1 Acute Wounds

- 5.3.2 Chronic Wounds

- 5.4 By End User

- 5.4.1 Hospitals and Clinics

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 3M

- 6.1.2 Smith+Nephew

- 6.1.3 HARTMANN USA Inc.

- 6.1.4 SANARA MEDTECH INC.

- 6.1.5 DermaRite Industries LLC

- 6.1.6 L&R Group

- 6.1.7 Coloplast Corp.

- 6.1.8 McKesson Medical-Surgical Inc.

- 6.1.9 Convatec Group PLC

- 6.1.10 DeRoyal Industries Inc.

- 6.1.11 Hollister Incorporated

- 6.1.12 Organogenesis Inc.