|

市場調査レポート

商品コード

1521694

ニューロテクノロジー:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Neurotechnology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ニューロテクノロジー:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

ニューロテクノロジーの市場規模は2024年に151億8,000万米ドルと推定され、2029年には285億7,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは13.5%で成長する見込みです。

ニューロエレクトロニクス市場の成長を促す要因としては、神経疾患の有病率の増加、神経科学と技術の急速な進歩、治療オプションの改善に対する需要の高まりなどが挙げられます。

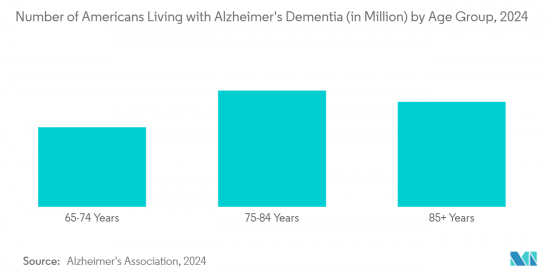

アルツハイマー病、パーキンソン病、てんかん、脳卒中などの神経疾患の罹患率が上昇していることから、効果的な診断・治療ソリューションに対する需要が高まっています。このような状況は、予測期間中の市場の成長を促進すると予測されています。Alzheimer's Association 2024, published in Alzheimer's Disease Facts and Figuresによると、アメリカの65歳以上の人口は2021年の5,800万人から2050年には8,800万人に増加すると予測されています。同出典によると、2024年末までに65歳以上のアメリカ人のうち推定650万人がアルツハイマー病に罹患し始め、この数は2060年末までに1,400万人に達すると予測されています。

国立神経疾患・脳卒中研究所が2024年1月に発表したデータによると、パーキンソン病(PD)は米国で2番目に多い神経変性疾患であり、同国の老人人口の約5%~10%が毎年罹患しています。同資料によると、毎年約50万人がパーキンソン病と診断されています。

WHOが2024年2月に発表したデータによると、世界中で5,000万人以上がてんかんを患っており、最も一般的な神経疾患の一つとなっています。てんかん患者の約80%は低・中所得国に住んでいます。適切な診断と治療を受ければ、てんかん患者の約70%が発作を起こさずに生活できると推定されています。このように、アルツハイマー病、パーキンソン病、てんかんを患う人々の増加は、早期発見、正確な診断、これらの疾患の標的治療のための新たな可能性を提供するニューロテクノロジー製品に対する需要を促進すると予測されます。

また、製品の上市や承認件数の増加も、予測期間中の市場成長を後押しするとみられます。例えば、2023年5月、Abbott社は脊髄刺激(SCS)システムで、腰の手術を受けられない人の慢性腰痛を治療するためのFDAの承認を取得しました。この種の腰痛は非手術性腰痛として知られています。この新たな適応は、Eterna SCSプラットフォームやProclaim SCSファミリーを含む、米国におけるアボット社のSCSに適用されます。2023年1月には、世界の医療技術企業であるアクソニックス社が、同社の第4世代充電式仙骨神経調節システムについて米国食品医薬品局(FDA)の承認を取得しました。このように、製品の承認件数の増加は、革新的な製品の入手可能性を後押しし、製品の安全性と有効性に対する人々の信頼を高めることによって、市場の成長を促進すると予測されます。

しかし、市場開拓にかかる高いコストと複雑な規制環境が、予測期間中の市場成長の妨げになる可能性があります。

ニューロテクノロジー市場の動向

神経刺激装置セグメントは予測期間中に大幅な成長が見込まれる

神経刺激装置は、神経活動を調節するために神経系の特定の神経または領域に電気的または磁気的刺激を与えるもので、疼痛管理、神経疾患の治療、神経調節、リハビリテーションなど、さまざまな治療目的に使用できます。これらのデバイスは、移植することも、外付けのガジェットとして使用することもできます。慢性疼痛、運動障害、精神疾患、その他の神経疾患を患う患者に、的を絞った個別化治療を提供するよう設計されています。

この市場セグメントの成長を牽引している主な要因としては、技術の急速な進歩、非侵襲的・低侵襲的治療に対する患者の嗜好、製品発売数の増加などが挙げられます。神経刺激装置は、従来の神経疾患だけでなく、より幅広い適応症に使用されるようになってきています。現在では疼痛管理、肥満治療、中毒治療、うつ病や不安障害などの精神疾患への応用が検討されており、これにより対処可能な市場が拡大し、急速な成長に寄与しています。

2022年1月にAmerican Academy of Neurology Journalが発表した論文によると、神経刺激装置は運動障害、てんかん、疼痛、うつ病の治療に承認されつつあります。同出典によると、2035年までに、神経解剖学的ネットワークの理解、刺激における作用機序、材料科学の範囲の拡大、小型化、エネルギー貯蔵設備、より優れた送達の進歩により、神経刺激装置の使用量が増加し、予測期間中にこの市場セグメントの成長を大きく促進します。

さらに、製品の発売や提携といった主要企業による戦略的活動の増加や、規制当局による製品承認の急増が市場の成長を後押しします。2022年1月、TensCare社はArab Health 2022で最新の経皮的電気神経刺激を展示しました。この治療器は、糖尿病性神経障害、腰痛、坐骨神経痛、変形性関節症、出産後の外傷などの慢性疼痛状態の長期治療において、薬物を使用しない疼痛緩和のために広く使用されています。

2022年11月、商業段階のバイオエレクトロニクス医療企業であるエレクトロコア社は、同社のガンマコアサファイア非侵襲性迷走神経刺激装置(nVNS)について、ベルギー製薬協会から独自の国家製品コード番号を取得しました。さらに2022年8月、Medtronic Private Limitedはインドで、運動障害やてんかんに伴う症状を治療する脳深部刺激(DBS)療法用のSenSight指向性リードシステムを発売しました。

製品発売数の増加や急速な技術進歩などの要因が、予測期間中の市場成長を促進すると予想されます。

北米は予測期間中に大幅な成長が見込まれる

北米市場は、高齢者人口の増加、神経疾患の増加、主要企業による戦略的製品投入などの要因により、健全な成長を示す可能性が高いです。

同地域では相当数の人々が様々な神経障害に苦しんでおり、予測期間中にニューロテクノロジーデバイスに対する高い需要が生まれると予測されています。2024年1月にParkinson's Foundationが更新したデータによると、米国では毎年約9万人がパーキンソン病と診断されており、2030年末までに全米で約120万人がパーキンソン病を患うと予想されています。

カナダ統計局が2024年1月に発表したデータによると、約75万人のカナダ人がアルツハイマー病やその他の認知症を患っています。2022年10月にThe Journal of Prevention of Alzheimer's Diseaseが発表した論文では、アルツハイマー病やその他の認知症関連疾患は、メキシコにおける障害調整生存年(DALY)をもたらすすべての神経疾患の中で第2位にランクされています。北米における神経疾患の増加は、神経疾患の診断と治療を目的とした革新的なニューロテクノロジーの開発に拍車をかけると予測されています。こうした発展は、北米市場の成長を促進すると予想されます。

さらに、製品開拓の増加が予測期間中の市場成長を加速すると予測されます。2024年1月、アボット社は、遠隔プログラミングが可能な最小クラスの充電式脳深部刺激(DBS)装置であるリベルタRC DBSシステムを、運動障害を抱える人々の治療のために発売する承認をFDAから取得しました。

2022年1月、ネブロ社は、非手術的難治性腰痛(NSRBP)治療用のセンザ脊髄刺激(SCS)システムの表示拡大についてFDAの承認を取得。2022年1月には、メドトロニックが糖尿病性末梢神経障害(DPN)に伴う慢性疼痛治療用の充電式神経刺激装置Intellisと充電不要の神経刺激装置VantaのFDA承認を取得しました。

このように、神経障害の事例の増加や製品開拓の増加などの要因が、予測期間中の地域市場の成長を促進すると予測されています。

ニューロテクノロジー産業の概要

ニューロテクノロジー市場は、世界的・地域的に事業を展開する複数の企業が存在するため、半固有の性質を持っています。主要企業は、合併、買収、提携など、さまざまな戦略的活動に継続的に関与しています。競合情勢としては、市場シェアを持ち知名度の高い地元企業や地域企業が存在感を示しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 神経疾患の有病率の上昇

- 神経科学と技術の急速な進歩

- 治療法の改善に対する需要の高まり

- 市場抑制要因

- ニューロテクノロジーデバイスの高コスト

- 厳しい規制枠組み

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-金額)

- 製品タイプ別

- 神経補綴

- 神経刺激装置

- ブレインコンピューターインターフェイス

- その他の製品

- 用途別

- 神経変性疾患

- 精神神経疾患

- 慢性疼痛管理

- その他の用途

- エンドユーザー別

- 病院およびクリニック

- 研究機関および学術センター

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Medtronic

- Abbott Laboratories

- Boston Scientific

- Siemens Healthineers

- GE Healthcare

- LivaNova PLC

- NeuroPace

- Neuronetics

- Koninklijke Philips N.V.

- Elekta AB

第7章 市場機会と今後の動向

The Neurotechnology Market size is estimated at USD 15.18 billion in 2024, and is expected to reach USD 28.57 billion by 2029, growing at a CAGR of 13.5% during the forecast period (2024-2029).

The factors that are driving the growth of the neuroelectronics market include the increasing prevalence of neurological disorders, rapid advancements in neuroscience and technology, and the rising demand for improved treatment options.

The rising incidence of neurological disorders, such as Alzheimer's disease, Parkinson's disease, epilepsy, and stroke, has led to a rising demand for effective diagnostic and therapeutic solutions. This situation is projected to drive the growth of the market during the forecast period. According to the Alzheimer's Association 2024, published in Alzheimer's Disease Facts and Figures, the American population aged 65 years and above has been projected to grow from 58 million in 2021 to 88 million by 2050. As per the same source, an estimated 6.5 million Americans aged 65 years and above are expected to start suffering from Alzheimer's disease by the end of 2024, and this number is estimated to reach 14 million by the end of 2060.

According to the data published by the National Institute of Neurological Disorders and Stroke in January 2024, Parkinson's disease (PD) is the second-most common neurodegenerative disorder in the United States, which affects around 5%-10% of the geriatric population of the country every year. As per the same source, approximately 500,000 citizens are diagnosed with Parkinson's disease every year.

According to the data published by the WHO in February 2024, more than 50 million people across the world suffer from epilepsy, making it one of the most common neurological diseases. Around 80% of people with epilepsy live in low- and middle-income countries. Estimates suggest that about 70% of people suffering from epilepsy could live seizure-free if they are properly diagnosed and treated. Thus, the rising number of people suffering from Alzheimer's disease, Parkinson's disease, and epilepsy is projected to drive the demand for neurotechnology products to offer new possibilities for early detection, precise diagnosis, and the targeted treatment of these conditions.

The rising number of product launches and approvals is also likely to drive the growth of the market during the forecast period. For instance, in May 2023, Abbott received the FDA's approval for its spinal cord stimulation (SCS) systems for treating chronic back pain in people who cannot undergo back surgery. This kind of back pain is known as non-surgical back pain. This new indication applies to Abbott's SCS in the United States, including the Eterna SCS platform and the Proclaim SCS family. In January 2023, Axonics Inc., a global medical technology company, received the United States Food and Drug Administration's approval for the company's fourth-generation rechargeable sacral neuromodulation system. Thus, the rising number of product approvals is projected to drive the growth of the market by boosting the availability of innovative products and increasing people's confidence in the safety and efficacy of products.

However, the high cost of development and the complex regulatory environment can hinder the growth of the market during the forecast period.

Neurotechnology Market Trends

Neurostimulation Devices Segment is Expected to Witness Significant Growth during the Forecast Period

Neurostimulation devices deliver electrical or magnetic stimulation to specific nerves or areas of the nervous system in order to modulate neural activity, which can be used for various therapeutic purposes, including pain management, treatment of neurological disorders, neuromodulation, and rehabilitation. These devices can be implanted or be used as external gadgets. They are designed to provide targeted and personalized therapy to patients suffering from chronic pain, movement disorders, psychiatric conditions, and other neurological conditions.

The major factors that are driving the growth of this market segment include rapidly rising technological advancements, patients' preferences for non-invasive and minimally invasive treatments, and the rising number of product launches. Neurostimulation devices are being increasingly used for a broader range of indications beyond traditional neurological disorders. They are now being explored for applications in pain management, obesity treatment, addiction therapy, and psychiatric disorders such as depression and anxiety, thereby expanding the addressable market and contributing to its rapid growth.

According to an article published by the American Academy of Neurology Journal in January 2022, neurostimulation devices are being approved for the treatment of movement disorders, epilepsy, pain, and depression. As per the same source, by 2035, advancements in the understanding of neuroanatomical networks, the mechanism of action in stimulation, the expanding scope of material science, miniaturization, energy storage facilities, and better delivery will lead to a higher usage of neurostimulation devices, which will significantly drive the growth of this market segment during the forecast period.

In addition, an increase in strategic activities by the key players, such as product launches and collaborations, and a surge in product approvals by the regulatory authorities will bolster the growth of the market. In January 2022, TensCare showcased its latest in transcutaneous electrical nerve stimulation at Arab Health 2022. This device is widely used for drug-free pain relief for the long-term treatment of chronic pain conditions such as diabetic neuropathy, backache, sciatica, osteoarthritis, and post-childbirth trauma.

In November 2022, ElectroCore Inc., a commercial-stage bioelectronic medicine company, received a unique national product code number from the Belgian Pharmaceutical Association for its gamma-core sapphire non-invasive vagus nerve stimulator (nVNS). Furthermore, in August 2022, Medtronic Private Limited launched the SenSight directional lead system for deep brain stimulation (DBS) therapy to treat symptoms associated with movement disorders and epilepsy in India.

Factors such as the rising number of product launches and rapid technological advancements are expected to drive the growth of the market during the forecast period.

North America is Expected to Witness Significant Growth during the Forecast Period

The North American market is likely to witness healthy growth, owing to factors like the rising geriatric population, increasing neurological disorders, and strategic product launches by the key players.

A significant number of people in the region are suffering from various neurological disorders, which is estimated to create a high demand for neurotechnology devices during the forecast period. According to the data updated by the Parkinson's Foundation in January 2024, approximately 90,000 people in the United States are diagnosed with Parkinson's disease every year, and around 1.2 million people across the country are expected to live with Parkinson's disease by the end of 2030.

According to the data published by Statistics Canada in January 2024, approximately 750,000 Canadians suffer from Alzheimer's disease or other forms of dementia. In an article published by The Journal of Prevention of Alzheimer's Disease in October 2022, Alzheimer's disease and other dementia-related diseases were ranked second among all neurological disorders that result in disability-adjusted life years (DALY) in Mexico. The rising number of neurological disorders in North America is projected to fuel the development of innovative neurotechnologies aimed at diagnosing and treating neurological disorders. These developments are expected to drive the growth of the North American market.

Furthermore, the rising number of product developments is projected to accelerate the growth of the market during the forecast period. In January 2024, Abbott received approval from the FDA to launch the Liberta RC DBS system, one of its smallest rechargeable deep brain stimulation (DBS) devices with remote programming, to treat people living with movement disorders.

In January 2022, Nevro Corp. received the FDA's approval for expanded labeling of its Senza Spinal Cord Stimulation (SCS) system for treating non-surgical refractory back pain (NSRBP). In January 2022, Medtronic received the FDA's approval for its Intellis rechargeable neurostimulator and Vanta recharge-free neurostimulator for treating chronic pain associated with diabetic peripheral neuropathy (DPN).

Thus, factors such as the rising instances of neurological disorders and the increasing number of product developments are projected to drive the growth of the regional market during the forecast period.

Neurotechnology Industry Overview

The neurotechnology market is semi-consolidated in nature due to the presence of several companies operating globally and regionally. The major players are continuously involved in various strategic activities, such as mergers, acquisitions, and partnerships. The competitive landscape includes a strong presence of local and regional companies that hold market shares and are well known, including Abbott, Boston Scientific, Medtronic, and GE Healthcare.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Neurological Disorders

- 4.2.2 Surging Advancements in Neuroscience and Technology

- 4.2.3 Growing Demand for Improved Treatment Options

- 4.3 Market Restraints

- 4.3.1 High Cost of Neurotechnology Devices

- 4.3.2 Stringent Regulatory Framework

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product Type

- 5.1.1 Neuroprosthetics

- 5.1.2 Neurostimulation Devices

- 5.1.3 Brain-Computer Interfaces

- 5.1.4 Other Products

- 5.2 By Application

- 5.2.1 Neurodegenerative Disorders

- 5.2.2 Neuropsychiatric Disorders

- 5.2.3 Chronic Pain Management

- 5.2.4 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals and Clinics

- 5.3.2 Research Institutes and Academic Centers

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic

- 6.1.2 Abbott Laboratories

- 6.1.3 Boston Scientific

- 6.1.4 Siemens Healthineers

- 6.1.5 GE Healthcare

- 6.1.6 LivaNova PLC

- 6.1.7 NeuroPace

- 6.1.8 Neuronetics

- 6.1.9 Koninklijke Philips N.V.

- 6.1.10 Elekta AB