|

市場調査レポート

商品コード

1521686

宇宙用極低温:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Space Cryogenics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 宇宙用極低温:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

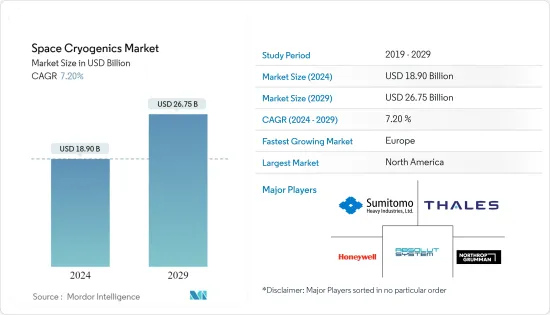

宇宙用極低温市場規模は2024年に189億米ドルと推定・予測され、2029年には267億5,000万米ドルに達し、予測期間中(2024~2029年)にCAGR 7.20%で成長すると予測されています。

宇宙用極低温市場の成長は、宇宙船に搭載されるオペレーションの簡素化が進んでいることに起因しています。宇宙ミッションが複雑化する中、長期間にわたって信頼性の高い性能を発揮できる極低温システムに対する需要が高まっています。

極低温技術の進歩は、過酷な宇宙環境に耐える、より堅牢で効率的な極低温システムの開発につながっています。宇宙ベースの用途におけるセンサーやコールドエレクトロニクスなどの極低温デバイスの進歩や開拓が、市場成長の原動力となっています。

極低温センサーやコールドエレクトロニクスは、材料科学の発展から恩恵を受けるデバイスです。貯蔵タンク、断熱材、移送システム、冷却機構を含む極低温インフラの開発、試験、配備には多額の財政投資が必要です。従って、極低温設備に必要な高い運営費と資本支出は、宇宙極低温市場の成長を妨げる大きな要因となっています。

宇宙用極低温市場の動向

予測期間中、宇宙科学ミッションセグメントが最高市場シェアを占める

宇宙科学ミッションセグメントは、宇宙ミッションにおけるクライオジェニクスの使用増加により、予測期間中に最大の収益シェアを占めると予測されています。世界的に、宇宙機関は人工衛星やロケットなどの打ち上げに率先して取り組んでいます。例えば、2023年5月には、インド宇宙研究機関(ISRO)によって、極低温上段を備えたGSLVロケットを利用する第2世代のナビゲーション衛星の打ち上げが成功しました。NVS-01は、正確でリアルタイムのナビゲーションを提供することで、同国の地域ナビゲーションシステムを補完します。

2022年11月、アメリカの宇宙機関であるNASAは、フロリダのケネディ宇宙センターでアルテミス-1ミッションを打ち上げました。打ち上げ中、コアステージエンジンは打ち上げ8分後に停止し、ロケットの残りの部分から分離しました。この後、中間極低温推進ステージ(ICPS)がオリオン宇宙船の推進に使用されました。オリオン宇宙船の4枚の太陽電池パネルは、NASAによって展開されました。OrionはICPSから切り離され、「トランスルーナー・インジェクション」を完了しました。現在、月軌道に向かって航行中。このような開発は、予測される数年間、このセグメントをリードすると予想されます。

予測期間中、欧州が最も高い成長を遂げる

宇宙用極低温技術市場では、予測期間中に進行中と計画中の宇宙イニシアティブの結果として、欧州が最も高い成長を示すと予測されています。例えば、英国が太陽系外惑星を研究するための宇宙望遠鏡の創設を主導するために、2022年に英国政府は3,105万米ドルの投資を発表しました。この資金により、同国はArielのペイロードモジュール、極低温クーラー、光学地上支援装置を受け取ると同時に、ミッションの科学運用とデータ処理を引き続き主導することが想定されています。

2023年7月、フランス議会は、2024~2030年までの7年間の軍事費プログラムを承認しました。このプログラムには、宇宙開発費として67億米ドルが含まれており、これは前期比45%の増加です。2023年9月、ドイツ政府は新たな宇宙戦略を発表し、2030年までの宇宙旅行の目標と機会を提示しました。

2023年10月、英国宇宙庁と米国の宇宙飛行サービス会社であるAxiom Spaceは、英国の宇宙飛行士を2週間にわたって軌道に送り込むことを目指し、初期協定に調印しました。英国とのミッションは、欧州宇宙機関が商業スポンサーとなり支援します。従って、この地域の宇宙産業における活動の増加は、宇宙用極低温に対する需要の増加につながっており、これが市場収益の成長を促進すると期待されています。

宇宙用極低温産業概要

宇宙用極低温市場は統合されており、大手企業が最も高い市場シェアを持っています。主要市場参入企業には、THALES、Northrop Grumman Corporation、Absolut System、Sumitomo Heavy Industries Ltd、Honeywell International Inc.などがあります。

これらの企業は極低温技術のリーダーであり、極低温クーラーのサプライヤーでもあります。各社は、自動制御、遠隔監視、メンテナンス機能を提供する極低温システムの研究開発に投資しており、宇宙船の運用を合理化し、人為的ミスのリスクを低減するのに役立っています。極低温システムの複雑さを軽減し、使いやすさを向上させることで、宇宙船のオペレーターは複雑なシステム管理よりもミッションの目標に集中することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブ概要

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 冷却タイプ別

- 高温クーラー

- 低温クーラー

- 用途別

- 地球観測

- 通信アプリケーション

- 技術実証ミッション

- クライオエレクトロニクス用途

- 温度別

- 120K以下

- 120 K

- 150K以上

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- ロシア

- フランス

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- THALES

- Absolut System

- Sumitomo Heavy Industries Ltd

- Air Liquide

- Oxford Instruments

- Parker Hannifin Corporation

- Honeywell International Inc.

- RICOR

- Creare

- Northrop Grumman Corporation

第7章 市場機会と今後の動向

The Space Cryogenics Market size is estimated at USD 18.90 billion in 2024, and is expected to reach USD 26.75 billion by 2029, growing at a CAGR of 7.20% during the forecast period (2024-2029).

The space cryogenics market growth can be attributed to the increasing simplicity of operations in onboard spacecraft. With space missions becoming more complex, the demand for cryogenic systems that can deliver reliable performance over extended periods is growing.

Advancements in cryogenic technologies are leading to the development of more robust and efficient cryogenic systems to withstand harsh space conditions. Advancements and developments in cryogenic devices, such as sensors and cold electronics in space-based applications, are driving market growth.

Cryogenic sensors and cold electronics are devices that benefit from the development of materials science. Substantial financial investments are required for the development, testing, and deployment of cryogenic infrastructure, which includes storage tanks, insulation, transfer systems, and cooling mechanisms. Hence, high operating expenses and capital expenditures required for cryogenic setups are major factors hindering the growth of the space cryogenics market.

Space Cryogenics Market Trends

The Space Science Missions Segment will Account for the Highest Market Share During the Forecast Period

The space science missions segment is expected to account for the largest share of revenue over the forecast period, owing to the increasing use of cryogenics in space missions. Globally, space organizations have been taking the initiative to launch satellites, rockets, and others. For instance, in May 2023, a second-generation navigation satellite that utilizes a GSLV rocket with a cryogenic upper stage was successfully launched by the Indian Space Research Organization (ISRO). The NVS-01 will supplement the country's regional navigation system by delivering precise and real-time navigation.

In November 2022, the American space agency, NASA, launched the Artemis-1 mission at Florida's Kennedy Space Center. During the launch, the core stage engines shut down eight minutes after liftoff and separated from the rest of the rocket. After this, the Interim Cryogenic Propulsion Stage (ICPS) was used to propel the Orion spacecraft. The four solar panels of the Orion spacecraft were deployed by NASA. Orion decoupled from the ICPS and completed 'translunar injection.' It is now traveling toward the lunar orbit. Such developments are expected to lead the segment during the forecasted years.

Europe will Witness the Highest Growth During the Forecast Period

In the space cryogenics market, Europe is projected to witness the highest growth as a result of the ongoing and planned space initiatives during the forecast period. For instance, to ensure that the United Kingdom leads the creation of a space telescope to study exoplanets, in 2022, the UK government announced an investment of USD 31.05 million. With this funding, the country is envisioned to continue leading the mission's scientific operations and data processing while also receiving the payload module, cryogenic cooler, and optical ground support equipment for Ariel.

In July 2023, the French parliament approved a seven-year military spending program for 2024-2030 that includes USD 6.7 billion for space programs, which is a 45% increase from the previous period. In September 2023, the German government presented a new Space Strategy and laid its goals and opportunities for space travel until 2030.

In October 2023, the UK Space Agency and a US spaceflight services company, Axiom Space, signed an initial agreement as they bid to send British astronauts into orbit for two weeks. The mission with the UK would be commercially sponsored and supported by the European Space Agency. Hence, increasing activities in the space industry in this region are leading to a rise in demand for space cryogenics, which is expected to drive growth in market revenue.

Space Cryogenics Industry Overview

The space cryogenics market is consolidated, with leading players having the highest market share. Some of the key market players include THALES, Northrop Grumman Corporation, Absolut System, Sumitomo Heavy Industries Ltd, and Honeywell International Inc.

These companies are leaders in cryogenic technology and suppliers of cryogenic coolers. Companies are investing in the R&D of cryogenic systems that offer automated controls, remote monitoring, and maintenance capabilities to help streamline spacecraft operations and reduce the risk of human error. By reducing the complexity of cryogenic systems and enhancing their ease of use, spacecraft operators can focus on mission objectives rather than intricate system management.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Cooling Type

- 5.1.1 High-Temperature Coolers

- 5.1.2 Low-Temperature Coolers

- 5.2 By Application

- 5.2.1 Earth Observation

- 5.2.2 Telecom Applications

- 5.2.3 Technology Demonstration Missions

- 5.2.4 Cryo-Electronics Applications

- 5.3 By Temperature

- 5.3.1 Less Than 120 K

- 5.3.2 120 K

- 5.3.3 More Than 150K

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Russia

- 5.4.2.4 France

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Israel

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 THALES

- 6.2.2 Absolut System

- 6.2.3 Sumitomo Heavy Industries Ltd

- 6.2.4 Air Liquide

- 6.2.5 Oxford Instruments

- 6.2.6 Parker Hannifin Corporation

- 6.2.7 Honeywell International Inc.

- 6.2.8 RICOR

- 6.2.9 Creare

- 6.2.10 Northrop Grumman Corporation