|

市場調査レポート

商品コード

1521667

宇宙軍事化:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Space Militarization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 宇宙軍事化:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

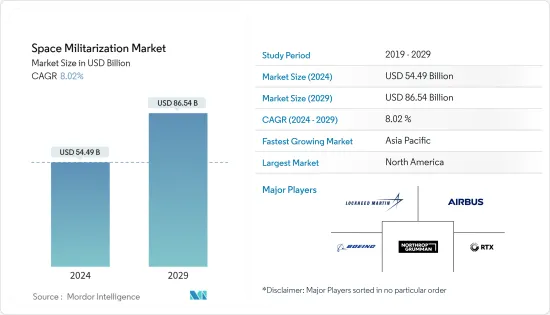

宇宙軍事化の市場規模は2024年に544億9,000万米ドルと推定・予測され、2029年には865億4,000万米ドルに達し、予測期間(2024-2029年)のCAGRは8.02%で成長すると予測されています。

軍事活動における宇宙の戦略的重要性はますます認識されつつあり、宇宙ベースの資産は通信、航行、情報、監視、偵察に不可欠なものとなり、宇宙軍事化市場の拡大に拍車をかけています。軍事的機能のための宇宙への依存は、そのような軍事化へのより高い需要につながります。

中国はこの分野における主要企業であるが、米国やロシアのような、宇宙ベースの資産を通じて軍事力を強化するために宇宙軍事化に多額の投資を行っている国からの手ごわい課題に直面しています。このライバル関係の激化により、中国は市場における軍事的優位性と戦略的地位を維持するため、宇宙軍事化への投資を拡大せざるを得なくなっています。

さらに、人工知能(AI)や指向性エネルギー兵器など、宇宙での用途に合わせた新たな技術の登場は、宇宙での軍事作戦に革命をもたらしています。これらの技術革新は軍事能力を増強し、宇宙空間をますます競合が激しく潜在的に危険な環境に変えています。

宇宙軍事化市場の動向

市場を独占するのは防衛セグメント

軍事的近代化、地政学的ダイナミクスの進化、国家安全保障への要請など、宇宙軍事化を推進する要因により、防衛分野が最大のシェアを占めて市場を独占すると予想されます。

宇宙ベースのシステムは、状況認識の拡張と知能能力の強化において極めて重要であり、国家の防衛上の立場を強化します。宇宙が戦略的な領域であるという認識に伴い、各国は自国の権益を守り、影響力を主張し、地球外の脅威を無力化する可能性のある軍事技術の開発と配備に資源を投入しています。

宇宙の軍事化に向けた動きは、潜在的な兵器化に伴うリスクを軽減しつつ、国家間のバランスを確保するという倫理的、法的、外交的課題も提起しています。例えば2023年8月、米国宇宙軍は新たな戦闘部隊、第75諜報・監視・偵察飛行隊(ISRS)を編成しました。この部隊は、敵対する宇宙軍や対宇宙軍脅威(宇宙攻撃軍)の一部である衛星や地上局、すなわち紛争中に米国が衛星システムを使用する能力を否定するために敵が設計した宇宙能力を標的とする任務を負っています。このような発展は、市場の成長を押し上げると予想されます。

予測期間中は北米が市場を独占する

北米は、宇宙分野への支出の増加、防衛用途の衛星打ち上げ数の増加、NASAやSpaceXによる宇宙探査活動の増加により、予測期間中に宇宙軍事化市場を独占すると予想されます。

宇宙ベースの技術は、輸送や物流を容易にするGPSシステム、世界な通信ネットワークを可能にする衛星、自然災害を予測する気象監視システム、金融取引のための安全なチャネルなど、日常生活の多くの側面や多くの産業の運営において重要な役割を果たしています。これらのシステムに依存しているということは、そのセキュリティと中断のない運用が最重要であることを意味します。したがって米国は、他の多くの国々と同様、経済的安定と国家安全保障を確保するため、宇宙資産の保護と発展に多額の投資を行っています。これは、最後のフロンティアが単なる探検の場ではなく、細心の注意を払って守らなければならない重要なインフラの領域であることを認識しているからです。

ボーイング社、ロッキード・マーチン社、ゼネラル・ダイナミクス社、RTX社、ノースロップ・グラマン社といった主要企業の存在が、この地域の市場地位を強化しています。このような発展は、予測期間中の市場成長を促進すると思われます。

宇宙軍事化産業の概要

宇宙軍事化市場は、The Boeing Company、Airbus SE、Lockheed Martin Corporation、Northrop Grumman Corporation、RTX Corporationといった航空宇宙産業の既存企業の存在によって統合され、その存在感を示しています。

市場プレイヤー間の戦略的提携やパートナーシップは、将来的に企業間の技術移転を促進すると予測されています。宇宙分野の成長機会が高いため、多くの新興企業や新規参入企業がさまざまな開発プログラムを通じてこの業界に進出しています。例えば、2024年2月、英国国防省(MoD)はロッキード・マーチン社に、将来の宇宙能力をタスク化、監視、制御するための、安全でオープンソースの地上セグメント・ソフトウェア・ソリューションを提供する研究開発契約を発注しました。このような企業による研究開発の集中的な進展は、市場の成長をさらに促進すると思われます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 能力

- 防衛

- 支援

- 運用形態

- 宇宙ベース

- 地上ベース

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Lockheed Martin Corporation

- Airbus SE

- Northrop Grumman Corporation

- The Boeing Company

- RTX Corporation

- L3Harris Technologies, Inc.

- General Dynamics Corporation

- Saab AB

- THALES

- BAE Systems plc

- China Aerospace Science and Technology Corporation

The Space Militarization Market size is estimated at USD 54.49 billion in 2024, and is expected to reach USD 86.54 billion by 2029, growing at a CAGR of 8.02% during the forecast period (2024-2029).

The strategic significance of space for military operations is being increasingly recognized, with space-based assets becoming integral for communication, navigation, intelligence, surveillance, and reconnaissance, fueling the expansion of the space militarization market. The reliance on space for military functions leads to a higher demand for such militarization.

While China is a key player in this arena, it faces formidable challenges from nations like the United States and Russia that also heavily invest in space militarization to enhance their military capabilities through space-based assets. This intensifying rivalry compels China to increase its investments in space militarization to maintain its military superiority and strategic position in the market.

Moreover, the advent of emerging technologies such as artificial intelligence (AI) and directed energy weapons, which are being tailored for space applications, is revolutionizing military operations in space. These technological innovations augment military capacities and transform space into an increasingly competitive and potentially hazardous environment.

Space Militarization Market Trends

The Defense Segment will Dominate the Market

The defense segment is expected to dominate the market with the largest share due to the factors that drive space militarization, such as military modernizations, evolving geopolitical dynamics, and imperatives toward national security.

Space-based systems are pivotal in augmenting situational awareness and bolstering intelligence capabilities, enhancing a nation's defense position. With the recognition of space as a strategic domain, nations are channeling resources into creating and deploying military technologies to safeguard their interests, assert influence, and potentially neutralize extraterrestrial threats.

The drive toward space militarization also raises ethical, legal, and diplomatic challenges in ensuring a balance between nations while mitigating the risks associated with its potential weaponization. For instance, in August 2023, the US Space Force formed a new combative unit, the 75th Intelligence, Surveillance and Reconnaissance Squadron (ISRS), which was tasked with targeting satellites and ground stations that are part of adversary space forces and counter-space force threats (space attack forces), namely space capabilities designed by the enemy to deny the United States the ability to use its satellite systems during conflict. Such developments are expected to boost the growth of the market.

North America will Dominate the Market During the Forecast Period

North America is expected to dominate the space militarization market during the forecast period due to the rising expenditure on the space sector, increasing number of satellite launches for defense applications, and growing space exploration activities from NASA and SpaceX.

Space-based technologies play a vital role in many aspects of daily life and the operations of many industries, such as GPS systems that make transportation and logistics easier, satellites that enable global communication networks, weather monitoring systems that forecast natural disasters, and secure channels for financial transactions. The reliance on these systems means that their security and uninterrupted operation are paramount. Thus, the United States, like many other countries, invests heavily in protecting and advancing its space assets to ensure economic stability and national security, recognizing that the final frontier is more than just a place of exploration; it is a domain of critical infrastructure that must be meticulously guarded.

The presence of key players such as The Boeing Company, Lockheed Martin Corporation, General Dynamics Corporation, RTX Corporation, and Northrop Grumman Corporation strengthens the region's market position. Such developments are going to drive the growth of the market during the forecast period.

Space Militarization Industry Overview

The space militarization market is consolidated and marked by the presence of aerospace incumbents such as The Boeing Company, Airbus SE, Lockheed Martin Corporation, Northrop Grumman Corporation, and RTX Corporation.

Strategic collaborations and partnerships between market players are projected to drive the technology transfer between companies in the future. Due to the high growth opportunities in the space sector, many new start-ups and companies have been venturing into the industry through various development programs. For instance, in February 2024, the UK Ministry of Defence (MoD) awarded Lockheed Martin Corporation an R&D contract to provide a secure, open-source, ground-segment software solution to task, monitor, and control its future space capabilities. Such focused developments in research and development by companies will further drive market growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Capability

- 5.1.1 Defense

- 5.1.2 Support

- 5.2 Mode of Operation

- 5.2.1 Space-based

- 5.2.2 Ground-based

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Lockheed Martin Corporation

- 6.2.2 Airbus SE

- 6.2.3 Northrop Grumman Corporation

- 6.2.4 The Boeing Company

- 6.2.5 RTX Corporation

- 6.2.6 L3Harris Technologies, Inc.

- 6.2.7 General Dynamics Corporation

- 6.2.8 Saab AB

- 6.2.9 THALES

- 6.2.10 BAE Systems plc

- 6.2.11 China Aerospace Science and Technology Corporation