宇宙用センサおよびアクチュエータ:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

Space Sensors And Actuators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1521641

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

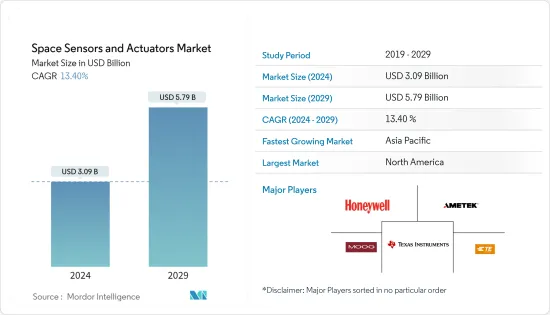

宇宙用センサおよびアクチュエータ市場規模は2024年に30億9,000万米ドルと推定され、2029年には57億9,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは13.40%で成長します。

宇宙産業は、非公開会社の参入と投資によって大きな変貌を遂げています。SpaceXやBlue Originのようなパイオニアは、宇宙船の設計、推進力、ミッション遂行に対する革新的なアプローチで展望を再構築しています。市販の部品は宇宙技術を民主化し、より身近で費用対効果の高いものにしています。これとロボット工学や積層造形技術の進歩が相まって、宇宙探査に対する経済的障壁が低くなっています。

新興国も宇宙予算を増やし、市場の成長をさらに刺激しています。こうした市場開拓は、宇宙用センサおよびアクチュエータ市場を前進させるだけでなく、宇宙がより幅広い探検家や起業家の手の届くところにあるという、惑星探査の新時代への道をも開いています。技術進歩と投資拡大の相乗効果により、かつては手の届かないと思われた将来の革新とミッションのための肥沃な土壌が生まれつつあります。

宇宙用センサー・アクチュエーター市場は、成長を阻害しかねない重大な課題に直面しています。地上ミッション用のセンサーとアクチュエーター技術の成熟度は、放射線や腐食性大気のような宇宙の過酷な条件に耐えるシステム設計の複雑さと同様に、重大な懸念事項です。宇宙船の開発と配備に関連する政府の政策も障害となる可能性があります。このような課題にもかかわらず、技術の進歩や非公開会社からの投資の増加により、市場の成長が見込まれています。

宇宙用センサおよびアクチュエータの市場動向

予測期間中、センサセグメントが市場成長を牽引すると予測

宇宙用センサおよびアクチュエータは、現代の宇宙ミッションに不可欠なコンポーネントであり、それぞれがそれぞれの用途のユニークな要求を満たすように調整されています。これらの洗練されたデバイスは、宇宙の過酷な条件下で動作するように設計されており、環境モニタリング、宇宙船の操縦、データ収集などの重要な機能を実行します。例えば、高度なセンサーを搭載した気象観測衛星は、大気の状態を正確に測定することができ、アクチュエーターは、最適な画像撮影や太陽光発電のための衛星の正確な位置決めを確実にします。

同様に、宇宙観測衛星は、微調整された動きのためにMEMSベースのアクチュエータを利用し、強烈な宇宙放射線に耐えるために放射線硬化センサーを利用します。これらの技術は、宇宙船や探査機の性能と信頼性を高め、宇宙ミッションの費用対効果に貢献します。テレダインe2vの高解像度センサーを採用したESAのコペルニクスのようなプログラムは、地球観測やその他の科学的試みをサポートする上で、これらのコンポーネントの重要性を例証しています。

宇宙探査が進化し続けるにつれて、センサーとアクチュエーターの役割は、宇宙技術で可能なことの限界を押し広げる上でますます不可欠になります。宇宙領域認識における進歩は、軌道上における安全保障と監視能力の強化に対する重要なコミットメントを反映しています。米国宇宙軍によるセンサーと監視システムへの投資は、ますます競合領域となりつつある宇宙空間での状況認識を維持するための戦略的な動きです。

光学望遠鏡と監視衛星の開発は、宇宙活動の監視能力を強化し、潜在的な脅威への迅速な対応を確保することを目的としています。このような積極的なアプローチは、国防と世界・セキュリティにとって重要なフロンティアとしての宇宙の重要性を強調しています。

予測期間中、北米が市場を独占する見込み

予測期間中、北米が宇宙用センサおよびアクチュエータ市場をリードすると見られています。北米の宇宙用センサおよびアクチュエータ市場は、米国が大きなシェアを占めています。米国における市場の成長は、宇宙用センサおよびアクチュエータシステムの主要メーカーの存在に起因しています。米国を拠点とする主要な宇宙用センサおよびアクチュエータメーカーには、Texas Instruments Incorporated、Sierra Nevada Corporation、Honeywell International Inc.、Moog Inc.、Bradford Spaceなどがあります。NASAによる打ち上げ数の増加も、予測期間中、惑星探査の観点から米国の宇宙センサー・アクチュエータ市場を牽引すると予想されています。例えば、SpaceX社はFalconシリーズのロケットで96のミッションを成功させています。

宇宙用センサおよびアクチュエータの使用は、放射線耐性のある電気光学宇宙センサの開発の増加や、衛星、カプセル貨物、惑星間宇宙船&探査機、ローバ/宇宙船着陸機、ロケット、宇宙ステーション用の宇宙用センサおよびアクチュエータの小型化によって成長すると予想されます。また、2023年6月、米国宇宙軍はL3Harris Technologies Inc.に、同軍が計画中の弾力性のあるミサイル警報・追跡衛星コンステレーション用のセンサーを設計する契約を2,900万米ドルで発注しました。このような発展は、予測期間中の市場の成長を促進すると思われます。

宇宙用センサおよびアクチュエータ産業の概要

著名な宇宙用センサおよびアクチュエータメーカーの存在感が増していることから、予測期間中に競争企業間の敵対関係が激化すると予想されます。市場は、以下のような主要プレイヤーの存在によって半固定化されています。 Honeywell International Inc., Moog Inc., Texas Instruments Incorporated, TE Connectivity Ltd., and Ametek Inc. These players have continuously expanded their operations by focusing on market expansions and acquisitions.

継続的な製品の発表と技術的なアップグレードは、宇宙分野における市場全体の成長に関して効果的にボールを転がします。例えば、2023年6月、ハネウェルと量子ネットワーキングとコンピューティングの会社であるAegiqは、宇宙ペイロードと関連する地上資産の設計と配備をより正確でコスト効率の高いものにするための包括的なソリューションの構築を検討するMoUに調印しました。この協力は、小型衛星で使用される光通信技術のリンク性能のために、Honeywellの大気センシング技術とAegiqのエミュレーションツールキットを組み合わせることを意図したものです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ

- センサー

- アクチュエーター

- プラットフォーム

- 衛星

- カプセル/カーゴモジュール

- 惑星間探査機

- ローバー/宇宙船着陸船

- ローンチビークル

- エンドユーザー

- 商業

- 政府・防衛

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Honeywell International Inc.

- TE Connectivity Ltd.

- Moog Inc.

- Ametek Inc.

- Texas Instruments Incorporated

- RUAG Group

- STMicroelectronics NV

- RTX Corporation

- Cobham Advanced Electronics Solutions(Cobham Limited)

- Maxar Technologies Inc.

- Bradford Space(Bradford Engineering BV)

目次

The Space Sensors And Actuators Market size is estimated at USD 3.09 billion in 2024, and is expected to reach USD 5.79 billion by 2029, growing at a CAGR of 13.40% during the forecast period (2024-2029).

The space industry is witnessing a significant transformation fueled by the entry and investments of private companies. Pioneers like SpaceX and Blue Origin are reshaping the landscape with their innovative approaches to spacecraft design, propulsion, and mission execution. Commercial-off-the-shelf components have democratized space technology, making it more accessible and cost-effective. This, coupled with robotics and additive manufacturing advancements, has reduced the financial barriers to space exploration.

Emerging countries are also increasing their space budgets, further stimulating the market's growth. These developments are not only propelling the space sensors and actuators market forward but are also paving the way for a new era of planetary exploration, where space is within reach of a broader range of explorers and entrepreneurs. The synergy of technological progress and increased investment is creating a fertile ground for future innovations and missions that once seemed beyond our grasp.

The space sensors and actuators market faces significant challenges that could impede growth. The maturity of sensor and actuator technologies for surface missions is a critical concern, as is the complexity of designing systems that can withstand the harsh conditions of space, such as radiation and corrosive atmospheres. Government policies related to spacecraft development and deployment can also pose obstacles. Despite these challenges, the market is expected to grow, driven by technological advancements and increased investments from private companies.

Space Sensors And Actuators Market Trends

The Sensors Segment is Anticipated to Drive the Growth of the Market During the Forecast Period

Space sensors and actuators are integral components of modern space missions, each tailored to meet the unique demands of their respective applications. These sophisticated devices are designed to operate in the harsh conditions of space, performing critical functions such as environmental monitoring, spacecraft maneuvering, and data collection. For instance, weather monitoring satellites with advanced sensors can accurately measure atmospheric conditions, while actuators ensure precise satellite positioning for optimal image capture or solar power generation.

Similarly, space observation satellites utilize MEMS-based actuators for fine-tuned movements and radiation-hardened sensors to withstand intense cosmic radiation. These technologies enhance the performance and reliability of spacecraft and rovers and contribute to the cost-effectiveness of space missions. Programs like ESA's Copernicus, which employs high-resolution sensors from Teledyne e2v, exemplify the importance of these components in supporting Earth observation and other scientific endeavors.

As space exploration continues to evolve, the role of sensors and actuators becomes increasingly vital in pushing the boundaries of what is possible in space technology. The advancements in space domain awareness reflect a significant commitment to enhancing security and surveillance capabilities in orbit. The US Space Force's investment in sensors and surveillance systems is a strategic move to maintain situational awareness in space, which is increasingly becoming a contested domain.

The development of optical telescopes and surveillance satellites aims to bolster the ability to monitor space activities, ensuring a rapid response to any potential threats. This proactive approach underscores the importance of space as a critical frontier for national defense and global security.

North America is Expected to Dominate the Market During the Forecast Period

North America is expected to lead the space sensors and actuators market during the forecast period. The US accounted for a major share of the space sensors and actuators market in North America. The market's growth in the US can be attributed to the presence of key manufacturers of space sensors and actuator systems. Some key US-based space sensors and actuator companies include Texas Instruments Incorporated, Sierra Nevada Corporation, Honeywell International Inc., Moog Inc., and Bradford Space. The rise in the number of launches from NASA is also anticipated to drive the US space sensors and actuators market in terms of planetary exploration during the forecast period. For instance, SpaceX launched 96 successful missions with its Falcon series of rockets.

The use of space sensors and actuators is expected to grow due to the increasing development of radiation-hardened electro-optical space sensors and the miniaturization of space sensors and actuators for satellites, capsules cargos, interplanetary spacecraft & probes, rovers/spacecraft landers, launch vehicles, and space stations. Also, in June 2023, the US Space Force awarded L3Harris Technologies Inc. a USD 29 million contract to design a sensor for the service's planned Resilient Missile Warning and Tracking satellite constellation. Thus, developments such as these will drive the market's growth during the forecast period.

Space Sensors And Actuators Industry Overview

The increasing presence of prominent space sensors and actuator manufacturers is expected to intensify competitive rivalry during the forecast period. The market is semi-consolidated with the presence of key players such as Honeywell International Inc., Moog Inc., Texas Instruments Incorporated, TE Connectivity Ltd., and Ametek Inc. These players have continuously expanded their operations by focusing on market expansions and acquisitions.

Continuous product launches and technological upgrades effectively set the ball rolling regarding overall market growth in the space sector. For instance, in June 2023, Honeywell and Aegiq, a quantum networking and computing company, signed an MoU to explore creating a comprehensive solution to enable more precise and cost-effective design and deployment of space payloads and related ground assets. This collaboration was intended to combine Honeywell's atmospheric sensing technology and Aegiq's emulation toolkit for link performance of optical communication technologies used by small satellites.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Sensors

- 5.1.2 Actuators

- 5.2 Platform

- 5.2.1 Satellites

- 5.2.2 Capsules/Cargo Modules

- 5.2.3 Interplanetary Spacecraft & Probes

- 5.2.4 Rovers/Spacecraft Landers

- 5.2.5 Launch Vehicles

- 5.3 End User

- 5.3.1 Commercial

- 5.3.2 Government and Defense

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Honeywell International Inc.

- 6.2.2 TE Connectivity Ltd.

- 6.2.3 Moog Inc.

- 6.2.4 Ametek Inc.

- 6.2.5 Texas Instruments Incorporated

- 6.2.6 RUAG Group

- 6.2.7 STMicroelectronics NV

- 6.2.8 RTX Corporation

- 6.2.9 Cobham Advanced Electronics Solutions (Cobham Limited)

- 6.2.10 Maxar Technologies Inc.

- 6.2.11 Bradford Space (Bradford Engineering BV)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日