|

市場調査レポート

商品コード

1521637

武器マウント:市場シェア分析、産業動向と統計、成長予測(2024~2029年)Weapon Mounts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 武器マウント:市場シェア分析、産業動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

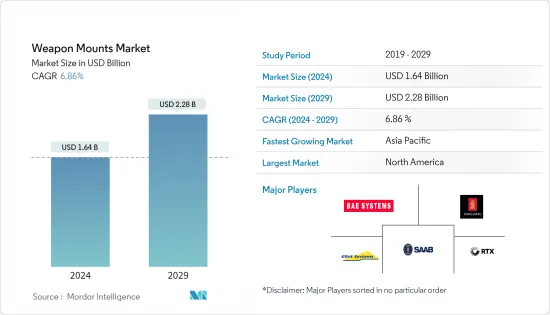

武器マウント市場規模は2024年に16億4,000万米ドルと推定され、2029年には22億8,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは6.86%で成長する見込みです。

世界の武器マウント市場は、各国の海軍プラットフォームの近代化により著しい盛り上がりを見せています。遠隔武器ステーション、防衛車両に搭載される技術兵器の需要の増加、高度な戦争装備の採用がこの成長を後押ししています。重要地帯での人的被害を最小限に抑えることが重視され、防衛システムへの投資が増加し、国境や敏感な地域での無人戦争部品が好まれるようになった。

世界の兵器の近代化計画や、遠隔操作兵器システム用の安定性の高いマウントの市場開拓は、市場拡大の新たな機会を提供すると期待されています。

しかし、武器マウントの耐久性の高さによる交換頻度の低下や、既存プラットフォームからの需要の飽和といった課題が、今後数年間の市場成長を抑制する可能性があります。このような課題にもかかわらず、革新と技術的進歩に重点を置く市場は、今後も市場を牽引していくと思われます。

武器マウント市場動向

予測期間中は陸上セグメントが市場を独占する見込み

世界の防衛産業は、投資の増加と新技術の採用によって大きな変化を経験しています。地政学的緊張が高まるにつれ、さまざまな陸上プラットフォーム向けの地上搭載型システムの開発など、軍事能力の近代化が重視されるようになっています。これらのシステムは、課題環境における安定性と性能を高めるように設計されています。

このような先進装備への需要は、防衛分野におけるデジタル化と革新に向けた幅広い傾向の一部です。企業は、進化する顧客の嗜好や持続可能性の目標を満たす製品イノベーションに注力する一方で、サプライチェーンの複雑さや労働力の課題に対処するため、デジタル技術に投資しています。

さらに、軍用モノのインターネット(IoMT)と自動化された軍事システムの統合が進んでおり、より相互接続された自律的な防衛ソリューションへのシフトを示しています。例えば、2024年3月、Milrem Roboticsは米国陸軍遠征戦士実験(AEWE)のための武器化無人地上車両のデモンストレーションを完了しました。この活動は、2040年まで戦闘員の致死性を高めるための「最先端の」ソリューションを検証することに重点を置いていました。

米国議会予算局(CBO)によると、米陸軍の地上戦闘車両の総取得費用は、2050年まで年間約50億米ドルに達すると予想されています。そのうち45億米ドルが調達費、5億米ドルが研究開発費です。このような調達と現有フリートのアップグレードに対する支出の増加は、予測期間中の市場の成長を促進すると予想されます。

予測期間中、アジア太平洋地域が最も高い成長を遂げる見込み

この地域における地政学的緊張の高まりにより、中国、インド、オーストラリア、韓国、シンガポール、日本などの国々は、30年以上運用されている老朽化した車両を置き換えるために、新車両の調達に多額の投資を行っています。インド、中国、日本、韓国を含む主要な軍事大国は、年間防衛予算を絶えず増額しています。この予算には、航空優勢を改善・拡大するための大きな部分が含まれており、この地域における軍事航空の成長を牽引しています。

例えば、インド政府は2023年度予算で、新型戦闘機ラファールやスホイ-30MKI、テジャス戦闘機の製造費など、インド空軍のために前回予算より約10%増額した予算を計上しました。また、2023年5月、韓国の国防調達計画庁(DAPA)は、大韓民国陸軍(RoKA)向けの現代ロテムK2主力戦車(MBT)の第4バッチの量産を承認しました。これらすべての要因が、予測期間中の同地域の市場成長を促進すると予想されます。

武器マウント産業の概要

武器マウント市場は半固体化しており、世界企業とローカル企業が価格競争と技術革新を通じて市場成長に大きく貢献しています。市場の主要企業には、RTX Corporation、BAE Systems PLC、Kongsberg Gruppen ASA、Saab AB、Elbit Systems Ltd.などがあります。顧客基盤を拡大し、技術的専門知識を共有するために、地元企業と提携している企業もあります。例えば、アダニ・ディフェンス・アンド・エアロスペース社は、エルビット・システムズ社と共同で、エルビット社のATMOS 155mm/52口径トラック搭載榴弾砲をベースとした搭載砲システム(MGS)を提供することで、インド陸軍の砲兵能力を強化しようとしています。

東欧、中東、アジア太平洋などの地域における地政学的不安定は、先進的な武器マウントシステムの需要を喚起しています。米国では、時代遅れの兵器を段階的に廃止し、最新鋭のシステムを採用することで、陸上部隊の近代化を図ろうとする協調的な取り組みが行われています。同時に、過去10年間における海軍力の重視の高まりにより、さまざまな軍艦の大幅な発注が行われ、海上防衛能力を強化するための新型搭載兵器の統合が必要となっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 静的

- 非静的

- 動作モード

- 手動

- 遠隔操作

- 用途

- 陸上

- 航空

- 海洋

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Kongsberg Gruppen ASA

- BAE Systems PLC

- RTX Corporation

- Saab AB

- Elbit Systems Ltd

- Dillion Aero

- FN Herstal

- AEI Systems Ltd

- Leonardo SpA

- Military Systems Group Inc.

The Weapon Mounts Market size is estimated at USD 1.64 billion in 2024, and is expected to reach USD 2.28 billion by 2029, growing at a CAGR of 6.86% during the forecast period (2024-2029).

The global weapon mounts market is experiencing a significant upsurge due to the modernization of naval platforms in various countries. The increasing demand for remote weapon stations, technical weapons in defense vehicles, and the adoption of advanced warfare equipment propels this growth. The emphasis on minimizing human casualties in critical zones has led to a rise in investments in defense systems and a preference for unmanned war components at borders and sensitive areas.

The global weapon modernization plans and the development of highly stabilized mounts for remotely operated weapon systems are expected to offer new opportunities for market expansion.

However, challenges such as the high durability of weapon mounts, which reduces the frequency of replacements, and a saturated demand from existing platforms may restrain market growth in the coming years. Despite these challenges, the market's focus on innovation and technological advancements will likely continue driving the market forward.

Weapon Mounts Market Trends

The Land Segment is Expected to Dominate the Market During the Forecast Period

The global defense industry is experiencing significant change, driven by increased investment and the adoption of new technologies. As geopolitical tensions rise, the emphasis on modernizing military capabilities, including developing ground-mounted systems for various land platforms, is increasing. These systems are designed to enhance stability and performance in challenging environments.

The demand for such advanced equipment is part of a broader trend toward digitalization and innovation within the defense sector. Companies are investing in digital technologies to address supply chain complexities and workforce challenges while focusing on product innovations that meet evolving customer preferences and sustainability goals.

Moreover, the integration of the Internet of Military Things (IoMT) and automated military systems is rising, indicating a shift toward more interconnected and autonomous defense solutions. For instance, in March 2024, Milrem Robotics completed a weaponized unmanned ground vehicle demonstration for the US Army Expeditionary Warrior Experiment (AEWE). The activity focused on validating "state-of-the-art" solutions to increase warfighter lethality through 2040.

The total acquisition costs for the US Army's ground combat vehicles are expected to reach around USD 5 billion per year through 2050, according to the US Congressional Budget Office (CBO). Of that, USD 4.5 billion is meant for procurement, and USD 0.5 billion for RDT&E. Such procurements and growing expenditure on the upgradation of the current fleet are expected to propel the growth of the market over the forecast period.

The Asia-Pacific Region is Expected to Witness the Highest Growth During the Forecast Period

Due to the increasing geopolitical tensions in the region, countries like China, India, Australia, South Korea, Singapore, and Japan are significantly investing in procuring new vehicles to replace their aging fleets, which have been in operation for over 30 years. Major military powers, including India, China, Japan, and South Korea, are constantly increasing their annual defense budgets. This budget includes a significant portion for improving and expanding air superiority, driving the growth of military aviation in the region.

For instance, in the budget of FY 2023, the Indian government allocated about 10% more for the Indian Air Force than the previous budget, including payments for the new Rafale fighters and the manufacturing of Sukhoi-30MKIs and Tejas fighters. Also, in May 2023, South Korea's Defense Acquisition Program Administration (DAPA) approved the mass production of a fourth batch of the Hyundai Rotem K2 main battle tank (MBT) for the Republic of Korea Army (RoKA). All these factors, in turn, are expected to drive the market's growth in the region during the forecast period.

Weapon Mounts Industry Overview

The weapon mounts market is semi-consolidated, with global and local players contributing significantly to the market's growth through competitive pricing and innovation. Some major companies in the market include RTX Corporation, BAE Systems PLC, Kongsberg Gruppen ASA, Saab AB, and Elbit Systems Ltd. Some players have partnered with local companies to expand their customer base and share technical expertise. For instance, in collaboration with Elbit Systems, Adani Defense and Aerospace is set to enhance the Indian Army's artillery capabilities by offering a Mounted Gun System (MGS) based on Elbit's ATMOS 155mm/52 caliber truck-mounted howitzer.

Geopolitical instabilities in regions like Eastern Europe, the Middle East, and Asia-Pacific catalyze the demand for advanced weapon mount systems. In the United States, there is a concerted effort to modernize land forces by phasing out obsolete weaponry in favor of cutting-edge systems. Concurrently, the heightened emphasis on naval strength over the past decade has resulted in substantial orders for various warships, necessitating the integration of new mounted weaponry to bolster maritime defense capabilities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Static

- 5.1.2 Non-Static

- 5.2 Mode of Operation

- 5.2.1 Manual

- 5.2.2 Remotely Operated

- 5.3 Application

- 5.3.1 Land

- 5.3.2 Air

- 5.3.3 Sea

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Kongsberg Gruppen ASA

- 6.2.2 BAE Systems PLC

- 6.2.3 RTX Corporation

- 6.2.4 Saab AB

- 6.2.5 Elbit Systems Ltd

- 6.2.6 Dillion Aero

- 6.2.7 FN Herstal

- 6.2.8 AEI Systems Ltd

- 6.2.9 Leonardo SpA

- 6.2.10 Military Systems Group Inc.