|

市場調査レポート

商品コード

1693955

原子時計:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Atomic Clock - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 原子時計:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

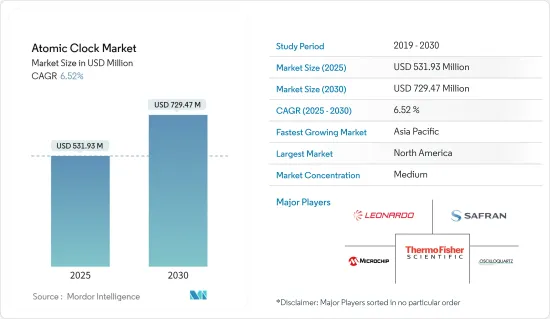

原子時計の市場規模は2025年に5億3,193万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.52%で、2030年には7億2,947万米ドルに達すると予測されています。

原子時計市場の成長は、航空宇宙や軍事セグメントで高精度原子時計のニーズが高まっていることに起因しています。原子時計は、正確な一方向距離測定を保証し、送信されたGPS信号の位相精度を確実に維持します。量子コンピューティングと量子通信の開発は、市場により良い機会をもたらすと予想されます。

世界ナビゲーションと測位システムの拡大、GPSとGNSSシステムにおける原子時計の用途の台頭も、原子時計市場の成長に拍車をかけています。しかし、配備とメンテナンスのコストが高いことが、予測期間中の市場成長の妨げになる可能性があります。

原子時計市場の動向

予測期間中、防衛が市場シェアを独占

世界の軍事が新しく正確な位置ナビゲーションシステムを統合することで老朽化した航空機の近代化を図っているため、原子時計は防衛セグメントのエンドユーザーから大きな需要があります。現行世代の航空機の多くはGNSS(GPS)とTACANの位置ナビゲーションシステムを利用しており、新しい航空機の需要も予測期間中に原子時計の並行需要を生むと考えられます。

これに関連して、2018年12月、米国空軍は、ナビゲーションと位置測定の品質を高めるために次世代GPS受信機を艦隊全体に統合すると発表しました。米国空軍ライフサイクル管理センターは、F-16航空機のフリートに最新世代のデジタルGPSアンチジャムレシーバ(DIGAR)を提供するためにロックウェルコリンズを選択しました。さまざまな軍事からの同様のイニシアチブは、予測期間中にセグメントの成長を推進すると予想されます。

米国、ドイツ、インド、オーストラリア、アラブ首長国連邦、中国などの多くの国は、まったく新しいプラットフォームを取得するのではなく、既存の軍用機フリートの近代化に投資しています。例えば、米国空軍は2018年12月、戦闘機に次世代GPS受信機を搭載し、ナビゲーションと測位測定の質を高めると発表しました。このイニシアチブの下、米国空軍ライフサイクル管理センターはロックウェル・コリンズ社を選定し、F-16航空機のフリートに最新世代のデジタルGPSアンチジャム受信機(DIGAR)を提供しました。さまざまな軍事からの同様のイニシアチブは、予測期間中にセグメントの成長を推進すると予想されます。

航空機用航法補助装置の進歩は、企業にとって新たな市場機会を生み出すと予想されます。例えば、Northrop Grumman CorporationのASAF(All Source Adaptive Fusion)ソフトウェアは、全地球測位システム(GPS)衛星信号を使用せずに軍用機や空中兵器システムを誘導することを可能にします。このようなソフトウェアを先進的センサシステムと併用することで、航空プラットフォームの運用効率が向上すると期待されています。

予測期間中、北米が最大の市場シェアを持つ見込み

ストックホルム国際平和ラボ(SIPRI)によると、世界の国防費は2022年に2兆米ドルを超え、米国などの軍事大国は2022年に国防予算を急増させています。米国の国防費は2021~2022年にかけて710億米ドル増加し、世界の国防費の40%近くを占めました。

米国空軍は、ロシアや中国との大国間紛争の要求に応えるため、次世代航空機の開発と調達を続けています。米国空軍は1万3,247機の航空機で構成され、運用機、予備機、アウトオブサービス機の一部となっています。日本や台湾といった国との外交・軍事関係から、中国からの挑発的な軍事行動に対抗するため、航空機の増備に多額の投資を余儀なくされています。

さらに、米国が中東地域の軍事紛争に関与していることが、攻撃機や輸送機の調達に大きく影響しています。空軍省は2023年度の予算要求として、2022年度予算要求から202億米ドル(11.7%)増の1,940億米ドルを提案しました。この予算の大部分は、新型航空機の調達と、国の軍事行動を支援する新技術の研究開発に充てられます。また、宇宙セグメントへの支出の増加、商業と防衛用途の衛星打ち上げ数の増加、NASAとSpaceXによる宇宙探査活動の拡大は、米国市場にとって重要なブースターであり、北米地域の原子時計市場を牽引しています。

原子時計産業概要

原子時計市場は半固定的であり、世界的に事業展開している参入企業は一握りです。Thermo Fisher Scientific Inc.、Oscilloquartz(Adtran Networks SE)、Microchip Technology Inc.、Leonardo SpA、Safranなどが主要参入企業です。同市場は競争が激しく、各社が最大の市場シェアを獲得しようと競い合っています。

各社は、自社製造能力、世界ネットワーク、製品ラインアップ、研究開発投資、強固な顧客基盤などを兵器にしのぎを削っています。明確な価格帯における技術力と製品の特徴もまた、重要な市場パラメータです。正確な測位とナビゲーション機能に対する需要の高まりは、市場参入企業を製品ポートフォリオの拡充に駆り立てています。新規参入業者の脅威は中程度であり、市場の競合情勢は製品/サービスの拡大と技術革新の高まりにより激化すると予測されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- ルビジウム(Rb)原子時計

- セシウム(Cs)原子時計

- 水素(H)メーザー原子時計

- エンドユーザー

- 防衛

- 戦闘機とヘリコプター

- 無人車両

- 装甲車

- ポータブルシステム

- 艦艇(駆逐艦、フリゲートなど)

- 潜水艦

- 哨戒艦

- 宇宙

- 防衛

- 用途

- モニタリング

- ナビゲーション

- 電子戦

- テレメトリー

- 通信

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- ポーランド

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- AccuBeat Ltd.

- Excelitas Technologies Corp.

- IQD Frequency Products Limited

- Leonardo S.p.A.

- Microchip Technology Incorporated

- Oscilloquartz(Adtran Networks SE)

- Stanford Research Systems

- Tekron International Limited

- VREMYA-CH JSC

- Safran

- MacQsimal(CSEM)(accelopment Schweiz AG)

- Thermo Fisher Scientific Inc

第7章 市場機会と今後の動向

The Atomic Clock Market size is estimated at USD 531.93 million in 2025, and is expected to reach USD 729.47 million by 2030, at a CAGR of 6.52% during the forecast period (2025-2030).

The atomic clock market's growth is attributed to the increasing need for high-precision atomic clocks in the aerospace and military sectors. Atomic clocks guarantee accurate one-way range measurements, ensuring the user maintains the transmitted GPS signal's phase precision. Developments in quantum computing and quantum communication are expected to create better opportunities for the market.

The expansion of global navigation and positioning systems and the rise of atomic clock applications in GPS and GNSS systems are also fueling the growth of the atomic clock market. However, the high cost of deployment and maintenance may hinder the market's growth during the forecast period.

Atomic Clock Market Trends

Defense to Dominate Market Share During the Forecast Period

The atomic clocks are in huge demand from defense end-users as the global armed forces look to modernize their aging fleet by integrating new and accurate position and navigation systems. Most current-generation aircraft utilize GNSS (GPS) and TACAN positioning and navigation systems, and the demand for new aircraft would also generate parallel demand for atomic clocks during the forecast period.

On this note, in December 2018, the US Air Force announced the fleet-wide integration of next-generation GPS receivers to enhance the quality of navigation and positioning measurements. The US Air Force Life Cycle Management Center selected Rockwell Collins to provide its latest-generation Digital GPS Anti-Jam Receiver (DIGAR) for its fleet of F-16 aircraft. Similar initiatives from various armed forces are anticipated to propel the segment's growth during the forecast period.

Many countries, such as the United States, Germany, India, Australia, the United Arab Emirates, and China, are investing in modernizing their existing fleet of military aircraft rather than acquiring entirely new platforms. For instance, in December 2018, the US Air Force announced that their fighter aircraft would be fitted with next-generation GPS receivers to enhance the quality of navigation and positioning measurements. Under this initiative, the US Air Force Life Cycle Management Center selected Rockwell Collins to provide its latest-generation Digital GPS Anti-Jam Receiver (DIGAR) for its fleet of F-16 aircraft. Similar initiatives from various armed forces are anticipated to propel the segment's growth during the forecast period.

The anticipated advancement of navigational aids for aircraft is expected to create new market opportunities for companies. For instance, Northrop Grumman Corporation's All Source Adaptive Fusion (ASAF) software allows military aircraft and airborne weapon systems to guide them without using Global Positioning System (GPS) satellite signals. Such software, when used with advanced sensor systems, is anticipated to improve the operational efficiencies of the air platforms.

North America is Expected to Have the Largest Market Share During the Forecast Period

The world defense expenditure crossed over USD 2 trillion in 2022, with significant military powers such as the US surging their defense budgets in 2022, according to the Stockholm International Peace Research Institute (SIPRI). US defense spending increased by USD 71 billion from 2021 to 2022, which comprised nearly 40% of global defense expenditures.

The US Air Force continues developing and procuring next-generation aircraft to meet the demands of great power conflicts with Russia and China. The US Air Force comprises 13,247 aircraft that are part of an operational, reserve, and out-of-service fleet. The country's diplomatic and military relations with nations such as Japan and Taiwan have compelled it to drive significant investments into increasing the fleet of aircraft to counter any provocative military action from China successfully.

Furthermore, the US involvement in the military conflict in the Middle Eastern region majorly drove its procurement of attack aircraft and transport aircraft. The Department of Air Force proposed a budget request of USD 194 billion for FY2023, a USD 20.2 billion or 11.7% increase from the FY2022 budget request. A major chunk of this budget will be channeled toward the procurement of new aircraft and research and development of new technologies that can aid the military actions undertaken by the country. Also, the rising expenditure on the space sector, increasing number of satellite launches for commercial and defense applications, and growing space exploration activities from NASA and SpaceX are significant boosters for the US market, which drives the atomic clock market in the North American region.

Atomic Clock Industry Overview

The atomic clock market is semi-consolidated, with a handful of players operating globally. Thermo Fisher Scientific Inc., Oscilloquartz (Adtran Networks SE), Microchip Technology Inc., Leonardo SpA, and Safran are some of the major market players. The market is highly competitive, with players competing to gain the largest market share.

Market players compete, leveraging their in-house manufacturing capabilities, global network footprint, product offerings, research and development investments, and robust client base. Technical capabilities and product features at definite price points are also key market parameters. The increasing demand for accurate positioning and navigation capabilities drives the market players to broaden their product portfolio. With a moderate threat of new entrants, the market's competitive landscape is projected to intensify due to heightened product/service extensions and technological innovations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Rubidium (Rb) Atomic Clock

- 5.1.2 Cesium (Cs) Atomic Clock

- 5.1.3 Hydrogen (H) Maser Atomic Clock

- 5.2 End User

- 5.2.1 Defense

- 5.2.1.1 Combat Aircraft and Helicopters?

- 5.2.1.2 Unmanned Vehicles?

- 5.2.1.3 Armoured Vehicles

- 5.2.1.4 Portable Systems

- 5.2.1.5 Naval Ships (Destroyers, Frigates, etc)

- 5.2.1.6 Submarines?

- 5.2.1.7 Patrol Vessels?

- 5.2.2 Space

- 5.2.1 Defense

- 5.3 Application

- 5.3.1 Surveillance

- 5.3.2 Navigation

- 5.3.3 Electronic Warfare?

- 5.3.4 Telemetry

- 5.3.5 Communication

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Italy

- 5.4.2.6 Spain

- 5.4.2.7 Poland

- 5.4.2.8 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 AccuBeat Ltd.

- 6.2.2 Excelitas Technologies Corp.

- 6.2.3 IQD Frequency Products Limited

- 6.2.4 Leonardo S.p.A.

- 6.2.5 Microchip Technology Incorporated

- 6.2.6 Oscilloquartz (Adtran Networks SE)

- 6.2.7 Stanford Research Systems

- 6.2.8 Tekron International Limited

- 6.2.9 VREMYA-CH JSC

- 6.2.10 Safran

- 6.2.11 MacQsimal (CSEM) (accelopment Schweiz AG)

- 6.2.12 Thermo Fisher Scientific Inc