|

市場調査レポート

商品コード

1521402

再保険:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Reinsurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 再保険:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

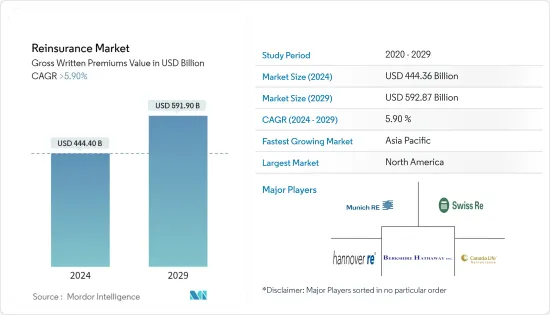

再保険市場規模は、2024年の4,444億米ドルから2029年には5,919億米ドルに拡大し、予測期間(2024~2029年)のCAGRは5.90%を超えると予測されます。

主なハイライト

- 市場の成長は、保険商品に対する意識の高まりによるものです。かつては、発展途上国や新興諸国における保険市場の成長は緩やかでした。なぜなら、国民は保険商品について知らず、政府もその重要性を主張していなかったからです。しかし、保険に対する意識の高まりとともに、これらの国々の保険・再保険市場は成長しています。

- 再保険市場は、財物災害プロテクションの成長により拡大が見込まれます。しかし、可処分所得の低さから保険普及率が低く、脆弱な経済と海外との競合が市場成長を阻害すると予想されます。一方、再保険会社内でのデジタル化は今後の市場成長を後押しします。

- さらに、損害再保険と導管再保険への嗜好が主要産業で高まっていることから、今後数年間は成長の好機が訪れると予想されます。

- 年金基金や資本市場投資家など、再保険市場に代わる資本源が増加しています。キャタストロフ・ボンドなどの保険リンク証券(ILS)は、資本市場へのリスク移転を促進し、再保険業界のキャパシティと流動性を高めています。

- 今年度、再保険業界は保険料と保険引受収益性を伸ばしました。しかし、債券価格の下落(金利の上昇と信用スプレッドの縮小による)と株式市場の下落により、自己資本利益率(ROE)と資本水準は低下しました。このような状況にもかかわらず、再保険業界の全体的な財務健全性は依然として高く、基礎的な収益性は改善し続けています。

再保険市場の動向

イノベーションが再保険市場を牽引

- 再保険業界は、業界内の長年の問題を解決するテクノロジー主導のビジネスを構築するために、その知識を活用した起業家たちによって活況を呈しています。テクノロジーの利点に対する意識の高まりと、再保険テック新興企業への資金提供の可能性の高まりが、このブームを後押ししています。

- テクノロジーの進化とニッチなソフトウェア・ソリューションの採用により、再保険市場は今後5年から10年の間に大きな変革を遂げると予想されます。こうした技術革新は、効率性と収益性の向上につながると思われます。

- 保険業界における数々のイノベーションが再保険市場を牽引しています。例えば、生命再保険プロバイダーは、糖尿病、HIV、メンタルヘルスの問題を含む商品や、職業性障害の補償範囲を広げる新しいコンセプトの商品を導入しています。

- キャタストロフ・リスク・モデリングの活用は、先進的アナリティクスで最も求められている分野の一つです。キャタストロフ・リスク・モデリングは、リスク選択、リスク軽減からポートフォリオ分析、プライシングの決定に至るまで、再保険機能の大部分に大きな影響を与えるため、再保険において重要な役割を果たしています。

北米が市場を独占している

- 再保険は、リスクを軽減するために他の保険会社が引き受ける保険の一形態です。再保険は、保険会社が損失する可能性のある金額を削減し、ひいては顧客を損失から守ることを目的としています。世界の再保険市場は、米国を中心とする世界中の企業にとって必要不可欠なものです。

- 米国の傷害・再保険(P&C)再保険市場では、国内外の様々な再保険会社が活躍しています。この市場の特徴は、法改正、大災害、市場環境の変化に左右されるダイナミックな性質にあります。

- 米国の再保険業界は国内の保険会社に再保険キャパシティを提供し続けているが、各州の規制当局は、競争力のある米国マーケットのニーズに応えるため、国内外の再保険キャパシティが必要であることを以前から認識していました。米国は再保険の枠組みを構築し、再保険料収入の大半を国外で再保険するという、開放的でありながら安全な再保険市場を形成してきました。

- 米国の再保険業界は、国内保険会社の再保険キャパシティの重要な供給源であることに変わりはないが、各州の規制当局は、米国のマーケットプレースのニーズを満たすために、国内再保険と非国内再保険の両方のキャパシティの必要性を長い間理解してきました。その結果、米国は再保険規制体制を確立し、再保険料収入の大半が米国外で再保険されるという、開放的でありながら安全な再保険市場を形成してきました。

再保険業界の概要

再保険市場は非常に細分化されています。現在、大きな市場シェアを持つのは一部の大手保険会社だけです。しかし、技術や商品開拓の進歩により、多くの企業が新規契約を結び、新興国市場に参入することで、市場でのプレゼンスを拡大しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

- 調査の枠組み

- 2次調査

- 1次調査

- データの三角測量と洞察の生成

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 保険普及率の増加

- 気候変動と災害の増加が再保険の必要性を高める

- 市場抑制要因

- 複雑なマクロ経済と地政学的シナリオ

- 再保険パフォーマンスにおける規制の壁

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 市場における技術革新に関する洞察

- 市場の規制と産業政策に関する洞察

- COVID-19の影響に関する洞察

- 主要市場リスクと影響分析

第5章 市場セグメンテーション

- タイプ別

- 任意再保険

- 特約再保険

- 用途別

- 損害保険

- 生命保険・健康保険

- 販売チャネル別

- ダイレクトライティング

- ブローカー

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第6章 競合情勢

- 市場集中度(概要と市場シェア)

- 企業プロファイル

- Munich RE

- Swiss RE

- Hannover Re Group

- Canada Life RE

- Berkshire Hathaway Inc.

- SCOR SE

- China Reinsurance Corp

- Lloyd's

- Reinsurance Group of America

- Everest Re Group

- Partner RE

- Renaissancere

- Sompo Holdings*

第7章 市場機会と今後の動向

第8章 免責事項および出版社について

The Reinsurance Market size in terms of gross written premiums value is expected to grow from USD 444.40 billion in 2024 to USD 591.90 billion by 2029, at a CAGR of greater than 5.90% during the forecast period (2024-2029).

Key Highlights

- The market's growth is due to the growing awareness of insurance products. In the past, the insurance market in developing and emerging countries grew slowly because the people were unaware of the product, and neither was the government insisting on its importance. However, with the growing awareness of insurance, these countries' insurance and reinsurance markets are growing.

- The reinsurance market is expected to grow due to the growth of property catastrophe protection. However, fragile economies with low insurance penetration due to low disposable income and competition from overseas are expected to impede market growth. On the other hand, digitalization within reinsurance companies will help the market grow in the future.

- Furthermore, the growing preference for property and casualty reinsurance and conduit reinsurance among leading industries is expected to provide lucrative opportunities for growth in the coming years.

- Alternative sources of capital for the reinsurance market have increased, including pension funds and capital markets investors. Insurance-linked securities (ILS), such as catastrophe bonds, facilitate the transfer of risk to capital markets, increasing the reinsurance industry's capacity and liquidity.

- In the current year, the reinsurance industry had growth in premiums and underwriting profitability. However, return on equity (ROE) and capital levels decreased due to a decline in bond prices (driven by rising interest rates and tightening credit spreads) and equity markets. Despite this, the overall financial health of the reinsurance industry remains strong, with underlying profitability continuing to improve.

Reinsurance Market Trends

Innovation Is Driving The Reinsurance Market

- The reinsurance industry is experiencing a boom driven by entrepreneurs who have used their knowledge to build technology-driven businesses that solve long-standing problems within the industry. A growing awareness of the benefits of technology and the growing availability of funding for reinsurance tech startups is driving this boom.

- The reinsurance market is expected to undergo a major transformation in the next 5 to 10 years as technology advances and niche software solutions are adopted. These innovations will result in greater efficiency and profitability.

- A number of innovations in the insurance industry are driving the reinsurance market. For instance, life reinsurance providers have introduced products that include diabetes, HIV, and mental health issues, as well as new concepts that broaden the scope of occupational disability coverage.

- The use of catastrophic risk modeling is one of the most sought-after areas of advanced analytics. Catastrophic risk modeling plays an important role in reinsurance because it has a significant impact on the majority of reinsurance functions, from risk selection and risk mitigation to portfolio analysis and pricing decisions.

North America Is Dominating The Market

- Reinsurance is a form of insurance that other insurance companies take out to reduce the risk. Reinsurance aims to reduce the amount of money an insurance company could lose and, in turn, protect its customers from losses. The global reinsurance market is essential for companies worldwide, especially in the United States.

- There are a variety of domestic and foreign reinsurers active in the United States personal injury and reinsurance (P&C) reinsurance market. The market is characterized by its dynamic nature, driven by changes in legislation, catastrophic events, and market conditions.

- While the US reinsurance industry continues to provide domestic insurance companies with reinsurance capacity, state regulatory authorities have long recognized the need for domestic and foreign reinsurance capacity to serve the needs of a competitive US marketplace. The United States has created a reinsurance framework that has led to an open but safe reinsurance market, with most reinsurance premium revenue reinsured outside the country.

- While the reinsurance industry in the United States remains an important source of reinsurance capacity for domestic insurance companies, state regulators have long understood the need for both domestic and non-domestic reinsurance capacity to meet the needs of the United States marketplace. As a result, the United States has established a reinsurance regulatory regime that has resulted in an open but secure reinsurance market where the majority of reinsurance premium income is reinsured outside the United States.

Reinsurance Industry Overview

The reinsurance market is highly fragmented. At present, only a few of the big players have a significant market share. However, due to advances in technology and product development, many firms are expanding their presence in the market by signing new contracts and entering new markets. The market is dominated by the following: Munich Re, Swiss Re, Hannover Re Group, Canada Life Re, and Berkshire Hathaway Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Insurance Penetration

- 4.2.2 Climate Change and Raising Catastrophes Drive the Need of Reinsurance

- 4.3 Market Restraints

- 4.3.1 Complex Macro-Economic and Geopolitical Scenario

- 4.3.2 Regulatory Barrier in Reinsurance Performance

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Insights on Technological Innovations in the Market

- 4.6 Insights on Regulatory and Industry Policies in the Market

- 4.7 Insights on the Impact of Covid-19

- 4.8 Key Market Risks and Impact Analysis

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Facultative Reinsurance

- 5.1.2 Treaty Reinsurance

- 5.2 By Application

- 5.2.1 Property & Casualty Insurance

- 5.2.2 Life and Health Insurance

- 5.3 By Distribution Channel

- 5.3.1 Direct Writing

- 5.3.2 Broker

- 5.4 By Region

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration (Overview and Market Share)

- 6.2 Company Profiles

- 6.2.1 Munich RE

- 6.2.2 Swiss RE

- 6.2.3 Hannover Re Group

- 6.2.4 Canada Life RE

- 6.2.5 Berkshire Hathaway Inc.

- 6.2.6 SCOR SE

- 6.2.7 China Reinsurance Corp

- 6.2.8 Lloyd's

- 6.2.9 Reinsurance Group of America

- 6.2.10 Everest Re Group

- 6.2.11 Partner RE

- 6.2.12 Renaissancere

- 6.2.13 Sompo Holdings*