|

市場調査レポート

商品コード

1521353

木材製建築建具および木工品:世界市場シェア分析、産業動向、成長予測(2024年~2029年)Global Builders Joinery And Carpentry Of Wood - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 木材製建築建具および木工品:世界市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

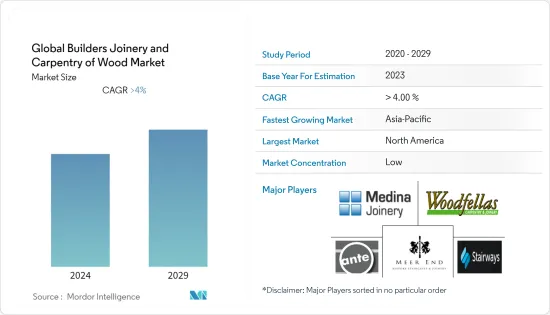

世界の木材製建築建具および木工品市場規模は2024年に769億4,000万米ドルと推定され、2029年には956億5,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは4.45%で成長すると予測されます。

主なハイライト

- 木材製建築建具および木工品は、その有利な特質から世界中の新興経済諸国で広く使用されています。特に中国、マレーシア、インドでは国民の可処分所得が増加しているため、新興国でも贅沢品に注目が集まっています。新興国の人々は特に、高価な木製家具、窓、ドア、そしてそれらのフレームに惹かれています。その結果、世界中の経済成長国から木材建具と大工の大きな需要が見込まれます。

- 建具産業では、フローリング、窓、ドア、階段、家具、室内建具など、さまざまな用途に木材を使用します。パイン材は、表面をきれいに仕上げることができ、心材が腐敗や害虫に対する自然な抵抗力を備えているため、通常よく使われます。パンデミック(世界的大流行)や世界市場における原材料の入手問題にもかかわらず、建具業界は好調に推移しています。

- 多くの国々の政府と欧州連合(EU)は、建設産業や環境保護(EUグリーン・ディールなど)を含む世界経済の発展を支援し、刺激するためのいくつかのプログラムを立ち上げています。

- こうした動きは建設資材の需要を刺激し、その結果、建具の売上が増加し、同分野の企業が新たな生産設備や技術に投資する動きが目に見える形で現れました。世界の建具業界は、逆説的な激動と好転の時期を過ごしました。

- 建築資材に対する需要の高まりと、その生産に必要な原材料の一時的な不足は、価格の上昇を招いたが、建具の販売水準を下げることはありません。間もなく実施期間に入る欧州や地方のプロジェクトが、建設業界の成長動向をさらに加速させる可能性があります。

木材製建築建具および木工品市場の動向

建築物の増加

- ブランド意識の高まりと進化し続けるインテリア・デザインの動向により、住宅や商業ビルのオーナーは木製家具への支出を拡大しています。家具メーカーは木工機械を活用し、精巧に作られた木製家具を顧客に提供しています。

- 今後10年間の木工機械需要の伸びが予想される背景には、作業員の生産性と全体的な効率を高めることを目的とした、産業部門における自動化志向の高まりがあります。建具部門は建設業界と密接に結びついており、建設が増えるということは、これらの空間に家具や設備を整えるための建具の需要が高まることを意味します。

- 住宅分野は、発展途上国における急速な都市化により、自分の住宅を求める個人の増加を反映し、収益貢献でリードすると予想されます。アジア太平洋地域の建設市場は、特定の国々における急速な経済成長と人口増加を背景とした建設プロジェクトの急増によって成長を遂げています。

- 中東・アフリカでは、工業、商業、住宅プロジェクトにより、市場収益は急速な成長を記録すると予測されます。欧州の建設市場は、一部の国における改修プロジェクトの増加に起因して、着実な収益成長が見込まれています。現在、英国は住宅セクターの建設プロジェクト数でリードしており、政府と投資の増加に大きく支えられています。

北米の住宅リフォームが市場を独占している

- 金利と不動産コストの上昇が、住宅改修サービス市場を大きく牽引しています。住宅改修サービス市場は当初、建設活動の制限のために阻害されていました。しかし、規制が解除されるにつれて市場は回復し始めました。この市場によって、木材産業における建具と大工の重要性が倍増しました。

- キッチンや浴室など内装の増改築ニーズの高まりは、市場の成長に影響を与えると思われます。この業界の事業者は、住宅(一戸建て住宅や集合住宅)の内装や外装のリフォームやリノベーションを行う。リフォーム業界の事業者は、増改築、改築、メンテナンス、補修工事などの活動を含む、住宅建築物の内装や外装のリフォームやリノベーションを行う。

- 2022年の住宅改修サービス市場では、北米が最大地域でした。Angiによると、2022年に住宅所有者が住宅改修プロジェクトに投資した金額は平均8,484米ドルでした。2023年には、金利上昇にもかかわらず、消費者の50%が同額、28%が支出減、22%が支出増を見込んでいます。ハーバード大学住宅センター共同センター(JCHS)によると、住宅改修プロジェクト支出は2019年の3,280億米ドルから2022年には4,720億米ドルに上昇し、2023年には4,850億米ドルの支出が予想されています。

- 住宅販売の停止や住宅ローンの借り換えなど、住宅産業が抱える問題の結果、2023年には住宅修繕プロジェクトが減少すると予想されています。人件費の高騰とサプライチェーンの持続的な問題が、住宅リフォーム部門を苦しめています。

- JCHSによれば、住宅リフォームの売上は2022年第3四半期にピークに達し、2023年には減少に転じた。JCHSは、2023年末までに4,850億米ドルの市場増加を予想することで、ある程度の収益成長に自信を保っています。

木材製建築建具および木工品産業の概要

世界の建具および木工大工市場は、国際的なプレーヤーやローカルプレーヤーが多数存在し、競争は緩やかです。企業は先手を打つために技術投資を行っています。また、建築の進歩に伴い、市場の競争も激化しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 政府の規制とイニシアチブ

- 木材製建築建具および木工品市場における今後のプロジェクトに関する洞察

- 技術動向

- COVID-19が世界の木材製建築建具および木工品市場に与える影響

第5章 市場力学

- 市場促進要因

- 持続可能な建設が市場を牽引

- 急速な都市化と建設活動の増加

- 市場抑制要因

- 労働力不足

- 市場機会

- 技術の進歩

- ポーターのファイブフォース分析

- 産業バリューチェーン/サプライチェーン分析

第6章 市場セグメンテーション

- タイプ別

- セルラーパネル

- 窓

- 組立式寄木パネル

- ドア

- その他のタイプ

- 用途別

- 家具

- 建物

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- ラテンアメリカ

- ブラジル

- コロンビア

- アルゼンチン

- その他ラテンアメリカ

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他アジア太平洋地域

- 中東・アフリカ

- イラン

- サウジアラビア

- イスラエル

- その他中東とアフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Masonite International Corporation

- JELD-WEN Holding, Inc.

- Pella Corporation

- Andersen Corporation

- VELUX Group

- Assa Abloy AB

- VELFAC(part of VKR Holding)

- Mason Company

- YKK AP Inc.

- Shenzhen Runcheng Chuangzhan Woodworking Co., Ltd.*

第8章 市場の将来

第9章 付録

目次

Product Code: 91344

The Global Builders Joinery And Carpentry Of Wood Market size is estimated at USD 76.94 billion in 2024, and is expected to reach USD 95.65 billion by 2029, growing at a CAGR of 4.45% during the forecast period (2024-2029).

Key Highlights

- Due to its advantageous qualities, builders' joinery and carpentry are widely used in developed economies all over the world. Due to the increased disposable income of the populace, particularly in China, Malaysia, and India, emerging economies are also turning their attention to luxury. People in emerging nations are particularly drawn to expensive wood furnishings, windows, doors, and their frames. As a result, there will be a large demand for wood joinery and carpentry from growing economies all over the world.

- The joinery industry uses wood for various purposes, including flooring, windows, doors, stairs, furniture, and interior fittings. Pine is the usual choice because it can be given a good surface finish, and the heartwood provides natural resistance to rot and insects. Despite the pandemic and problems with the availability of raw materials in the global markets, the joinery industry is performing well.

- Governments of many countries and the European Union (EU) have launched several programs to support and stimulate the development of the global economy, including the construction industry and environmental protection (e.g., the EU Green Deal).

- Such actions have stimulated demand for construction materials, resulting in increased sales of joinery and the visible activity of companies in the sector to invest in new production facilities and technologies. The global joinery industry has had a period of paradoxical turbulence and turnarounds.

- Rising demand for building materials and a temporary lack of raw materials for their production has caused prices to rise but has not reduced the level of joinery sales. European and local projects, which will soon enter the implementation period, may further accelerate growth trends in the construction industry.

Builders Joinery and Carpentry of Wood Market Trends

Increase in building construction is growing

- Due to the increasing awareness of brands and ever-evolving interior design trends, owners of residential and commercial buildings are expanding their spending on wooden furniture. Furniture manufacturers utilize woodworking machinery to deliver well-crafted wooden pieces to customers.

- Anticipated growth in the demand for woodworking machines over the next decade is driven by the rising preference for automation in industrial units, aiming to enhance worker productivity and overall efficiency. The joinery sector is closely tied to the construction industry; more construction means a higher demand for joinery to furnish and equip these spaces.

- The housing segment is expected to lead in revenue contribution due to rapid urbanization in developing countries, reflecting an increasing number of individuals seeking their own residential properties. The Asia Pacific construction market is experiencing growth fueled by a surge in construction projects across the region, driven by rapid economic expansion in certain countries and a growing population.

- In the Middle East & Africa, market revenue is projected to register rapid growth due to industrial, commercial, and residential projects. Europe's construction market is expected to demonstrate steady revenue growth, attributed to increasing renovation projects in some countries. Currently, the United Kingdom leads in the number of construction projects in the residential sector, supported significantly by the government and increasing investments.

North America home renovations are dominating the market

- The rise in interest rates and property costs majorly drives the home improvement services market. The home improvement services market was initially hampered owing to restrictions on construction activities. However, the market started recovering as lockdown restrictions were lifted. This market has made the importance of joinery and carpentry in the wood industry increase manifold.

- The increasing need for interior additions & alterations in kitchens and baths will influence the market growth. Operators in this industry remodel and renovate the interiors and exteriors of residential buildings (i.e., single-family homes and multifamily apartment building units). Operators in the remodeling industry remodel and renovate the interiors and exteriors of residential buildings, which includes activities such as additions, alterations, reconstruction, maintenance, and repair work.

- North America was the largest region in the home improvement services market in 2022. According to Angi, homeowners invested an average of USD 8,484 in home improvement projects in 2022. In 2023, 50% of consumers anticipated spending the same amount, 28% anticipated spending less, and 22% anticipated spending more despite rising interest rates. Home renovation project spending had climbed from USD 328 billion in 2019 to USD 472 billion in 2022, with an expected spending of USD 485 billion in 2023, according to the Joint Centre for Housing Centres of Harvard University (JCHS).

- Home repair projects are anticipated to decrease in 2023 as a result of problems with the housing industry, including halted home sales and mortgage refinancing. Rising labor costs and persistent supply chain problems plague the home renovation sector.

- According to JCHS, home improvement sales reached their peak in the third quarter of 2022 and began to fall off in 2023. By having anticipated a market increase of USD 485 billion by the end of 2023, JCHS remained confident about some revenue growth.

Builders Joinery and Carpentry of Wood Industry Overview

The global builders joinery and carpentry of wood market are moderately competitive, with the presence of many international and local players. Companies are investing in technology to stay ahead of the game. Also, with the advancement in construction the market will be becoming more competitive.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Government regulations and initiatives

- 4.3 Insights on upcoming projects in joinery and carpentry market

- 4.4 Technological Trends

- 4.5 Impact of COVID-19 on Global Builders Joinery and Carpentry Of Wood Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Sustainable Construction is driving the market

- 5.1.2 Rapid Urbanization and Increasing Construction Activities

- 5.2 Market Restraints

- 5.2.1 Labor Shortage

- 5.3 Market Opportunities

- 5.3.1 Technological Advancement

- 5.4 Porter's Five Forces Analysis

- 5.5 Industry Value Chain/Supply Chain Analysis

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Cellular Wood Panels

- 6.1.2 Windows

- 6.1.3 Assembled Parquet Panels

- 6.1.4 Doors

- 6.1.5 Other Types

- 6.2 By Application

- 6.2.1 Furniture

- 6.2.2 Building

- 6.2.3 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.1.3 Rest of North America

- 6.3.2 Latin America

- 6.3.2.1 Brazil

- 6.3.2.2 Colombia

- 6.3.2.3 Argentina

- 6.3.2.4 Rest of Latin America

- 6.3.3 Europe

- 6.3.3.1 Germany

- 6.3.3.2 United Kingdom

- 6.3.3.3 France

- 6.3.3.4 Rest of Europe

- 6.3.4 Asia Pacific

- 6.3.4.1 China

- 6.3.4.2 Japan

- 6.3.4.3 India

- 6.3.4.4 Rest of Asia Pacific

- 6.3.5 Middle East & Africa

- 6.3.5.1 Iran

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 Israel

- 6.3.5.4 Rest of Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration Analysis and Major Player)

- 7.2 Company Profiles

- 7.2.1 Masonite International Corporation

- 7.2.2 JELD-WEN Holding, Inc.

- 7.2.3 Pella Corporation

- 7.2.4 Andersen Corporation

- 7.2.5 VELUX Group

- 7.2.6 Assa Abloy AB

- 7.2.7 VELFAC (part of VKR Holding)

- 7.2.8 Mason Company

- 7.2.9 YKK AP Inc.

- 7.2.10 Shenzhen Runcheng Chuangzhan Woodworking Co., Ltd.*