水銀:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

Mercury - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1521327

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

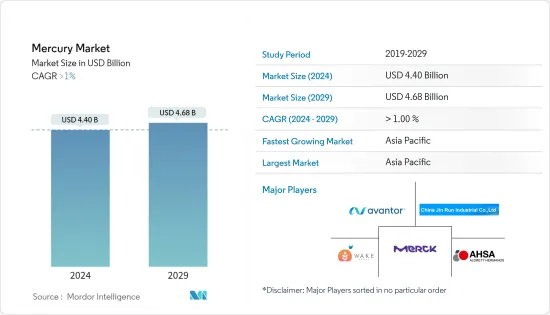

水銀の市場規模は2024年に44億米ドルと推計され、2029年には46億8,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは1%以上で成長すると予測されます。

COVIDパンデミックは水銀市場に様々な影響を与えました。一方では、経済活動の低下により、製造業や建設業など一部の産業で水銀需要が減少しました。他方、パンデミックは、政府や企業が自社の製品や環境に水銀汚染がないことを確認しようとしたため、水銀検査サービスの需要増加にもつながった。全体として、COVID-19が水銀市場に与える影響は比較的小さいと予想されます。

調査対象となった市場を牽引する主な要因は、測定・制御装置の需要です。

水銀の危険な性質は、市場の成長抑制要因として作用する可能性が高いです。その危険な性質のため、多くの国が水銀を含む電池、体温計、気圧計、血圧計を禁止しており、調査した市場に影響を与えています。

水銀市場は、化学プロセスにおける触媒や特定の医療機器など、代替品がまだ利用できない特定のニッチ用途における需要の増加により成長を遂げています。

アジア太平洋地域が世界市場の大半を占め、中国とタジキスタンからの需要が大半を占めると予想されます。

水銀市場の動向

測定・制御機器が最大セグメントに

- 水銀は、温度計、自動車部品、サーモスタットプローブ、気圧計、真空計、炎センサー、流量計、比重計、湿度計/乾湿計、マノメーター、高温計、医療機器など、さまざまな機器に使用されています。

- 水銀は、血圧測定用の血圧計に大規模に使用されています。また、血圧の測定は、さまざまな臨床状態の診断やモニタリングにおいて重要です。従来、血圧は血圧計を用いて非侵襲的に測定されてきました。これは現在でも血圧測定の「ゴールド・スタンダード」として認識されています。

- 2022年には、世界中で推定2,200トンの水銀が生産されました。水銀は主に電気・電子製品や工業用化学製品の製造に使用されています。

- しかし、水銀に関する環境問題への懸念から、欧州の一部の国では禁止措置がとられ、英国では現在、ヘルスケアへの供給が制限されています。水銀は、世界保健機関(WHO)によって、公衆衛生上重大な懸念のある化学物質トップ10または化学物質群のひとつとみなされています。

アジア太平洋地域が市場を独占する

- 水銀の最大市場はアジア太平洋地域です。アジア太平洋地域では、中国とキルギスが水銀の主要生産国です。これに加え、中国は世界最大の水銀鉱山生産量と埋蔵量を誇っています。また、中国では石炭を原料とする塩化ビニルモノマー製造の触媒として水銀化合物が使用されていました。

- したがって、中国は2022年には世界最大の水銀生産国となり、鉱山生産量は2,000トンとなります。第2位の水銀生産国タジキスタンの同年の生産量は約120トンです。

- 世界では、1,000万~2,000万人が職人的小規模金採掘(ASGM)セクターで働いており、その多くが日常的に水銀を使用しています。

- 職人的小規模金採掘(ASGM)は、人為的水銀排出の世界最大の原因(37.7%)であり、次いで石炭の定置燃焼(21%)です。

- USGSによると、中国、キルギスタン、メキシコ、ペルー、ロシア、スロベニア、スペイン、ウクライナは、世界で推定60万トンの水銀資源の大半を保有しています。

- さらに、職人的小規模金採掘(ASGM)は、アジア、南米、アフリカの55カ国以上にまたがる広範な事業を展開しています。ASGMはこれらの国々にとってミクロ経済の源泉として機能しているが、ASGMは環境と健康に悪影響を及ぼしています。

- 中国では、歯科用アマルガムの使用は西暦1000年にまでさかのぼる。今日、歯科用アマルガムは水銀と銀、スズ、銅の金属合金で構成されています。

- 前述の要因はすべて、この地域における水銀の消費を増大させると予想されます。

水銀産業の概要

水銀市場は部分的に断片化されています。主なプレーヤー(順不同)には、Avantor Inc.(サーモフィッシャーサイエンティフィック)、AHSA、Aldrett Hermanos SA de CV、Merck KGaA、Wake Group、China Jin Run Industrialなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 測定・制御機器からの需要

- 血圧測定用血圧計の需要

- 鉱業分野での金の抽出に広く使用されている

- 抑制要因

- 水銀の危険な特性

- その他の制約

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 製品タイプ

- 金属

- 合金

- 化合物

- 用途

- 電池

- 歯科用途

- 測定・制御装置

- ランプ

- 電気・電子機器

- 金の加工

- その他の用途(ヘルスケア、医薬品、電池)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ノルディック

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Aldrett Hermanos

- Antares Chem Private Limited

- Avantor Performance Materials

- Bethlehem Apparatus Co. Inc.

- China Jin Run Industrial Co. Ltd

- Mayasa

- Merck KGaA

- Powder Pack Chem

- Special Metals

- Tamilnadu Engineering Instruments

- Wake Group

第7章 市場機会と今後の動向

第8章 ニッチ用途での水銀需要の拡大

第9章 その他の機会

目次

The Mercury Market size is estimated at USD 4.40 billion in 2024, and is expected to reach USD 4.68 billion by 2029, growing at a CAGR of greater than 1% during the forecast period (2024-2029).

The COVID pandemic had a mixed impact on the mercury market. On the one hand, the decline in economic activity led to a decrease in demand for mercury in some industries, such as the manufacturing and construction sectors. On the other hand, the pandemic also led to an increase in demand for mercury testing services, as governments and businesses sought to ensure that their products and environments were free of mercury contamination. Overall, the impact of COVID-19 on the mercury market is expected to be relatively modest.

The major factor driving the market studied is the demand for measuring and controlling devices.

The hazardous properties of mercury are likely to act as a restraint to the growth of the market. Owing to its hazardous nature, many countries have banned mercury-containing batteries, thermometers, barometers, and blood pressure monitors, thus affecting the market studied.

The mercury market is experiencing growth due to increasing demand in specific niche applications, such as catalysts in chemical processes and certain medical devices, where alternatives are not yet available.

Asia-Pacific is expected to dominate the global market, with the majority of the demand coming from China and Tajikistan.

Mercury Market Trends

Measuring and Controlling Devices to be the largest segment

- Mercury is used in various devices such as thermometers, automotive parts, thermostat probes, barometers, vacuum gauges, flame sensors, flowmeters, hydrometers, hygrometers/psychrometers, manometers, pyrometers, medical devices, and more.

- Mercury is used on a large scale in the sphygmomanometer for the measurement of blood pressure. Also, the measurement of blood pressure is important in the diagnosis and monitoring of a wide range of clinical conditions. Traditionally, blood pressure is measured non-invasively using a sphygmomanometer. This is still recognized as the 'gold standard' for the measurement of blood pressure.

- In 2022, an estimated 2,200 metric tons of mercury was produced worldwide. It is mainly used in the manufacturing of electrical and electronic goods and industrial chemicals.

- However, environmental concerns regarding mercury have led to the imposition of bans in some European countries, and the supply of healthcare in the United Kingdom is now restricted. Mercury is considered by the World Health Organisation (WHO) as one of the top 10 chemicals or groups of chemicals of major public health concern.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is the largest market for mercury. In the Asia-Pacific region, China and Kyrgyzstan are the major producers of mercury. In addition to this, China has the world's largest mine production and reserves of mercury. Also, Mercury compounds were used as catalysts in the coal-based manufacture of vinyl chloride monomers in China.

- Therefore, China is the world's largest producer of mercury in 2022, with a mine production volume of 2,000 metric tons. The second leading producer of mercury, Tajikistan, produced approximately 120 metric tons in the same year.

- Globally, 10-20 million people work in the Artisanal and Small-Scale Gold Mining (ASGM) sector, and many of them use mercury on a daily basis.

- Artisanal and Small-Scale Gold Mining (ASGM) is the largest source of anthropogenic mercury emissions (37.7%) globally, followed by stationary combustion of coal (21%).

- According to USGS, China, Kyrgyzstan, Mexico, Peru, Russia, Slovenia, Spain, and Ukraine have most of the world's estimated 600,000 tons of mercury resources.

- Furthermore, Artisanal Small-Scale Gold Mining (ASGM) has extensive operations spanning over 55 countries across Asia, South America, and Africa. ASGM acts as a microeconomic source for these countries; however, ASGM has adverse environmental and health impacts.

- In China, the use of dental amalgams dates back to 1000 AD; today, dental amalgams consist of mercury and a metal alloy of silver, tin, and copper.

- All the aforementioned factors, in turn, are expected to augment the consumption of mercury in the region.

Mercury Industry Overview

The mercury market is partially fragmented in nature. The major players (not in any particular order) include Avantor Inc. (Thermo Fisher Scientific), AHSA, Aldrett Hermanos SA de CV, Merck KGaA, Wake Group, and China Jin Run Industrial Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Demand from Measuring and Controlling Devices

- 4.1.2 Demand for Sphygmomanometer for the Measurement of Blood Pressure

- 4.1.3 Widely Used in the Mining Sector for the Extraction of Gold

- 4.2 Restraints

- 4.2.1 Hazardous Properties of Mercury

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Metal

- 5.1.2 Alloy

- 5.1.3 Compounds

- 5.2 Application

- 5.2.1 Batteries

- 5.2.2 Dental Applications

- 5.2.3 Measuring and Controlling Devices

- 5.2.4 Lamps

- 5.2.5 Electrical and Electronics Devices

- 5.2.6 Processing of Gold

- 5.2.7 Other Applications (Healthcare, Pharmaceuticals, and Batteries)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.6 Saudi Arabia

- 5.3.7 South Africa

- 5.3.8 Nigeria

- 5.3.9 Qatar

- 5.3.10 Egypt

- 5.3.11 UAE

- 5.3.12 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share/Ranking Analysis**

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aldrett Hermanos

- 6.4.2 Antares Chem Private Limited

- 6.4.3 Avantor Performance Materials

- 6.4.4 Bethlehem Apparatus Co. Inc.

- 6.4.5 China Jin Run Industrial Co. Ltd

- 6.4.6 Mayasa

- 6.4.7 Merck KGaA

- 6.4.8 Powder Pack Chem

- 6.4.9 Special Metals

- 6.4.10 Tamilnadu Engineering Instruments

- 6.4.11 Wake Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 Growing Demand for Mercury in Niche Applications

9 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日