|

市場調査レポート

商品コード

1519949

金属接着剤:市場シェア分析、産業動向と統計、成長予測(2024~2029年)Metal Bonding Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 金属接着剤:市場シェア分析、産業動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

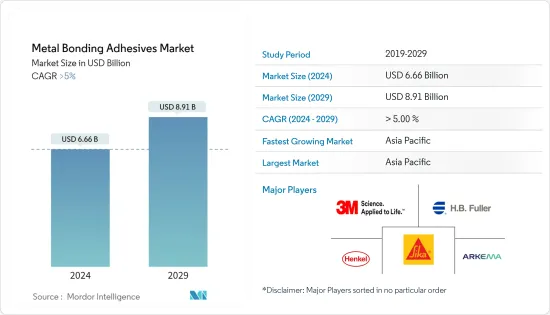

金属接着剤市場規模は2024年に66億6,000万米ドルと推計され、2029年には89億1,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは5%以上で成長する見込みです。

COVID-19の大流行は、サプライチェーンを混乱させ、生産の減速や停止、景気後退を引き起こし、金属接着剤市場に大きな影響を与えました。COVID-19の当初の影響はマイナスではありしたが、予測期間中、市場は回復基調にあるとみられます。

主なハイライト

- 市場を牽引している主な要因は、自動車・運輸業界の需要拡大です。

- その反面、各国間の地政学的緊張の高まりによる原料価格の変動が市場の成長を妨げています。

- バイオベース接着剤の革新と開発が市場に新たな機会をもたらします。

- アジア太平洋地域は最大の市場であり、中国、インド、日本などの国々からの消費増加により、予測期間中に最も急成長する市場になると予想されます。

金属接着剤市場の動向

自動車・運輸業界からの需要拡大

- OEMによって自動車および輸送産業で広く使用されており、シャーシの製作、自動車の外装、パネル接着、フレーム、および乗用車や大型車両の補強に用いられています。外装パネルとパネル接着は、自動車分野における主要な用途の一つです。

- さらに、航空宇宙産業では、金属接着剤は、最大限の耐久性、高強度、靭性、使用環境に応じて設計された耐熱性を持つように特別に設計されています。

- OICA(Organisation Internationale des Constructeurs d'Automobiles)によると、2022年には世界中で約8,501万台の自動車が生産され、2021年の8,020万5,000台と比較して5.99%の成長率を示しています。2022年には、世界中で約6,000万台の乗用車が生産され、2021年と比較して7.35%近く増加しました。

- アジア太平洋は、世界で最も価値のある自動車メーカーの本拠地です。中国、インド、日本、韓国などの新興諸国は、製造基盤を強化し、効率的なサプライチェーンを構築して収益性を高めるべく努力しています。

- Boeing Commercial Outlook 2023-2042によると、2042年までに新型民間ジェット機の需要は4万2,595機、金額にして8兆米ドルに達すると予想されています。世界のジェット機保有台数は、2042年までにほぼ倍増の48,600機となり、毎年3.5%ずつ拡大します。航空会社は、世界の航空機の約半分を、より燃費の良い新機種に入れ替えると思われます。

- 北米が9,250機で最大のシェアを占め、次いでユーラシア、中国と続き、2042年までの新型機納入総数は9,645機と推定され、航空業界の需要が高まっていることを示しています。

- 中国では、エアバスが2023年3月、ベストセラーの単通路ジェット機A320の生産を拡大し、販売を強化する計画を発表しました。中国は欧州の航空会社メーカーにとって最大市場の一つであり、これらの接着剤は航空機構造の軽量化や強度・耐疲労性の向上に使用されるため、この拡大は金属接着剤市場を大きく成長させると予想されます。

- 予測期間中、自動車と航空機の需要と生産の増加が市場を牽引するとみられます。

アジア太平洋地域が市場を独占する

- アジア太平洋地域の金属接着剤市場は、大きな市場シェアを占める中国での技術的に高度な家電製品や自動車生産に対する需要の増加により、大幅かつ急速な成長が見込まれます。

- 加えて、インド、タイ、インドネシア、中国における費用対効果の高い原材料と労働力のアクセス可能性に起因する製造拠点の移転は、産業やエレクトロニクス分野での多国籍企業による投資の増加とアジア太平洋地域における製造拠点を保持するために、市場プレーヤー間の競争の激化と相まって、この地域における金属接着剤の需要の増加を刺激する中心的な側面です。

- 中国の自動車製造業は世界最大です。同産業は2022年にわずかな成長を示し、生産と販売が増加しました。同様の動向は2021年も続き、2022年の生産台数は3%増となりました。中国汽車工業協会(CAAM)によると、BYD、上海汽車などの企業が燃料走行車や電気自動車分野で自動車生産の売上を伸ばしており、自動車生産は今後も成長すると予想されています。

- 中国汽車工業協会によると、中国の自動車メーカーは、2022年には690万台だった電気自動車とハイブリッド車の販売台数が、前年には約940万台になると予測しています。同協会はさらに、2024年の販売台数は引き続き増加し、1,150万台に達すると予測しています。

- 例えば、中国の自動車大手BYDは、2023年に300万台以上のバッテリー駆動車を販売しました。そのうち、160万台は完全電気自動車で、140万台はガソリンとバッテリーのハイブリッド車です。これらを合わせると、2022年と比べて62%の増加となります。さらに、BYDは昨年上半期に利益を3倍の15億米ドルにまで増やしたと報告しています。

- India Todayによると、2023年には国内市場で410万8,000台の自動車が販売されました。暦年で400万台を超えたのはこれが初めてです。2022年の販売台数は379万2,000台でした。インドでは、マルチ、ヒュンダイ、タタ、ホンダ、マヒンドラといった大手自動車メーカーが、売れ残り在庫のために生産を停止しています。これは近い将来、インドの自動車生産に大きな悪影響を及ぼすと予想されます。

- 中国は世界最大のヘルスケアセクターのひとつです。第13次5ヵ年計画では、中国政府は健康と技術革新を優先しており、予測期間中に医療機器製造セクターへの投資が増加すると予想されます。また、COVID-19の発生により、同国ではヘルスケア分野への投資が徐々に拡大しています。

- 金属接着剤は、溶接、リベット、ボルト締めといった従来の接合方法よりも数多くの利点を提供し、近代建築において重要な役割を果たしています。

- 中国の成長はまた、住宅や商業建築部門の急速な拡大と国の経済の拡大によって燃料を供給されています。中国は継続的な都市化プロセスを奨励し、それに耐えており、2030年までにその割合は70%に達すると予測されています。その結果、中国のような国々における建築活動の活発化が、この地域の接着剤産業に拍車をかけると予測されています。すべてのそのような要因は、地域全体の接着剤の需要を増加させる傾向があります。

- 中国国家統計局によると、建設生産額は2021年の29兆3,100億人民元(4兆2,000億米ドル)から増加し、2022年には31兆2,000億人民元(4兆5,000億米ドル)を占めます。さらに、住宅・都市・農村開発省の予測によると、中国の建設部門は2025年以降もGDPの6%を維持すると予想されています。

- Invest Indiaによると、 インドの建設業界は2025年までに1兆4,000億米ドルに達する見込みで、インドの建設業界は250のサブセクターにわたり、他のセクターと連携しており、PMAY-Uの技術サブミッションの下で特定された54以上の世界的な革新的建設技術が、新しい時代のインドの建設セクターを開始するために導入されています。

- さらに、アジア、北米、太平洋地域からの旺盛な需要により、韓国の建設業者の海外建築受注は2022年に3年連続で300億米国ドルを突破しました。

- したがって、上記の要因のおかげで、同国の金属接着剤の需要は同地域で急上昇しています。

金属接着剤産業の概要

金属接着剤市場は部分的に統合されています。主要企業(順不同)は、Henkel AG &Co.KGaA、3M、H.B. Fuller Company、アルケマ、シーカAGなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 自動車・運輸業界からの需要拡大

- 建設・インフラ分野からの消費増加

- その他の促進要因

- 抑制要因

- 厳しい規制政策

- 持続可能性への懸念

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 樹脂タイプ

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他の樹脂タイプ(バイオベース樹脂、ハイブリッド樹脂など)

- 用途

- 自動車および輸送

- 航空宇宙・防衛

- 電気・電子

- 産業用組立

- 建設・インフラ

- その他の用途(海洋、医療など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ノルディック

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Arkema

- Ashland

- Avery Dennison Corporation

- Beardow Adams

- DELO Industrie Klebstoffe GmbH & Co. KGaA5

- Dow

- DuPont

- H.B. Fuller Company

- Henkel AG & Co. KgaA

- Huntsman International LLC

- Hexion

- ITW Performance Polymers(Illinois Tool Works Inc.)

- Parker Hannifin Corp(Lord Corporation)

- Parson Adhesives Inc.

- Sika AG

- Solvay

第7章 市場機会と今後の動向

- バイオベース接着剤の革新と開発

- 複合材料の接着へのシフト

The Metal Bonding Adhesives Market size is estimated at USD 6.66 billion in 2024, and is expected to reach USD 8.91 billion by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

The COVID-19 pandemic significantly impacted the metal bonding adhesive market by disrupting the supply chain, causing production to slow down and shut down and an economic downturn. While the initial impact of COVID-19 was negative, the market appears to be on a recovery path during the forecast period.

Key Highlights

- Major factors driving the market studied are growing demand from the automotive and transportation industry.

- On the flip side, volatility in raw material prices, due to the rising geopolitical tensions between various nations is hindering the growth of the market.

- Innovation and development of bio-based adhesives to open new opportunities for the market.

- The Asia-Pacific region represents the largest market, and it is also expected to be the fastest-growing market over the forecast period, owing to the increasing consumption from countries, such as China, India, and Japan.

Metal Bonding Adhesives Market Trends

Growing Demand from the Automotive and Transportation Industry

- Metal bonding adhesives are widely used in the automotive and transportation industry by OEMs for fabricating chassis, automotive exteriors, panel bonding, frames, and reinforcement of the passenger, as well as heavy vehicles segment. Exterior panels and panel bonding are among the top applications in the automotive segment.

- Furthermore, in the aerospace industry, metal bonding adhesives are specifically designed for maximum durability, high strength, and toughness with temperature resistance designed for their operating environment.

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), in 2022, around 85.01 million vehicles were produced across the globe, witnessing a growth rate of 5.99% compared to 80.205 million vehicles in 2021, thereby indicating an increased demand for metal hoses from the automotive industry. In 2022, around 60 million passenger cars were manufactured worldwide, up nearly 7.35% compared to 2021.

- The Asia-Pacific is home to some of the world's most valuable vehicle manufacturers. Developing countries such as China, India, Japan, and South Korea have been working hard to strengthen the manufacturing base and develop efficient supply chains for greater profitability.

- According to the Boeing Commercial Outlook 2023-2042, the demand for new commercial jets by 2042 is expected to reach 42,595 units, valued at USD 8 trillion. The global fleet will nearly double to 48,600 jets by 2042, expanding by 3.5% annually. Airlines will replace about half of the global fleet with new, more fuel-efficient models.

- North America accounts for the largest share with 9,250 deliveries, followed byEurasia and China, with the total deliveries of new airplanes estimated to be 9,645 units by 2042, indicating rising demand from the industry.

- In China, Airbus announced plans in March 2023 to expand production of its best-selling A320 single-aisle jet and boost sales. China is one of the largest markets for European airline manufacturers, and this expansion is expected to significantly grow the metal bonding adhesives market as these adhesives are used in weight reduction and improving strength and fatigue resistance experienced by the aircraft structures.

- Over the forecast period, increasing demand and production of automotive vehicles and aircrafts are likely to drive the market.

The Asia-Pacific Region to Dominate the Market

- The Asia-Pacific metal bonding adhesives market is anticipated to witness significant and fastest growth, owing to the growing demand for technologically advanced consumer electronics and automobile production in China, which holds a significant market share.

- In addition, the relocation of manufacturing hubs due to the accessibility of cost-effective raw materials and labor in India, Thailand, Indonesia, and China, coupled with increasing investments by multinationals in the industrial and electronics sectors and growing competition among market players to hold a manufacturing base in the Asia-Pacific, is the central aspect stimulating the increasing demand for metal bonding adhesives in the region.

- The Chinese automotive manufacturing industry is the largest in the world. The industry witnessed a slight growth in 2022, wherein production and sales increased. A similar trend continued in 2021, with production witnessing a 3% incline in 2022. According to the China Association of Automobile Manufacturers (CAAM), automotive production is expected to grow in the future, with companies like BYD, SAIC Motors, and more increasing their automotive production sales in the fuel-run and electric vehicles segment.

- According to the China Association of Automobile Manufacturers, Chinese automakers are anticipated to report sales of approximately 9.4 million electric vehicles and hybrids in the previous year, up from 6.9 million in 2022. The association further projects a continued increase in sales for 2024, reaching 11.5 million units.

- For Example, China's automotive giant BYD sold over 3 million battery-powered cars in 2023, of which both batteries and gasoline power 1.6 million fully electric vehicles and another 1.4 million hybrids. Together, that is a 62 percent increase over 2022. BYD is also making money, tripling its profit to USD 1.5 billion in the first half of last year, according to BYD.

- According to India Today, 4,108,000 cars were sold in the domestic market in 2023. This was the first time during a calendar year that over 4 million units were sold in the country. In 2022, the industry witnessed sales of 3,792,000 units. In India, major automotive manufacturers, like Maruti, Hyundai, Tata, Honda, and Mahindra, have shut down their production owing to the unsold stock. This is expected to have a substantial negative impact on India's automotive production in the near future.

- China has one of the largest healthcare sectors in the world. Under the 13th Five-Year Plan, the Government of China prioritized health and innovation, which is expected to increase investments in the medical device manufacturing sector during the forecast period. Additionally, due to the COVID-19 outbreak, investment in the healthcare sector has been gradually growing in the country.

- Metal bonding adhesives play a crucial role in modern construction, offering numerous advantages over traditional joining methods like welding, riveting, or bolting.

- China's growth is also fueled by rapid expansion in the residential and commercial building sectors and the country's expanding economy. China is encouraging and enduring a continuous urbanization process, with a projected rate of 70% by 2030. As a result, increased building activity in nations like China is projected to fuel the region's adhesive industry. All such factors tend to increase the demand for adhesives across the region.

- According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.31 trillion (USD 4.2 trillion) in 2021. Moreover, as per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025.

- As per Invest India, the construction industry in India is expected to reach USD 1.4 Trillion by 2025, and the construction industry in India works across 250 sub-sectors with linkages across sectors and over 54 global innovative construction technologies identified under a Technology Sub-Mission of PMAY-U to start a new era in Indian Construction Sectors.

- Furthermore, South Korean builders' overseas building orders have surpassed 30 billion US dollars for the third consecutive year in 2022, owing to strong demand from Asia, North America, and the Pacific Ocean regions.

- Hence, owing to the factors mentioned above, the demand for metal bonding adhesives in the country has been on the rapid rise in the region.

Metal Bonding Adhesives Industry Overview

The Metal Bonding Adhesives market is partially consolidated in nature. The major players (not in any particular order) include Henkel AG & Co. KGaA, 3M, H.B. Fuller Company., Arkema and Sika AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Automotive and Transportation Industry

- 4.1.2 Increased Consumption from Construction and Infrastructure Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Regulatory Policies

- 4.2.2 Sustainability Concerns

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resin Types (Bio-Based Resins, Hybrid, etc.)

- 5.2 Application

- 5.2.1 Automotive and Transportation

- 5.2.2 Aerospace and Defense

- 5.2.3 Electrical and Electronics

- 5.2.4 Industrial Assembly

- 5.2.5 Construction and Infrastructure

- 5.2.6 Other Applications (Marine, Medical, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Beardow Adams

- 6.4.6 DELO Industrie Klebstoffe GmbH & Co. KGaA5

- 6.4.7 Dow

- 6.4.8 DuPont

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KgaA

- 6.4.11 Huntsman International LLC

- 6.4.12 Hexion

- 6.4.13 ITW Performance Polymers (Illinois Tool Works Inc.)

- 6.4.14 Parker Hannifin Corp (Lord Corporation)

- 6.4.15 Parson Adhesives Inc.

- 6.4.16 Sika AG

- 6.4.17 Solvay

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation and Development of Bio-based Adhesives

- 7.2 Shifting Focus Towards Adhesive Bonding for Composite Materials