|

市場調査レポート

商品コード

1910722

液体屋根材:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Liquid Roofing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 液体屋根材:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

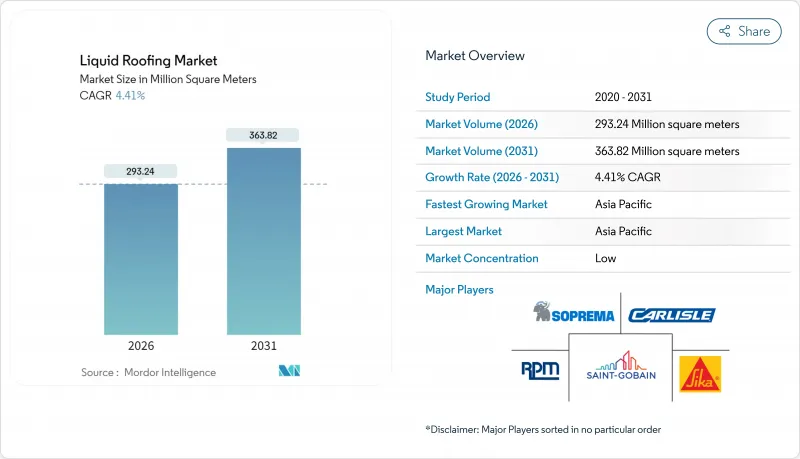

液体屋根材市場は、2025年の2億8,085万平方メートルから2026年には2億9,324万平方メートルへ成長し、2026年から2031年にかけてCAGR4.41%で推移し、2031年までに3億6,382万平方メートルに達すると予測されております。

急速なインフラ近代化、頻発する暴風雨、より厳格なエネルギー基準により、屋根の張り替えサイクルが短縮され、現場硬化型のシームレスコーティング材への仕様選択が促進されております。施工業者は、切断や溶接を必要とせず貫通部を包み込む液体系システムを好んで採用しており、これにより漏水リスクと現場の廃棄物が低減されます。揮発性有機化合物(VOC)の許容値を厳格化する規制の動きは、水性化学製品をさらに有利にしており、一方でクールルーフに対する政府の優遇措置は、高温地域および温帯地域における採用を促進しています。同時に、プライベート・エクイティによる買収の波が流通網を再構築しており、入札決定において供給の確実性が価格と同等の重要性を帯びてきています。

世界の液体屋根材市場の動向と洞察

気候変動による異常気象を背景とした屋根改修需要の急増

強風、雹、降水量の激化により、建物所有者は保証期間満了前に老朽化した屋根の改修を迫られています。液体システムは湿潤環境下でも硬化し、トーチ溶接や溶剤溶接を必要とせずに微細なひび割れを補修できる点で優れています。カテゴリー4の暴風雨後には請負業者に数ヶ月分の受注が積み上がり、保険会社は将来の保険金請求を軽減するシームレスなコーティング(連続膜)を優先します。自治体の復興資金は、特にハリケーン多発地域にある学校や医療施設を対象とした公共屋根改修プログラムを加速させています。既存の基材上に液体製品をスプレーまたはローラーで塗布できる特性は、埋立処分費用の削減につながり、暴風雨被害を受けた構造物の早期再利用を促進します。

現場のダウンタイムを短縮する速硬化ポリウレアおよびハイブリッドシステム

純粋なポリウレア膜はわずか30秒で完全硬化を達成し、当日中の歩行可能化と機械設備工事の迅速な準備を可能にします。ハイブリッドアクリル・ポリウレタン系化学組成は低コストと乾燥加速を両立し、施工業者が閑散期における日次生産枠の拡大を実現します。施設管理者は営業を中断せずに小売店舗の上部屋根を修復できる選択肢を高く評価しています。早期導入事例としては、稼働停止が直接的な処理能力の損失につながる物流倉庫や、継続的な環境制御を必要とするデータセンターが挙げられます。硬化プロファイルの改善に伴い、設計者は厳しいスケジュールが課せられた重要工程プロジェクトにおいても、液体材料の導入に確信を持てるようになりました。

揮発性のイソシアネートとアスファルト価格の高騰が請負業者の利益率を圧迫

ポリウレタン液体システムはMDIやHDIなどのイソシアネートモノマーに依存していますが、2024年に欧州工場のメンテナンス停止に伴い、その価格が15~20%急騰しました。中小規模の屋根工事業者は、発注がスポット価格に切り替わったことで資金繰りに苦慮しました。この価格変動は、石油化学派生品を使用しない水性アクリル系やシリコーン系への代替を加速させています。大量発注契約を結んでいる請負業者は、原材料まで遡って統合するサプライヤーを通じてコスト変動をヘッジしています。大手OEMメーカーは追加料金の転嫁が容易なため、競合格差が拡大し、さらなる業界再編が進んでいます。

セグメント分析

アクリル系塗料は2025年需要の51.47%を占め、VOC規制やクールルーフ基準への適合性が評価されました。ポリマーの継続的改良による引張強度と耐水溜まり性の向上により、2031年までCAGR4.74%が見込まれます。アクリル系液状屋根材の市場規模は、幅広い下地材との適合性により支えられており、施工業者は老朽化した単層防水シートを撤去せずに再塗装が可能です。ポリウレタン系システムは、優れた耐摩耗性が求められる化学処理施設や冷蔵施設において依然として不可欠ですが、価格感応度の高さが拡大を抑制しています。シリコーン系製品は、年間紫外線曝露日数が300日を超える砂漠気候地域で足場を固めています。

アクリル系製品の採用は、清掃の容易さと設備投資の低さからも恩恵を受けており、ローラーやエアレススプレー装置を備えた小規模な施工業者も参入が可能となります。水性技術への規制移行により、溶剤系アスファルト製品の市場浸食が加速しています。エポキシ樹脂やPMMA(ポリメチルメタクリレート)といったニッチソリューションは、石材や歴史的基材への接着性がコストを上回る重工業分野や歴史的建造物分野で活用されています。全体として、今後施行されるマイクロプラスチック排出規制に適合可能な化学製品が将来のシェアを獲得する見込みです。

液体屋根材レポートは、タイプ別(ポリウレタンコーティング、アクリルコーティング、アスファルト系コーティング、シリコーンコーティングなど)、用途別(ドーム屋根、傾斜屋根、平屋根)、エンドユーザー産業別(住宅、商業、産業/公共施設、インフラ)、地域別(アジア太平洋、北米、欧州など)に分類されています。市場予測は数量(平方メートル)ベースで提供されます。

地域別分析

アジア太平洋地域は2025年に世界の41.18%を占め、2031年までCAGR4.82%で拡大が見込まれます。これは、現場硬化型防水シートを好む鉄道、空港、データセンターのパイプラインに支えられています。中国では地方都市の改修補助金により老朽化した住宅団地の防水改修が推進され、インドではスマートシティ入札に屋根冷却システムが組み込まれています。ASEAN諸国では官民連携による学校・診療所で液体仕様を推進し、維持管理予算の削減を図っています。インドネシアやベトナムでは、地域に混合プラントを保有するサプライヤーが国境を越えた物流上の摩擦を軽減し、現地調達規制を満たしています。

北米市場は、2005年から2010年に建設された小売大型店舗や倉庫の屋根の交換サイクルにより、依然として重要な市場です。インフラ投資・雇用法により、交通拠点や水処理施設への資金が投入され、付属建物に液体防水が採用されています。コロラド州などの州では、エネルギー基準の改訂によりカリフォルニア州の反射率基準が採用され、アクリル系白色屋根の需要が刺激されています。テキサス州とオクラホマ州における激しい雹害の発生により、耐衝撃性ポリウレタンエラストマーを用いた屋根の張り替えが加速しております。

欧州では、高揮発性有機化合物(VOC)含有材料の段階的廃止による環境規制順守が重視され、クールルーフ導入に対して固定資産税控除による優遇措置が講じられています。ドイツで提案されているグリーン刺激策では公共建築物の改修が優先され、歴史的スレート屋根の外観を損なわずにシリコーン系トップコートを施工する機会が生まれています。英国では「未来の住宅基準」の実現に向け、夏季の過熱を抑制する反射性防水シートの採用を建設業者に促しています。南欧のホスピタリティリゾートでは、閑散期に実施される防水塗装工事中の宿泊客移転を回避するため、液体防水材の採用が指定されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 気候変動による異常気象を背景とした屋根改修需要の急増

- 速硬化ポリウレアおよびハイブリッドシステムによる現場のダウンタイム削減

- 米国およびEUにおける遮熱・反射屋根への税制優遇措置

- アジア太平洋地域の主要都市におけるインフラ刺激策

- ドローンを活用したスプレー式施工による労働生産性の向上

- 市場抑制要因

- イソシアネート及びアスファルト価格の変動が請負業者の利益率を圧迫しております

- 高揮発性有機化合物(VOC)製品に対する地域的な禁止措置

- 新興経済国における熟練施工者の不足

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- ポリウレタンコーティング

- アクリルコーティング

- アスファルト系コーティング

- シリコーンコーティング

- エポキシ樹脂コーティング

- その他のタイプ

- 用途別

- ドーム型屋根

- 切妻屋根

- 平屋根

- エンドユーザー産業別

- 住宅用

- 商業用

- 産業・機関

- インフラ

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- 3M

- Akzo Nobel N.V.

- Alumasc Building Products

- Carlisle Companies Incorporated

- Fosroc, Inc.

- Garland Company, Inc.

- Johns Manville(A Berkshire Hathaway Company)

- Kemper System Ltd

- Langley UK Ltd

- Mapei S.p.A.

- PPG Industries, Inc.

- RPM INTERNATIONAL INC.

- Saint-Gobain

- SIG plc

- Sika AG

- SOPREMA Group

- Standard Industries Inc.