|

市場調査レポート

商品コード

1519945

電池原料:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Battery Raw Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電池原料:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

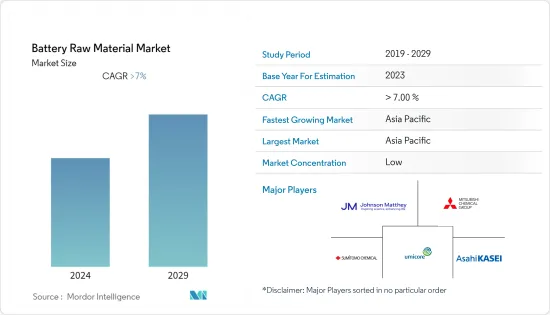

電池原料市場規模は2024年に587億米ドル、2029年には972億3,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは10.62%で成長します。

COVID-19パンデミックは電池材料市場を混乱させました。封鎖措置、工場閉鎖、移動制限により、採鉱作業、鉱石加工施設、物流網が混乱し、原材料の供給に影響が出ました。自動車、エレクトロニクス、エネルギーなど各産業の経済活動の再開が電池原料市場の回復に寄与しました。

主なハイライト

- 電池原料市場は、自動車や家電分野での使用増加により急速に拡大しています。

- しかし、電池原料市場の成長は、電池の保管・輸送に関する厳しい安全規制によって阻害されると予想されます。

- バナジウムフロー技術の研究開発活動の高まりと、携帯電子機器や消費者向け機器の需要の増加は、今後数年間、電池原料市場に機会をもたらすと予想されます。

- 中国やインドなどの国々で自動車用バッテリーや家電用バッテリーの消費が伸びていることが、アジア太平洋地域が世界市場を支配する要因となっています。

電池原料市場の動向

市場を独占する自動車セグメント

- 電気自動車の急速な普及に伴い、自動車産業は大きな変革期を迎えています。重要なエネルギー貯蔵であるリチウムイオン電池には、様々な重要な原材料が必要とされます。EVの販売が世界的に急増を続ける中、これらの電池原料の需要が急増し、電池原料市場の自動車分野の成長を牽引しています。

- 国際自動車工業会(OICA)が発表した推計によると、2022年には世界中で約8,163万台の自動車が販売されます。

- さらに、連邦自動車交通局(フレンスブルク)によると、ドイツにおけるバッテリー電気自動車の総登録台数は、2020年の136,617台から2023年には1,013,009台に増加します。

- 家電・自動車分野では、中国、日本、韓国、インドなどのアジア太平洋諸国が電池原料の使用量を大きく伸ばしており、予測期間中の市場の牽引役となることが予想されます。

- 世界のEV充電インフラの拡大は、EVに対する消費者の信頼を高め、電気自動車の普及に拍車をかけています。政府、電力会社、非公開会社は、充電ステーション、急速充電ネットワーク、スマートグリッド技術の導入に多額の投資を行っています。こうして、EVの保有台数の増加を支えています。このようなインフラ整備は、車載用リチウムイオン電池の需要増に対応するため、電池原料の堅調な市場を生み出しています。

- 連邦ネットワーク庁が発表したデータによると、ドイツには2023年10月時点で、EV用の平均速度充電が可能な公共サイトが8万7,155カ所、公共急速充電ステーションが2万1,111カ所あります。

- 電気自動車の普及拡大は、クリーンエネルギー政策と一致しています。中国政府は、需要に対する供給ギャップを縮小するため、自動車メーカーによる中国への自動車輸入規制を緩和する意向です。

- 予測期間中、電池材料市場は上記のすべての要因によって牽引されると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋は、自動車からエレクトロニクス、再生可能エネルギーに至るまで、幅広い分野の重要な製造拠点です。この地域には、多数の電池メーカー、電池セルメーカー、電池原料サプライヤーが存在します。このように製造施設が集中していることが、アジア太平洋における電池原料の需要を牽引しています。

- アジア太平洋の電気自動車市場は、中国、日本、韓国などの国々で急速に成長しています。これらの国々は世界最大の電気自動車の生産国であり消費国でもあります。電気自動車用リチウムイオン電池の生産には、リチウム、コバルト、ニッケル、黒鉛などの電池原料が大量に必要であり、これが電池原料市場におけるアジア太平洋の優位性につながっています。

- 中国汽車工業協会(CAAM)が発表したデータによると、中国では2022年に約540万台のバッテリー電気自動車が販売され、2021年比で83.5%増加しました。同年、中国でのプラグインハイブリッド車の販売台数は前年比151.91%増の150万台以上となりました。

- 日本の自動車検査登録情報協会(AIRIA)が発表したデータによると、2023年に日本で使用される電気乗用車の台数は約16万2,390台となり、10年前より増加しました。

- インドでは、Vahanのデータによると、2023年3月のEV販売台数は139,789台で、2022年3月の77,128台に比べ、前年同月比82%増加しました。合計すると、2022年度の4,58,746台から11,80,597台へと、157%もの驚異的な伸びを示しました。

- したがって、予測期間中の同地域における電池原料の需要は、これらすべての市場開拓によって牽引されると予想されます。

電池原料業界の概要

電池原料市場は断片化されており、少数の大手プレーヤーと多数の小規模プレーヤーが存在します。主要企業(順不同)には、Umicore、Asahi Kasei Corporation、Johnson Matthey、Sumitomo Chemical、Mitsubishi Chemical Corporationが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- コンシューマー・エレクトロニクスからの需要拡大

- 自動車産業におけるアプリケーションの増加

- 抑制要因

- 電池の保管・輸送に関する厳しい安全規制

- その他の抑制要因

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

第5章 市場セグメンテーション(金額ベース市場規模)

- 電池タイプ別

- 鉛蓄電池

- リチウムイオン

- その他の電池タイプ(ニッケル水素電池、固体電池)

- 原料別

- 正極

- 負極

- 電解液

- セパレーター

- 用途別

- 家電

- 自動車

- 産業用

- 通信用

- その他(再生可能エネルギー貯蔵)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- タイ

- マレーシア

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- トルコ

- ロシア

- ノルディック

- その他欧州

- 世界のその他の地域

- 南米

- 中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Asahi Kasei Corporation

- BASF SE

- Celgard LLC

- ENTEK

- ITOCHU Corporation

- Johnson Matthey

- Mitsubishi Chemical Corporation.

- NICHIA CORPORATION

- Sumitomo Chemical Co. Ltd

- Targray Technology International Inc.

- Umicore

第7章 市場機会と今後の動向

- 電池におけるバナジウムフロー技術の研究開発

- ポータブル電子機器と消費者向け機器の需要増加

The Battery Raw Material Market size is estimated at USD 58.70 billion in 2024, and is expected to reach USD 97.23 billion by 2029, growing at a CAGR of 10.62% during the forecast period (2024-2029).

The COVID-19 pandemic disrupted the battery materials market. Lockdown measures, factory closures, and restrictions on movement led to disruptions in mining operations, ore processing facilities, and logistics networks, impacting the supply of raw materials. The resumption of economic activities across industries, including automotive, electronics, and energy, contributed to the recovery of the battery raw materials market.

Key Highlights

- The market for battery raw materials is proliferating due to the increasing use of these products in the automotive and consumer electronics sectors.

- However, the growth of the battery raw materials market is expected to be hampered by strict safety regulations for batteries through storage and transport.

- The rising research and development activities in vanadium flow technology and increasing demand for portable electronics and consumer devices are expected to provide opportunities for the battery raw material market in the coming years.

- The growing consumption of automotive and consumer electronics batteries in countries such as China and India is driving Asia-Pacific to dominate the global market.

Battery Raw Material Market Trends

Automotive Segment to Dominate the Market

- With the rapid rise in the adoption of electric vehicles, the car industry is undergoing a significant change. Various critical raw materials are required for the Lithium-ion battery, which is a crucial energy storage. As EV sales continue to surge globally, the demand for these battery raw materials has skyrocketed, driving growth in the automotive segment of the battery raw materials market.

- According to the estimate released by the International Organization of Motor Vehicle Manufacturers (OICA), around 81.63 million vehicles were sold around the world in 2022.

- Furthermore, according to the Federal Motor Transport Authority, Flensburg, the registration of the total number of battery electric cars in Germany increased from 136,617 units in 2020 to 1,013,009 units in 2023.

- In the consumer electronics and automotive sectors, Asia-Pacific countries such as China, Japan, South Korea, and India are experiencing strong growth in the use of battery raw materials, which is expected to drive the market over the forecast period.

- The expansion of EV charging infrastructure worldwide has bolstered consumer confidence in EVs and fueled the adoption of electric vehicles. Governments, utilities, and private companies are investing heavily in the deployment of charging stations, fast-charging networks, and smart grid technologies. Thus, this supports the growing fleet of EVs. This infrastructure development has created a robust market for battery raw materials to meet the increasing demand for lithium-ion batteries in automotive applications.

- According to the data published by the Federal Network Agency, in Germany, there were 87,155 public sites with average speed recharging for EVs available in October 2023 and 21,111 public quick charge stations.

- The increase in the adoption of electric vehicles aligns with the clean energy policy. The Chinese government intends to relax restrictions on the import of vehicles by automobile manufacturers into China in order to narrow the supply gap for demand.

- The market for battery materials is expected to be driven by all of the above factors during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is an important manufacturing hub for a wide range of sectors, from automotive to electronics and renewables. The region hosts a large number of battery manufacturers, cell producers, and suppliers of battery raw materials. This concentration of manufacturing facilities drives demand for battery raw materials in Asia-Pacific.

- The Asia-Pacific market for electric vehicles is growing at a rapid rate in countries such as China, Japan, and South Korea. These countries are the biggest producers and consumers of electric vehicles in the world. The production of lithium-ion batteries for EVs requires significant quantities of battery raw materials such as lithium, cobalt, nickel, and graphite, contributing to the dominance of Asia-Pacific in the battery raw materials market.

- According to the data published by the China Association of Automobile Manufacturers (CAAM), in China, approximately 5.4 million battery electric vehicles were sold in 2022, an increase of 83,5 % compared to 2021. In the same year, there was an increase of 151.91% in sales of plugin hybrids to over 1.5 million vehicles in China from a year earlier.

- According to the data published by the Automobile Inspection & Registration Information Association, Japan (AIRIA), in 2023, the number of electric passenger cars in use in Japan increased to about 162.39 thousand vehicles, which was an increase from 10 years ago.

- In India, according to Vahan's data, EV sales in March 2023 increased by 82 % Y-o-Y, with 1,39,789 units sold compared to 77,128 EVs sold in March 2022. In total, sales increased by a staggering 157% in the period, from 4,58,746 to 11,80,597 during fiscal year 2022.

- Therefore, the demand for battery raw materials in the region during the forecast period is expected to be driven by all these market developments.

Battery Raw Material Industry Overview

The battery raw material market is fragmented, with the presence of a few large-sized players and a large number of small players operating. The major players (not in any particular order) include Umicore, Asahi Kasei Corporation, Johnson Matthey, Sumitomo Chemical Co. Ltd, and Mitsubishi Chemical Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Consumer Electronics

- 4.1.2 Rising Application in Automotive Industry

- 4.2 Restraints

- 4.2.1 Stringent Safety Regulations for Batteries through Storage and Transportation

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Battery Type

- 5.1.1 Lead-acid

- 5.1.2 Lithium-ion

- 5.1.3 Other Battery Types (Nickel-metal Hydride (NiMH), and Solid-state Batteries)

- 5.2 By Material

- 5.2.1 Cathode

- 5.2.2 Anode

- 5.2.3 Electrolyte

- 5.2.4 Separator

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive

- 5.3.3 Industrial

- 5.3.4 Telecommunication

- 5.3.5 Other Applications (Renewable Energy Storage)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Thailand

- 5.4.1.6 Malaysia

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Turkey

- 5.4.3.7 Russia

- 5.4.3.8 NORDIC

- 5.4.3.9 Rest of Europe

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Asahi Kasei Corporation

- 6.4.2 BASF SE

- 6.4.3 Celgard LLC

- 6.4.4 ENTEK

- 6.4.5 ITOCHU Corporation

- 6.4.6 Johnson Matthey

- 6.4.7 Mitsubishi Chemical Corporation.

- 6.4.8 NICHIA CORPORATION

- 6.4.9 Sumitomo Chemical Co. Ltd

- 6.4.10 Targray Technology International Inc.

- 6.4.11 Umicore

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Research and Development in Vanadium Flow Technology in Batteries

- 7.2 Increasing Demand for Portable Electronics and Consumer Devices