|

市場調査レポート

商品コード

1641847

サードパーティ決済:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Third Party Payment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| サードパーティ決済:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 108 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

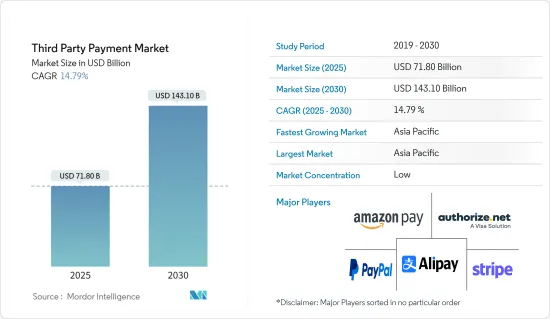

サードパーティ決済の市場規模は2025年に718億米ドルと推計され、2030年には1,431億米ドルに達すると予測され、市場推計・予測期間(2025-2030年)のCAGRは14.79%です。

サードパーティ決済には、ペイメントプロセッサーやペイメントアグリゲーター、またはクレジットカード処理会社が含まれ、加盟店は加盟店アカウントを必要とせずにクレジットカード決済やオンライン取引、その他のキャッシュレス方式を受け入れることができます。PayPal、Stripeなどを含むこれらのサードパーティ決済ソリューションプロバイダーは、加盟店の業務運営を簡素化し、簡単な決済フローと取引を保証し、サードパーティ決済ソリューションの市場需要を支えています。

主なハイライト

- eコマースのビジネスソリューションは、国境を越えた取引や国際的な決済を実現するために進化しています。オンラインショッピングプラットフォームはシームレスなAPI統合を活用し、企業と顧客の安全で効率的な購買体験を保証しています。決済ゲートウェイ・サービスやプラグインは、銀行やさまざまなプロバイダーから直接入手できます。これは、eコマース分野での応用による研究市場の需要を示しています。

- インターネットへのアクセスが普及するにつれ、個人や企業は金融取引のためにデジタル・チャネルを利用するようになった。この動向は、便利で安全なオンライン決済ソリューションを提供するサードパーティ決済プロバイダーの成長にとって有益な環境を生み出しています。

- テクノロジープロバイダーがクラウドベースの決済ソリューションをイントロダクションとして導入することで、小売業者が消費者の期待の変化に対応できるようになり、成長がさらに加速しています。例えば、SAP SEは2024年3月、変化する顧客の期待を先取りする小売業者を支援する新しいコンポーザブル決済ソリューションを発表しました。この新ソリューション「SAP Commerce Cloud」はオープンな決済フレームワークで、BNPL(Buy Now, Pay Later)などの新しい決済オプションが普及するにつれて、小売業者がより機敏に対応できるようになります。

- セキュリティとプライバシーに関する懸念は、世界のサードパーティ決済市場の成長を大きく阻害し、消費者の信頼と規制遵守に直接影響を及ぼしています。金融情報や個人情報を含む決済データは機密性が高いため、サードパーティ決済プラットフォームはサイバー犯罪者の格好の標的となっています。データ漏洩やサイバー攻撃は、不正取引、なりすまし、金融詐欺につながる可能性があります。消費者はますます取引の安全性を優先するようになっているため、強固なセキュリティ対策を実施できないプラットフォームは、より安全性の高い代替プラットフォームに市場シェアを奪われるリスクがあります。

サードパーティ決済市場の動向

モバイルが大きく成長

- IT技術の進歩により、小売業やeコマースなどのエンドユーザーがサードパーティ決済プラットフォーム(3PP)と提携し、消費者にモバイル決済サービスを提供するケースが増えています。3PPがサプライチェーンに統合されることで、キャッシュフロー・ダイナミクスが変化するだけでなく、消費者の価格感応度が低下し、クレジットベースの購入が促進されることで需要が高まる。モバイル・ペイメント・ソリューションは、モバイルPOSシステムまたはスマートフォンやタブレット端末などのデバイスを利用して、あらゆる場所で商品やサービスの支払いをシームレスに受け付けることを可能にします。

- モバイルサードパーティ決済システムは、主にその安全性、効率性、利便性により、対面での顧客取引を促進するために大きな人気を博しています。近年、インターネットの進化とスマート・モバイル・デバイスの普及により、個人のライフスタイルや娯楽の嗜好が大きく変化しています。サードパーティーモバイルペイメントソリューションの台頭と進化は、こうした変化の主な要因のひとつです。サードパーティーモバイルペイメントが進化を続ける中、ユーザーがこれらの支払方法を採用する意欲に影響を与える決定要因も継続的に更新されるであろう。

- インターネットへのアクセスやスマートフォンの利用が増加したことは、インドのデジタル環境の向上に大きく寄与しています。Internet and Mobile Association of Indiaのレポートによると、2023年までにインドのインターネットユーザー数は8億人に達すると予測されています。このようなインターネット接続の急増は、おサイフケータイユーザーの増加にも貢献すると予想され、2025年には9億人に達すると予測されています。

- GSMAによると、2023年末までに世界人口の69%にあたる56億人がモバイルサービスに加入するといいます。これは2015年から16億人増加したことになります。モバイルインターネット利用の拡大はさらに顕著です。2023年末までに、世界人口の58%がモバイルインターネットを利用し、そのユーザー数は47億人に達し、2015年以来21億人の増加となります。さらに、2023年末までに5G接続数は16億に達し、2030年には55億に増加すると予測されているといいます。このようなモバイルインターネット接続の著しい成長は、サードパーティ決済市場の可能性を押し上げると思われます。

アジア太平洋が大きな成長を遂げる

- 技術革新、規制状況の変化、消費者の嗜好の変化により、アジア太平洋地域の決済状況は大きく変わりつつあります。

- Worldpayが2024年3月に発表した「Global Payments Report 2024」によると、アリペイやウィーチャットペイといった中国企業とマレーシアのグラブペイがシンガポールの電子財布市場で圧倒的な地位を占めており、合計で35.3%という驚異的な市場シェアを誇っています。しかし、Gojekが開発したインドネシアのGoPayも重要なプレーヤーであることは注目に値します。戦略的な動きとして、真に世界なプレゼンスを持つウォレットであるPayPalは、2023年12月にGoPayの買収を発表しました。

- これらの決済プラットフォームは、金融サービス、eコマース、日常的な公共サービスをシームレスに統合し、多様な消費者ニーズに対応するエコシステムを形成しています。アジアのさまざまな地域で普及している電子財布は、プロンプトペイやMoMoなど、タイやベトナムの離島でさえ、観光客や地元のベンダーに代替決済手段を提供しています。さらに、モバイル決済手段は、特に銀行口座を持たない人々の金融包摂を促進する上で革命的なものとなっています。

- さらに、中国やインドのような国々では、デジタル決済にモバイル・ウォレットを採用する動きが加速しており、アジア太平洋市場の大幅な成長に拍車をかけています。モバイルデバイスの普及、強固なデジタルインフラ、アプリケーションの人気の高まりが、アジア太平洋地域におけるデジタル/モバイルウォレットの急速な拡大を後押ししています。

- この地域の銀行は、安全な取引を促進し、観光産業をサポートするために、サードパーティの決済サービスプロバイダーと協力しています。例えば、2024年6月、モンゴルの最高級フルサービス銀行であるハーン銀行と、アント・インターナショナルが提供する国境を越えたモバイル決済ソリューションであるアリペイ・プラス(Alipay+)との提携により、8カ国・地域の12の人気海外eウォレットのユーザーは、モンゴルでシームレスにデジタル・モバイル決済ができるようになった。

サードパーティ決済業界の概要

サードパーティ決済市場は競争が激しく、細分化されています。かなり以前からこのビジネスに参入しているプレーヤーもいます。その後、多くの新興企業がこの市場の巨大な機会を捉えようとしています。特定の地域にのみ進出しているプレーヤーもいます。主なプレーヤーには、PayPal Holdings Inc.、Stripe Inc.、Alipay.com、Amazon Payments Inc.

サードパーティ決済市場は、競争の激しい市場空間で差別化ポイントを獲得することに注力するプレーヤーで構成されています。新しい新興企業が市場を牽引しています。

この市場の特徴は、製品の差別化が緩やかであること、製品の普及レベルが高まっていること、市場で優位に立とうとする技術革新のレベルが高く競争が激しいことです。

予測期間中、企業集中率はさらに高まると予想されます。複数のソフトウェア企業が、この市場を自社製品を統合し、提携や買収に踏み切る好機と考えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリーと主要調査結果

第4章 市場洞察

- 市場概要

- 業界のバリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- インターネットの普及によるデジタル決済の普及

- クラウドベースのシステムによるB2B販売の成長とPOSセグメントの売上増加

- 世界の高成長地域におけるeコマースの成長

- 市場抑制要因

- セキュリティとプライバシーへの懸念が市場を抑制

第6章 市場セグメンテーション

- タイプ別

- オンライン

- モバイル

- POS

- エンドユーザー別

- BFSI

- 小売

- eコマース

- その他エンドユーザー

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- PayPal Holdings Inc.

- Stripe Inc.

- Alipay.com Co. Ltd

- Amazon Payments Inc.(Amazon.com Inc.)

- Authorize.Net(Visa Inc.)

- WePay Inc.(JPMorgan Chase & Co.)

- 2Checkout.com Inc.(VeriFone Inc.)

- Adyen NV

- First Data Corporation(Fiserv Inc.)

- One97 Communications Limited(Paytm)

第8章 投資分析

第9章 市場機会と今後の動向

The Third Party Payment Market size is estimated at USD 71.80 billion in 2025, and is expected to reach USD 143.10 billion by 2030, at a CAGR of 14.79% during the forecast period (2025-2030).

Third-party payment includes payment processors and payment aggregators or credit card processing companies, enabling merchants to accept credit card payments, online transactions, and other cashless methods without requiring their merchant accounts. These third-party payment solution providers, including PayPal, Stripe, and others, can simplify business operations for merchants, ensuring easy payment flows and transactions and supporting the market demand for third-party payment solutions.

Key Highlights

- E-commerce business solutions are evolving to perform cross-border transactions and international payments. Online shopping platforms leverage seamless API integration, ensuring businesses and customers a secure and efficient purchasing experience. Payment gateway services and plugins are available directly from banks and various providers. This shows the demand for the studied market due to their applications in the e-commerce sector.

- As internet access becomes more widespread, individuals and businesses turn to digital channels for their financial transactions. This trend has created a beneficial environment for the growth of third-party payment providers offering convenient and secure online payment solutions.

- Technology providers' introduction of cloud-based payment solutions to help retailers meet changing consumer expectations further augments growth. For instance, in March 2024, SAP SE introduced a new composable payment solution to help retailers stay ahead of changing customer expectations. This new solution, SAP Commerce Cloud, is an open payment framework that helps retailers become more agile as new payment options such as buy now, pay later (BNPL) gain popularity.

- Security and privacy concerns significantly challenge the growth of the third-party payments market globally, directly affecting consumer trust and regulatory compliance. The sensitive nature of payment data, including financial and personal information, makes third-party payment platforms prime targets for cybercriminals. Data breaches or cyberattacks can lead to unauthorized transactions, identity theft, or financial fraud. Since consumers increasingly prioritize transaction security, platforms that fail to implement robust security measures risk losing market share to more secure alternatives.

Third Party Payment Market Trends

Mobile Witness Major Growth

- The advancement of information technology has led to a growing number of end users, such as those in retail and e-commerce, collaborating with third-party payment platforms (3PPs) to offer mobile payment services to consumers. The integration of 3PPs into supply chains not only alters cash flow dynamics but also reduces consumer price sensitivity and enhances demand by promoting credit-based purchases. Mobile payment solutions enable the seamless acceptance of payments for goods or services at any location, utilizing mobile point-of-sale systems or devices such as smartphones and tablets.

- Mobile third-party payment systems have gained significant popularity for facilitating in-person customer transactions, primarily due to their security, efficiency, and convenience. In recent years, the ongoing advancement of the Internet and the widespread adoption of smart mobile devices have significantly transformed individuals' lifestyles and entertainment preferences. The rise and evolution of third-party mobile payment solutions are among the key factors contributing to these changes. As third-party mobile payment continues to evolve, the determinants influencing users' willingness to adopt these payment methods will also undergo continuous updates.

- The rise in internet access and smartphone usage has been instrumental in enhancing the digital landscape in India. A report from the Internet and Mobile Association of India projects that the number of Internet users in the country will approach 800 million by 2023. This surge in internet connectivity is anticipated to contribute to a corresponding increase in mobile wallet users, which is expected to reach 900 million by 2025.

- GSMA said that by the end of 2023, 5.6 billion individuals, or 69% of the global population, had subscribed to a mobile service. This marks an increase of 1.6 billion since 2015. The expansion of mobile internet usage has been even more pronounced. By the end of 2023, 58% of the global population utilized mobile internet, amounting to 4.7 billion users, which represents a rise of 2.1 billion since 2015. Moreover, it said that by the end of 2023, the number of 5G connections reached 1.6 billion, and it is projected to increase to 5.5 billion by the year 2030. Such significant growth in mobile internet connectivity will drive the potential of the third-party payment market.

Asia-Pacific Witness Major Growth

- Technological innovations, regulatory shifts, and changing consumer preferences are reshaping the payment landscape in the Asia-Pacific region.

- According to the Global Payments Report 2024, published by Worldpay in March 2024, Chinese companies such as Alipay and WeChat Pay, along with Malaysia's GrabPay, command a dominant position in Singapore's e-wallet market, collectively holding an impressive 35.3% market share. However, it's worth noting that Indonesia's GoPay, developed by Gojek, is also a significant player. In a strategic move, PayPal, a wallet with a truly global presence, announced its acquisition of GoPay in December 2023.

- These payment platforms seamlessly integrate financial services, e-commerce, and daily utilities, forming an ecosystem that addresses diverse consumer needs. E-wallets, prevalent in various Asian regions, provide tourists and local vendors on even the most remote Thai and Vietnamese islands with alternative payment options, such as PromptPay and MoMo. Furthermore, mobile payment methods have been revolutionary, especially in promoting financial inclusion for the unbanked.

- Additionally, countries like China and India are increasingly embracing mobile wallets for digital payments, fueling significant growth in the Asia-Pacific market. Widespread mobile device usage, a robust digital infrastructure, and the rising popularity of applications propel the rapid expansion of digital/mobile wallets in the Asia-Pacific region.

- Banks in the region are collaborating with third-party payment service providers to facilitate secure transactions and support the tourism industry. For instance, in June 2024, owing to a collaboration between Khan Bank, Mongolia's premier full-service bank, and Alipay+, a suite of cross-border mobile payment solutions by Ant International, users of 12 popular overseas e-wallets from eight countries and regions can now seamlessly make digital mobile payments in Mongolia.

Third Party Payment Industry Overview

The third-party payment market is highly competitive and fragmented. Some players have been in the business for quite some time. Subsequently, many startups are coming up to seize this market's huge opportunity. Some players have a presence only in a particular geography. The major players include PayPal Holdings Inc., Stripe Inc., Alipay.com Co. Ltd, Amazon Payments Inc. (Amazon.com Inc.), and Authorize.Net (Visa Inc.)

The third-party payment market comprises players who focus on gaining a point of difference in the contested market space. New startups are gaining traction in the market.

This market is characterized by moderate product differentiation, growing product penetration levels, and high levels of competition with a high level of innovation, which aims to gain an edge in the market.

The firm concentration ratio is expected to grow more during the forecast period. Several software firms consider this market a lucrative opportunity to consolidate their offerings and enter partnerships or acquisitions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Penetration of Internet Leading to Proliferation of Digital Payments

- 5.1.2 Cloud Based Systems Leading to Growth of B2B Sales and also Higher Sales in the POS Segment

- 5.1.3 Growth of E-Commerce Across the High Growth Regions of the World

- 5.2 Market Restraints

- 5.2.1 Security and Privacy Concerns to Restrain the Market

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Online

- 6.1.2 Mobile

- 6.1.3 Point of Sale

- 6.2 By End User

- 6.2.1 BFSI

- 6.2.2 Retail

- 6.2.3 E-Commerce

- 6.2.4 Other End Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 PayPal Holdings Inc.

- 7.1.2 Stripe Inc.

- 7.1.3 Alipay.com Co. Ltd

- 7.1.4 Amazon Payments Inc. (Amazon.com Inc.)

- 7.1.5 Authorize.Net (Visa Inc.)

- 7.1.6 WePay Inc. (JPMorgan Chase & Co.)

- 7.1.7 2Checkout.com Inc. (VeriFone Inc.)

- 7.1.8 Adyen NV

- 7.1.9 First Data Corporation (Fiserv Inc.)

- 7.1.10 One97 Communications Limited (Paytm)