パイプ内ハイドロシステム:市場シェア分析、産業動向・統計、成長予測(2024~2029年)

In-Pipe Hydro Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1519851

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

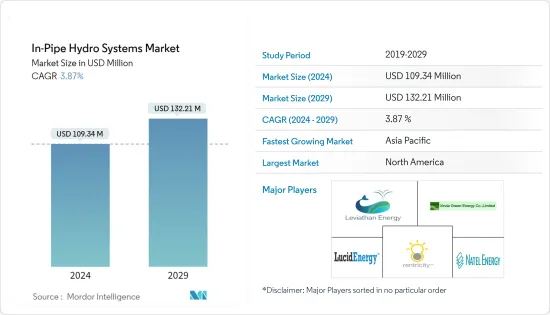

パイプ内ハイドロシステムの市場規模は、2024年に1億934万米ドルと推定され、2029年には1億3,221万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは3.87%で成長します。

主なハイライト

- 中期的には、再生可能エネルギー発電への注目の高まりや、商業・産業用途の双方における効率的な発電へのニーズの高まりといった要因が、パイプ内ハイドロシステムの需要を牽引すると予想されます。

- 一方、初期コストの高さ、自然流下による中断、水供給不足といった要因が、この市場の成長を抑制すると予想されます。

- とはいえ、世界中で水インフラ施設の拡大が進んでおり、自家発電システム導入の大きな機会が生まれています。

- 北米が最大の市場になると予想され、需要の大半は米国やカナダなどの国々からもたらされます。

パイプ内ハイドロシステム市場動向

大きな需要が見込まれる工業用水処理システム

- 産業部門は、パイプ内ハイドロシステム市場に大きなビジネスチャンスを提供しています。鉄鋼や化学などの産業界では、水の需要が広く存在しています。そのため、こうした産業の水道管網を利用して、自家消費に利用できる管内発電システムを設置することができます。

- 世界的に産業全体のエネルギー効率対策が注目される中、工業プラントの水道管網からの発電は、エネルギー消費の効率化につながります。

- 太陽光発電システムや風力発電システムに加え、工業用水パイプラインの余剰水圧からクリーンなエネルギーを利用できる可能性があるため、管内水力発電システムも産業規模での再生可能エネルギー源の統合に利用されています。

- マイクロ水力発電システムは、幅広い揚程と流量条件で運転できるため、自治体、エネルギー集約型産業、農業灌漑地区に導入することができます。これにより、風力発電や太陽光発電のような典型的な断続性がなく、クリーンで継続的なエネルギーを安定して供給することができます。また、パイプラインの管理とメンテナンスにも役立ちます。

- インドや中国などの新興市場における水需要の増加が、世界中のパイプライン内水力システムの需要を牽引しています。ユネスコによると、産業・エネルギー部門が2010年に必要とした水量は約83万7000立方メートル。この数字は、2050年までに倍増し、これらの部門による水の消費量は年間約138万1000立方メートルに達すると予想されています。

- したがって、上記の要因に基づき、工業用水システムは予測期間中に大きな需要を目の当たりにすると予想されます。

市場を独占する北米

- パイプ内ハイドロシステムの低コストと都市化および建設により、パイプ内ハイドロシステム市場は予測期間中に成長すると予想されます。

- 予測期間中、北米が最大の市場シェアを占めると予想されます。これは、タービン設置の増加、技術の進歩、同地域の有力企業の存在によるものです。

- 再生可能エネルギー市場におけるパイプ内ハイドロシステム分野は、2018年以降人気を博しており、これらのシステムは利用可能な場所であればどこでも大規模に使用されています。

- 環境とグリーンエネルギー発電技術に対する意識の高まりが、米国におけるパイプ内水力システム市場の主な促進要因となっています。

- ニューイングランドの水道事業の管内で発生したエネルギーを減圧弁で回収することは、必要な業務には影響しないです。しかし、このプロセスは、金銭と再生可能エネルギーの方程式を変えます。それゆえ、キーン(ニューハンプシャー州)の施設は、北米初のエネルギーニュートラルな浄水場となった。

- 米国が老朽化した水インフラをアップグレードしていく中で、管内水力発電は、水インフラをよりスマートで持続可能、かつ強靭なものにするための新たなソリューションを提供しています。

- MWの設置容量による小規模水力発電は、カナダで50未満、米国で5~100と予想されます。

- カナダで今後予定されている産業および水処理建設プロジェクトが、パイプ内ハイドロシステム市場を牽引すると予想されます。例えば、2023年10月、カナダとブリティッシュ・コロンビア州政府は、1,806万米ドル以上を投資して、地域社会に安全で健康的な飲料水へのアクセスを提供する水処理プラントWilliams Lakeの建設を発表しました。このプロジェクトでは、約850メートルの新しい水道管が敷設され、地域社会に新鮮で清潔な飲料水の供給が増加する見込みです。

- そのため、特に北米地域における意識の高まりや設置の増加といった要因が、予測期間中にパイプ内ハイドロシステム市場にプラスの影響を与えると予想されます。

管内ハイドロシステム産業概要

配パイプ内ハイドロシステム市場は統合されています。同市場の主要企業(順不同)には、Leviathan Energy、Xinda Green Energy Co.Limited、Lucid Energy Inc.、Rentricity Inc.、Natel Energyなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と展開

- 政府の規制と政策

- 市場力学

- 促進要因

- 再生可能エネルギー発電への注目の高まり

- 効率的な発電へのニーズの高まり

- 抑制要因

- 自然な水の流れの中断

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 用途

- 地方自治体の上下水道システム

- 工業用水システム

- その他(灌漑システム、都市・建築用途など)

- 容量

- ピコ水力(5kWまで)

- マイクロ水力(100kWまで)

- ミニ水力(100kW以上)

- 地域

- 北米

- 米国

- カナダ

- その他北米地域

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- カタール

- エジプト

- その他中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Leviathan Energy

- Lucid Energy Inc.

- Rentricity Inc.

- Xinda Green Energy Co. Limited

- Natel Energy

- Tecnoturbines SL

- HS Dynamic Energy Co. Ltd

- GS-Hydro

- InPipe Energy

- Market Ranking/Share Analysis

第7章 市場機会と今後の動向

- 拡大する水インフラ施設

目次

Product Code: 48958

The In-Pipe Hydro Systems Market size is estimated at USD 109.34 million in 2024, and is expected to reach USD 132.21 million by 2029, growing at a CAGR of 3.87% during the forecast period (2024-2029).

Key Highlights

- In the medium term, factors such as increased focus on renewable power generation and rising need for efficient power generation in both commercial and industrial applications are expected to drive the demand for in-pipe hydro systems.

- On the other hand, factors such as high initial cost, interruptions caused by the natural flow of water, and shortage of water supply are expected to restrain the growth of the market studied.

- Nevertheless, expanding water infrastructure facilities across the world is creating huge opportunities for in-house power system deployment, which is expected to create opportunities in the market studied in the near future.

- North America is expected to be the largest market, with most of the demand coming from countries such as the United States and Canada.

In-Pipe Hydro Systems Market Trends

Industrial Water Systems to Witness Significant Demand

- The industrial sector offers vast business opportunities for the in-pipe hydro systems market. The requirement for water across industries, such as steel and chemicals, is widespread. Therefore, water pipeline networks in such industries can be used to install an in-pipe power generation system that can be used for self-consumption.

- As the focus across the world has increased on implementing energy efficiency measures across industries, the power generation from the water pipeline network in the industrial plants can lead to efficiency in energy consumption.

- In addition to solar photovoltaic and wind systems, in-pipe water-to-wire power systems are also being used for the integration of renewable sources at an industrial scale due to the potential to harness clean energy from excess head pressure in industrial water pipelines.

- Micro hydro power systems can be deployed in municipalities, energy-intensive industries, and agricultural irrigation districts since they can operate across a wide range of head and flow conditions. This provides a consistent amount of clean and continuous energy without the typical intermittency of wind and solar. This also aids in pipelines management and maintenance.

- The increased water needs in emerging markets, such as India and China, drive the demand for in-pipe hydro systems worldwide. According to UNESCO, the industrial and energy sectors demanded approximately 837,000 cubic meters of water in 2010. This figure is expected to double by 2050, by which the water consumption from these sectors is expected to reach some 1,381,000 cubic meters annually.

- Therefore, based on the above-mentioned factors, industrial water systems are anticipated to witness significant demand over the forecast period.

North America to Dominate the Market

- Owing to the low cost of in-pipe hydro systems, coupled with urbanization and construction, the in-pipe hydro systems market is expected to grow during the forecast period.

- North America is expected to have the maximum market share during the forecast period. This is due to increasing turbine installations, technological progress, and the presence of prominent players in the region.

- The in-pipe hydro systems segment in the renewable energy market has been gaining popularity since 2018, and these systems are being used on a large scale wherever available.

- The rising awareness about the environment and green energy generation techniques is the key driver for the in-pipe hydro systems market in the United States.

- Harvesting energy generated in a New England water utility's pipe via pressure-reducing valves does not affect required operations. However, the process changes the monetary and renewable energy equation. Hence, the Keene (New Hampshire) facility became the first energy-neutral water treatment plant in North America.

- As the United States upgrades its aging water infrastructure, in-pipe hydropower offers new solutions to help make water infrastructure smarter, more sustainable, and more resilient.

- The small-scale hydropower by installed capacity in MW is expected to be less than 50 for Canada and 5-100 for the United States.

- Upcoming industrial and water treatment construction projects in Canada are anticipated to drive the in-pipe hydro system market. For instance, in October 2023, the governments of Canada and British Columbia announced the construction of a water treatment plant, Williams Lake, that will provide the community access to safe and healthier drinking water, with an investment of more than USD 18.06 million. The project is expected to install approximately 850 meters of new water main, providing the community with an increased supply of fresh, clean drinking water.

- Therefore, factors such as rising awareness and increasing installations, especially in the North American region, are expected to positively impact the in-pipe hydro systems market over the forecast period.

In-Pipe Hydro Systems Industry Overview

The in-pipe hydro systems market is consolidated. Some of the major players (in particular order) in the market include Leviathan Energy, Xinda Green Energy Co. Limited, Lucid Energy Inc., Rentricity Inc., and Natel Energy, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increased Focus on Renewable Power Generation

- 4.5.1.2 Rising Need for Efficient Power Generation

- 4.5.2 Restraints

- 4.5.3 Interruptions Caused in the Natural Flow of Water

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Municipal Water or Wastewater Systems

- 5.1.2 Industrial Water Systems

- 5.1.3 Other Applications (Irrigation Systems, Urban and Building Applications, etc.)

- 5.2 Capacity

- 5.2.1 Pico-hydro (Up To 5kW)

- 5.2.2 Micro-hydro (Up To 100kW)

- 5.2.3 Mini-hydro (100kW and Above)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States of America

- 5.3.1.2 Canada

- 5.3.1.3 Rest of the North America

- 5.3.2 Asia-Pacific

- 5.3.2.1 China

- 5.3.2.2 Japan

- 5.3.2.3 South Korea

- 5.3.2.4 India

- 5.3.2.5 Malaysia

- 5.3.2.6 Thailand

- 5.3.2.7 Indonesia

- 5.3.2.8 Vietnam

- 5.3.2.9 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 Germany

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of the Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of the South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 Rest of the Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Leviathan Energy

- 6.3.2 Lucid Energy Inc.

- 6.3.3 Rentricity Inc.

- 6.3.4 Xinda Green Energy Co. Limited

- 6.3.5 Natel Energy

- 6.3.6 Tecnoturbines SL

- 6.3.7 HS Dynamic Energy Co. Ltd

- 6.3.8 GS-Hydro

- 6.3.9 InPipe Energy

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expanding Water Infrastructure Facilities

パイプ内ハイドロシステム:市場シェア分析、産業動向・統計、成長予測(2024~2029年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日