|

市場調査レポート

商品コード

1642960

医療用包装フィルム:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Medical Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 医療用包装フィルム:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

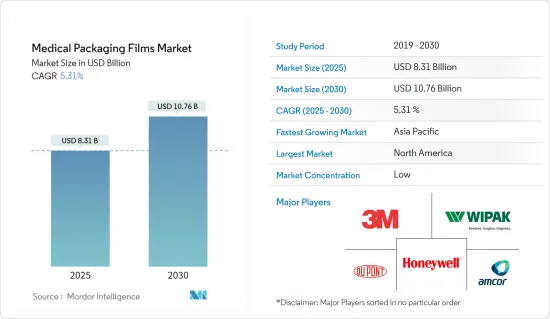

医療用包装フィルムの市場規模は2025年に83億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.31%で、2030年には107億6,000万米ドルに達すると予測されます。

この市場規模は、医療包装業界の用途にわたる包装用フィルム製品の価値を反映したもので、実質的な用語で計算されています。包装用フィルムは、ポリエチレン、ポリプロピレン、二軸延伸ポリエチレンテレフタレート、ポリフェニレンエーテル、ポリ塩化ビニル、EVOH、ポリスチレン(PS)、ナイロンなどのプラスチック材料から作られており、市場調査範囲として様々な金属が考慮されています。

主なハイライト

- 世界各国政府は、被害対策とCOVID-19パンデミック再発防止のため、医療・医薬品製品やソリューションに多額の投資を行っています。例えば、2021年9月に発表されたInstitute for Health Metrics and Evaluation(IHME)によると、世界の一人当たり医療費は2019年に1,129米ドルであり、2050年には1,515米ドルに増加すると予測されています。医療業界では革新的な包装と先手を打った対策が常識となり、医療用包装フィルムの需要を牽引すると予想されます。

- この市場は包装分野の急成長分野であり、サプライチェーンの安全保障問題、規制要求の変化、需給の不均衡といった課題がある中で、多くの促進要因が成長を加速させています。予測期間中、バイオプラスチックフィルムは、プラスチック材料の使用を抑制するために様々な市場主体によって取られたいくつかのイニシアチブを理由に、シェアを拡大すると予想されます。しかし、調査された市場の性質が厳しいため、これらのイニシアチブは、プラスチックフィルムの他のエンドユーザー産業と比較して、プラスチックフィルムを持続可能なパッケージングフィルムに置き換えることへの影響は少ないと思われ、それによって市場の成長が維持されます。

- 市場は、がんなどの慢性疾患の治療薬の増加や、治療薬用のパウチ、袋、小袋の需要の増加により、大きな成長が見込まれています。さらに、人口の高齢化と糖尿病の発生率が市場拡大の新たな機会をもたらすと予測されています。

- 市場成長の主な課題としては、原材料価格の変動、プラスチックベースの包装製品を生分解性材料に置き換えることを含む持続可能性への継続的な取り組み、プラスチック包装における消費者使用後再生(PCR)プラスチックの使用義務化などが挙げられます。通常、この業界では原材料費が売上高の55~60%を占める。そのため、収益性は原材料価格の変動に影響を受けやすいです。軟包装用フィルムの主要な投入コストは原油誘導体であり、これは本質的に変動しやすいです。

- COVID-19の大流行の際、包装用フィルムメーカーは問題山積みになり、1~2年近く長引いた。ロックダウンの影響には、サプライチェーンの混乱、労働力不足、製造工程で使用される原材料の入手不足、最終製品の生産が膨らみ予算を超える原因となった価格変動、輸送問題などがあった。

医療用包装フィルムの市場動向

バイオプラスチック素材とリサイクル可能な包装材への需要の増加が医療用包装フィルム市場を牽引

- バイオプラスチックは、環境負荷を減らすために調査された市場で使用されています。産業におけるプラスチックの多用により、廃棄物の量は劇的に増加しています。したがって、医療用途に生分解性プラスチックを使用することは環境保護に貢献します。

- 医療用バッグは、医療用製品の保護、輸送の容易さ、ブランド促進などの主な利点があるため、特に大量で低コストの包装が必要な場合に、医療用途で広く使用されています。これらの袋は、救急箱、医薬品、医療機器の保管によく使用されます。パウチは、道具や液体薬の保管にも使用できます。

- さらに、包装フィルムメーカーは、製品提供においてより高い持続可能性を達成するために、リサイクル可能な材料を使用した医療用包装ソリューションの革新に注力しています。例えば、2021年11月、持続可能なパッケージング・ソリューション・プロバイダーであるCoveris社は、Flexopeel TとFormpeel Tというブランドの医療用パッケージング用のモノフィルムをベースにしたリサイクル可能なモノPEフィルムを発売しました。同社は、デュポン社のコーティングされていないタイベック1073Bと、PE樹脂をベースにしたコベリス社のモノ構造フィルムを組み合わせた。

- 包装分野でのバイオプラスチック材料への需要の高まりが、市場調査を後押ししています。包装製品メーカーが、バイオプラスチックという形でポリマー系プラスチックの代替品を持っているからです。バイオプラスチックの使用は、医療用パッケージングにおける禁止措置の影響を軽減し、持続可能性への懸念から、ポリマー樹脂ベースのパッケージング使用量の減少が予想されます。European Bioplasticsによると、2021年のフレキシブルパッケージング用バイオプラスチックの世界生産能力は66万5,000トンです。

- 調査対象市場の主要企業は、消費者の嗜好の変化に対応し、市場の需要に対応し続けるために新製品を発売しています。例えば、カナダの包装・投薬ディスペンサー企業であるジョーンズ・ヘルスケア・グループは、2021年12月に持続可能な包装製品で薬局向けのQubeとFlexRx投薬アドヒアランス製品ラインを拡大しました。同社は、医療認可を取得したバイオプラスチックBio-PET製のQube Pro、FlexRx One、FlexRx Resealブリスターパックを発売しました。

アジア太平洋地域が急成長市場になる見込み

- アジア太平洋地域は、中国、インド、インドネシア、マレーシアなどの新興経済諸国における中間層人口の増加、可処分所得の増加、医療・医薬品需要の増加などにより、調査した市場の中で最も高い成長率で拡大すると予想されます。同地域における医薬品生産の活況が、同地域のバリアフィルム市場の成長を大きく牽引しています。

- アジアにおける腎臓病の有病率の増加は、治療を改善するための高度な装置を含む新しい治療法の開発を必要としました。アジアにおける腎臓病の有病率は、糖尿病や高血圧の増加により増加しています。さらに、医療機器や製品の保存期間を延ばし、細菌やウイルスによる汚染の可能性を排除することが重視され、医療・ヘルスケア産業における包装フィルムの需要が増加しています。

- 医療用包装フィルムソリューションは、コスト削減、持続可能性、包装製品の安全性などの利点を提供するため、中国やインドなどの人口の多い新興諸国の医療用包装フィルムに大きな成長が見られます。さらに、アジア太平洋地域は、強固な産業基盤、持続可能な包装ソリューションに対する需要の増加、主要メーカーの存在により、金額および数量で市場をリードすると予想されています。

- 医療用包装フィルムの需要は、移植可能なデバイスの需要増加やヘルスケア市場の活況によっても促進されています。移植可能な機器に対する需要の高まりと、中国やインドのような新興国市場における一般市民の意識の高まりにより、市場は拡大しました。

- ヘルスケア分野の拡大とともに、中国の医療機器市場は驚異的なペースで増加しています。この特定分野は、中国で最も急速に成長している分野のひとつです。このセクターは、ダイナミックな規制によって2桁の成長率で増加しており、その70%近くが病院からの調達によるものです。伝統的に中国の医療機器市場は、大量のローエンド消耗品、機械治療機器、補助器具でよく知られています。必要なハイエンド消耗品の調達は、伝統的に国内で製造されていなかったため、輸入に大きく依存してきました。

- 現在、高価値でリスクの高い医療機器は国産にシフトしており、これが中国の医療用包装フィルム市場を牽引すると期待されています。さらに、高齢化も中国製ハイエンド医療機器の需要増加の原動力の一つとなっています。世界保健機関(WHO)によると、中国では2040年までに60歳以上の高齢者人口が28%に達すると予想されています。この増加する人口層はますます裕福になり、以前よりもヘルスケアサービスにお金をかけられるようになると予想されます。

医療用包装フィルム産業の概要

医療用包装フィルム市場は細分化されており、以下のような大手企業が参入しています。 Honeywell, 3M, Amcor, etc. have used various strategies such as new product launches, joint ventures, partnerships, acquisitions, and others to increase their footprints in this market.

- 2022年4月- 責任あるパッケージング・ソリューションの開発と生産で世界をリードするAmcor社は、医薬品パッケージング・ポートフォリオに持続可能な高シールドラミネートを追加すると発表しました。新しい低炭素でリサイクル可能なパッケージングオプションは、製薬会社のリサイクル可能な目標をサポートしながら、業界で必要とされる高いバリア性と性能要件を提供し、2つの面で実現します。

- 2022年1月-再生材料製品と高バリア性保護包装の主要企業であるクロックナー・ペンタプラスト社は、消費者向け健康・医薬品食品包装市場における持続可能なイノベーションの提供をさらに拡大するため、北米地域における消費者再生材料(PCR)PETの生産能力を大規模な投資により拡大する計画を発表しました。同社は、生産量の20%以上をPCR素材から製造する能力を有しています。今回の拡張により、押出ライン1基と熱成形機2基が追加され、合計1万5,000トンのrPETまたはPETの生産能力が新たに加わることになります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界バリューチェーン分析

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- バイオプラスチックとリサイクル可能な包装材料に対する需要の増加

- 主に慢性疾患の増加によるヘルスケア施設への支出の増加

- 市場抑制要因

- 原材料価格の変動

第6章 市場セグメンテーション

- 材料タイプ別

- プラスチックフィルム

- PE

- PP

- PVC

- PC

- メタリックフィルム

- プラスチックフィルム

- 用途別

- バッグ&パウチ

- チューブ

- その他の用途

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Honeywell International Inc.

- 3M Company

- Wipak Oy

- Amcor Plc

- DuPont de Nemours, Inc.

- Renolit Medical

- PolyCine GmbH

- Glenroy, Inc.

- Toray Industries, Inc.

- Klockner Pentaplast Group

- Dunmore Corporation

- Covestro AG

第8章 投資分析

第9章 市場機会と今後の動向

The Medical Packaging Films Market size is estimated at USD 8.31 billion in 2025, and is expected to reach USD 10.76 billion by 2030, at a CAGR of 5.31% during the forecast period (2025-2030).

The market size reflects the value of packaging film products across medical packaging industry applications and is computed in the real term. Packaging films are made from plastic materials, such as polyethylene, polypropylene, biaxially oriented polyethylene terephthalate, polyphenylene ether, polyvinyl chloride, EVOH, polystyrene (PS), nylon, and various metals are considered as per the scope of the market study.

Key Highlights

- Governments worldwide are heavily investing in medical and pharmaceutical products and solutions in damage control and the prevention of any potential resurgence of the COVID-19 pandemic. For instance, according to the Institute for Health Metrics and Evaluation (IHME), published in September 2021, the global per capita health expenditure was USD 1,129 in 2019, and it is projected to increase to USD 1,515 by 2050. Innovative packaging and preemptive measures are expected to become the norm in the medical industry, driving the demand for medical packaging films.

- The market studied is a burgeoning segment of the packaging sector, with many drivers accelerating the growth amid the challenges in the form of supply chain security woes, changing regulatory demands, and supply and demand imbalances. During the forecast period, bioplastic films are expected to increase their share on account of several initiatives taken by various market entities to curb the use of plastic materials. However, owing to the severe nature of the market studied, these initiatives are likely to have less impact on replacing plastic films with sustainable packaging films compared to other end-user industries of plastic films, thereby sustaining the market growth.

- The market is expected to experience significant growth, owing to the increase in therapeutics for chronic illnesses, such as cancer and the increasing demand for pouches, bags, and sachets for therapeutic medicines. Additionally, the aging population and the incidence of diabetes are projected to present new opportunities for market expansion.

- Some of the major challenges for the market growth are the volatility of raw material prices, the ongoing drive for sustainability, which includes replacing plastic-based packaging products with biodegradable materials, and mandates of using post-consumer recycled (PCR) plastics in plastic packaging. Usually, raw material costs are attributed to 55-60% of sales in this industry. Therefore, profitability is vulnerable to volatility in raw material prices. The key input cost for flexible packaging film is crude derivatives, which have been inherently volatile.

- During the COVID-19 pandemic, packaging film manufacturers were flooded with a pool of issues that lasted long for nearly one or two years. Some of the effects of lockdown included supply chain disruptions, labor shortages, lack of availability of raw materials used in the manufacturing process, fluctuating prices that caused the production of the final product to inflate and go beyond budget, transportation problems, etc.

Medical Packaging Films Market Trends

Increasing Demand for Bioplastic Material and Recyclable Packaging Material Drives the Medical Packaging Films Market

- Bioplastics are being used in the market studied to reduce environmental impact. The amount of waste increased dramatically due to the extensive use of plastics in the industry. Thus, using biodegradable plastic in medical applications contributes to environmental protection.

- Medical bags are widely used in medical applications, particularly when low-cost packaging in large quantities is required, owing to the primary benefits, such as medical product protection, ease of transportation, and brand promotion. These bags are frequently used to store first aid kits, medications, and medical equipment. Pouches can be used to store tools or liquid medications.

- Moreover, packaging film manufacturers are focusing on innovating medical packaging solutions with recyclable materials to achieve greater sustainability in their product offerings. For instance, in November 2021, Coveris, a sustainable packaging solution provider, launched recyclable mono-PE film based on mono films branded Flexopeel T and Formpeel T for medical packaging. The company combined an uncoated Tyvek 1073B from DuPont and a mono-structure film from Coveris, based on PE resins.

- The increasing demand for bioplastic material in the packaging segment has been driving the market study, as packaging product producers have alternatives for polymer-based plastic in the form of bioplastic. Using bioplastic reduced the impacts of bans and an anticipated reduction in polymer plastic-based packaging usage in medical packaging, owing to sustainability concerns. According to European Bioplastics, in 2021, the global production capacity of bioplastics for flexible packaging was 665,000 metric tons.

- Key players in the market studied are launching new products to cater to changing consumer preferences and stay relevant to market demand. For instance, the Canadian packaging and medication dispenser company Jones Healthcare Group expanded the Qube and FlexRx medication adherence product lines for pharmacies with sustainable packaging products in December 2021. The company launched Qube Pro, FlexRx One, and FlexRx Reseal blister packs made of Bio-PET, a bioplastic that received medical approval.

Asia Pacific is Expected to be the Fastest Growing Market

- The Asia Pacific is expected to expand with the highest growth rate in the market studied, majorly due to the increasing middle-class population, disposable incomes, and demand for medical and pharmaceutical products in developing economies such as China, India, Indonesia, and Malaysia. The booming pharmaceutical production in the region is significantly driving the growth of the barrier film market in the region.

- The increasing prevalence of kidney disease in Asia necessitated the development of new therapies, including sophisticated devices to improve treatment. The prevalence of kidney disease in Asia is increasing due to increasing rates of diabetes and hypertension. Furthermore, the emphasis on extending the shelf life of medical devices and products and eliminating the possibility of bacterial or viral contamination increased the demand for packaging film in the medical and healthcare industries.

- As medical packaging film solutions offer benefits, like cost savings, sustainability, and safety of packaged products, significant growth has been seen for medical packaging films from populated developing countries, such as China and India. Moreover, the Asia-Pacific region is anticipated to lead the market studied in terms of value and volume due to the solid industrial base, increased demand for sustainable packaging solutions, and the presence of key manufacturers in the region.

- The demand for medical packaging films is also fueled by the increasing demand for implantable devices and the booming healthcare market. The market expanded due to the escalating demand for implantable devices and increasing public awareness in developing nations like China and India.

- Along with the expanding healthcare sector, China's medical device market is increasing at an incredible pace. This specific sector is one of the fastest-increasing sectors in China. The sector is increasing at a double-digit growth rate, driven by dynamic regulations, nearly 70% of which was contributed to by hospital procurement. Traditionally China's medical devices market is well known for large volumes of low-end consumables, mechanotherapy devices, and aids. There has been large dependence on imports for procuring required high-end consumables as they were not traditionally manufactured in the country.

- Currently, there has been a shift toward domestically made high-value and high-risk medical devices, which are expected to drive the Chinese medical packaging film market. Moreover, the aging population is one of the driving factors for the increase in demand for high-end Chinese devices. According to the World Health Organization (WHO), the population aged more than 60 years is expected to reach 28% in China by 2040. This increasing demographic, which is increasingly affluent, is expected to be able to spend more on healthcare services than before.

Medical Packaging Films Industry Overview

The Medical Packaging Films Market is fragmented in nature, and the major players such as Honeywell, 3M, Amcor, etc. have used various strategies such as new product launches, joint ventures, partnerships, acquisitions, and others to increase their footprints in this market.

- April 2022 - Amcor, one of the global leaders in developing and producing responsible packaging solutions, announced the addition of sustainable high shield laminates to its pharmaceutical packaging portfolio. The new low carbon, recycle-ready packaging options deliver on two fronts, providing the high barrier and performance requirements needed for the industry while supporting pharmaceutical companies' recyclable objectives.

- January 2022 - Klockner Pentaplast, a leading company in recycled content products and high-barrier protective packaging, announced its plans to expand its post-consumer recycled content (PCR) PET capacity in the North America region with a significant investment to further increase its sustainable innovation offering in consumer health and pharmaceutical food packaging markets. The company has the capacity, with more than 20% of its volumes made from PCR material. The expansion is set to add an extrusion line and two thermoformers, providing a total of 15,000 metric tons of new rPET or PET capacity.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat Of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Bioplastic and Recyclable Packaging Material

- 5.1.2 Increased Spending on Healthcare Facilities, Primarily Owing to Increase in Chronic Diseases

- 5.2 Market Restraints

- 5.2.1 Fluctuation in the Prices of Raw Materials

6 MARKET SEGMENTATION

- 6.1 Material Type

- 6.1.1 Plastic Film

- 6.1.1.1 PE

- 6.1.1.2 PP

- 6.1.1.3 PVC

- 6.1.1.4 PC

- 6.1.2 Metallic Film

- 6.1.1 Plastic Film

- 6.2 Application

- 6.2.1 Bags & Pouches

- 6.2.2 Tubes

- 6.2.3 Other Applications

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Honeywell International Inc.

- 7.1.2 3M Company

- 7.1.3 Wipak Oy

- 7.1.4 Amcor Plc

- 7.1.5 DuPont de Nemours, Inc.

- 7.1.6 Renolit Medical

- 7.1.7 PolyCine GmbH

- 7.1.8 Glenroy, Inc.

- 7.1.9 Toray Industries, Inc.

- 7.1.10 Klockner Pentaplast Group

- 7.1.11 Dunmore Corporation

- 7.1.12 Covestro AG