|

市場調査レポート

商品コード

1445969

小児医療機器: 市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Pediatric Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 小児医療機器: 市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

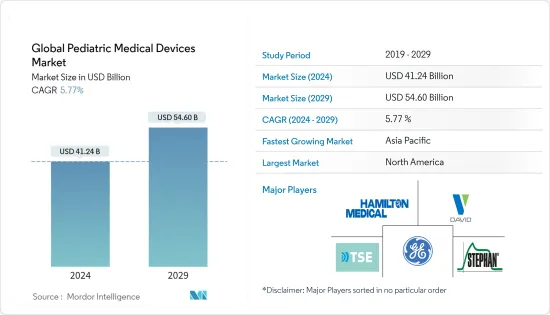

世界の小児医療機器市場規模は、2024年に412億4,000万米ドルと推定され、2029年までに546億米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.77%のCAGRで成長します。

COVID-19感染症のパンデミックによってもたらされた健康への脅威は、前例のないものでした。市場の影響を明らかにするために、数多くの調査が発表されています。たとえば、2020年10月に発表された論文「Pediatric COVID-19:Systematic Review of the Literature」によると、SARS-CoV-2感染検査で陽性となった小児患者の14.9%は無症状でした。患者が経験する症状としては、咳(48%)、発熱(47%)、喉の痛み/咽頭炎(28.6%)が最も多く、鼻炎、くしゃみ、鼻づまりなどの上気道症状(13.7%)、吐き気などと比較しました。嘔吐(7.8パーセント)、下痢(10.1パーセント)。その結果、小児におけるこれらの疾患の罹患率の高さにより救命救急の必要性が高まり、小児医療機器市場に好影響を与えました。

市場拡大の主な原因は、貧血、喘息、水痘、ジフテリア、白血病、麻疹、おたふく風邪、肺炎、結核、百日咳、ライム病などの小児慢性疾患の発生率の増加です。ユニセフの2021年4月の報告書によると、毎年80万人以上の5歳未満の子どもが肺炎で死亡しており、これは他のどの感染症よりも多いです。これには15万3,000人以上の新生児が含まれます。小児で最も一般的な慢性疾患の1つは肺炎であり、これにより医療機器の需要が増加し、市場が拡大しています。さらに、調査中の業界に新しいデバイスがイントロダクションと、市場は大幅に拡大するでしょう。たとえば、GetingeのFlow-eおよびFlow-c麻酔システムは、新生児や幼児から病的肥満者に至るまで、最も要求の厳しい患者に対してもカスタマイズされた麻酔投与を可能にし、2020年 8月に米国食品医薬品局(FDA)によって承認されました。さらに、小児医療機器イノベーションのための看護師主導のテクノロジーとイノベーションを促進するために、西海岸小児科テクノロジー&イノベーション・コンソーシアム(CTIP)とナーシング・イノベーション・ハブ社(NIHUB)が2020年3月に提携しました。小児部門の医療インフラを開発するための政府による研究開発プログラムが市場の成長を促進しています。

ただし、利用可能な小児医療機器に対する認識の欠如は、市場の成長の大きな欠点です。

小児医療機器市場動向

新生児ICUデバイスセグメントは、予測期間中に大幅な成長を示すと予想される

分娩中の課題、早産、または出生後の健康上の問題により、NICUケアが必要な子供たちは、生後24時間以内にNICUに移送されることがよくあります。妊娠 37週より前に生まれた赤ちゃんは早産とみなされます。米国で生まれた赤ちゃんの10人に1人が早産でした。早産率は2019年の10.2パーセントから2020年の10.1パーセントへと1パーセント減少しました。早産で生まれた赤ちゃんは、敗血症や肺炎などの病気にかかりやすいです。前述の報告書によると、2020年のアフリカ系アメリカ人女性の早産率(14.4%)は、白人女性やヒスパニック系女性の早産率(それぞれ9.1%、9.8%)よりも約50%高くなっています。これにより、今後数年間でこの分野の成長が促進される可能性があります。

この分野での新しい商品のイントロダクションよっても、市場の有利な拡大がもたらされるでしょう。たとえば、世界初のポータブル新生児用 CPAP装置の1つであるSAANSは、2019年 8月にInnAccelによって導入されました。これは、呼吸窮迫症候群(RDS)を患う重症新生児に、輸送中および呼吸困難な状況の両方で呼吸サポートを提供するように設計されています。限られたリソース。さらに、メドトロニックは、NICU向けのSonarMed気道モニタリングシステムを導入するために、2020年 12月にSonarMed Inc.を買収しました。呼吸補助を必要とするすべての新生児は、このテクノロジーを通じてより良い治療を受けることができる可能性があります。結果として、市場の主要な競合他社によるこのような戦略的な動きは、新生児ICUセグメントで利用可能な製品の範囲を増やし、市場を推進するでしょう。その結果、前述の理由により、このセグメントの成長が大幅に増加し、市場が推進されると予想されます。

北米が市場を独占しており、予測期間にも同様の成長が予想される

予測期間を通じて、北米が市場全体を支配すると予想されます。市場の成長は、主要企業の存在、地域における小児慢性疾患の高い有病率、確立されたヘルスケアインフラ、新製品の発売などの要因によるものです。米国疾病管理予防センターの10月の報告書によると、米国では学齢期の児童と青少年の40%以上が、喘息、肥満、その他の身体疾患、行動や学習の問題など、少なくとも1つの慢性的な健康状態を抱えています。 2021年のレポートです。慢性疾患を持つ子供たちは、日常的な管理と潜在的な緊急事態への備えの両方を必要とする、複雑かつ継続的なヘルスケアニーズを抱えている場合があります。その結果、より充実したケアを提供するという考えのもとに小児用医療機器が生み出され、市場に大きな影響を与えることになります。

研究対象となっている国の市場でも、そこでの製品デビューから恩恵を受けると思われます。たとえば、Preceptis Medical, Inc.は、オフィスベースの小児耳管手術用の次世代ハミングバード鼓膜切開チューブシステム(TTS)を2021年 6月にリリースすると発表しました。新しいハミングバードデバイスは人間工学に基づいたレイアウトが改良されており、幼児に耳管をより効果的に投与できるようになります。右心室から肺に血液を運ぶ心臓の部分である右心室流出路(RVOT)が天然または外科的に修復された小児患者を治療するハーモニー経カテーテル肺弁(TPV)システムが、米国食品医薬品局から承認を取得しました。この装置は、心臓の右下腔への血液漏出を特徴とする重度の肺弁逆流症の患者を対象としています。先天性心疾患がこの病気を引き起こすことがよくあります。さらに、政府の取り組みの奨励と調査協力数の増加も、市場の拡大を後押しすると予想される要因の一つです。有利なヘルスケア政策、多数の患者人口、発達したヘルスケア市場により、この地域は将来的に成長すると予想されています。

小児医療機器業界の概要

小児医療機器市場は適度な競争があり、いくつかの主要企業で構成されています。現在、いくつかの大手企業が市場シェアの点で市場を独占しています。各社はデバイスに対する需要の高まりに応える取り組みを進めています。現在市場を独占している企業には、TSE MEDICAL、DAVID、Hamilton Medical、GEヘルスケア、Fritz Stephan GmbH、Phoenix Medical Systems、Novonate Inc.、Elektro Mag、Trimpeks、Atom Medical Corpなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 小児における感染症の有病率の増加

- 小児の健康問題に対する医療インフラの開発

- 市場抑制要因

- 小児用機器開発への課題と対応可能性の低い市場

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- IVDデバイス

- 心臓病学用機器

- 麻酔および呼吸管理装置

- 新生児ICU装置

- 監視デバイス

- その他

- エンドユーザー別

- 病院

- 診断研究所

- 小児科クリニック

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- TSE MEDICAL

- Ningbo David Medical Device Co. Ltd

- Hamilton Medical

- GE Healthcare

- Fritz Stephan GmbH

- Phoenix Medical Systems Pvt Ltd

- Novonate Inc.

- Elektro-Mag

- Trimpeks

- Atom Medical Corporation

- Abbott

- Medtronic PLC

第7章 市場機会と将来の動向

The Global Pediatric Medical Devices Market size is estimated at USD 41.24 billion in 2024, and is expected to reach USD 54.60 billion by 2029, growing at a CAGR of 5.77% during the forecast period (2024-2029).

The health threat posed by the COVID-19 pandemic was unparalleled. Numerous research has been released to shed light on the market's consequences. For instance, according to the article "Pediatric COVID-19: Systematic Review of the Literature," which was released in October 2020, 14.9% of pediatric patients who tested positive for SARS-CoV-2 infection were asymptomatic. Cough (48 percent), fever (47 percent), and sore throat/pharyngitis (28.6 percent) were the most prevalent symptoms experienced by patients, compared to upper respiratory symptoms such as rhinitis, sneezing, and nasal congestion (13.7 percent), nausea and vomiting (7.8 percent), and diarrhea (10.1 percent ). As a result, the high prevalence of these disorders in children raised the need for critical care, which had a favorable effect on the pediatric medical devices market.

The main cause of the market's expansion is the rising incidence of chronic illnesses in children, such as anemia, asthma, chickenpox, diphtheria, leukemia, measles, mumps, pneumonia, tuberculosis, whooping cough, and Lyme disease. Over 800,000 children under the age of five die from pneumonia each year, more than any other infectious disease, according to UNICEF 2021's April report. This includes more than 153,000 new babies. One of the most common chronic diseases in children is pneumonia, which is increasing the demand for medical equipment and boosting the market. Additionally, the introduction of new devices in the industry under study will result in substantial market expansion. For instance, Getinge's Flow-e and Flow-c Anesthetic Systems, which allow tailored anesthesia delivery for even the most demanding patients, from neonates and toddlers to the morbidly obese, was approved by the US Food & Drug Administration (FDA) in August 2020. Additionally, to encourage nurse-led technology and innovation for pediatric medical device innovation, the West Coast Consortium for Technology & Innovation in Pediatrics (CTIP) and Nursing Innovation Hub, Inc. (NIHUB) partnered in March 2020. Furthermore, the growing investments in research and development programs by the government to develop the medical infrastructure in the pediatric section are boosting the market growth.

However, the lack of awareness of the pediatric medical devices available is the major drawback of market growth.

Pediatric Medical Devices Market Trends

Neonatal ICU Devices Segment is Expected to Show Significant Growth Over the Forecast Period

Due to challenges during delivery, early birth, or health issues after birth, children who require NICU care are frequently moved there within 24 hours of birth. A baby is considered preterm if it is born before 37 weeks of pregnancy. One out of every ten babies born in the United States in 2020 suffered from preterm birth, according to the Centers for Disease Control and Prevention's November 2021 update. From 10.2 percent in 2019 to 10.1 percent in 2020, the preterm birth rate decreased by one percent. Babies born prematurely are more prone to illnesses like sepsis, pneumonia, etc. According to the previously stated report, preterm birth rates among African-American women (14.4%) in 2020 were approximately 50% higher than those among white or Hispanic women (9.1 percent and 9.8 percent respectively). This is likely to boost the growth of the segment in upcoming years.

A lucrative expansion of the market will also result from the introduction of new items in the area. For instance, SAANS, one of the first portable, neonatal CPAP devices in the world, was introduced by InnAccel in August 2019. It is designed to give severely ill newborns with Respiratory Distress Syndrome (RDS) breathing support both during transportation and in situations with limited resources. In addition, Medtronic purchased SonarMed Inc. in December 2020 in order to introduce SonarMed Airway Monitoring System for NICUs. All newborns who need help breathing are likely to receive better treatment through this technology. As a result, such strategic moves by major market competitors would increase the range of products available in the neonatal ICU segment, propelling the market. As a result, it is anticipated that the aforementioned reasons will significantly increase the segment's growth, propelling the market.

North America Dominates the Market and Expected to do Same in the Forecast Period

North America is expected to dominate the overall market, throughout the forecast period. The market growth is due to the factors such as the presence of key players, high prevalence of pediatric chronic diseases in the region, established healthcare infrastructure, and launch of new products. In the United States, more than 40% of school-aged children and adolescents have at least one chronic health condition, such as asthma, obesity, other physical diseases, and behavior/learning issues, according to the Centers for Disease Control and Prevention's October 2021 report. Children with chronic illnesses can have complex, ongoing healthcare needs that require both routine management and preparation for potential emergencies. As a result, pediatric medical devices are created with the idea of providing enhanced care, which will greatly influence the market.

The country's studied market will benefit from the product debuts there as well. Preceptis Medical, Inc., for instance, announced the release of its next-generation Hummingbird Tympanostomy Tube System (TTS) for office-based pediatric ear tube surgeries in June 2021. The new Hummingbird device has an improved ergonomic layout that makes it possible to administer ear tubes to toddlers more successfully. The Harmony Transcatheter Pulmonary Valve (TPV) System, which treats pediatric patients with a native or surgically repaired right ventricular outflow tract (RVOT), the portion of the heart that carries blood from the right ventricle to the lungs, received approval from the U.S. Food and Drug Administration in March 2021. The device is intended for patients with severe pulmonary valve regurgitation, which is characterised by blood leakage into the right lower chamber of the heart. Congenital heart disease frequently causes this illness. In addition, encouraging government initiatives and a rise in research collaboration numbers are among the factors anticipated to boost market expansion. Due to favourable healthcare policies, a large patient population, and a developed healthcare market, the region is expected to grow in the future.

Pediatric Medical Devices Industry Overview

The pediatric medical devices market is moderately competitive and consists of several major players. A few major players are currently dominating the market in terms of market share. The companies are taking initiatives to meet the higher demand for devices. Some of the companies which are currently dominating the market are TSE MEDICAL, DAVID, Hamilton Medical, GE Healthcare, Fritz Stephan GmbH, Phoenix Medical Systems, Novonate Inc., Elektro Mag, Trimpeks, and Atom Medical Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Infectious Diseases among the Pediatric Population

- 4.2.2 Development of Health Care Infrastructure for Pediatric Health Issues

- 4.3 Market Restraints

- 4.3.1 Challenges to Pediatric Device Development and Low Addressable Market

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Product

- 5.1.1 IVD Devices

- 5.1.2 Cardiology Devices

- 5.1.3 Anesthesia & Respiratory Care Devices

- 5.1.4 Neonatal ICU Devices

- 5.1.5 Monitoring Devices

- 5.1.6 Others

- 5.2 By End-User

- 5.2.1 Hospitals

- 5.2.2 Diagnostic Laboratories

- 5.2.3 Pediatric Clinics

- 5.2.4 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 TSE MEDICAL

- 6.1.2 Ningbo David Medical Device Co. Ltd

- 6.1.3 Hamilton Medical

- 6.1.4 GE Healthcare

- 6.1.5 Fritz Stephan GmbH

- 6.1.6 Phoenix Medical Systems Pvt Ltd

- 6.1.7 Novonate Inc.

- 6.1.8 Elektro-Mag

- 6.1.9 Trimpeks

- 6.1.10 Atom Medical Corporation

- 6.1.11 Abbott

- 6.1.12 Medtronic PLC