ハードディスクドライブ(HDD)-市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Hard Disk Drive (HDD) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1911495

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

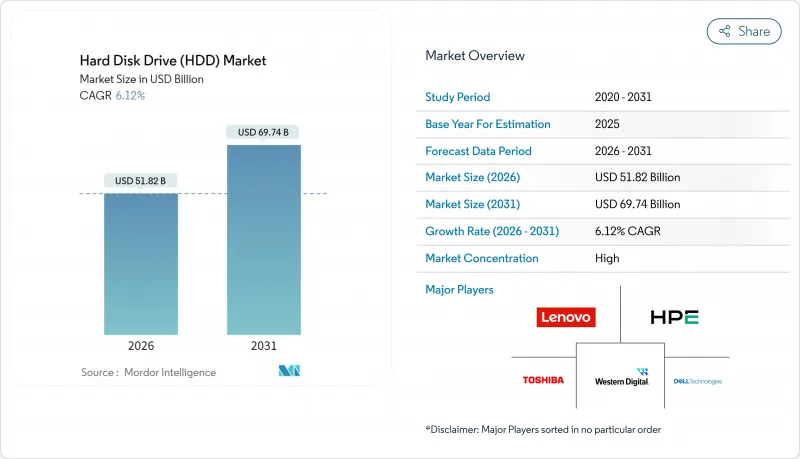

2026年のハードディスクドライブ(HDD)市場規模は518億2,000万米ドルと推定され、2025年の488億3,000万米ドルから成長し、2031年には697億4,000万米ドルに達すると予測されています。

2026~2031年にかけての年間平均成長率(CAGR)は6.12%となる見込みです。

1テラバイトあたりのコスト優位性、100TB超を目指すHAMR技術による容量ロードマップ、AI生成によるコールドデータの急増により、ハードドライブはハイパースケールストレージ戦略の中核であり続けます。クラウドプロバイダが2025年の過去最高となる3,150億米ドルの資本予算の約15~20%をストレージインフラに割り当てる中、ニアラインエンタープライズ導入が拡大しています。一方、電力制約のあるデータセンター市場では、テラバイトあたりのエネルギー消費量指標が需要を支えています。インターフェース動向では、SATAの広範な導入基盤が確認される一方、高帯域幅が不可欠な領域ではSASと新興のNVMeパスウェイが勢いを増しています。供給動態は依然として繊細な状況です。3社のサプライヤーがほぼ全生産量を支配しているため、貿易摩擦から自然災害に至るあらゆる混乱がハードディスクドライブ(HDD)市場に急速に波及するからです[WESTERN DIGITAL.COM]。同時に、アジア太平洋のと北米の地域による製造優遇策が生産拠点の再編を促し、ミッションクリティカルな企業向け受注の最終組立プロセスにおけるニアショアリングを後押ししています。

世界のHDD市場の動向と洞察

ハイパースケールとクラウドストレージ容量への需要増加

ハイパースケールデータセンター数は2024年末時点で1,136ヶ所に達し、AIアクセラレータがコンピューティングの足跡を再構築する中、2030年までに3倍に増加すると予測されています。主要クラウド事業者の2025年設備投資計画の約5分の1をストレージが占め、超大容量ラックに数十億米ドルが投入される見込みです。これにより、コールドティア展開向けのハードディスクドライブ(HDD)市場が優位となります。ウエスタンデジタル社は、主にHAMR技術による密度向上を原動力として、2024~2028年にかけてHDDのエクサバイト出荷量が23%増加すると予測しています。米国はハイパースケール容量の54%を占めていますが、現地の電力制約により、ワット/テラバイト性能に優れたドライブが評価されています。分散型アーキテクチャにより、コンピューティングとストレージが分離され、HDDが膨大なコールドデータプールを処理する一方、SSDがホットデータアクセスを管理する体制が整っています。

ニアラインワークロードにおけるSSDに対するコスト/TB優位性

シーゲート社は2024会計年度に出荷した398エクサバイトにおいて、1テラバイトあたり15米ドルを達成したと報告しており、エンタープライズ向けSSDとのコスト差は約2.5倍を維持しています。30TB容量ポイントでは価格差が約3~4倍に拡大し、コスト重視のコールドデータ層におけるハードディスクドライブ(HDD)市場の優位性を強化しています。フラッシュメーカーは3D NANDの微細化によりテラバイトあたりのコストを引き続き低減していますが、耐久性と書き込みコストの制約により、シーケンシャル処理が中心のワークロードではドライブの総所有コスト(TCO)が依然として有利です。企業バイヤーは、支出とサービスレベル目標を最適化するため、高性能SSD階層と大規模なHDD容量プールを組み合わせたハイブリッド戦略をますます明確に打ち出しています。

SSDの1TBあたりのコストの急速な低下とエンタープライズ向けフラッシュのTCO優位性

フラッシュベンダーは現在232層3D NANDを生産し、四半期ごとにビット単価を引き下げています。ピュア・ストレージのハイパースケーラー向け設計採用事例は、電力・冷却・設置面積の節約効果を総合的に考慮した場合、フラッシュが圧倒的な総コスト優位性を実現するシナリオを示しています。61.44TBエンタープライズSSDの登場は、高価格ながら容量収束の兆しを示しています。QLC NANDはさらなるビット単価の低減を約束しますが、耐久性の制約から、こうした製品は読み取り中心のワークロードに限定されます。企業バイヤーが総合的な調達視点を取り入れる中、HDDはフラッシュがコスト差を縮める速度を上回るペースで容量を向上させ続ける必要があります。

セグメント分析

3.5インチ製品は2025年に売上高の65.62%を占め、2031年までCAGR9.29%でハードディスクドライブ(HDD)市場全体を上回る成長が見込まれます。大容量プラッタにより優れたラック当たりギガバイト効率を実現し、床面積を平方フィート当たり数千ドルで評価するハイパースケール事業者にとって極めて重要です。3.5インチ製品のハードディスクドライブ(HDD)市場規模は、2031年までに452億米ドルを超えると予測されています。HAMR(磁気ヒート回転記録)とUltraSMR(超密記録技術)の進歩により、ベンダーは同じ筐体で40TBを実現するロードマップを策定可能となり、このセグメントの規模の経済性を強化しています。

小型の2.5インチドライブはノートブックやコンパクトサーバー向けですが、SSDへの代替が進んでおり、成長展望は限定的です。1.8インチ以下のフォームファクタは、ニッチな家電や産業機器に採用されています。3.5インチプラットフォームを基盤とする高密度JBODシャーシは、少ないスピンドル数でエクサバイト規模の目標を達成できるため、コールドティアアーキテクチャにおいてコスト優位性を維持しています。シーゲイトが最近日本で発表した20TBと24TBのBarraCuda SKUは、消費者向け価格設定であり、大容量3.5インチロードマップへの継続的な投資を強調するものです。

ニアラインエンタープライズ環境は2025年出荷量の44.10%を占め、主要ワークロードの中で最速となるCAGR9.52%で成長します。クラウドアーキテクトは拡大するAIトレーニングセットを低コスト高密度層に集約し、ペタバイト規模クラスターの中核としてHDD市場を維持します。ニアライン用途におけるHDDの市場シェアは、マッキンゼーが予測するコールドデータの急増から恩恵を受け、これはドライブの順次書き込み性能と経済的な保存特性と合致します。

コンシューマー向けデスクトップとゲーミングPCは着実にSSDへ移行しており、1TB以下のエントリードライブに対するユニット需要は減少傾向にあります。モニタリング用アレイやNASデバイスは、書き込みパターンや容量ニーズが磁気メディアに適しているため、堅調さを維持しています。エンタープライズデータセンターチームはSSDとHDDが共存する分散型モデルを採用し続けていますが、ニアライン層は今後10年間で絶対的なエクサバイト成長量が最も大きい層となります。

地域別分析

アジア太平洋は2025年に世界収益の36.10%を占め、2031年までCAGR6.84%で拡大しています。中国と日本はハイパースケール拡大と国内OEM出荷により地域需要を支え、タイは2024年8月に承認されたウエスタンデジタル社による6億9,300万米ドルの拡大計画により製造拠点としての地位を維持しています。インドの小売向けドライブ出荷台数は、電子商取引と在宅勤務の動向が持続したため、2024年第2四半期に前期比12%増加しました。マレーシアの170億米ドル規模のデータセンターモニタリングプログラムを含む東南アジア全域のスマートシティ予算が、地域のエクサバイト需要を加速させています。

北米は第2の主要地域であり、設置済みクラウド容量の54%を占める米国のハイパースケール事業者によって牽引されています。貿易施策の逆風によりコスト不確実性が生じていますが、提案されている優遇措置はサプライチェーン短縮につながる国内組立を促進する可能性があります。バージニア州のデータセンター回廊周辺で増大する電力網の制約により、設計者はワット/テラバイト効率を重視するようになり、オールフラッシュアレイよりもハードディスクドライブ(HDD)市場が有利となっています。カナダとメキシコは、土地、再生可能電力、越境物流上の優位性を提供することで支援的役割を果たしています。

欧州では厳格なデータ主権規制のもと、企業向けリプレースサイクルが安定的に維持されています。ドイツと英国はコンプライアンス保持期間対応のためコールドティアクラスターを導入し、フランスは公共部門のクラウドワークロードを拡大中です。同地域の循環型経済への注力はベンダーのリサイクルプログラムと連動しており、例えばウエスタンデジタル社は2024年に廃棄ドライブ5万英ポンドから希土類元素を回収する計画です。長期的な炭素税の議論は、記録技術選択に影響を与える可能性があります。HDDメーカーは競合ストレージメディアよりもライフサイクルCO2排出量が低いことを示しています。

その他の特典

- エクセル形態の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ハイパースケールとクラウドストレージ容量に対する需要の増加

- ニアラインワークロードにおけるSSDに対するコスト/TB優位性

- スマートシティ展開に伴うビデオモニタリングデータの増加

- AI駆動型コールドデータ階層化の導入

- 大容量HAMRロードマップ(50TBドライブまで)

- 循環型経済リサイクルプログラムによる部品原価(BOM)の削減

- 市場抑制要因

- SSDの$/TBの急激な低下とエンタープライズ向けフラッシュのTCO改善

- サプライヤーの極端な集中とサプライチェーンの混乱

- エネルギー集約型HDD生産に対する見込まれる炭素税

- フラッシュベースアーキテクチャを有利にするラック密度限界

- バリュー/サプライチェーン分析

- 規制情勢

- 技術の展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済的影響評価

第5章 市場規模と成長予測

- フォームファクタ別

- 2.5インチ

- 3.5インチ

- その他(1.8インチ以下、エンタープライズJBOD)

- 用途別

- モバイル/ポータブル

- コンシューマー向けデスクトップとゲーミング

- NASとSOHO

- エンタープライズとデータセンター

- ニアライン/コールドデータ

- モニタリングとスマートシティ

- ストレージ容量別

- 1TB以下

- 1~3TB

- 3~5TB

- 5TB超

- インターフェース別

- SATA

- SAS

- PCIe/NVMe(U.2、U.3)

- エンドユーザー産業別

- IT・通信

- 家電メーカー

- クラウドとハイパースケールプロバイダ

- 産業用とビデオモニタリング

- 政府・防衛

- 記録技術別

- CMR/PMR

- SMR

- HAMRとエネルギー補助型

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他のアジア太平洋

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他の中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 中東

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Western Digital Corporation

- Toshiba Electronic Devices & Storage Corporation

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Lenovo Group Limited

- Huawei Technologies Co., Ltd.

- Transcend Information Inc.

- ADATA Technology Co., Ltd.

- Buffalo Inc.

- Nidec Corporation

- Showa Denko K.K.

- Hoya Corporation

- NetApp Inc.

- Pure Storage Inc.

- Samsung Electronics Co., Ltd.(external HDD brand)

- Micron Technology Inc.(external storage systems)

- Violin Systems LLC

- Synology Inc.

- QNAP Systems Inc.

- LaCie S.A.S.(Seagate brand)

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日