|

|

市場調査レポート

商品コード

1692532

電源ユニット(PSU)-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Power Supply Units (PSU) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電源ユニット(PSU)-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 136 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

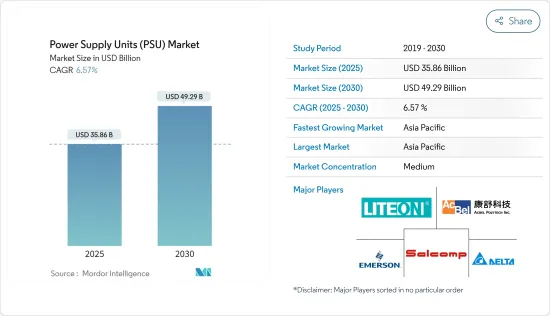

電源ユニットの市場規模は2025年に358億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.57%で、2030年には492億9,000万米ドルに達すると予測されます。

同市場は、ホームオートメーションシステムやビルオートメーションシステムの普及により大きく成長しています。民生用電子機器、医療、軍事・航空宇宙など、さまざまな産業で電源に対する需要が高く、市場に収益機会をもたらしています。

主要ハイライト

- 電源ユニットは、電力を電気負荷に供給する電気機器です。電源ユニットの主要目的は、電源からの電流を、負荷への通電に必要な適切な電圧、電流、周波数に変換することです。そのため、電源ユニットは電力変換器と呼ばれることもあります。ある種の電源ユニットは独立系ユニットであるが、他の電源ユニットは、通電する負荷機器に一体化されています。長年にわたる電源ユニット技術の進歩は、数多くの利点をもたらしてきました。洗練された回路と部品の利用により、電源ユニットはエネルギーの浪費を最小限に抑えながら、安定した電圧出力を提供することができます。

- 歴史を通じて、人類は太陽、風、水をエネルギー源として利用してきました。しかし、技術の進歩に伴い、これらの古代のエネルギー形態は先進的発電源へと進化しました。これに伴い、電力供給装置は、消費と運転のために電気負荷にエネルギーを供給する重要な役割を果たすため、年々ますます普及しています。様々な産業や産業機器における電源需要の高まりは、その需要をさらに押し上げると予想されます。

- 電源ユニットの主要目的は、電源からの電流を負荷の動作に必要な適切な電圧、電流、周波数に変換することです。この変換には、交流を直流に変換する場合と、直流を直流に変換する場合があります。その結果、電源ユニットはしばしば電力変換器と呼ばれます。電源ユニットの主要機能は、適切な量のエネルギーが負荷に供給されるよう、電力の電流と電圧をモニタリング・調整することです。電化製品に内蔵されている電源ユニットもあれば、電化製品の電気的誤動作を防ぐために別個に設置される電源ユニットもあります。

- 購入可能な電子機器の大半は、EMCとEMI(電磁両立性と電磁干渉)規制を遵守しなければならないです。これらの規制は、機器が他の機器の動作を妨げないこと、外部からの電気ノイズが認証された機器の適切な機能を妨げないことを保証するものです。直流電源ユニットは、認証を受け、規制要件に準拠する必要があります。これを怠ると、これらの電源ユニットの売上が減少する可能性があります。

- 民生用電子機器と自動車セグメントでは、電気自動車の普及が主因となって、電源ユニットの需要が顕著に増加しています。自動化技術に対する需要の高まりは、市場をさらに押し上げると予想されます。

電源ユニット(PSU)市場動向

コンシューマー・モバイルセグメントが大きな成長を遂げる

- スマートウォッチ、フィットネストラッカーなどのウェアラブルデバイスの人気が高まっており、コンパクトで効率的な電源ソリューションへの需要が高まっています。これらの機器は、バッテリ寿命を延ばし、中断のない使用を可能にするため、電力効率の高い部品を必要とし、様々な電源ユニットへの需要を牽引しています。

- AC-DC電源は、コンピューター、携帯電話(壁掛け充電器など)、テレビなど、さまざまな電子機器に幅広く使用されています。これらの電源ユニットは、多様な環境と条件下で広く採用されており、民生用電子機器製品はその顕著な実装領域です。民生用電子機器の使用拡大により、電源ユニットのニーズはさらに高まると予想されます。

- スマートフォンやタブレットデバイスは、充電のための安定した電源に依存しており、これらのガジェットが、繊細な内部部品に危害を及ぼす可能性のある変動なしに、安定したエネルギー供給を受けられるようにするために、DC電源を使用しています。これは、携帯電話のバッテリーが直流電力を蓄えるためで、交流電力に比べて蓄えやすいです。外部電源は通常交流であるため、携帯電話やその他の携帯機器を充電する前に、整流器を使用して交流を直流に変換する必要があります。市場機会の拡大が期待されるのは、このような変換機能に対する需要が高まっているためです。

- GSMAによると、アジア太平洋、ラテンアメリカ、サハラ以南のアフリカでは、スマートフォンの普及が最も進むと予想されています。スマートフォンの平均販売価格は低下しており、さまざまな取り組みが普及促進に成功しています。2030年までにスマートフォン接続数は90億に達し、総接続数の92%を占めると予測されています。インターネット普及率の上昇、スマートフォンベンダーによるマーケティング活動、ソーシャルメディアへの登録数の増加がスマートフォンの販売を後押しし、電源ユニットの大幅な需要増につながると予想されます。

大幅な成長が見込まれるアジア太平洋

- アジア太平洋は、中国、インド、韓国などの重要な国々の存在により、市場の成長という点では最大地域のひとつです。工業情報化省によると、中国は、その技術革新とブランド構築能力の強化により、民生用電子機器製品の生産と販売で世界トップの地位を確保しています。コンシューマーエレクトロニクスの生産能力を強化するための投資がこの地域で増加しており、市場は牽引力を増すと予想されます。

- 同様に、5Gネットワークの導入やモノのインターネット(IoT)などの技術的進歩も、電子製品の急速な普及を後押ししています。デジタルインド」や「スマートシティ」プロジェクトといった、電子製品産業に革命を起こそうとする取り組みが、電子機器市場におけるIoTの需要をさらに押し上げています。このような取り組みは、市場の成長を促進する要因のひとつです。

- この地域は、著名な医療機器メーカーが医療機器を生産・調達するのに理想的です。市場の成長は、定期的な医療検診の普及と医療機器技術の進歩によるものです。アジア太平洋の多くの国が医療機器市場に投資しており、AC/DCコンバータの需要を増大させる可能性が高いです。

- 例えば、インド政府によると、インドの医療機器市場は2025年までに500億米ドルに達すると予測されています。このセグメントは、投資の増加により着実な成長を遂げています。国内生産をさらに促進するため、政府はProduction Linked Incentive Schemesを導入し、医療機器に4億米ドル相当の財政的インセンティブを提供しています。その結果、短絡保護や過熱保護などの先進的保護機能を備えたAC/DCコンバータなど、医療機器の生産能力を強化するために多くの企業が多額の投資を行っています。

電源ユニット(PSU)市場概要

電源ユニット市場は、Delta Electronics Inc.、Emerson Electric Co.、LITE-ON Technology Corporation、Acbel Polytech Inc.、Salcomp PLCなどの大手企業が存在し、半固体化しています。同市場の参入企業は、製品ラインナップを強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年10月、ライトンは、最新のポートフォリオにレベル3の電気自動車(EV)用DC急速充電器を追加すると発表しました。これらのEV用充電器は、多電圧入力により既存の電気的枠組みとの調整が容易であり、顧客は余分な枠組みや設置コストを回避しながら、迅速にアイテムを導入することができます。これらの充電器は、米国の制御伝達基盤に見られるどの入力電圧設定でも、ベース制御から派生することなく調整することができます。

- 2023年7月、AcBel Polytech Inc.は、ABBの電力変換部門の株式を100%取得しました。この買収により、同社は最先端技術の創出とシステムソリューションの専門知識の拡大を目指し、多くの主要事業セグメントにおける顧客の力強い成長機会を促進します。さらに、AcBelは米国における顧客基盤の拡大、現地サービス能力の強化、世界の製造施設ネットワークの拡大を図ることができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業サプライチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場の促進要因

- ホームオートメーションとビルオートメーションシステムの採用拡大

- エネルギー効率の高いデバイスに対する需要の増加

- 市場抑制要因

- 厳しい規制コンプライアンスと安全基準

第6章 市場セグメンテーション

- デバイスタイプ別

- AC-DC電源

- DC-DCコンバータ

- エンドユーザー産業別

- 通信

- 産業用

- コンシューマー・モバイル

- 自動車

- 運輸

- 照明

- その他

- 地域別

- 南北アメリカ

- 欧州

- アジア

- オーストラリア・ニュージーランド

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Delta Electronics Inc.

- Emerson Electric Co.

- Lite-On Technology Corporation

- Acbel Polytech Inc.

- Salcomp PLC

- Mean Well Enterprises Co. Ltd

- Siemens AG

- Murata Manufacturing Co. Ltd

- TDK-Lambda Corporation(TDK Corporation)

第8章 投資分析

第9章 市場の将来

The Power Supply Units Market size is estimated at USD 35.86 billion in 2025, and is expected to reach USD 49.29 billion by 2030, at a CAGR of 6.57% during the forecast period (2025-2030).

The market has experienced significant growth due to the increasing popularity of home and building automation systems. There is a high demand for power supply in various industries, such as consumer electronics, medical & healthcare, and military & aerospace, which presents a profitable opportunity for the market.

Key Highlights

- A power supply is an electrical apparatus that delivers electric power to an electrical load. The primary objective of a power supply is to transform electric current from a source into the appropriate voltage, current, and frequency required to energize the load. Consequently, power supplies are occasionally denoted as electric power converters. Certain power supplies are independent units, whereas others are integrated into the load appliances they energize. The progressions in power supply technology throughout the years have yielded numerous benefits. Through the utilization of sophisticated circuitry and components, power supplies can furnish a steady voltage output while minimizing energy wastage.

- Throughout history, humans have been utilizing the sun, wind, and water as sources of energy. However, with the advancements in technology, these ancient energy forms have evolved into advanced power generation sources. In line with this, power supply devices become increasingly popular over the years, as they play a crucial role in providing energy to electric loads for consumption and operation. The growing demand for power supply in various industries and industrial equipment is anticipated to boost its demand further.

- The primary purpose of a power supply is to transform electric current from a source into the appropriate voltage, current, and frequency required to operate the load. This conversion may involve either changing AC to DC or DC to DC. As a result, power supplies are often referred to as electric power converters. The primary function of a power supply is to monitor and adjust the current and voltage of electrical power to ensure that the correct amount of energy is delivered to the load. While some power supplies are integrated into electrical appliances, others are installed separately to prevent any electrical malfunctions in the appliances.

- The majority of electronic devices available for purchase must adhere to EMC and EMI (electromagnetic compatibility and electromagnetic interference) regulations. These regulations ensure that the devices do not interfere with the operation of other equipment and that external electrical noise does not hinder the proper functioning of certified equipment. DC power supplies must undergo certification and comply with regulatory requirements. Failure to do so may result in declining sales of these power supplies.

- There has been a noticeable increase in demand for power supply devices in consumer electronics and automotive sectors, largely due to the growing adoption of electric vehicles. The rising demand for automation technologies is expected to propel the market further.

Power Supply Units (PSU) Market Trends

Consumer and Mobile Segment to Witness Major Growth

- The increasing popularity of wearable devices such as smartwatches, fitness trackers, and other devices is fueling demand for compact and efficient power supply solutions. These devices need power-efficient components to enhance battery life and enable uninterrupted usage, driving demand for various power supply devices.

- AC-DC power supplies are extensively used in various electronic devices such as computers, cell phones (e.g., wall chargers), and televisions. These power supplies are widely employed in diverse settings and conditions, with consumer electronics being a prominent implementation domain. The growing use of consumer electronic devices is anticipated to drive the need for power supply devices further.

- Smartphones and tablet devices rely on a stable power source for charging and use DC power supplies to ensure these gadgets receive a consistent energy supply without any fluctuations that could potentially harm their sensitive internal components. This is because cell phone batteries store DC power, which is easier to store compared to AC power. As the external power supply is typically AC, the conversion of AC to DC using a rectifier is necessary before charging cell phones or other portable devices. This expected enhancement in the market opportunities is due to the increasing demand for such conversion capabilities.

- According to GSMA, the Asia-Pacific, Latin America, and Sub-Saharan Africa are expected to experience the largest surge in smartphone adoption due to the growing affordability of these devices. The average selling prices of smartphones are decreasing, and various initiatives are proving successful in driving uptake. It is projected that by 2030, there will be 9 billion smartphone connections, which will account for 92% of total connections. The increasing Internet penetration, marketing activities by smartphone vendors, and increasing subscriptions in social media are expected to boost smartphone sales, leading to a significant increase in demand for power supplies.

Asia-Pacific Projected to Witness Significant Growth

- Asia-Pacific is one of the largest regions in terms of the growth of the market, with the presence of significant countries like China, India, South Korea, etc. According to the Ministry of Industry and Information Technology, China has secured the top position worldwide in the production and sales of consumer electronics through its enhanced innovation and brand-building capacity. With the increasing investments in the region to enhance its consumer electronics production capabilities, the market is expected to gain traction.

- Similarly, technological advancements such as the implementation of 5G networks and the Internet of Things (IoT) are propelling the rapid adoption of electronic products. Initiatives such as 'Digital India' and 'Smart City' projects, which are set to revolutionize the electronic products industry, are further boosting the demand for IoT in the electronics devices market. Such initiatives are some of the factors driving the market's growth.

- The region is ideal for prominent medical device manufacturers to produce and procure medical devices. The market's growth is attributed to the rising adoption of routine healthcare check-ups and medical device technology advancements. Many countries in Asia-Pacific are investing in the medical devices market, which is likely to augment the AC/DC converters demand.

- For instance, according to the Government of India, the Indian medical devices market is projected to reach USD 50 billion by 2025. This sector has been experiencing steady growth due to increased investments. To further promote domestic production, the government has introduced the Production Linked Incentive Schemes, offering financial incentives worth USD 400 million for medical devices. Consequently, numerous companies are making substantial investments to enhance the production capabilities of healthcare equipment, including AC/DC converters with advanced protection features like short-circuit and over-temperature protection.

Power Supply Units (PSU) Market Overview

The power supply devices market is semi-consolidated with the presence of major players like Delta Electronics Inc., Emerson Electric Co., LITE-ON Technology Corporation, Acbel Polytech Inc., and Salcomp PLC. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- October 2023: LITEON announced its latest portfolio addition, a Level 3 Electric Vehicle (EV) DC fast charger. These EV chargers effortlessly coordinate with the existing electrical framework due to their multi-voltage input, which empowers clients to rapidly introduce the item while dodging extra framework and establishment costs. These can be coordinates in any input voltage setup found in the US control conveyance foundation without deriving from the base control obtained.

- July 2023: AcBel Polytech Inc. acquired a 100% stake in ABB Ltd's Power Conversion division. Through this acquisition, the company aims to create cutting-edge technology and expand its expertise in system solutions designed to fuel strong growth opportunities for customers in many of its core business sectors. Moreover, it will allow AcBel to grow its customer base in the United States, strengthen its local service capabilities, and extend its network of global manufacturing facilities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Supply Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Home and Building Automation Systems

- 5.1.2 Increasing Demand for Energy-efficient Devices

- 5.2 Market Restraints

- 5.2.1 Stringent Regulatory Compliance and Safety Standards

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 AC-DC Power Supplies

- 6.1.2 DC-DC Converters

- 6.2 By End-user Industry

- 6.2.1 Communication

- 6.2.2 Industrial

- 6.2.3 Consumer and Mobile

- 6.2.4 Automotive

- 6.2.5 Transportation

- 6.2.6 Lighting

- 6.2.7 Other End-user Industries

- 6.3 By Geography

- 6.3.1 Americas

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Delta Electronics Inc.

- 7.1.2 Emerson Electric Co.

- 7.1.3 Lite-On Technology Corporation

- 7.1.4 Acbel Polytech Inc.

- 7.1.5 Salcomp PLC

- 7.1.6 Mean Well Enterprises Co. Ltd

- 7.1.7 Siemens AG

- 7.1.8 Murata Manufacturing Co. Ltd

- 7.1.9 TDK-Lambda Corporation (TDK Corporation)