|

市場調査レポート

商品コード

1690923

ソリッドグレード熱可塑性アクリル(ビーズ)樹脂:市場シェア分析、産業動向、成長予測(2025~2030年)Solid-grade Thermoplastic Acrylic (Beads) Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ソリッドグレード熱可塑性アクリル(ビーズ)樹脂:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

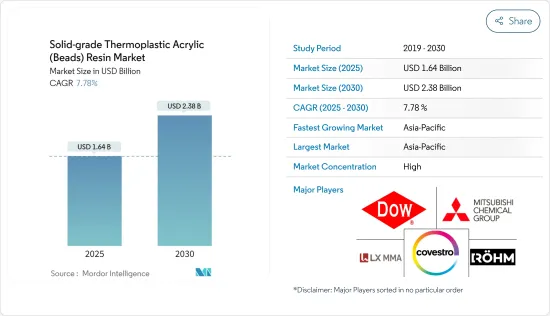

ソリッドグレード熱可塑性アクリル樹脂市場規模は2025年に16億4,000万米ドルと推定され、2030年には23億8,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは7.78%です。

COVID-19パンデミックは、サプライチェーンの混乱と様々な製造業や建設活動の閉鎖につながった全国的なロックダウンと社会的距離の義務化により、2020年の市場にマイナスの影響を与えました。しかし、規制が解除されてからは順調に回復しています。内装・外装用途におけるさまざまなセクタからの塗料・コーティング需要の増加は、調査対象市場にプラスの影響を与えると予想されます。

主要ハイライト

- 短期的には、塗料・コーティング産業の拡大と、ソリッドグレード熱可塑性アクリル(ビーズ)樹脂が提供するさまざまな利点が市場需要を牽引する要因のひとつです。

- 逆に、原料に関する政府の厳しい規制は市場の成長を妨げます。

- 電気自動車産業の拡大は、今後数年間で市場に機会をもたらすと考えられます。

- アジア太平洋が市場を独占し、予測期間中に最も高いCAGRで推移すると見られています。

ソリッドグレード熱可塑性アクリル(ビーズ)樹脂の市場動向

塗料・コーティング産業における用途の増加

- ソリッドグレード熱可塑性アクリル(ビーズ)樹脂は、塗料やコーティング剤の配合に広く使用されています。さらに、これらの樹脂は主に塗料・コーティングセグメントの工業用塗料、建築用塗料、輸送用塗料、コイル塗料に使用されています。

- ソリッドグレード熱可塑性アクリル(ビーズ)樹脂は、塗料やコーティングの強力なバインダーです。これらの樹脂は有機溶剤やUVモノマーに容易に溶解します。また、キシレン、エステル、ケトンにも溶ける。

- これらの樹脂は、金属、プラスチック、セメント系など複数の基材に接着します。さらに、耐久性に優れ、光沢があり、耐アルカリ性に優れ、速乾性があり、幅広い基材に容易に接着します。ソリッドグレード熱可塑性アクリル樹脂は、木材塗料や電子塗料などにも使用されています。

- Coating Worldの報告書によると、すべての国からの各種塗料の輸出額を合計すると、2020年の216億米ドルに対し、2021年には249億米ドルに達します。年の顕著な増加も示しています。さらに、世界の塗料・コーティング市場は、2022年には約1,980億米ドルとなりました。

- Coating Worldの報告書によると、塗料・コーティング産業にとって、アジアは世界市場シェアの45%近くを占める最大地域であり、次いで北米のシェア23%、ラテンアメリカシェア7%、中東・アフリカのシェア6%となっています。

- アジア太平洋の継続的な経済力と、それに対応するインフラ、機械、製造装置などへのニーズの高まりが、同地域における塗料とコーティング剤の需要を促進すると考えられます。また、鉄鋼、化学、石油・ガス、製造、建設などのエンドユーザー産業では、生産設備の拡大や投資の増加が新たなビジネス機会につながると考えられます。

- 米国コーティング協会の報告書によると、2022年の米国における建築用コーティングの市場規模は約159億米ドルでした。2023年末には170億米ドル以上に達すると考えられます。

- カナダには約260社の塗料・塗装メーカーがあります。カナダ国内の塗料・塗装製造業は米国より少なく、年間GDPに占める割合は0.5%以下です。

- 欧州には多くの大規模な塗料産業があり、ドイツ、フランス、イタリア、スペインを含む4大主要経済圏があります。この地域には老舗企業が複数存在するため、予測期間中、塗料・コーティングセグメントは拡大すると予測されます。ドイツは欧州における塗料・コーティングの主要生産国のひとつです。Haltermann Carlessによると、同国は年間約260万トンの塗料・コーティング剤を生産しており、自動車、建築、一般産業、腐食防止など様々な用途で使用されています。

- 中東・アフリカでは構造改革が進んでいるため、工業用塗料の需要が旺盛になると予想されます。また、サウジアラビアでは、ビジョン2030の発表とそれに伴う国家変革計画(NTP)により、医療や教育など様々なセグメントへの投資が増加しました。

- こうしたあらゆる要因から、ソリッドグレード熱可塑性アクリル(ビーズ)樹脂市場は予測期間中に安定した成長が見込まれます。

市場を独占するアジア太平洋

- アジア太平洋が市場を独占すると予想されます。この地域では、中国がGDPで最大の経済大国です。中国とインドは、世界で最も急速に成長している新興国のひとつです。

- Coatings Worldの報告書によると、アジア太平洋は2022年も世界の塗料・コーティング産業で最も活気のある地域です。これは、好調な経済成長と良好な人口動向により、この地域が長年にわたり世界で最も急成長している塗料・コーティング市場になったためです。

- アジア太平洋は、可処分所得の増加と相まって中流階級の人口増加が見込まれています。それがこの地域の住宅セクタの拡大を促進しました。そのため、建設産業の市場開拓により、建築用塗料市場として最も重要な位置を占めています。

- さらに、アジア太平洋は世界で最も急速に成長している地域であり、新たに工業化する国も増えています。このような産業成長はエネルギーインフラの需要を煽り、その需要も増大し、塗料やコーティングの必要性を高めています。しかし、COVID-19パンデミックによる閉鎖のため、アジア太平洋の塗料・コーティング市場の成長は一様ではなく、その結果、需要に大きな振れが生じています。

- さらに、アジア太平洋におけるソリッドグレード熱可塑性アクリル(ビーズ)樹脂の消費水準は、輸送、建築、建築・建設、エレクトロニクス、石油・ガス、太陽光発電、その他の産業部門からのアクリル複合材料、塗料、コーティングの需要増加により、今後数年間でかなりの割合で上昇すると予想されます。

- アジアは最大の地域であり、世界市場シェアの45%近くを占め、2022年には900億米ドルに達します。アジアの中で最大の小地域は中華圏で、アジアの塗料・コーティング市場のほぼ58%を占めています。

- European Coatingsによると、1万社近くの塗料メーカーが中国に進出しています。日本ペイント、アクゾノーベル、中国海洋塗料、PPGインダストリーズ、BASF SE、アクサルタ・コーティングスなど、世界の大手塗料メーカーのほとんどが中国に製造拠点を置いています。塗料・コーティング企業は、同国への投資をますます増やしています。

- 2022年、インドの塗料産業は6,200億インドルピー(80億米ドル)以上と評価されました。過去20年間、2桁台の安定した成長を続けており、世界的に最も急成長している塗料経済です。国内には3,000社以上の塗料メーカーがあり、ほぼすべての世界企業が進出しています。建築用塗料は市場全体の約75%を占め、工業用塗料は25%のシェアを占めています。

- Coatings Worldによれば、タイは最も活気のある塗料・コーティング市場のひとつです。タイの塗料・コーティング市場は高度に統合されており、上位4社(TOA Paint(Thailand)Public Company Limited、Akzo Nobel Paints(Thailand)Company Limited、Jotun Thailand Limited、Berger)が市場シェアの75%以上を占めています。

- 経済産業省によると、2021年の日本の合成樹脂塗料の生産量は約101万トンで、塗料の生産量は莫大です。塗料全体の生産量は、2020年の150万トンに対し、2021年には約153万トンに増加しました。

- 韓国の塗料・塗装市場はアジア太平洋で4番目に大きいです。KCC、Samhwa Paints、Kangnam Jevisco(旧Kunsul Chemical Industrial Company、通称KCI)、Noroo Paints、Chokwang Paintsが主要な塗料・コーティングメーカーです。彼らは韓国の塗料・コーティング市場を約75%の累積市場シェアで支配しており、産業におけるアクリル酸の使用量を高めています。

- さらに、約80の大・中・小規模の塗料・コーティングメーカーが存在するマレーシアの塗料・コーティング産業は、東南アジア地域で最も先進的な製品の一つです。

- オーストラリア塗料工業連合会(APMF)は、同国の塗料・コーティング産業の機能をモニタリングする公式団体です。国内には220社以上の塗料メーカーがあります。主要企業には、Dulux Group、PPG Industries、Sherwin-Williams、Akzo Nobel、Axalta、Haymes Paintsなどがあります。

- このように、上記の要因は予測期間中、アジア太平洋におけるソリッドグレード熱可塑性樹脂(ビーズ)の需要を促進すると予想されます。

ソリッドグレード熱可塑性アクリル(ビーズ)樹脂産業概要

ソリッドグレード熱可塑性アクリル(ビーズ)樹脂市場は、その性質上、統合されています。市場の主要企業には、Covestro AG、Dow、Mitsubishi Chemical Corporation、LX MMA、Rohm GmbHなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 塗料・コーティング産業の拡大

- ソリッドグレード熱可塑性アクリル(ビーズ)樹脂の利点

- 抑制要因

- 原料に関連する厳しい政府規制

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 用途

- アクリル複合樹脂

- 塗料とコーティング

- コイルコーティング

- 工業用塗料

- 建築塗料

- 輸送用塗料

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- その他

- 南米

- 中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Chansieh Enterprises Co. Ltd.

- Covestro AG

- Dow

- Heyo Enterprises Co. Ltd.

- LX MMA

- Makevale Group

- Mitsubishi Chemical Corporation

- Pioneer Chemicals Co. Ltd.

- Polyols & Polymers Pvt. Ltd.

- Rohm Gmbh

- Suzhou Direction Chemical Co. Ltd.

- Trinseo

第7章 市場機会と今後の動向

- 電気自動車産業の拡大

The Solid-grade Thermoplastic Acrylic Resin Market size is estimated at USD 1.64 billion in 2025, and is expected to reach USD 2.38 billion by 2030, at a CAGR of 7.78% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market in 2020 due to nationwide lockdowns and social distancing mandates which led to supply chain disruption and the closure of various manufacturing industries and construction activities. However, the sector is recovering well since restrictions were lifted. Increasing demand for paints and coatings from different sectors in interior and exterior applications is expected to impact the studied market positively.

Key Highlights

- Over the short term, the expansion of the paint and coatings industry and the various benefits offered by solid-grade thermoplastic acrylic (beads) resins are some of the factors driving the market demand.

- Conversely, stringent government regulations regarding raw materials hinder the market's growth.

- Expansion of the electric vehicle industry is likely to create opportunities for the market in the coming years.

- The Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Solid-grade Thermoplastic Acrylic (Beads) Resin Market Trends

Increasing Usage in the Paints and Coatings Industry

- Solid-grade thermoplastic acrylic (beads) resins are widely used in the formulation of paints and coatings. Furthermore, these resins are used primarily in industrial, architectural, transportation, and coil coatings in the paints and coatings segment.

- Solid-grade thermoplastic acrylic (beads) resins are a strong binder for paints and coatings. These resins can be easily dissolved in organic solvents or UV monomers. They are also soluble in xylene, esters, and ketones.

- These resins offer adhesion to multiple substrates such as metal, plastics, and cementitious. Furthermore, they are durable, have a high gloss, offer good alkali resistance, are fast drying, and easily adhere to a broad substrate range. Solid-grade thermoplastic acrylic resins are also used in wood coatings, electronic coatings, and others.

- According to the Coating World report, the combined exports of various types of paint from all countries amounted to around USD 24.9 billion in 2021, compared to USD 21.6 billion in 2020. It also indicates a notable increase in years. Furthermore, the global paints and coatings market stood at around USD 198 billion in 2022.

- For the paints and coatings industry, Asia is the largest region, with nearly 45% of the global market share, followed by Europe with a 23% share, North America with a 19% share, Latin America with a 7% share, and the Middle East and Africa with a 6% share, as per the Coating World report.

- Asia-Pacific region's continuing economic strength and corresponding increasing need for infrastructure, machinery, manufacturing units, and others are likely to propel the demand for paints and coatings in the region. In addition, expanding production units and increasing investments in the area will likely offer newer opportunities in the end-user industries such as iron and steel, chemical, oil and gas, manufacturing, construction, and others.

- According to the report of the American Coatings Association, in 2022, the market value of architectural coatings in the United States was around USD 15.9 billion. It will likely reach more than USD 17 billion by the end of 2023.

- Canada includes around 260 paint and coating manufacturers. Canada's domestic paint and coating manufacturing industries are fewer than the United States and contribute less than 0.5% to its annual GDP.

- Europe is home to many large paint industries, with the four largest mainland economies, including Germany, France, Italy, and Spain. The presence of several well-established players in the region is projected to expand the paints and coatings segment over the forecast period. Germany is among the leading producers of paints and coatings in Europe. According to Haltermann Carless, the country produces approximately 2.6 million tons of paints and coatings annually, used in various applications such as automotive, architectural, general industry, corrosion protection, and others.

- Due to the region's increasing structural reforms, the Middle East and African regions are anticipated to witness strong demand for industrial coatings. In addition, the announcement of Vision 2030, coupled with the associated National Transformation Plan (NTP), increased investments in various sectors, including healthcare and education in Saudi Arabia.

- Due to all such factors, the market for solid-grade thermoplastic acrylic (beads) resins is expected to grow steadily during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the market. In the area, China is the largest economy in terms of GDP. China and India are among the fastest emerging economies in the world.

- As per the report by Coatings World, the Asia-Pacific region continued to be the most dynamic in the paint and coatings industry worldwide in 2022. It happened to owe to strong economic growth coupled with favorable demographic trends that have made this region the fastest-growing paint and coatings market across the globe for many years.

- The Asia-Pacific region is anticipated to witness an increasing middle-class population coupled with rising disposable income. It facilitated the expansion of the residential sector in the area. Hence, it is the most significant architectural coatings market due to the construction industry's development.

- In addition, Asia-Pacific is the fastest-growing region in the world, with more and more countries becoming newly industrialized. This industrial growth is fuelling the demand for energy infrastructure, which is also multiplying, driving the need for paints and coatings. However, due to COVID-19 pandemic-induced lockdowns, the paints and coatings market growth in the Asia-Pacific region was uneven, resulting in large swings in demand.

- Moreover, the consumption levels of solid-grade thermoplastic acrylic (beads) resins in the Asia-Pacific region are expected to rise at a significant rate in the coming years, owing to the increasing demand for acrylic composites, paints, and coatings from the transportation, architectural, building, and construction, electronics, oil and gas, solar power, and other industrial sectors.

- Asia is the largest region, with nearly 45% of the global market share, amounting to USD 90 billion in 2022. Within Asia, the largest sub-region is Greater China which accounts for almost 58% of the Asian paint and coatings market.

- According to European Coatings, nearly 10,000 coatings manufacturers are located in China. Most leading global coating manufacturers, such as Nippon Paint, AkzoNobel, Chugoku Marine Paints, PPG Industries, BASF SE, and Axalta Coatings, have manufacturing bases in China. Paints and coatings companies have been increasingly growing investments in the country.

- In 2022, the Indian Paint Industry was valued at over INR 62,000 crores (USD 8 billion). It is the fastest-growing paint economy globally, with stable double-digit growth over the last two decades. The country includes over 3,000 paint manufacturers, with nearly all global companies present. Architectural paints constitute around 75% of the overall market, and industrial paints take a 25% share.

- As per the Coatings World, Thailand is one of the most vibrant paints and coatings markets. Thailand's paints and coatings market is highly consolidated in nature, with the top four players [TOA Paint (Thailand) Public Company Limited, Akzo Nobel Paints (Thailand) Company Limited, Jotun Thailand Limited, and Berger Co. Ltd] accounting for more than 75% of market share.

- According to the Ministry of Economy, Trade, and Industry (Japan), the production volume of synthetic resin paints in Japan amounted to approximately 1.01 million metric tons in 2021, making up an enormous production volume of paints. Overall, paints' production volume increased to nearly 1.53 million metric tons in 2021, compared to 1.50 million metric tons in 2020.

- The South Korean paint and coating market is the fourth-largest in the Asia-Pacific region. KCC, Samhwa Paints, Kangnam Jevisco (formerly Kunsul Chemical Industrial Company, popularly called KCI), Noroo Paints, and Chokwang Paints are the primary paint and coating producers. They dominate the South Korean paints and coating market with a cumulative market share of approximately 75%, enhancing acrylic acid usage in the industry.

- Furthermore, catered by about 80 large, mid-sized, and small-scale paint and coatings producers, the Malaysian paints and coatings industry is one of the most advanced product offerings in the Southeast Asian region.

- The Australian Paint Manufacturers' Federation Inc. (APMF) is the official association that monitors the functioning of the paints and coatings industry in the country. There were more than 220 manufacturers of paints and coatings in the country. The major companies include Dulux Group, PPG Industries, Sherwin-Williams, Akzo Nobel, Axalta, and Haymes Paints.

- Thus, the above factors are expected to propel the demand for solid-grade thermoplastic resins (beads) in the Asia-Pacific region during the forecasted period.

Solid-grade Thermoplastic Acrylic (Beads) Resin Industry Overview

The solid-grade thermoplastic acrylic (beads) resin market is consolidated in nature. Some of the major players in the market include Covestro AG, Dow, Mitsubishi Chemical Corporation, LX MMA, and Rohm GmbH, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Expansion of the Paints and Coatings Industry

- 4.1.2 Benefits of Solid-grade Thermoplastic Acrylic (beads) Resins

- 4.2 Restraints

- 4.2.1 Stringent Government Regulations Related to Raw Materials

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Acrylic Composite Resins

- 5.1.2 Paints and Coatings

- 5.1.2.1 Coil Coatings

- 5.1.2.2 Industrial Coatings

- 5.1.2.3 Architectural Coatings

- 5.1.2.4 Transportation Coatings

- 5.1.3 Other Applications

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 Rest of the World

- 5.2.4.1 South America

- 5.2.4.2 Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chansieh Enterprises Co. Ltd.

- 6.4.2 Covestro AG

- 6.4.3 Dow

- 6.4.4 Heyo Enterprises Co. Ltd.

- 6.4.5 LX MMA

- 6.4.6 Makevale Group

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 Pioneer Chemicals Co. Ltd.

- 6.4.9 Polyols & Polymers Pvt. Ltd.

- 6.4.10 Rohm Gmbh

- 6.4.11 Suzhou Direction Chemical Co. Ltd.

- 6.4.12 Trinseo

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion of the Electric Vehicle Industry